Your credit score shapes your financial life in Canada. It affects whether you get approved for mortgages, car loans, and credit cards-and what interest rates you’ll pay.

At Financial Canadian, we’ve created this guide to help you understand how Canada credit scores work, what impacts them, and how to improve yours. Whether you’re starting from scratch or fixing past mistakes, you’ll find actionable steps to build stronger credit.

How Canada’s Credit System Works

The Two Bureaus That Control Your Financial History

Canada’s credit system relies on two private companies-Equifax and TransUnion-that collect and maintain your financial history. These aren’t government agencies. They’re for-profit businesses that lenders pay to access your credit information. Every time you borrow money or make a payment, lenders report that activity to one or both bureaus. This data feeds directly into your credit score, a three-digit number between 300 and 900 that lenders use to decide whether you qualify for credit and what interest rate you’ll pay.

How Your Score Gets Calculated

The higher your score, the lower your risk appears to lenders, and the better terms you’ll receive. Most Canadian lenders treat a score of 650 as a baseline for decent credit, though some use 680 as a threshold. Scores above 720 open doors to significantly better rates and more favorable terms. The gap between a 650 score and a 750 score can easily cost or save you thousands of dollars over a mortgage or car loan. Your score isn’t fixed-it changes monthly as new information arrives at the bureaus. This means your financial behavior today directly shapes your borrowing power tomorrow.

Understanding Your Score Range

A score between 800 and 900 is excellent and qualifies you for the best rates available. Between 720 and 799, you’re in very good territory with broad credit options. From 650 to 719, you have good credit but won’t access the absolute lowest rates. Below 650, lenders see real risk, and mainstream financing becomes harder to obtain.

The Five Factors Behind Your Number

Credit scores are calculated from five concrete factors: payment history carries the heaviest weight, credit utilization measures how much of your available credit you’re using, length of credit history rewards older accounts, new credit inquiries show recent borrowing behavior, and credit mix reflects whether you handle different types of debt. You can check your actual score and report for free through your Canadian bank’s online portal-most major banks including RBC, BMO, and Scotiabank offer this service.

Errors on Your Report Cost You Real Money

Your credit report lists every mortgage, loan, and credit card you’ve held, plus any missed payments, liens, or judgments. Errors on your report directly damage your score, so verification matters. If you spot inaccurate information, contact the bureau immediately to request correction. Many people improve their score simply by fixing reported errors that never should have appeared in the first place. Understanding what appears on your report sets the stage for the specific actions that move your score higher.

What Actually Moves Your Credit Score

Payment History: The Dominant Factor

Payment history shapes your credit score more than any other factor, accounting for roughly 40% of your total score according to standard credit scoring models. This means one missed payment can erase months of responsible financial behavior. A single late payment stays on your report for six years in Canada, and lenders interpret it as a warning sign that you might miss future obligations.

The damage hits hardest when payments fall 30, 60, or 90 days overdue-a 90-day missed payment can drop your score by 100 points or more. Set up automatic payments for at least your minimum balance on every account. Missing even one payment isn’t worth the score damage and the years required to recover.

Credit Utilization: The Second Major Driver

Credit utilization ratio measures how much of your available credit you actively use, and it accounts for roughly 30% of your score. If you hold a credit card with a $5,000 limit and carry a $3,000 balance, your utilization sits at 60%-which lenders view as risky behavior. Keeping utilization below 30% signals that you manage credit responsibly and aren’t desperate for money. Utilization resets monthly based on your statement date, so paying down balances before your statement closes produces immediate impact on your score. This single action often yields faster results than waiting for older accounts to age.

Length of History, New Credit, and Credit Mix

The three remaining factors-length of credit history (15%), new credit inquiries (10%), and credit mix (10%)-matter less individually but compound over time. Closing old accounts damages your score because it shortens your credit history and reduces your total available credit, both of which harm your standing. Opening multiple new credit accounts in a short window triggers hard inquiries that temporarily lower your score by a few points each. Credit mix means holding different types of debt-a mortgage, car loan, and credit card together look better to lenders than three credit cards alone. Payment history and utilization dominate your score, so focusing your energy on paying bills on time and keeping balances low produces far better results than obsessing over credit mix or the age of your oldest account.

Moving Forward With Your Score

These five factors work together to determine whether lenders approve your applications and what rates they offer. Understanding which factors carry the most weight helps you prioritize your actions and see faster improvement. The next section shows you exactly how to check your current score and which practical steps move it higher fastest.

Checking Your Score and Taking Action

Access Your Credit Report for Free

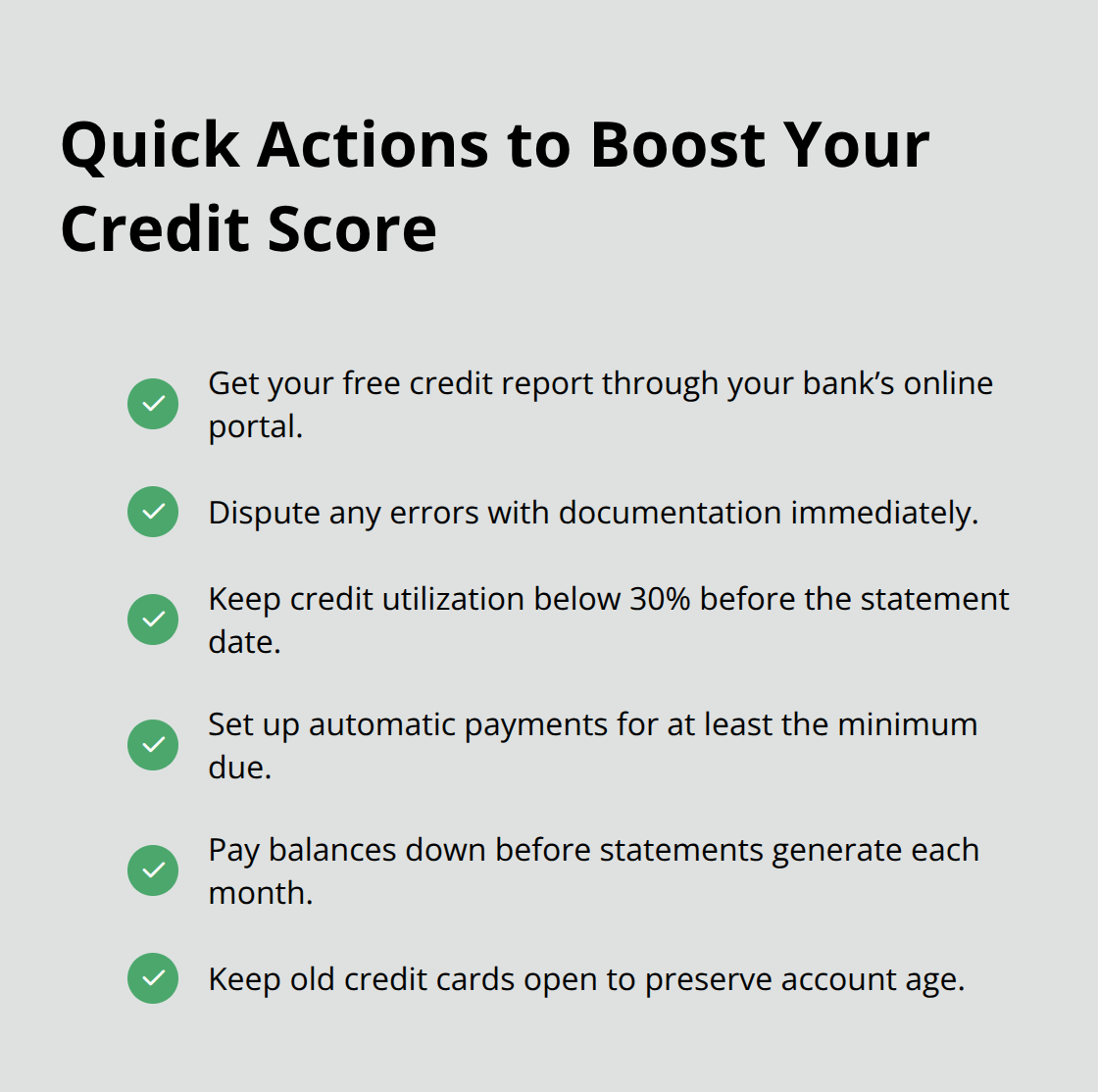

You can obtain your credit score and report at no cost through your Canadian bank’s online portal right now. RBC, BMO, and Scotiabank all offer this service to account holders, with scores updated monthly. Equifax and TransUnion also allow you to request your credit report directly from their websites at no cost. The report itself doesn’t include your score, but you can calculate it from the data listed. Once you have your report in hand, verify every detail: check that all listed accounts belong to you, confirm payment history is accurate, and scan for any liens or judgments that shouldn’t be there. Errors happen frequently, and fixing them produces immediate score improvements without requiring months of financial discipline.

Dispute Errors Immediately

Contact the bureau directly if you find mistakes, providing documentation to support your dispute. This single step costs nothing and often yields results faster than any other action you can take. Many people improve their score simply by correcting reported errors that never should have appeared in the first place.

Reduce Your Credit Utilization

The fastest way to raise your score involves managing credit utilization strategically. If you currently carry balances near your credit limits, your score suffers dramatically. Reduce your credit utilization to below 30 percent of your available credit before your statement closing date, and your score will improve within one billing cycle. This doesn’t mean paying off everything permanently-lenders actually want to see you using credit responsibly, not avoiding it entirely. Instead, charge purchases to your cards as normal, then pay the balance down before statements generate. Automatic payments set to clear your full balance monthly work exceptionally well for this approach.

Combined with on-time payments going forward, this strategy alone can move you from fair to good credit within three to four months. The key is consistency: one month of good behavior doesn’t matter if you slip back into old patterns.

Understand Your Timeline for Improvement

Improvement speed depends on where you’re starting. A recent missed payment that dropped your score by 100 points can recover faster than an old judgment that’s been sitting on your report. Payment history improvements begin showing within 30 days of establishing on-time payments, with meaningful movement typically visible after 60 to 90 days of perfect payment behavior. Credit utilization changes reflect even faster-sometimes within weeks of paying down balances.

However, negative items like missed payments stay on your report for up to seven years, gradually losing impact as they age. A missed payment from five years ago damages your score far less than one from five months ago. Hard inquiries from credit applications disappear after three years. The oldest accounts on your report actually strengthen your standing over time, so keeping old credit cards open (even unused) helps more than closing them. Building excellent credit from poor credit typically requires 12 to 24 months of consistent on-time payments and low utilization, assuming no new negative events occur during that period.

Final Thoughts

Your credit score determines whether you access affordable financing or face rejection and higher rates. At Financial Canadian, we believe understanding how Canada credit scores explained empowers you to take control of your financial future instead of letting past mistakes define your borrowing power indefinitely. The actions that matter most are straightforward: pay every bill on time without exception, keep credit card balances below 30 percent of your limits, and verify your credit report for errors at least annually.

Start by checking your free credit report through your bank’s online portal or directly from Equifax and TransUnion. Dispute any errors immediately, then commit to paying bills on time and managing utilization strategically. These steps cost nothing and require only discipline, not income or luck (most people move from fair to good credit within three to four months of establishing on-time payments and reducing utilization).

If you’re building a financial presence online, we at Financial Canadian offer web design services that help businesses establish credibility and reach customers effectively. Your credit score reflects your financial reliability to lenders, and your website reflects your professionalism to customers.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment