Debt can feel overwhelming, but you don’t need to pay for help to turn things around. At Financial Canadian, we’ve compiled the free resources available across Canada that can guide you toward financial stability.

Whether you’re struggling with credit card balances, student loans, or multiple debts, legitimate counselling services and government programs exist to support you at no cost. This guide shows you exactly where to find them and how to use them effectively.

Where to Find Free Debt Counselling in Canada

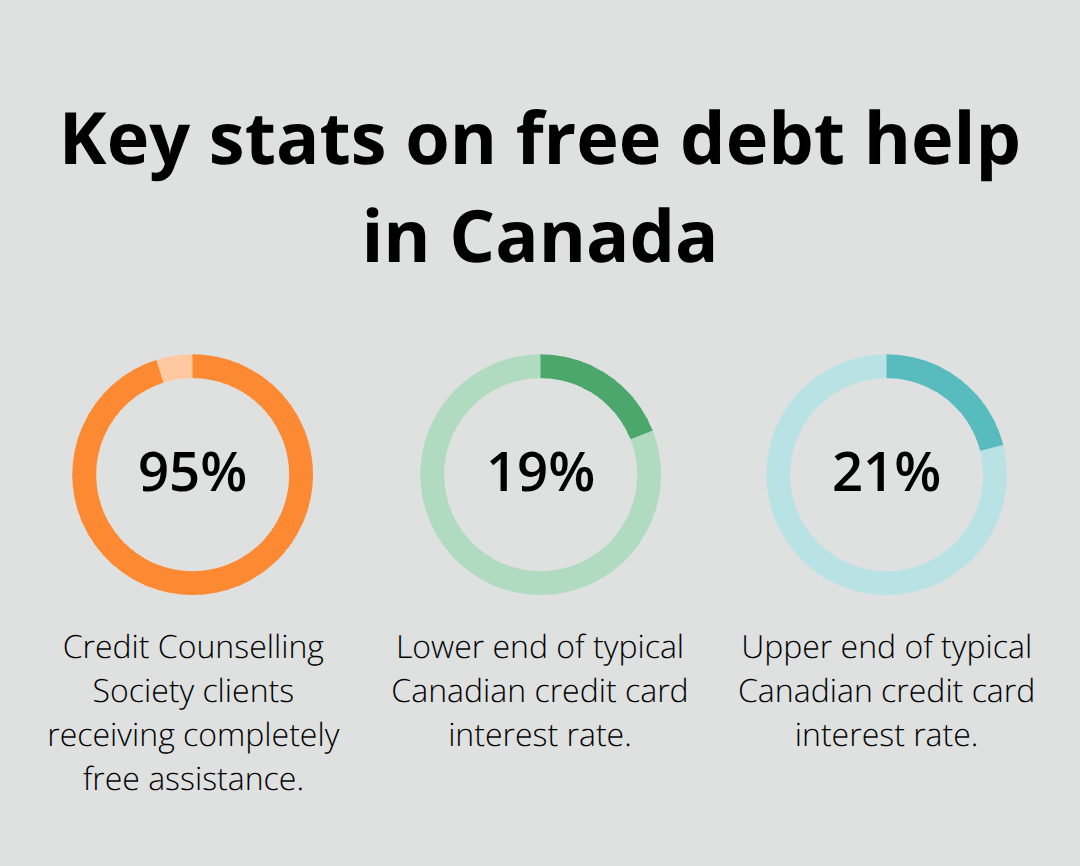

Canada’s non-profit debt counselling sector has operated for decades with a clear mandate: help people without charging fees. The Credit Counselling Society has provided free credit counselling across Canada for 29 years, with about 95% of clients receiving completely free assistance. Credit Canada, the country’s longest-standing non-profit credit counselling agency, has delivered free one-on-one financial counselling with certified counsellors for over 60 years. Both organizations operate on a non-profit model, which means their counsellors earn salaries rather than commissions, removing the financial incentive to steer you toward expensive solutions.

This structural difference matters significantly-when a counsellor’s paycheck doesn’t depend on what product you choose, the advice you receive is genuinely independent.

Licensed Insolvency Trustees Provide Free Initial Assessments

Canada’s most regulated debt professionals are Licensed Insolvency Trustees, the only fully regulated debt help professionals in the country. They provide free, impartial consultations at no cost, making them an excellent starting point if you’re considering formal debt relief options like a Consumer Proposal or bankruptcy. Unlike credit counsellors, whose training and credentials vary across provinces, Licensed Insolvency Trustees must meet strict federal standards. You can locate a trustee in your province through official directories, and the consultation itself carries zero financial obligation. This free assessment helps you understand whether formal options apply to your situation or whether counselling alone will work better.

Non-Profit Organizations Offer Comprehensive Debt Solutions

The Credit Counselling Society operates in all provinces and territories, from BC to Nunavut, meaning geographic location shouldn’t prevent you from accessing help. Their Debt Management Program consolidates credit card payments into a single monthly payment, often with no interest or significantly reduced rates. Credit Canada similarly offers Debt Consolidation Programs that can reduce or eliminate interest on unsecured debts while consolidating them into one payment. Both organizations provide free tools beyond counselling-budget calculators, expense trackers, and financial workshops-so you can start taking action immediately without waiting for an appointment. The Credit Counselling Society publishes its books to external auditors annually and holds the Better Business Bureau’s highest rating, reflecting genuine accountability. If you need immediate help, calling 1-888-527-8999 for the Credit Counselling Society or 1-800-267-2272 for Credit Canada connects you with a counsellor without appointment requirements.

What Comes Next in Your Debt Relief Journey

These free resources form the foundation of your debt relief strategy, but understanding which option fits your specific situation requires a closer look at the actual support programs available to you.

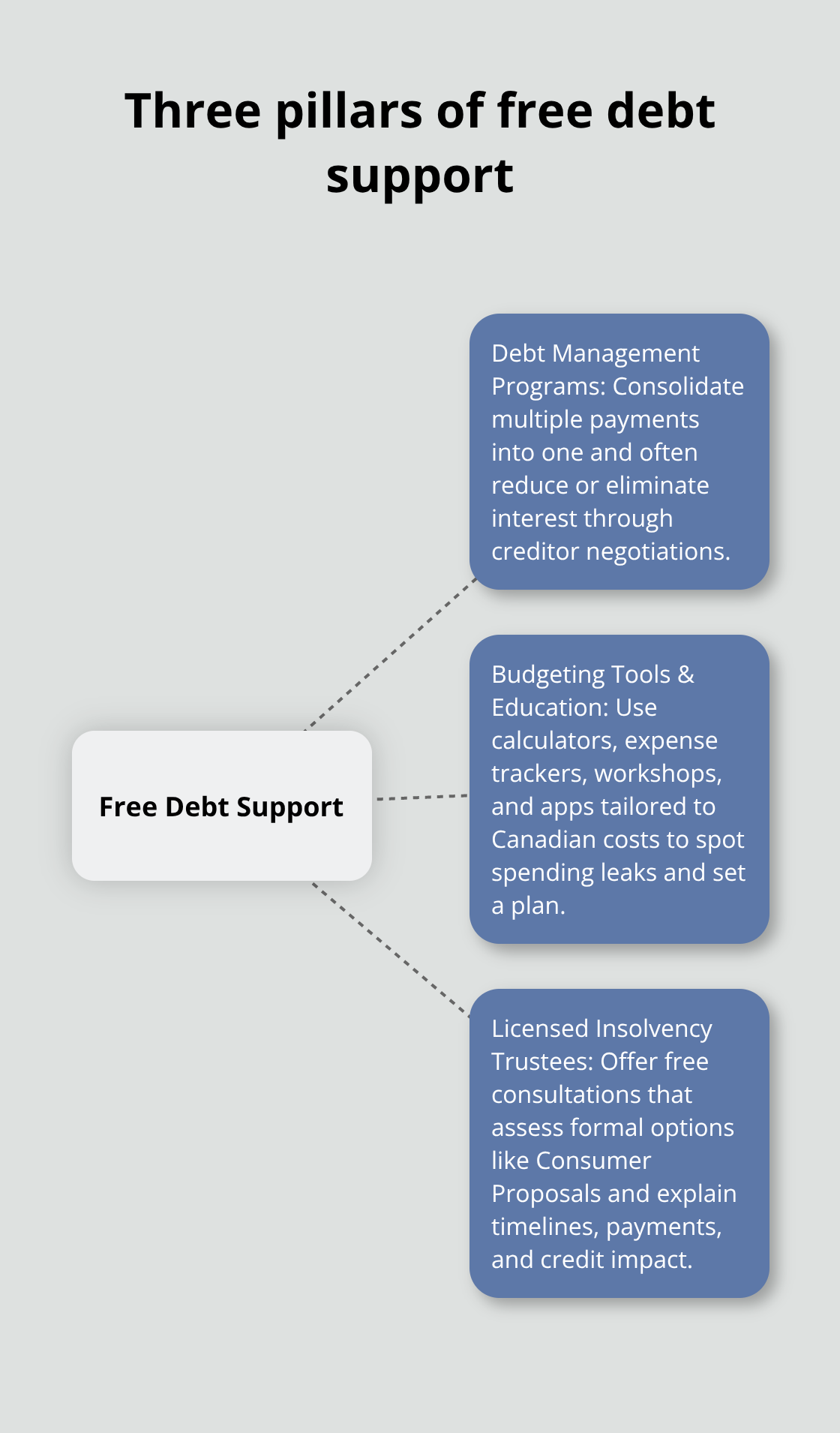

What Free Debt Support Actually Does for You

How Debt Management Programs Reduce Your Interest Burden

Debt Management Programs offered by organizations like the Credit Counselling Society and Credit Canada work differently than most people expect. Rather than simply advising you to pay down debt faster, these programs actively negotiate with your creditors on your behalf. The Credit Counselling Society’s program consolidates multiple credit card payments into one monthly payment, frequently at zero interest or dramatically reduced rates. This matters because the average Canadian carrying credit card debt pays interest rates between 19-21%, meaning a $10,000 balance costs you roughly $1,900-$2,100 annually in interest alone. When a program eliminates or reduces that interest, you redirect that money directly toward principal. Credit Canada’s debt consolidation program similarly reduces or eliminates interest while combining payments, with the added benefit that you qualify even with poor credit history. The practical advantage is immediate: one payment replaces five or ten separate ones, eliminating the cognitive load of tracking multiple due dates and making it harder to miss a payment.

Budgeting Tools Help You Identify Hidden Spending Patterns

Budgeting tools and financial education form the second pillar of free support, but they only work if you actually use them consistently. The Credit Counselling Society provides budget calculators, expense trackers, and financial workshops at no cost, while Credit Canada offers similar tools including their free Butterfly budgeting app specifically designed for newcomers to Canada. These aren’t generic spreadsheets-they’re built around Canadian living costs and help you identify spending leaks most people miss. When you enter your actual expenses into these tools, you typically discover patterns that help redirect your spending more effectively.

Licensed Insolvency Trustees Assess Your Formal Options

Licensed Insolvency Trustees provide the most direct path for formal options: their free consultations assess whether a Consumer Proposal makes sense for your situation. A Consumer Proposal is a legally binding agreement between you and your creditors to repay a percentage of what you owe in exchange for full debt forgiveness. The trustee explains the timeline, monthly payment amount, and credit impact upfront, giving you concrete numbers rather than vague promises. This free assessment costs nothing and carries no obligation to proceed, yet it provides clarity that most debtors lack when they’re drowning in multiple accounts.

Understanding which of these three support pillars applies to your situation depends on where you stand financially right now-and that’s exactly what the next section addresses.

Getting Started With Free Debt Counselling

Verify Legitimacy Before You Commit

Legitimate debt counselling organizations in Canada operate under strict accountability standards, and identifying them protects you from predatory services charging hidden fees. The Credit Counselling Society and Credit Canada both hold the Better Business Bureau’s highest ratings and submit to annual external audits, meaning independent verification confirms their practices. Licensed Insolvency Trustees must meet federal standards and appear on official government registries, making verification straightforward. When you contact an organization, ask directly whether they operate as non-profit, whether counsellors earn salaries rather than commissions, and what their actual fee structure is. If someone promises to eliminate debt through a government grant or claims a guaranteed outcome, that’s a red flag-no legitimate Canadian program works that way. The Credit Counselling Society reports that about 95% of their clients receive completely free assistance, with fees only applying if you enroll in their Debt Management Program (which remains optional).

This transparency signals an organization prioritizing client welfare over revenue extraction.

Prepare for Your Initial Assessment

Your first conversation with a counsellor involves answering straightforward questions about your income, expenses, and debt amounts. Credit Canada’s assessment quiz takes four questions and identifies which options actually apply to your situation before you speak with anyone. During the session itself, the counsellor will review your budget, identify where money leaks, and present realistic options rather than pressure you toward a specific product. A counsellor working for a non-profit won’t push you into a Debt Management Program if simple budgeting adjustments could work instead. After this assessment, you’ll understand whether you need ongoing counselling, a debt consolidation program, or a formal option like a Consumer Proposal.

Take Action Immediately After Your Session

Implement whatever plan emerges from that conversation right away-whether that’s using a budget calculator, stopping credit card usage, or calling a Licensed Insolvency Trustee for a formal assessment. The Credit Counselling Society’s phone line at 1-888-527-8999 and Credit Canada’s line at 1-800-267-2272 both offer callback options if you can’t speak immediately, eliminating delays in availability. These organizations don’t require appointments, meaning you can start your assessment process today without waiting weeks for an opening.

Final Thoughts

Free debt advice Canada offers real solutions without the financial burden of paid services. Contact the Credit Counselling Society at 1-888-527-8999 or Credit Canada at 1-800-267-2272 today, and both organizations offer callback options if you can’t speak immediately. During your initial assessment, you’ll answer basic questions about your income, expenses, and debts, then receive a clear picture of which options actually apply to your situation-this conversation costs nothing and carries no obligation to proceed further.

Legitimate organizations like the Credit Counselling Society and Credit Canada operate across every province and territory, providing counselling, budgeting tools, and formal debt relief options at zero cost. Non-profit organizations publish audited financial statements, hold Better Business Bureau ratings, and structure counsellor compensation around salaries rather than commissions, which means the advice you receive prioritizes your financial recovery. Licensed Insolvency Trustees add another layer of support through free assessments that clarify whether formal options like Consumer Proposals fit your situation.

Building long-term financial stability starts with understanding your current position and taking action immediately. Whether you implement budgeting changes, enroll in a Debt Management Program, or pursue a Consumer Proposal, the momentum matters more than perfection. If you’re building a financial presence online, Financial Canadian offers web design services that help establish credibility and reach your audience.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment