When you need cash fast, payday loans can feel like your only option. But the fees and interest rates can trap you in a cycle that’s hard to escape.

At Financial Canadian, we’ve reviewed the best payday loans in Canada to help you understand what you’re actually paying for. This guide breaks down how these loans work, compares top lenders, and shows you alternatives that might save you money.

How Payday Loans Actually Work

A payday loan in Canada is a short-term, unsecured cash advance that you repay by your next payday. The loan amounts typically range from $20 to $3,000 per transaction, though some lenders offer installment loans up to $25,000 with longer repayment terms stretching from 6 to 84 months. The catch lies in the cost structure. Ontario regulations cap the maximum borrowing cost at $14 per $100 borrowed, which sounds modest until you calculate the annual percentage rate. For a two-week $300 payday loan in Ontario, you’ll pay roughly $42 in fees, translating to an APR of approximately 365%. In other provinces, the effective costs climb even higher: Alberta payday loans hover around 121.67% APR for short-term borrowing, while Manitoba reaches 425.83% APR for very short loan periods. Installment loans carry APRs between 34.56% and 34.95%, which is substantially lower than payday products but still significantly higher than traditional bank loans. If you borrow $4,500 over 36 months through an installment loan, your monthly payments land around a few hundred dollars, illustrating how the compounding effect of high APRs impacts your wallet over time.

The Application Process and Speed

The application process is deliberately streamlined because speed is the main selling point. You need to be at least 19 years old, have proof of steady income, and maintain an active bank account with three to six months of transaction history. Most lenders don’t require a credit check, instead prioritizing your current income and employment status over your credit score, which means approval rates are high even for people with bad credit. Online applications take five to ten minutes and are available 24/7, including weekends and holidays. Funding typically arrives within 15 minutes to 24 hours via Interac e-Transfer, depending on when you apply and which lender you choose. Understanding eligibility requirements helps you prepare the right documentation before applying.

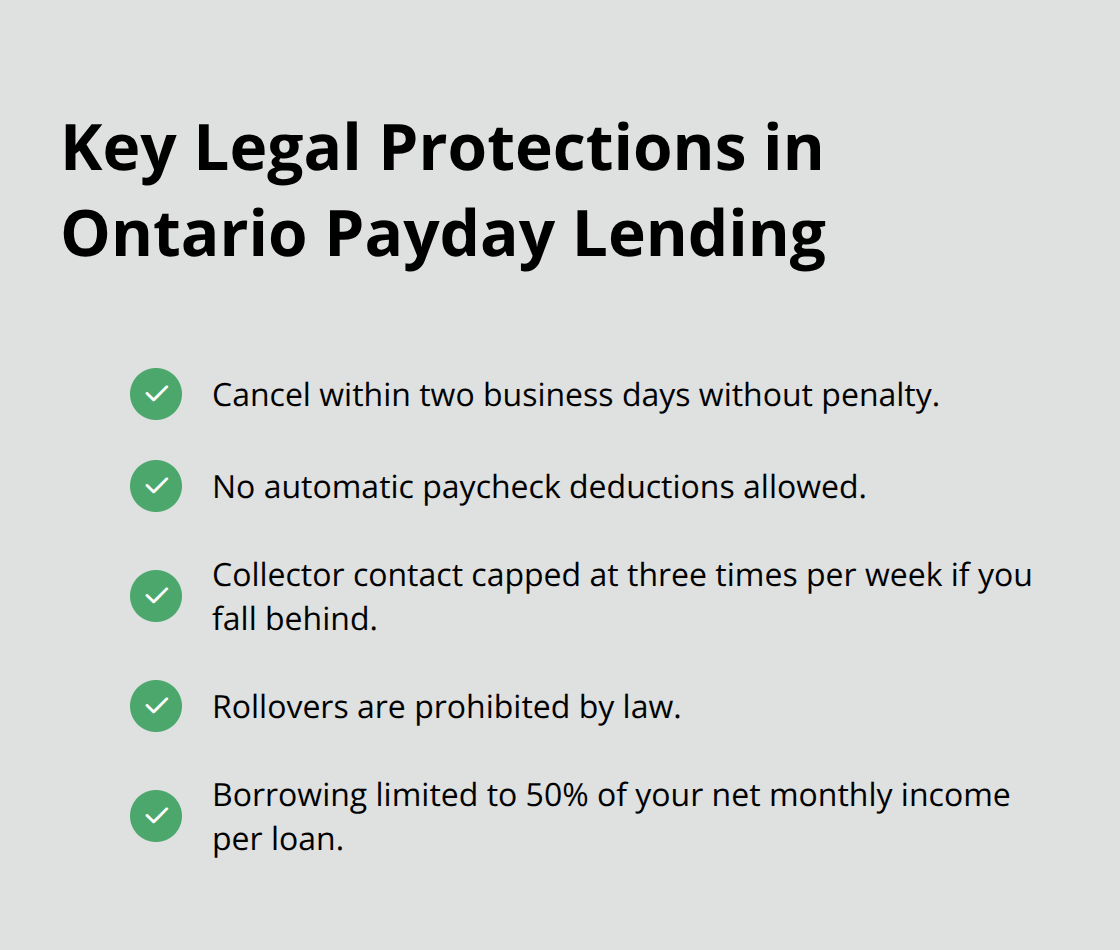

Repayment Options and Legal Protections

The flexibility in repayment schedules includes weekly, bi-weekly, monthly, and bi-monthly payment options, which gives you some control over how you manage the debt. Ontario’s Payday Loans Act protects you with specific safeguards: you have two business days to cancel without penalty, lenders cannot require automatic paycheck deductions, and they’re capped at contacting you no more than three times per week if you fall behind. The law also prevents rollovers and limits how much you can borrow to 50% of your net monthly income per loan, a rule designed to prevent the debt spiral that catches many borrowers. These protections exist because payday loans carry real risks, which is why understanding what lenders offer becomes essential before you commit to any agreement.

Which Payday Lender Actually Delivers

Money Mart: Canada’s Longest-Standing Option

Money Mart has operated since 1982 with both online and in-store locations across the country, making it the most established player in Canada’s payday lending space. The lender offers two distinct products: Payday Boost loans ranging from $100 to $1,500 for short-term borrowing, and Installment Loans from $500 to $25,000 with repayment terms stretching from 6 to 84 months. For Payday Boost, the APR varies dramatically by province-Alberta borrowers face around 121.67% APR, while Ontario and Saskatchewan sit closer to 365% APR, and Manitoba reaches 425.83% APR for very short loan periods. Installment Loans carry more moderate APRs between 34.56% and 34.95%, making them genuinely cheaper if you can tolerate longer repayment schedules.

Speed and Eligibility at Money Mart

Money Mart’s funding speed is competitive: Interac e-Transfer deposits typically arrive within 24 hours on weekdays, though applications processed after hours or on weekends may take until the next business day. The eligibility check happens instantly online without impacting your credit score, and new customers receive a promotional $300 first-time Payday Boost offer in participating provinces. However, Payday Boost is unavailable in Newfoundland and Labrador, New Brunswick, and Quebec, so geography matters significantly when you choose this lender. The Payday Protection Plan option, underwritten by Canadian Premier Life Insurance Company, covers loan payments during job loss, injury, sickness, or death-a genuine safety net for people with unstable employment.

Beyond Loans: Money Mart’s Additional Services

Money Mart operates beyond loans, offering MoneyGram transfers, currency exchange, bill payment, and cheque cashing in-store, which matters if you need multiple financial services in one location. For a concrete comparison, a $4,500 installment loan over 36 months costs roughly $14 per $100 borrowed through the fee structure, translating to monthly payments in the hundreds.

Online-Only Competitors and Their Trade-Offs

Online lenders across Canada typically promise 15-minute funding via e-Transfer for loans up to $3,000, with no credit check required and approval rates above 90% for employed borrowers with active bank accounts. These faster online-only competitors emphasize convenience over branch access, making them ideal if you need cash outside traditional banking hours. Direct deposit funding takes longer than e-Transfer but offers another option for those without immediate online payment access. In-store borrowing through Money Mart provides face-to-face service and immediate cash access, though you sacrifice the 24/7 availability of online-only platforms.

Choosing Your Lender and Avoiding Predators

The real decision comes down to what you prioritize: Money Mart’s established reputation and dual online-plus-branch presence versus faster e-Transfer competitors if you’re comfortable handling everything digitally. Avoid any lender that isn’t licensed in your province-verify through your provincial regulator before you apply, as unlicensed operators expose you to predatory terms and potential identity theft through data-selling schemes. Once you’ve selected a lender and understand the costs involved, the next step requires you to recognize which situations actually warrant a payday loan and which alternatives might serve you better.

Better Options Than Payday Loans

Before you lock into a payday loan at 365% APR, explore what banks, employers, and credit unions actually offer. The alternatives cost substantially less and often arrive faster than you’d expect.

Personal Lines of Credit from Your Bank

A personal line of credit from your bank costs dramatically less than payday borrowing. Most Canadian banks offer unsecured lines of credit with APRs between 7% and 21%, depending on your credit score and income. If you have decent credit, a bank line of credit at even 15% APR saves you roughly $300 in interest compared to a $300 payday loan over two weeks. The application takes longer than a payday loan-typically three to five business days-but if your emergency isn’t truly immediate, this delay pays off. Ask your bank whether you qualify for a pre-approved line of credit, since many institutions offer these without a full application process. Some banks also offer overdraft protection, which functions as an emergency buffer without the predatory costs of payday products.

Salary Advances From Your Employer

Your employer represents an overlooked resource. Roughly 40% of Canadian employers offer salary advance programs, where you receive a portion of your earned wages before payday without fees or interest.

Companies like Wagepoint and Instant Financial manage these programs for employers, and the advance costs you nothing except the wait until your regular payday. If your workplace uses one of these platforms, you access your money within 24 hours at zero cost-far superior to any payday lender. Ask your HR department directly whether this option exists at your company, since many employees never discover it.

Credit Union Loans and Emergency Assistance

Credit unions across Canada operate under different regulations than banks and frequently offer emergency loans at lower rates than traditional banks. The Canadian Credit Union Association reports that credit union personal loans offer competitive rates, with faster approval than banks and more flexibility for people with imperfect credit. Credit unions also offer emergency assistance programs specifically designed to help members avoid payday loans during temporary hardship. Saskatchewan Credit Union, for example, offers emergency loans up to $2,500 at preferential rates for members facing unexpected expenses. Contact your local credit union directly to ask about emergency lending products, since these programs vary significantly by institution and aren’t always advertised prominently online.

The Real Cost Comparison

A $1,000 payday loan costs $140 in fees over two weeks; the same amount borrowed through a credit union at 12% APR costs roughly $23 for two weeks. Even if you need the money slightly faster, the cost difference justifies waiting an extra day or two for approval.

The only scenario where a payday loan makes sense is when all alternatives have genuinely failed and you face immediate consequences like eviction or disconnection of essential services. Most people discover too late that their employer, bank, or credit union would have solved the problem at a fraction of the cost. Make those calls first, before you apply anywhere else.

Final Thoughts

Payday loans should only enter your decision-making after you’ve exhausted every legitimate alternative and face immediate financial consequences. Your employer may offer a salary advance at zero cost, your bank might approve a line of credit at a fraction of payday rates, or your credit union could provide emergency lending faster than you’d expect. The best payday loans Canada offers still cost far more than these options, which is why they should be your last resort, not your first call.

Red flags appear immediately when you encounter unlicensed lenders, pressure tactics, or promises of guaranteed approval without income verification. Legitimate lenders verify your employment and income because they want repayment, not because they’re trying to trap you. If a lender contacts you repeatedly, threatens wage garnishment, or demands payment from family members, they’re breaking provincial law-report them to your provincial regulator and stop communication.

The financial moves that actually work involve building a safety net before emergencies hit. Open a line of credit with your bank while you have stable employment and good credit, ask your employer about salary advances and other employee benefits you might have overlooked, and join a credit union if your current bank doesn’t offer competitive rates on emergency borrowing. We at Financial Canadian help you build a strong financial foundation through expert guidance and resources designed to keep you out of high-cost debt traps.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment