Debt can feel overwhelming, especially when you’re unsure where to turn for help. At Financial Canadian, we’ve created this guide to connect you with real debt help services in Canada that actually work.

Whether you’re drowning in credit card balances or facing more serious financial trouble, you need to know which providers are legitimate and which ones to avoid. We’ll walk you through your options so you can make a confident choice.

What Debt Help Services Actually Work in Canada

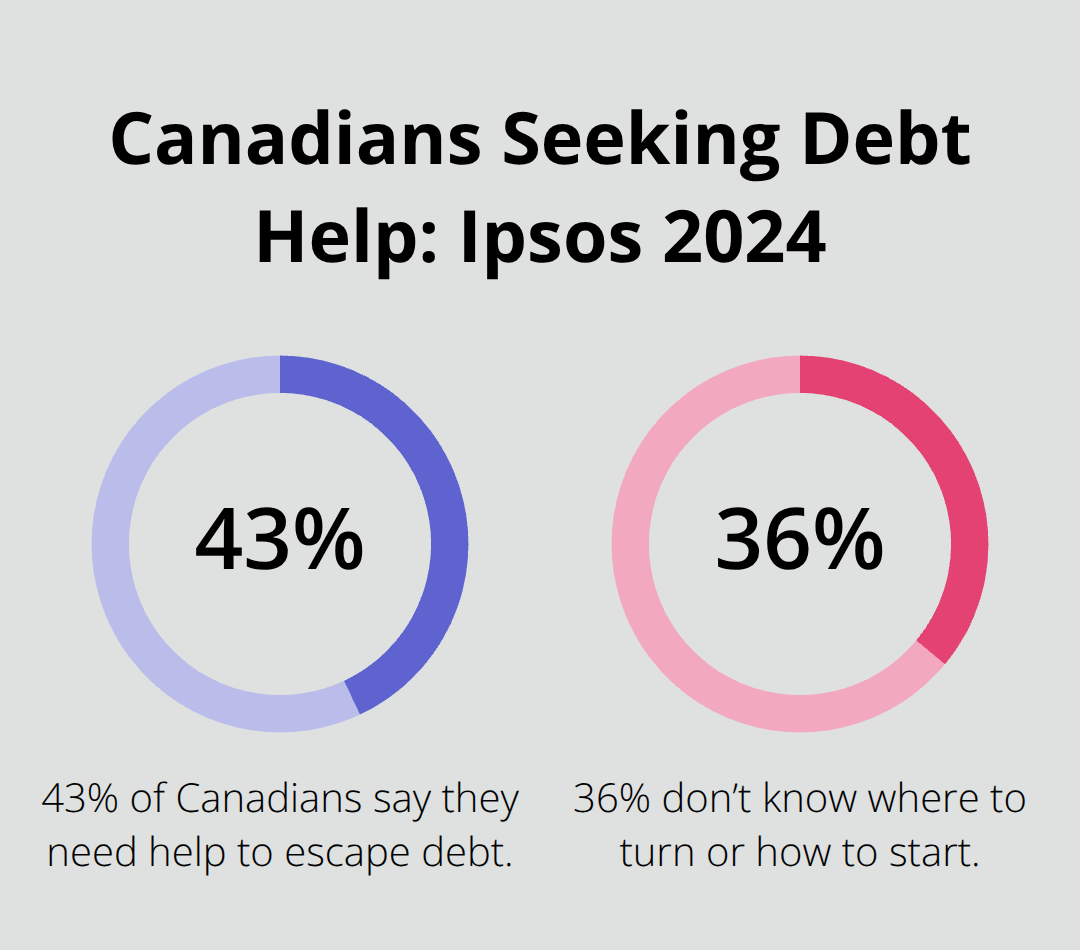

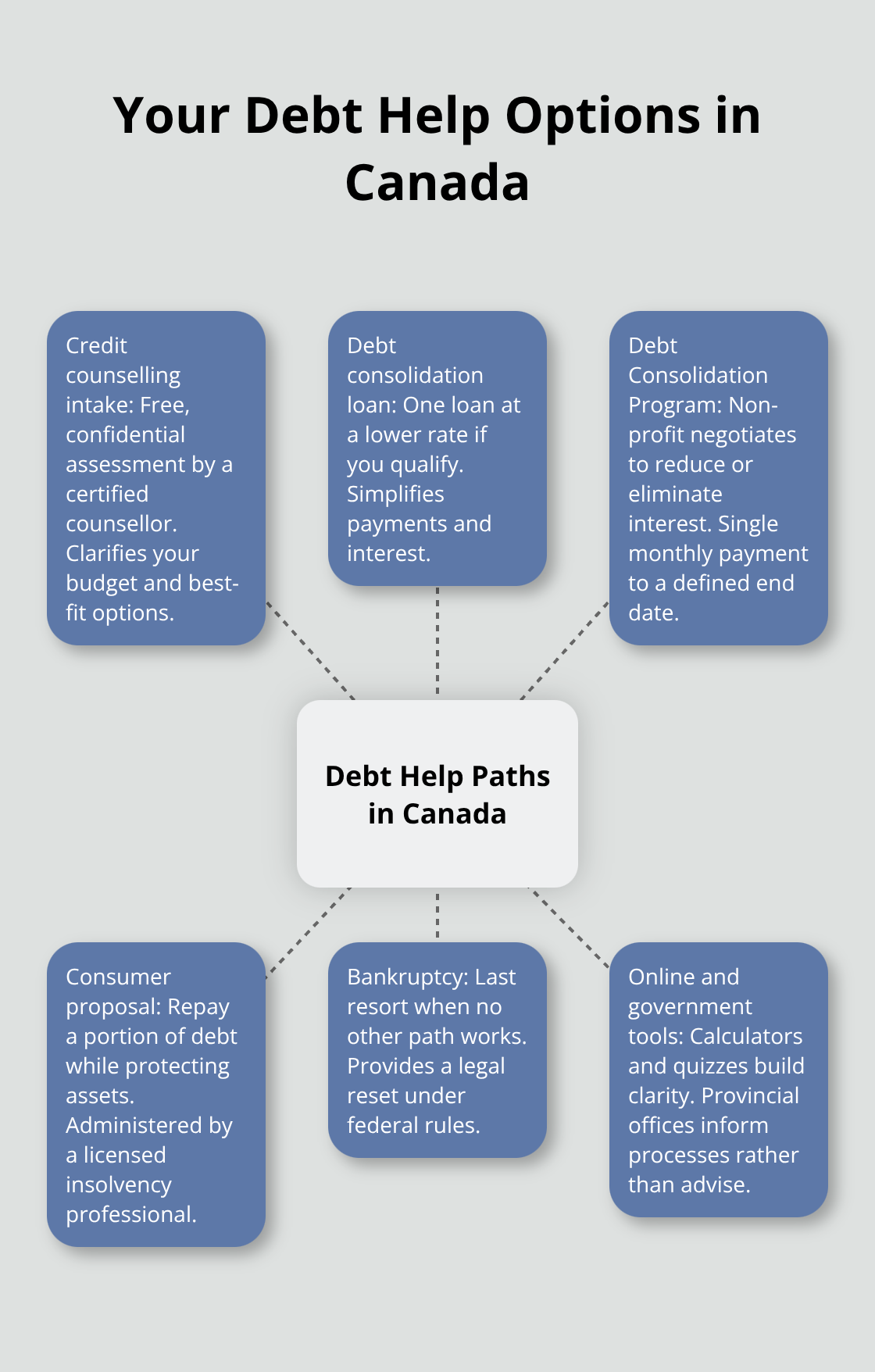

Credit counselling stands out as the most practical first step for anyone struggling with debt. According to an Ipsos poll conducted in December 2024 for MNP LTD, 43% of Canadians say they need help to escape debt, yet 36% don’t know where to turn or how to start. A certified credit counsellor will assess your income, expenses, debts, and assets during a free, confidential intake session and then recommend the path that fits your situation. Credit Canada, Canada’s first and longest-standing non-profit credit counselling agency with over 60 years of experience, offers these sessions at no cost.

The counsellor won’t judge your situation-they’ve seen it all, and their job is to find what actually works for your circumstances, not push you toward an expensive solution.

Debt consolidation when you’re ready to act

If you have unsecured debt spread across multiple creditors, two consolidation options exist. A debt consolidation loan works if you have decent credit and can secure a lower interest rate than what you’re currently paying across all your debts combined. However, the real advantage goes to those with poor or fair credit who qualify for a Debt Consolidation Program, a non-profit arrangement where counsellors negotiate directly with your creditors to reduce or eliminate interest charges. You then make a single monthly payment toward a defined end date. The Ipsos data shows 26% of Canadians paid only the minimum on their credit cards in the past year, and 20% went deeper into credit card debt-consolidation stops this cycle by locking in one affordable payment. Women are more likely than men to fall into this trap, with 29% paying minimums compared to 22% of men. If consolidation isn’t right for your situation, a consumer proposal lets you repay a portion of your debt and avoid bankruptcy while keeping your assets intact.

Bankruptcy as a last resort with clear eyes

Bankruptcy should never be your first option, but it’s worth understanding when it becomes necessary. The stigma is real-40% of Canadians believe there’s shame around bankruptcy that prevents people from seeking help, and 48% would feel embarrassed if bankruptcy entered the conversation. However, 80% of Canadians agree there is no shame in seeking financial help with debt generally. The truth is that bankruptcy exists precisely for situations where no other path works, and a certified insolvency counsellor can walk you through whether it’s actually your best option or whether a consumer proposal or debt consolidation program would serve you better. Don’t let fear or stigma keep you stuck in a worse financial position.

The next step involves identifying which providers actually merit your trust-and which ones exploit your desperation.

Spotting Real Debt Help vs. Predatory Scams

The debt relief industry in Canada has a trust problem. According to the Ipsos poll from December 2024, 63% of Canadians fear debt-relief scams when seeking help, and 53% have difficulty trusting professional debt-help companies. Your skepticism is justified. The market attracts both legitimate non-profit counsellors and profit-driven operators who prey on desperation. The difference between them matters enormously for your financial future.

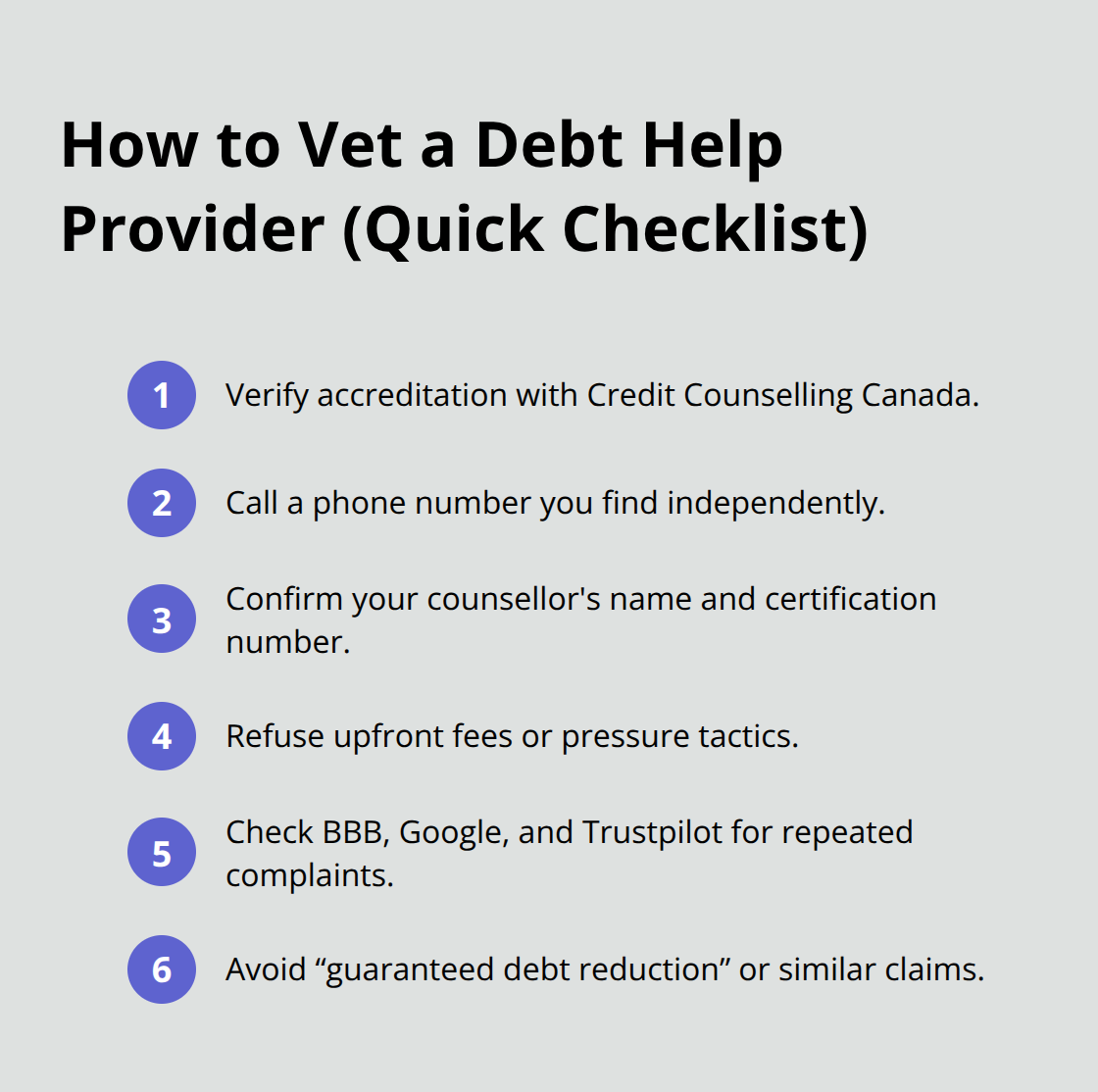

Verify accreditation through the right channels

Start by checking accreditation through Credit Counselling Canada, the only legitimate industry body that vets and certifies advisors across the country. If a provider won’t display this credential or can’t provide a verification number, walk away immediately. Credit Canada, Canada’s first and longest-standing non-profit credit counselling agency with over 60 years of experience, holds this accreditation and an A+ Better Business Bureau rating with consistent 5-star Google and Trustpilot reviews. This is the standard you should expect. Non-profit status matters too because it means the organization legally cannot prioritize profit over your outcome. For-profit debt settlement companies often push you toward expensive programs that benefit them, not you.

Confirm credentials before you sign anything

Never sign paperwork with any debt provider until you confirm they’re registered with Credit Counselling Canada. Call the organization directly using a phone number you find independently, not one they provide. Ask for the name of your assigned counsellor and their certification number. Legitimate counsellors will never pressure you into quick decisions or demand upfront fees for assessment. Credit Canada’s intake process is entirely free and confidential, setting the benchmark for how trustworthy providers operate.

Check their reviews on Google, Trustpilot, and the Better Business Bureau specifically for patterns. A few negative reviews are normal, but watch for repeated complaints about hidden fees, pressure tactics, or false promises about debt elimination. If you see language like “guaranteed debt reduction” or “bankruptcy avoidance with no assessment,” that’s a red flag. Real counsellors will tell you upfront that outcomes depend on your specific situation, income, and creditor cooperation.

Understand what legitimate programs actually cost

The most important rule: legitimate credit counselling and debt assessment cost nothing. If someone charges you for an initial consultation, they’re not operating in your interest. Debt consolidation programs through non-profit agencies involve creditor negotiations that are free to you as the client. The agency may receive nominal payments from creditors as part of the settlement, but this never comes from your pocket as a separate fee.

A debt consolidation loan from a bank or credit union has interest costs, yes, but these are transparent and disclosed upfront. Compare the total interest you’d pay on the loan against what you’re currently paying across multiple debts. If the loan rate is higher than your combined current rates, reject it. For consumer proposals, you’ll repay a negotiated portion of your debt over a defined period, but again, this is transparent before you commit.

Avoid red flags in fee structures

Steer clear of any provider who quotes vague fees, mentions success payments, or suggests they’ll negotiate with creditors for a percentage of what you save. These structures create perverse incentives where the provider benefits from keeping you in debt longer. Legitimate organizations operate with clear, upfront pricing that aligns their success with yours, not against it.

The providers worth your trust share one trait: they make money only when you actually move forward with a real solution, not by stringing you along with false hope. Once you’ve identified a trustworthy provider, the next step involves understanding exactly what each debt solution will cost you and how long it will take to reach freedom.

Where to Find Reliable Debt Help Right Now

Start with Credit Canada’s free assessment

Credit Canada stands as the most straightforward entry point for Canadians seeking legitimate support. With over 60 years of experience as Canada’s first and longest-standing non-profit credit counselling agency, they offer completely free intake assessments where a certified counsellor reviews your income, expenses, debts, and assets in a confidential setting. This matters because Ipsos poll data shows Canadians are more cautious about taking on new debt, yet many don’t know where to turn or how to start. Credit Canada’s A+ Better Business Bureau rating and consistent 5-star reviews on Google and Trustpilot demonstrate they operate differently than profit-driven competitors. The accreditation through Credit Counselling Canada provides third-party verification that their counsellors meet rigorous standards. When you call, ask specifically about their Debt Consolidation Program if you have multiple creditors, their consumer proposal pathway if bankruptcy feels looming, or their debt management options if you want to restructure payments on your own terms.

The intake process takes roughly 30 to 45 minutes, costs nothing, and creates zero obligation to proceed with their services.

Navigate government resources with realistic expectations

Government-backed resources exist but require more legwork to navigate. Provincial insolvency offices can provide information about bankruptcy and consumer proposals, though they won’t counsel you through the decision like Credit Canada does. You’ll need to contact your provincial office directly and ask what materials they provide about your options. Most provinces offer free information sessions, but these focus on explaining processes rather than helping you choose the right path for your circumstances.

Use online tools to establish clarity first

Online tools matter more practically here. The Debt Assessment Quiz available through reputable non-profit agencies helps you determine whether you can manage debt independently, qualify for a consolidation loan, need a Debt Consolidation Program, or face bankruptcy as your only option. Credit Canada’s Budget Calculator and Debt Calculator let you model different scenarios before committing to anything. These resources work best when you use them to establish clarity before speaking with a counsellor, not as substitutes for professional guidance when your situation involves multiple creditors or significant debt levels. Butterfly, a free budgeting app designed for newcomers to Canada, builds realistic budgets tailored to local costs if standard tools feel disconnected from your actual expenses.

Final Thoughts

Choosing the right debt help services Canada provider comes down to three concrete factors. First, verify accreditation through Credit Counselling Canada and confirm non-profit status, because these credentials mean the organization is legally bound to prioritize your outcome over profit. Second, demand transparency about costs and timelines before you commit to anything. Legitimate counsellors will never charge for initial assessments or pressure you into quick decisions.

Contact Credit Canada or another accredited non-profit agency and request a free intake assessment (bring documentation of your income, debts, and monthly expenses so the counsellor can give you an accurate picture of which path actually works for your situation). This conversation costs nothing and creates zero obligation. If you’re uncertain whether you’re ready to talk to someone, use the Debt Assessment Quiz or Budget Calculator first to establish clarity about your numbers.

The data shows 43% of Canadians need help escaping debt, yet 36% don’t know where to turn. You’re already ahead by reading this guide and understanding the difference between legitimate support and predatory operators. The shame and fear that keep people stuck are real, but they’re also the reason trustworthy organizations exist.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment