Mortgage rates shift constantly, and what made sense last year might not work today. At Financial Canadian, we’ve seen homeowners leave thousands of dollars on the table simply because they didn’t understand their refinance mortgage Canada options.

This guide walks you through when to refinance, what types of refinancing exist, and how to pick the option that actually saves you money.

When Should You Refinance Your Mortgage

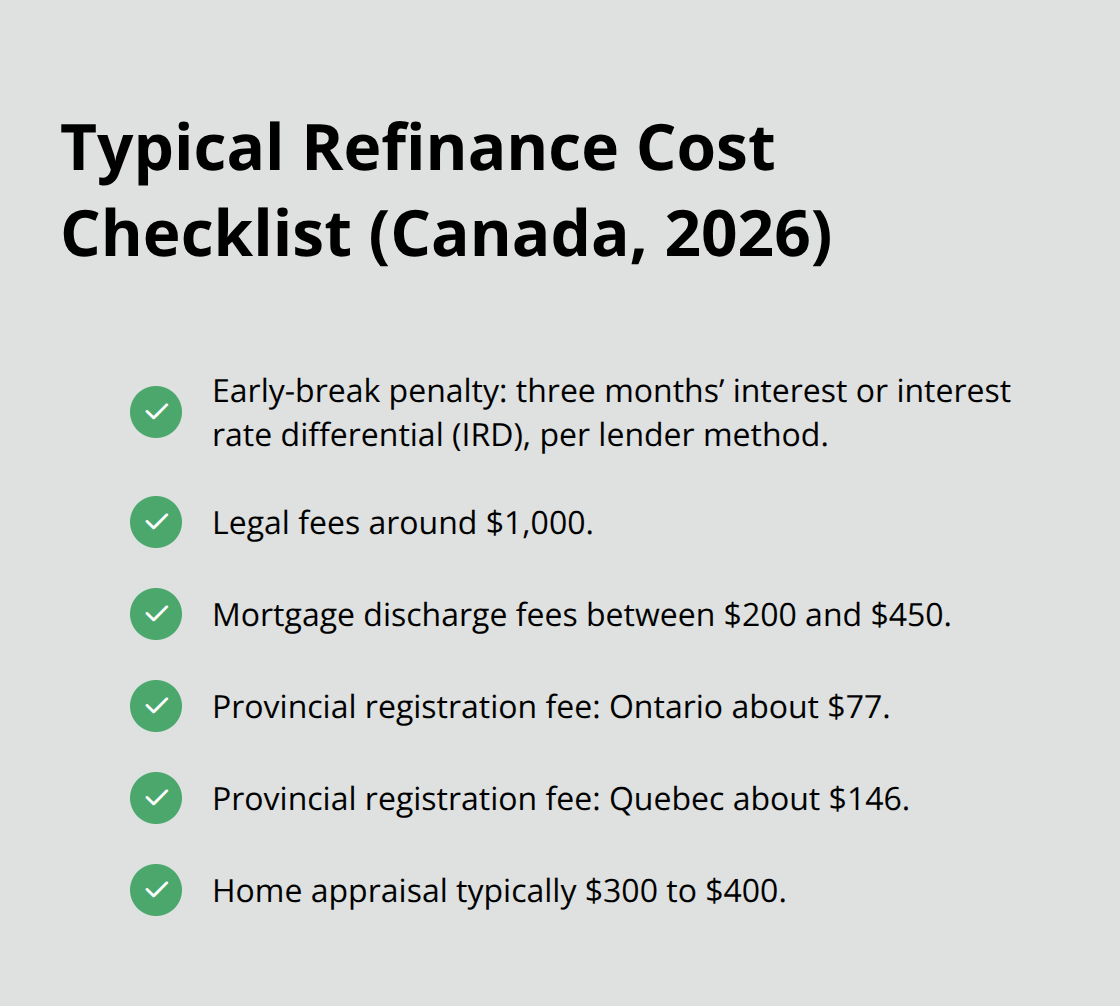

The decision to refinance hinges on three concrete factors that directly impact your wallet. First, compare your current mortgage rate against what lenders offer today. As of April 22, 2026, refinance rates sit around 4.8% for fixed terms, down from the 6.31% average in January 2024. If your rate is substantially higher, refinancing becomes mathematically attractive. However, this alone doesn’t tell the full story. You must calculate your break-even point by factoring in prepayment penalties and refinancing costs. If you break your mortgage early, you’ll face a penalty-typically three months’ interest or an interest rate differential, depending on your lender’s method. Add legal fees around 1,000 dollars, mortgage discharge fees between 200 and 450 dollars, and provincial registration fees. In Ontario, expect roughly 77 dollars; in Quebec, around 146 dollars. A home appraisal typically costs 300 to 400 dollars.

If your total costs exceed the annual interest savings, refinancing won’t benefit you financially. For example, if refinancing costs total 2,500 dollars but you’ll save 2,000 dollars annually in interest, you’ll break even in roughly 1.5 years-worthwhile only if you plan to stay in your home long enough to recoup that investment.

Compare Your Current Rate to Market Rates

Your existing rate matters less than the spread between your rate and available rates. A homeowner at 5.8% facing 4.8% options has a full percentage point advantage. That translates to roughly 100 dollars monthly savings on a 300,000 dollar mortgage. Conversely, someone at 5.2% refinancing to 4.8% saves only 33 dollars monthly-barely enough to justify the upfront costs. Timing also shapes your decision. If your current mortgage renews within six months, refinancing early may trigger unnecessary penalties when renewal would cost nothing. Near renewal, your lender often waives prepayment penalties, making the switch far cheaper. If you’re early in your term, the penalty sting is sharper, and the math becomes less favorable unless rate savings are substantial.

Assess Your Financial Goals and Time Horizon

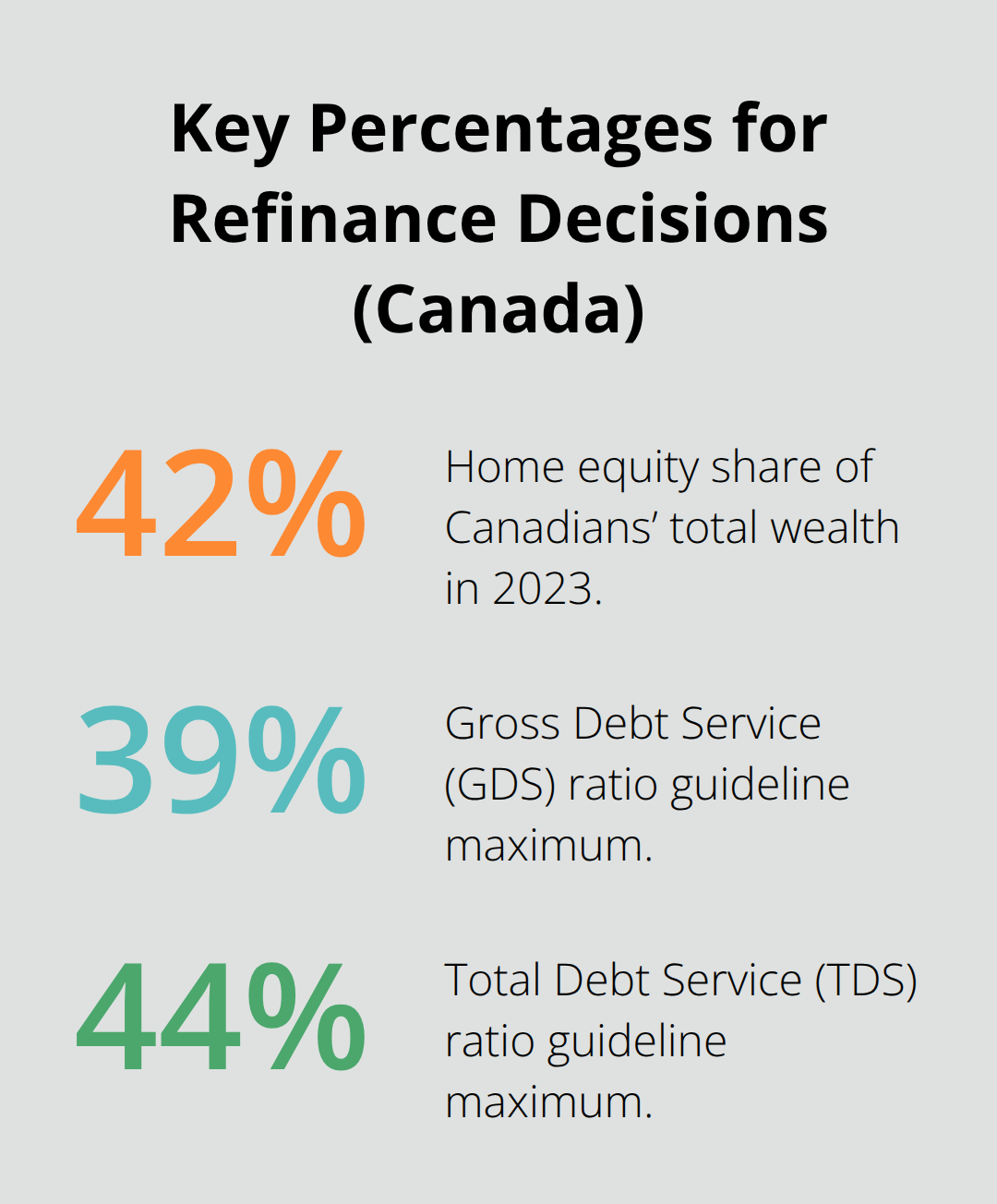

Refinancing serves purposes beyond chasing lower rates. If you want to access your home’s equity for renovations or debt consolidation, refinancing becomes a cash-out strategy rather than a rate play. Home equity represented about 42% of Canadians’ total wealth in 2023, and tapping that equity through refinancing can make financial sense if you’re consolidating high-interest debt or funding necessary home improvements. Your time horizon matters tremendously here. If you plan to sell within two years, refinancing costs rarely justify themselves unless you’re cashing out significant equity. If you stay put for five years or longer, the numbers shift dramatically in refinancing’s favor because you have more time to recoup costs through savings.

Verify Your Eligibility and Credit Standing

Your credit score and debt service ratios determine whether refinancing is even possible. Lenders typically require a minimum score around 600 to 620, though scores above 700 unlock better rates. Your gross debt service ratio should stay at or below 39%, and your total debt service ratio at or below 44%, according to CMHC guidelines. If your financial situation has deteriorated since you obtained your original mortgage, refinancing approval becomes uncertain, and you may face higher rates or need to explore alternative lenders.

Understanding these three factors positions you to evaluate the specific refinancing options available to you.

Types of Mortgage Refinancing Available in Canada

Canada’s refinancing landscape offers three distinct approaches, each suited to different financial situations and goals. Understanding which path fits your circumstances allows you to maximize savings and align your mortgage with your current needs.

Rate and Term Refinancing

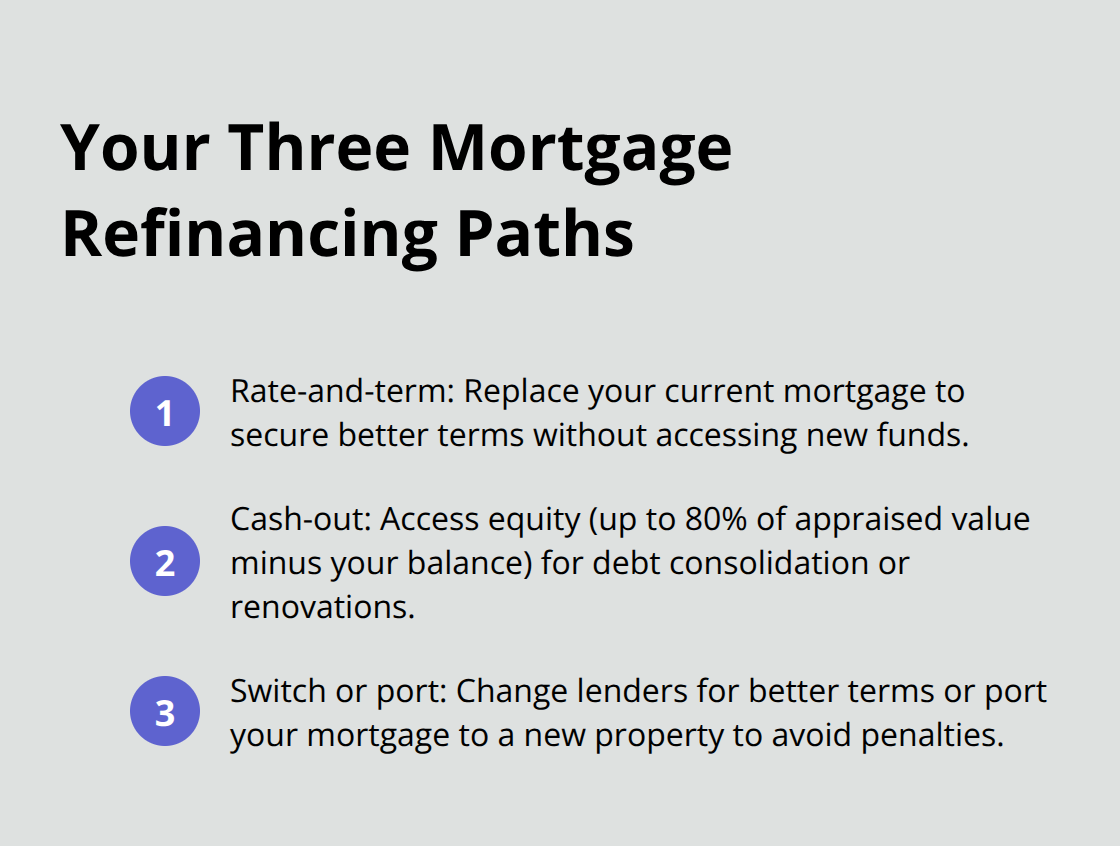

The simplest option replaces your current mortgage with a new one at better terms without accessing additional funds. This works best when rates have dropped significantly since you locked in your original mortgage. As of April 22, 2026, refinance rates sit around 4.8% for fixed terms, meaning anyone paying 5.5% or higher has a clear case to act.

The math is straightforward: calculate your monthly savings, subtract refinancing costs (roughly 2,000 to 3,000 dollars total when accounting for legal fees, discharge fees, and appraisal), then divide costs by monthly savings to find your break-even timeline. Most homeowners should refinance when the break-even point falls within two years or less.

You can also adjust your amortization during rate and term refinancing, which deserves serious consideration. Stretching your amortization from 20 years to 25 years reduces monthly payments further, though it increases total interest paid over the life of the mortgage. This trade-off makes sense only if your cash flow is genuinely tight and you plan to aggressively prepay once your financial situation improves.

Cash-Out Refinancing for Equity Access

Cash-out refinancing allows homeowners to access their equity for specific purposes like debt consolidation or home improvements. If your home has appreciated and you’ve paid down your mortgage, you can borrow against that equity up to 80% of your home’s current appraised value, minus what you still owe. This approach proves powerful for consolidating high-interest credit card debt or personal loans into your mortgage at a lower rate, though it does extend the repayment timeline and increases total interest costs if you lack discipline.

Switching Lenders and Portability Options

The third path involves switching lenders entirely or exploring portability options. Switching lenders gives you maximum flexibility to negotiate rates and terms, but it triggers legal fees, discharge fees, and possibly prepayment penalties if you’re breaking your current term. Portability, offered by some lenders, allows you to move your mortgage to a new property without breaking your contract, which eliminates penalties and discharge fees entirely. This option remains underutilized by homeowners who move before their term ends, yet it can save thousands in unnecessary costs.

Comparing Your Three Paths

When comparing these three paths, focus on total costs, not just the interest rate advertised. Published rates exclude taxes, fees, and insurance, so request a detailed quote that itemizes every cost. Shop with at least three lenders, including both major banks and mortgage brokers who access a wider panel of options. Variable-rate refinances currently hover around 4% or higher, making them attractive for risk-tolerant borrowers who believe rates will stay stable or decline, while fixed rates at 4.8% appeal to those seeking payment certainty and protection against future rate hikes.

Each refinancing path carries different cost structures and outcomes. Your next step involves calculating which option delivers the greatest financial benefit for your specific situation-a process that requires comparing actual offers side by side.

How to Compare and Choose the Best Refinance Option

The gap between a mediocre refinance deal and an excellent one often exceeds $10,000 over the life of your mortgage. Most homeowners shop with one lender, accept the first offer, and move forward without realizing they’ve left substantial savings on the table. The refinancing market rewards those who invest a few hours comparing offers side by side.

Request Detailed Quotes from Multiple Lenders

Start with at least three lenders: your current bank, one competing major bank, and a mortgage broker who can access multiple lenders simultaneously. Request that each quote breaks down every single cost-the interest rate, legal fees, discharge fees, appraisal costs, and provincial registration charges. Don’t accept rates quoted without these itemized costs attached, because published rates tell you almost nothing about the true cost of refinancing.

As of April 22, 2026, fixed rates hover around 4.8%, but one lender might charge $1,500 in fees while another charges $2,800. That $1,300 difference wipes out months of interest savings. Create a spreadsheet comparing the total cost of refinancing at each lender, not just the interest rate. Calculate your monthly payment under each scenario, multiply it by your amortization in months, add the upfront costs, and subtract any incentives the lender offers.

Evaluate Total Costs and Incentive Offers

Some lenders provide cash back incentives for refinancing, which can offset costs significantly. A lender offering 4.8% with $1,000 cash back is fundamentally different from another offering 4.75% with zero incentives, even though the second rate appears better. The true cost comparison requires you to factor in these incentives alongside fees and interest rates.

Variable-rate refinances currently hover around 4% or higher, making them attractive for risk-tolerant borrowers who believe rates will stay stable or decline, while fixed rates at 4.8% appeal to those seeking payment certainty and protection against future rate hikes. Your spreadsheet should include both options so you can see the real financial impact of each choice.

Review Prepayment Privileges and Penalty Structures

Terms and conditions contain traps that derail refinance plans after closing. Review prepayment privileges carefully because they determine whether you can pay down your mortgage faster without penalties. Some lenders cap prepayment at 15 percent of the original principal annually, while others allow unlimited prepayment. If you anticipate receiving bonuses or inheritances and want to accelerate your payoff, restrictive prepayment terms cost you thousands in extra interest.

Check whether the lender charges a mortgage discharge fee when you eventually switch again, and verify the exact calculation method for any early repayment penalties. Interest rate differential penalties typically cost less than three months’ interest when rates have fallen, but confirm this with your specific lender before signing. Ask explicitly about stress test requirements; as of April 2026, a stress test is typically required unless your mortgage is insured, and this adds complexity and cost to your application.

Clarify Hidden Fees and Insurance Implications

Request clarity on whether your property tax or home insurance documentation will trigger any additional fees. Some lenders bundle appraisal costs into their quote while others bill separately after the appraisal is ordered. Hidden appraisal fees range from $300 to $500 depending on your property’s complexity, so understanding this upfront prevents surprises.

If you’re switching lenders and your original mortgage was CMHC insured, ask how the new lender handles insurance implications on your refinanced loan, because this affects your total borrowing cost significantly. Finally, confirm the timeline from application to funding because you need to know whether your refinance closes before or after your current term expires, which determines whether you’ll face penalties.

Final Thoughts

Refinancing your mortgage isn’t a one-size-fits-all decision, and the refinance mortgage Canada options available to you depend entirely on your rate environment, financial goals, and time horizon. The homeowners who benefit most invest time comparing offers from multiple lenders, calculate their true break-even point, and understand the full cost structure before signing anything. As of April 2026, rates have fallen significantly from their 2024 peaks, creating genuine opportunities for those paying 5.5% or higher.

Your immediate next step is straightforward: gather your current mortgage documents and request detailed quotes from at least three lenders (your bank, a competing major bank, and a mortgage broker who accesses a wider panel of options). Request itemized costs for every component-interest rate, legal fees, discharge fees, appraisal, and provincial registration charges. Build a spreadsheet comparing total costs across all three scenarios, factoring in any cash-back incentives your lenders offer, and this exercise typically reveals savings exceeding $5,000 over your mortgage’s remaining life.

Once you’ve identified your best option, verify your eligibility by confirming your credit score sits above 700 and your debt service ratios align with CMHC guidelines. We at Financial Canadian understand that navigating refinancing decisions requires clarity and confidence, and our visually stunning, highly functional websites help financial professionals communicate complex mortgage information to homeowners and make comparison and decision-making easier. Move forward only when the numbers genuinely work in your favor.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment