Payday loans can feel like a quick fix when cash runs short, but the fees attached to them often catch borrowers off guard. At Financial Canadian, we’ve seen how a small loan can balloon into an expensive debt trap when you don’t understand the true cost upfront.

The good news is that payday loan fees in Canada follow predictable patterns, and knowing what to expect puts you in control. This guide breaks down exactly what you’ll pay and how to sidestep the surprises that cost Canadians thousands every year.

How Payday Loan Fees Actually Work

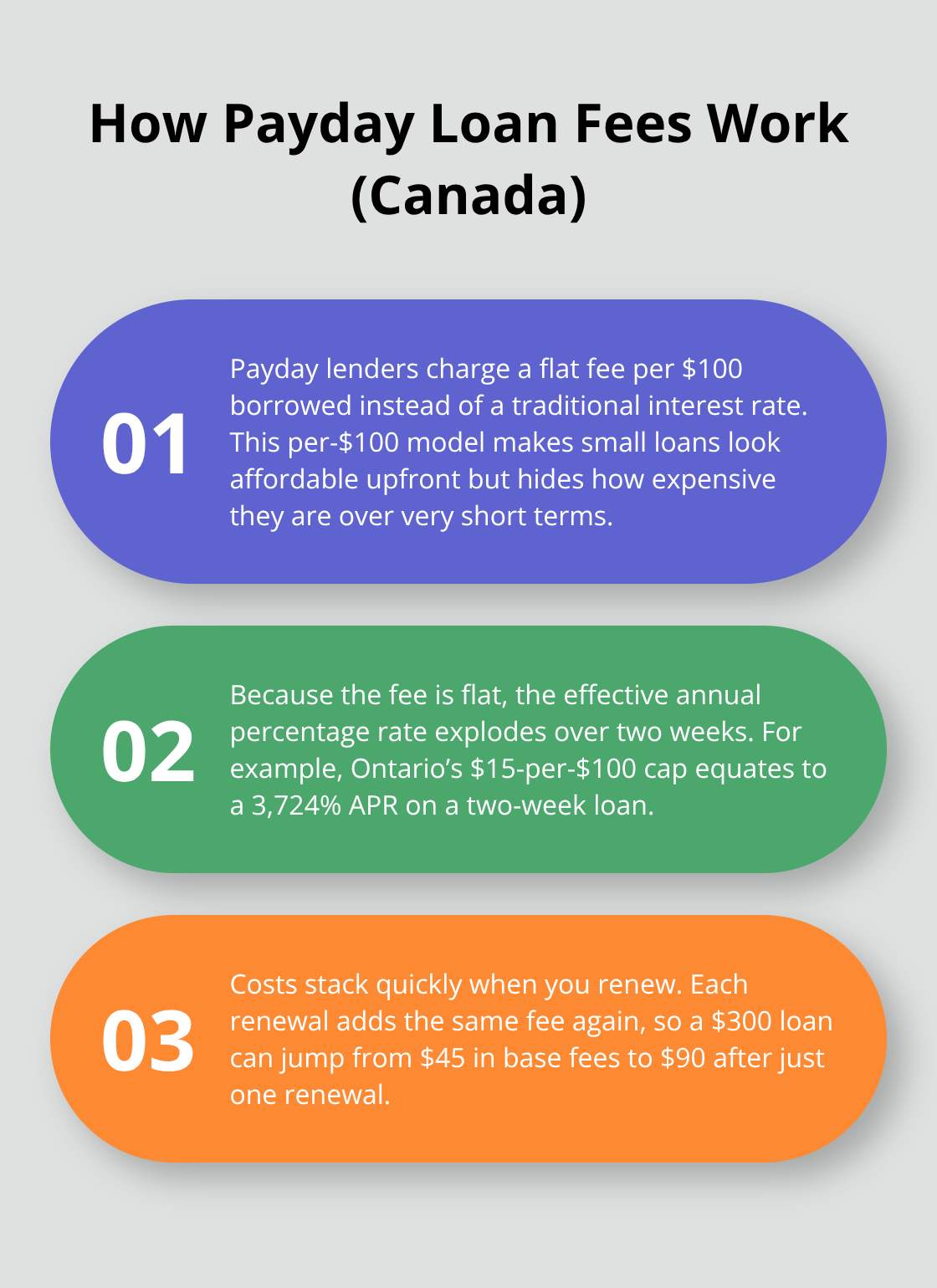

Payday loan fees in Canada operate on a per-$100-borrowed model rather than traditional interest rates, which is why the true cost shocks so many borrowers. Most provinces cap what lenders can charge at $14 to $17 per $100 borrowed, but this flat fee structure creates annual percentage rates that soar into the thousands. Take Ontario as an example: the $15-per-$100 cap produces an effective APR of 3,724% for a two-week loan. A $300 loan costs roughly $45 in fees alone, and if you renew that loan even once, you pay another $45 on top, pushing your total cost to $90 on what started as a $300 problem. This is why the fee structure matters far more than the interest rate label-you’re not borrowing money at 15% annually; you’re paying a fixed chunk upfront that compounds when you can’t repay on time.

Provincial Fee Caps Vary Dramatically

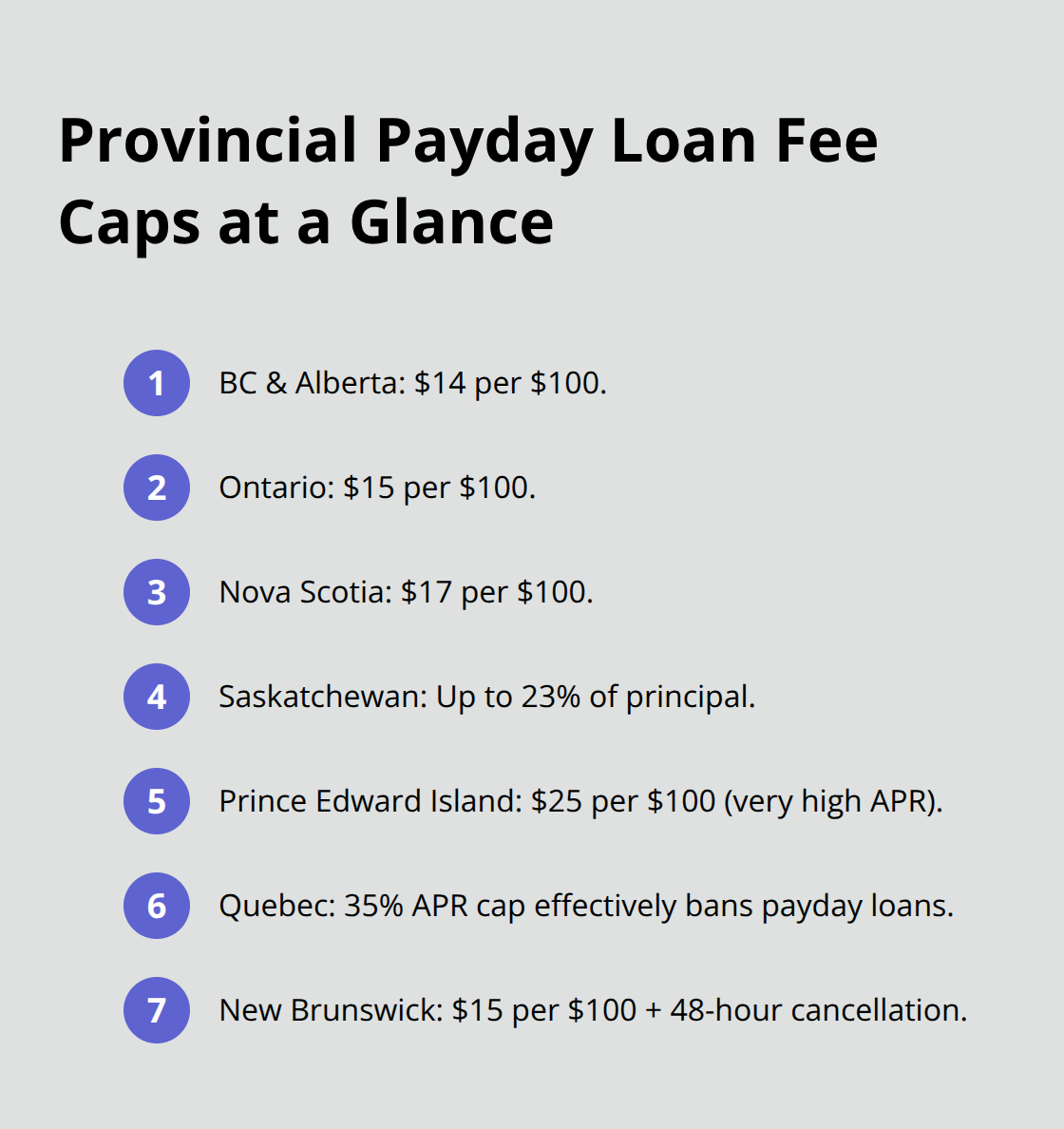

Each province sets its own ceiling, and the differences are substantial. British Columbia caps charges at 14 per $100, while Prince Edward Island allows $25 per $100, which translates to an APR of roughly 33,519% for a two-week term. Alberta introduced a $15-per-$100 cap specifically to become the lowest among regulated provinces. New Brunswick requires a $15-per-$100 fee, allows a 48-hour cancellation window, and limits loans to 30% of your net pay. Saskatchewan caps charges at 23% of the principal, while Quebec has effectively banned payday loans by capping all short-term lending at around 35% APR. The practical takeaway: if you live in a province with a tighter cap like BC or Alberta, your fees are lower, but you’re still paying hundreds of dollars in fees on small loans. If you’re in PEI or borrowing in a province without clear regulation, the cost becomes predatory fast.

Hidden Fees That Add Up Quickly

The per-$100 fee is only the beginning. Lenders charge dishonoured cheque fees when your payment bounces, late payment fees if you miss the due date, and deferral or renewal fees when you extend the loan. A $40 renewal fee on a $300 loan is common, and many borrowers renew multiple times. The federal cap on dishonoured cheque fees is now $20, but lenders can still layer on late charges and interest on the outstanding balance at up to 2.5% per month. If you access your loan online or require faster approval, some lenders tack on processing fees. The real danger emerges when you miss a payment and the lender attempts repeated withdrawals from your bank account-each failed attempt triggers additional NSF charges from your bank, not just the payday lender.

What You Must Do Before Signing

Request the full loan document and identify every fee listed, including what happens if payment fails or you need to extend. Ask specifically about late charges, deferral fees, and processing costs. Many borrowers only discover these fees after they’ve already borrowed and can’t pay back on time. Understanding the complete fee structure upfront means you can calculate whether a payday loan makes sense for your situation or whether you should explore other options that cost far less.

Typical Payday Loan Fees Across Canadian Provinces

Fee Ranges by Province

The fee you pay depends entirely on which province you live in, and the gap between the cheapest and most expensive provinces is staggering. British Columbia and Alberta cap charges at $14 per $100 borrowed, which translates to $14 on a $100 loan or $42 on a $300 loan. Ontario charges $15 per $100, Nova Scotia $17 per $100, and Saskatchewan allows up to 23% of the principal. But move to Prince Edward Island and you’ll pay $25 per $100 borrowed, which creates an APR of 33,519% for a two-week term according to PEI government information. Quebec has effectively banned payday loans by capping all short-term lending at 35% APR, so if you need fast cash in Quebec, you simply won’t find a licensed payday lender. New Brunswick requires $15 per $100 and adds a 48-hour cancellation window, which at least gives you a brief escape route if you change your mind. The federal cap of $14 per $100 now applies in designated provinces, but this floor doesn’t help borrowers in provinces that already allow higher charges. What matters most is this: a $300 loan in BC costs $42 in base fees, while the same loan in PEI costs $75 before any renewal or late charges hit.

How Payday Loans Stack Up Against Other Borrowing Options

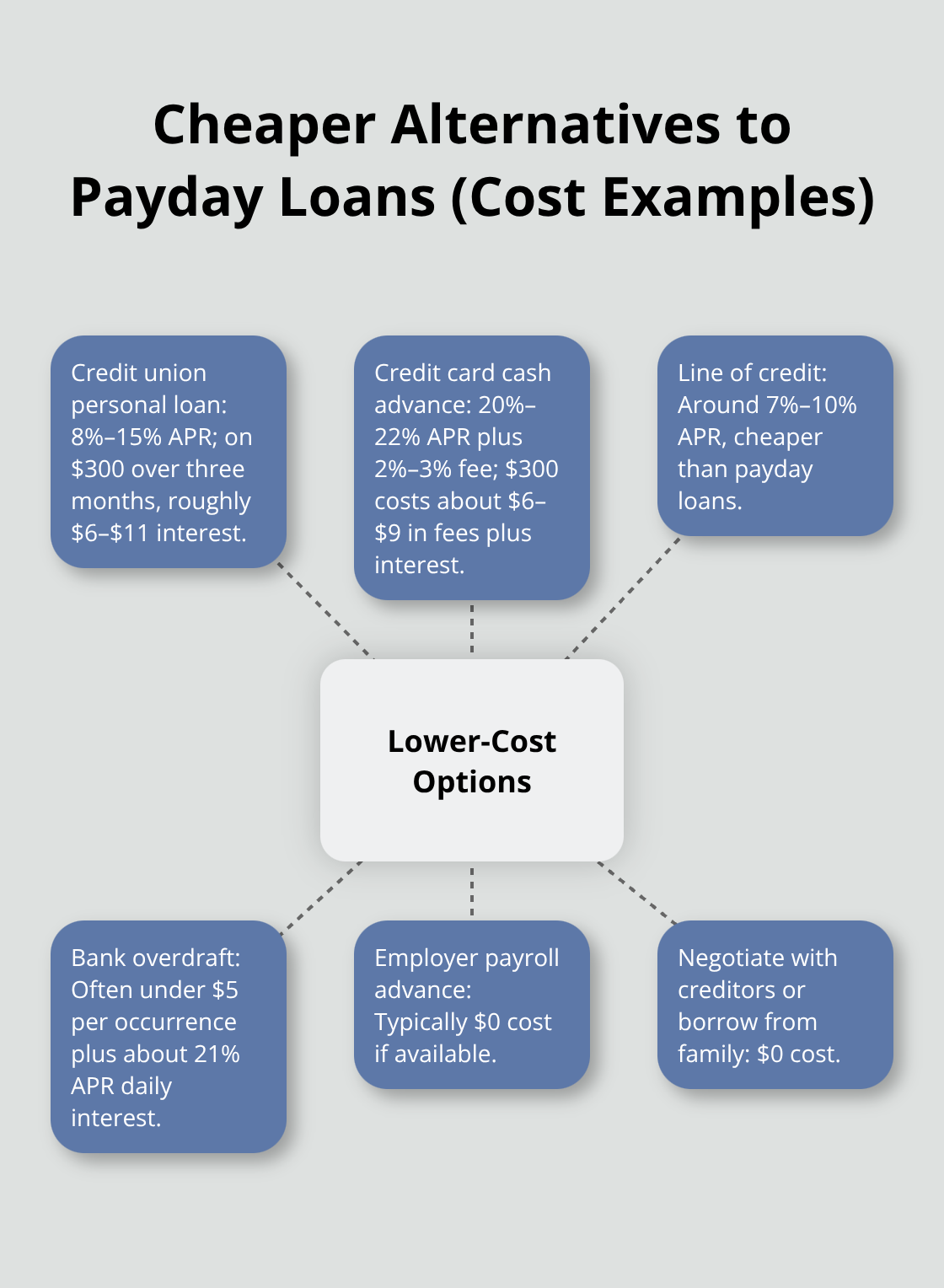

Comparing these costs to other borrowing options reveals why payday loans should be your absolute last resort. A personal loan from a credit union typically charges 8% to 15% APR, which on a $300 loan over three months costs roughly $6 to $11 in interest. A credit card cash advance runs 20% to 22% APR plus a 2% to 3% upfront fee, so withdrawing $300 costs around $6 to $9 in fees plus interest. Even a line of credit at 7% to 10% APR is cheaper than any payday loan.

An overdraft from your bank, while not ideal, usually costs less than $5 per occurrence plus daily interest around 21% APR. If your employer offers payroll advances, you pay nothing. If you negotiate with creditors for a payment extension or ask family for a short-term loan, the cost drops to zero.

Why the Math Matters Before You Borrow

The payday loan fee structure only makes sense if no other option exists, and even then, the cost compounds rapidly if you can’t repay within two weeks. Most borrowers who use payday loans have already exhausted traditional credit options, but before you sign, call your bank, ask your employer, contact a local credit union, and verify whether a personal loan is possible. The difference between a $42 payday loan fee and a $6 credit union interest charge means you keep an extra $36 in your pocket. This comparison shows why exploring alternatives first (rather than turning to payday loans immediately) protects your finances and your future repayment capacity. Once you understand what you’ll actually pay across provinces and against other options, the next step involves learning how to spot and avoid the hidden fees that lenders don’t advertise upfront.

How to Spot and Stop Hidden Payday Loan Fees Before They Drain Your Account

Read the Loan Agreement Word by Word

The loan agreement is where lenders hide the real cost, and most borrowers never read it before signing. Open the document and search for every mention of fees: renewal fees, deferral fees, processing fees, late payment charges, and NSF fees. Write down the exact dollar amount or percentage for each one. Many lenders list these in fine print scattered across multiple pages, which is deliberate.

The maximum cost of borrowing is $14 per $100 in provinces where there are payday loan regulations. Dishonoured cheque fees cap at $20 federally, yet lenders can still charge late payment interest up to 2.5% per month on any outstanding balance. If you renew the loan, expect another $14 to $25 fee depending on your province.

Ask the lender directly: What happens if my payment bounces? What is the late fee? If I renew, what do I pay? Get written answers before you commit.

Understand the Automatic Withdrawal Trap

One critical detail most borrowers miss is the automatic withdrawal clause. Lenders require access to your bank account and will attempt repeated withdrawals if your first payment fails. Each failed attempt triggers NSF charges from your bank, sometimes $35 or more per attempt.

Some lenders make three or four withdrawal attempts, and you end up paying $140 in bank fees alone on top of the payday loan fee. This is why reading the withdrawal authorization section matters as much as the fee schedule. The lender controls when and how often they attempt to pull money from your account, and your bank charges you for each failure.

Calculate the True Cost Before You Commit

Calculating the true cost means converting the per-$100 fee into what you actually owe in dollars, then projecting what happens if you renew. A $300 loan in Ontario at $15 per $100 costs $45 in base fees, due in two weeks. If you cannot pay and renew, you pay another $45 on top of the original $300, bringing your total debt to $390 for a four-week period. If you renew again, you reach $435.

Payday lenders drained more than $2.4 billion in fees from borrowers in a single year, but this assumes you borrow once and repay on time. Most payday loan users renew multiple times, which erases these savings. Before you borrow, calculate how many paycheques you need to cover the loan plus fees without renewing. If you cannot pay within two weeks without renewing, the loan is too expensive.

Compare Payday Loans to Real Alternatives

Compare this cost to alternatives: a credit union personal loan at 12% APR on $300 over three months costs roughly $9 in interest. A credit card cash advance at 21% APR plus a 3% fee costs about $9 to $15 total. An overdraft at 21% APR costs roughly $5 per occurrence plus daily interest. If your employer offers payroll advances, the cost is zero.

Contact your bank, credit union, and employer before you apply for a payday loan. Ask specifically for the APR and total cost in dollars on a $300 loan over two weeks. Compare these numbers directly. The difference between a $45 payday loan fee and a $9 credit union interest charge is $36 you keep. This comparison takes 15 minutes and can save you hundreds of dollars annually.

Final Thoughts

Payday loan fees in Canada follow a predictable pattern, but understanding that pattern separates borrowers who stay in control from those who spiral into debt. A $300 payday loan in Ontario costs $45 upfront, while the same loan in Prince Edward Island costs $75 before renewal fees enter the picture. These differences determine whether you can actually afford to repay without renewing, and renewal is where the trap closes.

Read the full loan agreement before you sign and calculate the total cost in actual dollars, not just the per-$100 fee. Verify what happens if your payment bounces or you need to extend, since most borrowers discover hidden fees only after they’ve already committed. The dishonoured cheque fee cap is $20 federally, but your bank charges you separately for each failed withdrawal attempt, and lenders often make multiple attempts (which means these bank fees stack on top of payday lender fees and double your actual cost).

Before you apply for a payday loan, call your bank, credit union, and employer to ask for the APR and total cost in dollars on a $300 loan over two weeks. A credit union personal loan at 12% APR costs roughly $9 in interest on that amount, while a credit card cash advance costs $9 to $15 total. If you’ve already borrowed and feel trapped by payday loan fees, professional debt guidance can help you explore options and build better financial habits.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment