Choosing between a secured vs unsecured credit card can be a pivotal decision for your financial future.

At Financial Canadian, we understand the importance of making informed choices when it comes to credit cards.

This guide will break down the key differences between these two types of cards, helping you determine which option aligns best with your financial goals and current situation.

What Are Secured Credit Cards?

Definition and Purpose

Secured credit cards serve as financial tools for individuals who want to build or rebuild their credit. These cards require a cash deposit, which typically becomes the credit limit. For example, a $500 deposit usually results in a $500 credit limit.

How Secured Credit Cards Function

When you apply for a secured credit card, you must provide a security deposit. This deposit acts as collateral, which reduces the risk for the card issuer. The Bank of Montreal offers a secured credit card with a minimum deposit of $500 (a fairly standard amount in the industry).

You use a secured credit card like any other credit card. You make purchases and must pay the balance. The main difference lies in the fact that if you default on your payments, the issuer can keep your deposit.

Credit-Building Potential

Secured credit cards excel as tools for building credit. They report to major credit bureaus like Equifax and TransUnion, just as unsecured cards do. This means that responsible use can improve your credit score over time.

A survey found that among new Canadians who have applied for credit, 59% agree they would have a more positive living experience in Canada with better access to credit.

Considerations and Drawbacks

While secured credit cards offer a path to better credit, they come with some drawbacks. Annual fees are common (often ranging from $20 to $50). Interest rates tend to be high, with some cards charging over 20% APR.

Moreover, credit limits on secured cards are typically low. This can result in high credit utilization if you’re not careful, which may negatively impact your credit score. The Canadian Bankers Association recommends you keep your credit utilization below 30% for optimal credit health.

Transitioning to Unsecured Cards

As you build your credit with a secured card, you may become eligible for an unsecured credit card. Many issuers review accounts periodically and may offer to return your deposit and convert your account to an unsecured card. This transition marks a significant milestone in your credit journey and leads us to explore unsecured credit cards in more detail.

What Are Unsecured Credit Cards?

Unsecured credit cards are financial products that don’t require a security deposit. These cards extend credit based on your creditworthiness, income, and other financial factors.

Key Differences from Secured Cards

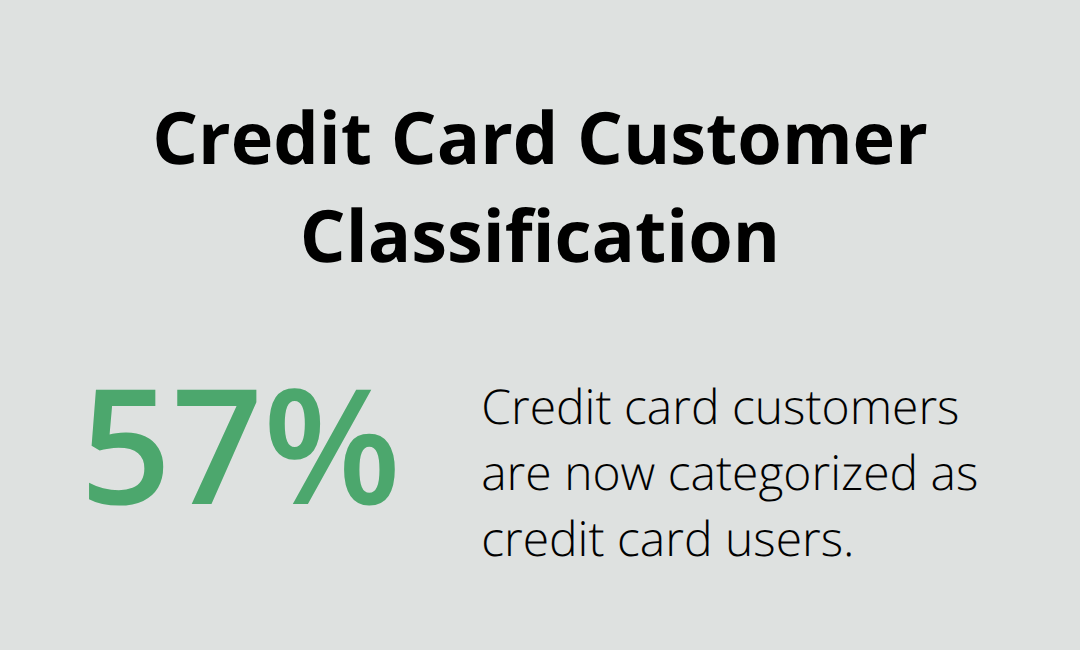

The main distinction between unsecured and secured cards is the absence of collateral. Unsecured card issuers take on more risk, which results in stricter approval criteria. According to the J.D. Power 2024 Canada Credit Card Satisfaction Study, 57% of credit card customers are now categorized as credit card users.

Qualification Requirements

To qualify for an unsecured card, you typically need a fair to good credit score. Most Canadian issuers look for scores above 660, though some may approve applicants with scores as low as 600. The application process involves a hard credit check, which can temporarily lower your credit score by a few points.

Income requirements vary, but many issuers expect annual earnings of at least $12,000 to $15,000. Some premium cards may require significantly higher incomes (for example, the BMO World Elite Mastercard requires a minimum annual income of $80,000 individual or $150,000 household).

Benefits and Rewards

Unsecured cards often come with higher credit limits, which can help keep your credit utilization ratio low.

Rewards programs are another significant advantage. Many unsecured cards offer cash back, travel points, or other perks. For instance, some cards offer up to 4% cash back on eligible purchases.

Potential Risks

While unsecured cards offer numerous benefits, they also come with risks. Interest rates are often high, with the average Canadian credit card APR hovering around 19.99% as of 2025. Some cards for those with lower credit scores may charge rates up to 29.99%.

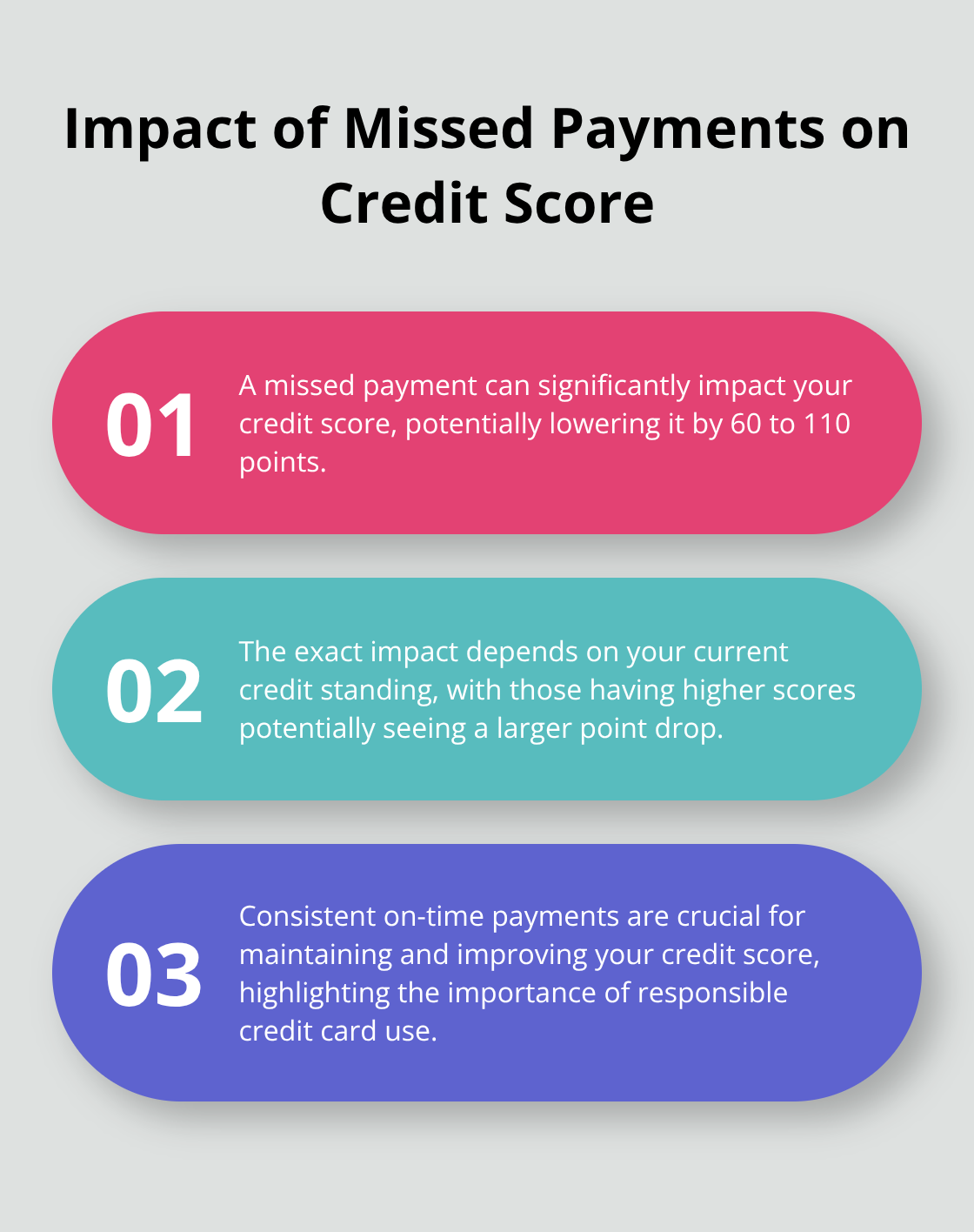

Late payments can result in hefty fees and damage to your credit score. A missed payment can lower your score by 60 to 110 points, depending on your current credit standing.

We always recommend paying your balance in full each month to avoid interest charges. If you can’t pay in full, try to pay more than the minimum to reduce interest costs and pay off your balance faster.

As we move forward to compare secured and unsecured credit cards, it’s important to weigh these benefits and risks against your personal financial situation and goals.

How Do Secured and Unsecured Cards Stack Up?

Credit Score Requirements

Secured cards offer more leniency for credit scores. Many issuers don’t require a credit check. You must be a Canadian citizen or resident and be the age of majority (18 or 19, depending on your province) to apply for a credit card. Unsecured cards typically require at least a fair credit score.

Interest Rates and Fees

Both card types often carry high interest rates. Secured cards from major banks like RBC and TD typically have APRs around 19.99% for purchases. Unsecured cards for those with fair credit might have slightly higher rates, sometimes reaching 22.99%.

Annual fees vary widely. Many secured cards charge $0-$50 annually. The Capital One Guaranteed Secured Mastercard has no annual fee (making it an attractive option). Unsecured cards have a broader range, from no-fee options to premium cards with fees over $100.

Approval Odds and Accessibility

Secured cards offer near-guaranteed approval if you can provide the security deposit. This makes them highly accessible for those with poor or no credit.

Unsecured cards present more challenges. Approval odds increase with better credit scores and higher income. The Tangerine Money-Back Credit Card, while unsecured, has more flexible requirements and is often recommended for those new to credit.

Credit Limit Potential

Secured cards typically start with low limits, often equal to your deposit. Some issuers allow deposits up to $10,000, but this is uncommon. Limit increases usually require additional deposits.

Unsecured cards offer more flexibility. Starting limits can range from $500 to several thousand dollars. Many issuers review accounts periodically for automatic limit increases.

Impact on Credit Scores

Both card types can significantly improve your credit score when used responsibly. Issuers of secured credit cards typically report payment activity to the credit bureaus. So, when used responsibly, a secured card can help you build your credit.

Unsecured cards, while equally effective at building credit, suit those who already have a fair credit score and want to improve it further. The Scotia Momentum No-Fee Visa Card not only helps build credit but also offers cash back rewards, which provides additional benefits as you improve your financial standing.

Final Thoughts

Your choice between a secured vs unsecured credit card depends on your financial situation and goals. Secured cards provide a path to credit building for those with limited or poor credit history, requiring a deposit as collateral. Unsecured cards don’t require a deposit but typically need a fair to good credit score for approval, often offering higher credit limits and more attractive rewards programs.

Consider your current credit score, financial stability, and long-term objectives when deciding. If you’re new to credit or rebuilding after setbacks, a secured card might be your best starting point. For those with fair to good credit, an unsecured card might be more suitable (providing higher credit limits and robust rewards programs).

We at Financial Canadian understand the importance of making informed financial decisions. Our expert web design services can help you create a strong online presence to share your financial journey. Whether you’re a financial advisor or passionate about personal finance, our tailored web solutions can help you reach and engage your audience effectively.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment