Your average credit score in Canada directly shapes how much you’ll pay for mortgages, credit cards, and loans. A lower score can cost you thousands in extra interest over time.

At Financial Canadian, we’ve seen how borrowers often don’t realize the real impact their credit score has on their finances. This guide breaks down what your score means and how to improve it.

What’s the Average Credit Score in Canada

The national average credit score in Canada sits at 760 according to FICO as of November 2024, though this figure masks significant variation depending on where you live and which scoring model a lender uses. That 760 average actually dropped two points from 2023, signaling a concerning trend for Canadian borrowers. However, Borrowell reported a notably lower average of 672 in 2022, illustrating why you shouldn’t rely on a single number. Different credit bureaus use different models, and lenders may pull scores from Equifax or TransUnion, or alternative providers, meaning your actual score could differ substantially depending on who’s checking it. Understanding where you stand relative to these benchmarks matters because lenders use your score to determine whether they’ll lend to you and at what rate.

How Your Score Stacks Up by Region

Credit scores vary dramatically across Canada, with Vancouver sitting at 705 and Toronto at 696, while Alberta and Saskatchewan average around 658. This isn’t random variation. Borrowell’s 2022 data shows Ontario residents average 686, British Columbia 694, and Quebec 678, with Atlantic provinces like New Brunswick trailing at 649. Age compounds these regional differences significantly. Canadians aged 18 to 25 average 692, while those over 65 reach 750, meaning younger borrowers face steeper obstacles regardless of location. If you’re in Alberta or Saskatchewan and under 35, you’re fighting against two headwinds simultaneously. Conversely, if you’re in British Columbia or Ontario and over 45, your demographic advantages translate to better borrowing terms before you even apply. Knowing your province’s baseline helps you set realistic improvement targets and understand whether lenders will view your score favorably.

The Five Factors That Build Your Score

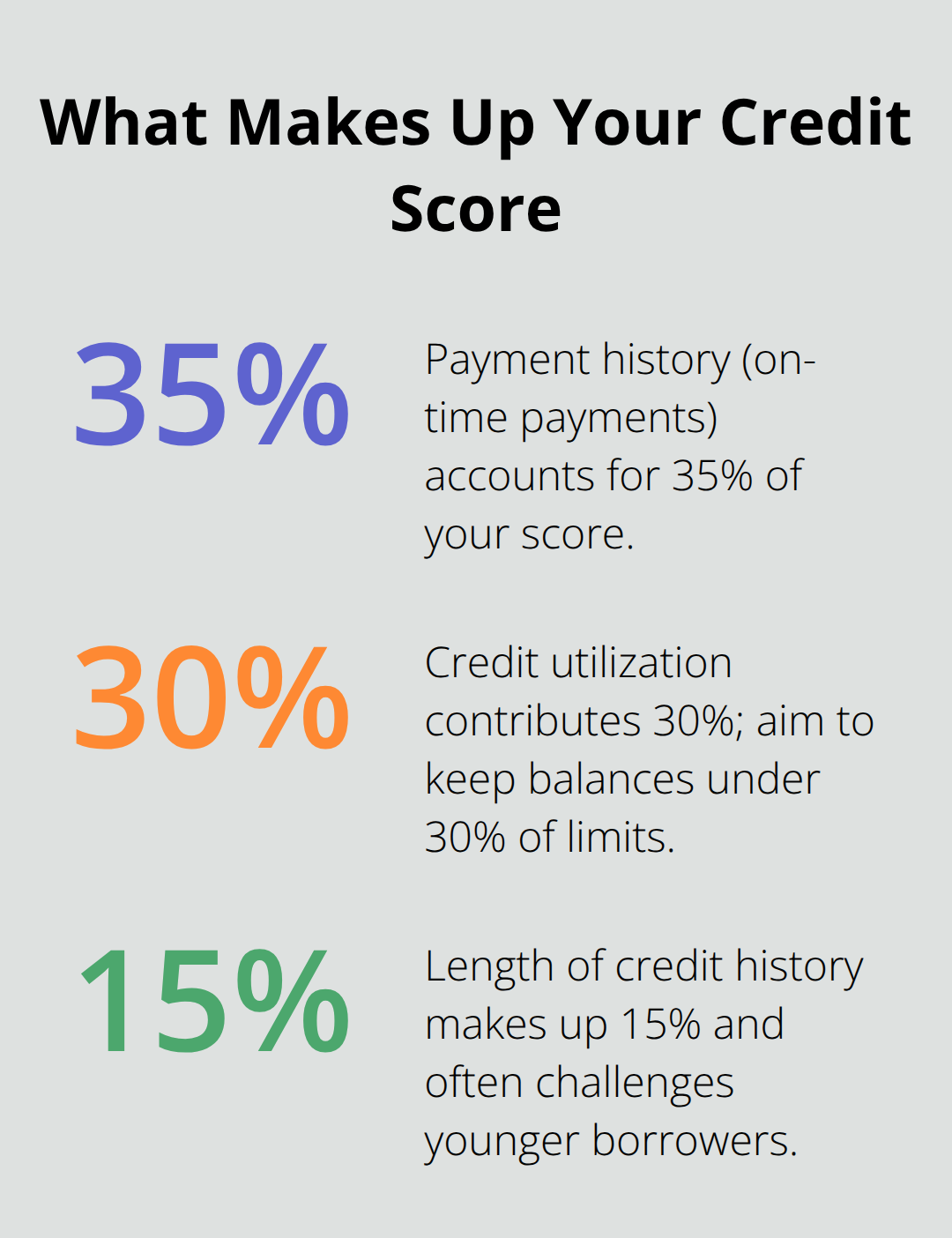

Payment history accounts for 35 percent of your score, making on-time payments non-negotiable. Credit utilization sits at 30 percent, meaning you should keep your total debt below 30 percent of available credit limits across all cards and lines. Length of credit history contributes 15 percent, which explains why younger Canadians struggle.

Credit mix represents 10 percent, so a mortgage, credit card, and perhaps an auto loan strengthen your profile more than relying solely on credit cards. Hard inquiries consume the final 10 percent, and each application for new credit temporarily reduces your score. Most people focus exclusively on payment history and miss the other levers entirely. If you’re stuck at 700 and can’t seem to move higher, examine your utilization first. Paying down balances to 20 percent utilization often yields faster score improvements than waiting for older accounts to age.

What These Benchmarks Mean for Your Borrowing Power

A score of 760 places you in the good-to-excellent range, which translates to competitive rates on mortgages and credit products. Lenders view scores above 740 as low-risk, meaning they’ll approve your applications faster and quote you their best rates. If your score falls below 660, lenders either reject you outright or charge substantially higher interest rates to offset their perceived risk.

The difference between a 650 and 750 score can cost thousands of dollars in extra interest on a mortgage over 25 years. Regional and age-based averages matter because they set the competitive bar in your market. If you’re in New Brunswick with a 680 score, you’re above your provincial average but still below the national benchmark, which affects what rates you’ll qualify for when you apply for credit.

How Your Credit Score Determines What You Pay

Your credit score directly dictates the interest rate lenders offer you, and the difference between a mediocre score and a strong one translates into thousands of dollars over the life of a loan.

Mortgage Rates and Your Score

Mortgage lenders are the most transparent about how scores affect rates. A borrower with a 760 score qualifies for significantly better rates than someone with a 680 score on the same mortgage amount. The gap widens dramatically for mortgages because lenders view a 25-year commitment as high-risk, meaning they scrutinize your score intensely. If you apply for a mortgage and your score sits between 660 and 712, you’ll pay a premium compared to borrowers above 740. Even a single percentage point difference in your mortgage rate costs thousands over time.

Credit Cards and Interest Rates

Credit card issuers apply the same logic but more aggressively. A 760 score might qualify you for a card with a 19.99 percent interest rate, while a 650 score gets offered 21.99 percent or faces outright rejection. The issuer’s risk calculation is straightforward: lower scores indicate higher default risk, so they charge more or decline the application entirely.

Personal Loans and Accessibility

Personal loan accessibility follows the same pattern. Banks and credit unions require minimum scores for unsecured loans, typically 660 or higher, and your exact rate depends on where your score lands within their approved range. A score of 700 versus 680 on a five-year personal loan can mean a 2 to 3 percent difference in your interest rate, adding hundreds to your total cost.

Your Action Plan Before Applying

The practical reality is that you should prioritize improving your score from 680 to 740 if you plan to borrow within the next 12 to 24 months. This improvement window matters because hard inquiries temporarily lower your score, so you want to reach your target before applying for major credit. Focus first on reducing your credit utilization across all accounts, as this factor accounts for 30 percent of your score and responds quickly to debt paydown. Second, maintain zero late payments for the next six months minimum, as payment history weighs 35 percent. Third, avoid applying for new credit unless absolutely necessary.

If you live in Alberta or Saskatchewan where the provincial average sits at 658, hitting 700 puts you above your local benchmark and materially improves your borrowing power. A borrower in Toronto with a 700 score sits below the city average of 696, but functionally you remain competitive. Lenders don’t view your score in isolation; they compare it against their internal risk models and the borrower pool they’re currently serving. This means your 700 score carries more weight when interest rates are rising and lenders tighten standards than when rates are falling and competition loosens.

Check your actual score across multiple bureaus before applying for any major credit product. Equifax offers daily updates with paid monitoring, while Borrowell provides free weekly updates. Seeing your score from multiple sources prevents surprises when a lender pulls a different bureau’s data than you expected. Once you understand your current position across these bureaus, you can move forward with a concrete strategy to address the specific factors holding your score back.

How to Boost Your Credit Score Fast

Target Payment History and Utilization First

Payment history accounts for 35 percent of your score, but most borrowers waste energy here because they assume one missed payment destroys everything. The reality is harsher and simpler: lenders care about your recent behavior far more than ancient history. A late payment from six months ago matters significantly more than one from three years ago. If you’ve missed payments recently, stop that pattern immediately-lenders notice when you correct course. Your next six months of on-time payments move the needle faster than dwelling on past mistakes.

If your payment history is already clean, shift focus to credit utilization instead. Credit utilization below 30 percent can boost your score by 20 to 50 points within weeks. This matters because utilization responds instantly to your actions, unlike payment history which requires months of perfect behavior. If you’re sitting at a 680 and need to reach 720 before applying for a mortgage, reducing utilization from 65 percent to 25 percent across your cards often accomplishes this in 30 to 60 days.

The tactical approach here is to pay down your highest-balance card first, not because it matters mathematically, but because watching one card drop to zero utilization provides psychological momentum to tackle the others.

Check Your Credit Report for Errors

Monitoring your credit report for errors separates borrowers who gain 10 points from those who gain 50. You can check your full report for free once yearly from Equifax and TransUnion, and inaccurate information on these reports directly damages your score. Common errors include accounts you’ve closed still appearing as open, payment dates recorded incorrectly, or fraudulent accounts opened in your name. Disputing these errors takes weeks but costs nothing, and successful disputes remove negative information immediately.

The problem most borrowers face is they never check their reports in the first place. Equifax allows free online access with account registration, while TransUnion offers free scores to Quebec residents specifically. Services like Borrowell provide weekly score updates at no cost, letting you track your progress as you execute your improvement strategy.

Manage Hard Inquiries Strategically

Hard inquiries represent a critical tactical lever, and this is where borrowers sabotage themselves without realizing it. Each application for new credit temporarily lowers your score by five to ten points, but the real damage happens when you apply for multiple products within a short window. Lenders interpret this as desperation and assume you’re taking on debt recklessly.

If you plan to apply for a mortgage, avoid applying for credit cards, personal loans, or car financing for at least three months beforehand. This waiting period allows hard inquiries to age off your report and gives your score time to recover from the utilization improvements you’ve made.

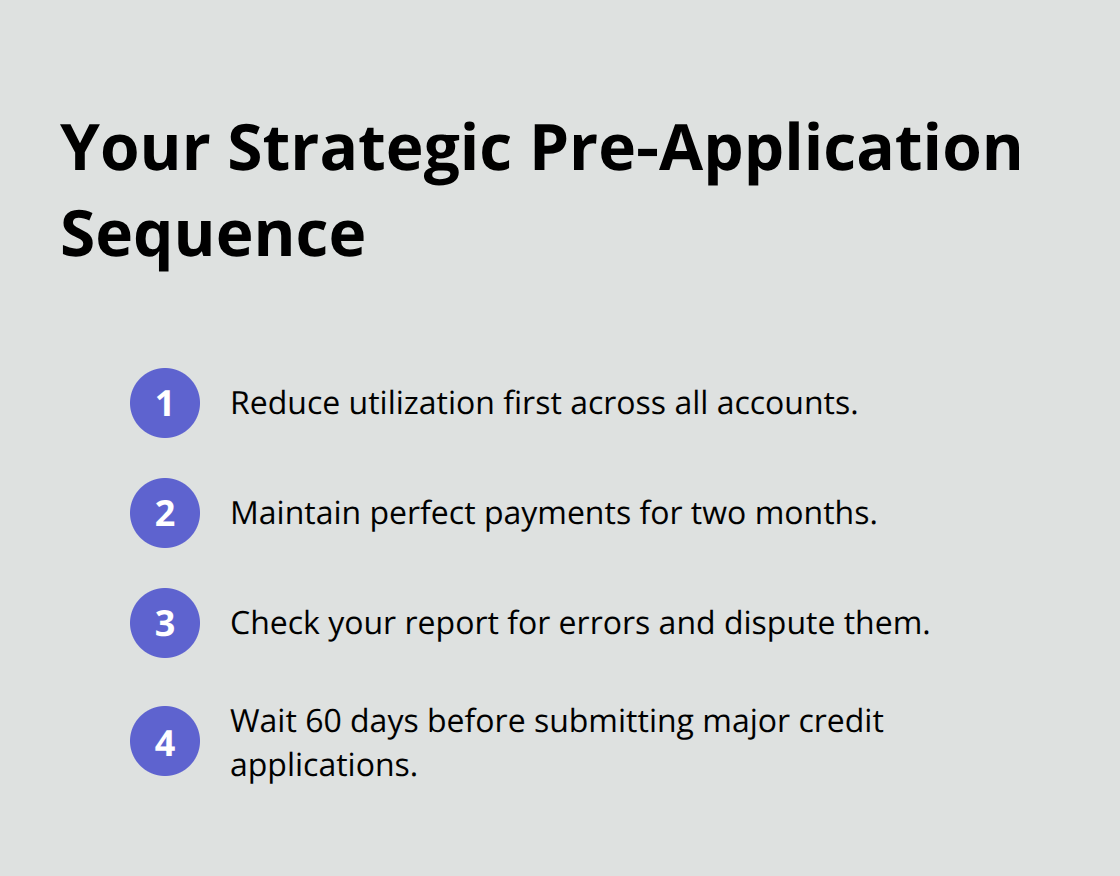

The strategic sequence is: reduce utilization first, maintain perfect payments for two months, check your report for errors and dispute them, then wait 60 days before submitting any major credit applications.

Final Thoughts

Your credit score isn’t abstract financial theory-it’s the number that determines whether you qualify for a mortgage, what interest rate you’ll pay, and how much money stays in your pocket over the next 25 years. The average credit score in Canada sits at 760, but that benchmark only matters if you understand where you stand relative to it and what actions move your score upward. We at Financial Canadian believe the most important insight from this guide is that your score responds to deliberate action, not wishful thinking.

You’re not stuck with whatever number appears on your report today. Reducing credit utilization from 60 percent to 25 percent boosts your score by 30 to 50 points within weeks. Maintaining perfect payments for six months signals to lenders that you’ve corrected past mistakes. Disputing errors on your credit report removes negative information that shouldn’t be there in the first place (and these errors are far more common than most borrowers realize). These aren’t theoretical improvements-they’re concrete steps that produce measurable results.

Start by checking your actual score across multiple bureaus this week, since Equifax and TransUnion both offer free access to your report annually, and services like Borrowell provide weekly updates at no cost. Once you see your current position, identify which factor is holding you back most severely, then execute a focused three to six month improvement plan before you apply for major credit. Financial Canadian offers comprehensive resources to help you navigate your financial decisions with confidence and clarity.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment