Buying your first home is one of the biggest financial decisions you’ll make. At Financial Canadian, we know that navigating a first time mortgage in Canada can feel overwhelming without the right guidance.

This guide walks you through everything you need to know-from understanding mortgage types to preparing your finances and completing your application. By the end, you’ll have a clear roadmap to secure your first home loan.

Understanding Mortgage Types in Canada

When you’re ready to buy your first home, mortgage structures trip up most first-time buyers. Canada’s mortgage market offers three primary options: conventional mortgages, insured mortgages, and alternative mortgages. A conventional mortgage requires a down payment of at least 20 percent of the purchase price, which lets you avoid mortgage insurance altogether. If your down payment falls below 20 percent, you’ll need mortgage insurance from providers like CMHC, Sagen, or Canada Guaranty. These insurance premiums get added directly to your loan amount, increasing what you’ll ultimately pay.

An insured mortgage is often the only realistic path for first-time buyers since saving 20 percent takes years for most people. Alternative mortgages exist but typically come with higher interest rates and stricter qualification requirements, so they’re worth avoiding unless you have specific circumstances that prevent traditional financing.

Fixed Rates Protect Your Budget

The fixed-rate versus variable-rate decision matters far more than most people realize. With a fixed-rate mortgage, your interest rate stays locked in for your entire term, meaning your monthly payment never changes regardless of what happens in the broader economy. This predictability is invaluable for budgeting and financial planning. Variable-rate mortgages fluctuate with prime lending rates, which means your payment can increase substantially if rates climb. Since 2022, rates have been volatile and unpredictable, making fixed rates the safer choice for first-time buyers who can’t absorb payment shocks. The rate difference between fixed and variable might look tempting on paper, but that savings evaporates quickly if rates spike.

Amortization Periods Shape Your Long-Term Costs

Your amortization period determines how long you’ll take to pay off the mortgage completely. Standard amortization runs 25 years for most borrowers, but first-time buyers and those with newly built properties can stretch this to 30 years according to federal guidelines. A longer amortization means lower monthly payments but significantly higher total interest paid over the life of the loan. A 30-year amortization versus a 25-year one on a $400,000 mortgage adds substantially more in total interest costs. If you can afford the higher payments of a shorter amortization, that’s the smarter financial move. Many lenders will let you adjust your amortization term during renewal, so starting with 30 years doesn’t lock you in forever if your financial situation improves.

Now that you understand the mortgage structures available to you, the next critical step involves preparing your finances to qualify for the amount you need.

Prepare Your Finances Before Applying

Check Your Credit Score and Fix Problems

Your credit score determines whether you’ll qualify for a mortgage and what interest rate you’ll pay. Lenders pull your credit report to assess risk, and even a 50-point difference costs you thousands in interest over 25 years. If your score sits below 680, most traditional lenders will reject your application outright.

Check your credit report through Equifax or TransUnion, which you can access free once annually. Look for errors like accounts you don’t recognize or missed payments that aren’t yours-these happen more often than people think and you can dispute them directly with the credit bureau. If your score needs improvement, focus on paying down existing debt before applying.

Carrying high credit card balances signals financial stress to lenders, even if you make payments on time. Try to keep credit utilization below 30 percent of your available limits. This alone can boost your score by 20 to 50 points within a few months. Don’t open new credit accounts or make large purchases on credit during this period, as both actions temporarily lower your score.

Build Your Down Payment Strategically

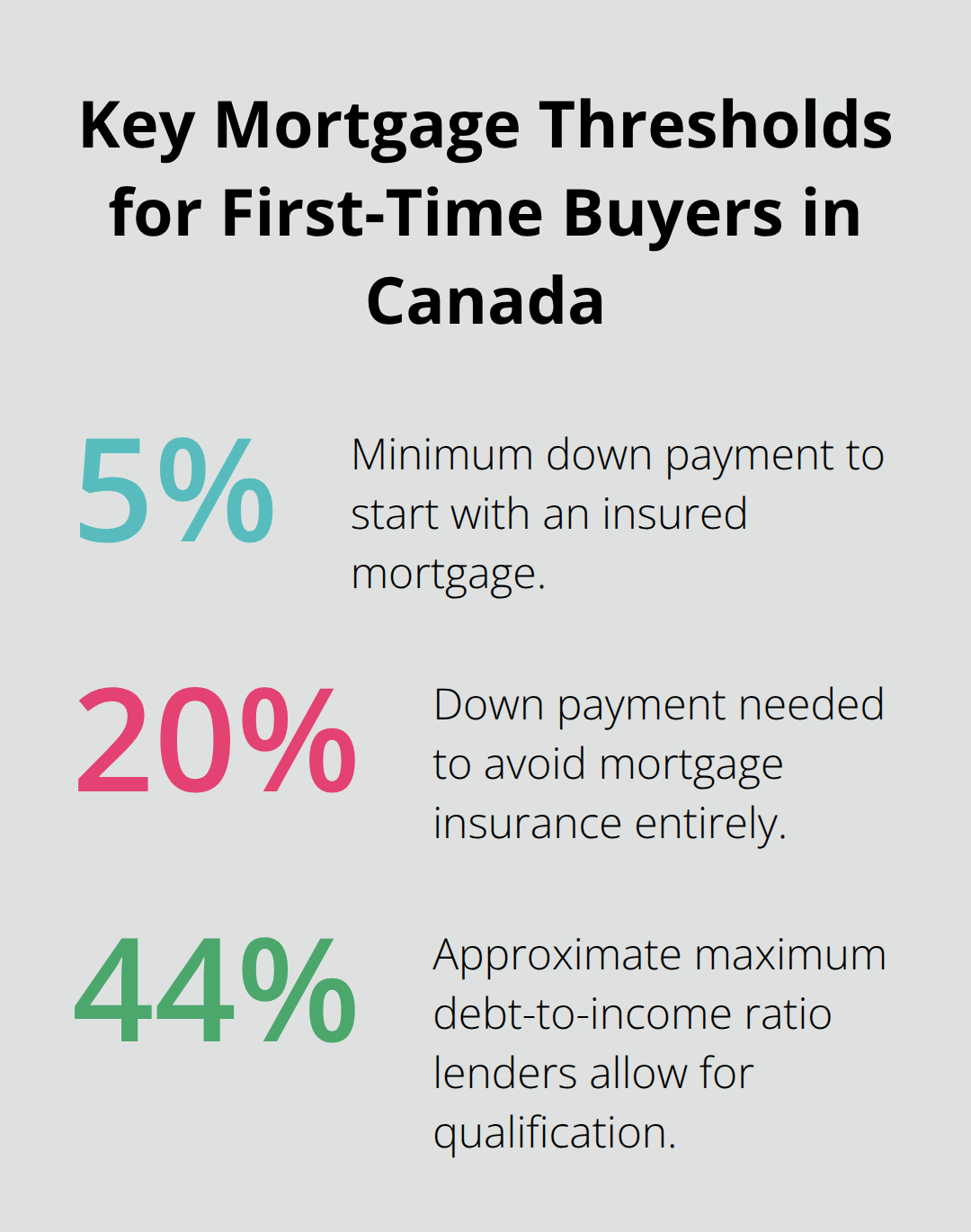

Down payment size directly affects your mortgage costs and qualification odds. Most first-time buyers can start with just 5 percent of the purchase price, but this triggers mandatory mortgage insurance that adds thousands to your loan. A $400,000 home with a 5 percent down payment requires roughly $12,000 in insurance premiums, which gets rolled into your mortgage balance. A 20 percent down payment eliminates mortgage insurance entirely, saving you real money.

Consider tapping your RRSP through the Home Buyers’ Plan, which lets you withdraw up to $60,000 tax-free for your first home-or $120,000 if you’re buying with a partner. You’ll repay this over 15 years starting in year 5, but it’s far cheaper than paying mortgage insurance. Gifts from family count toward your down payment, though lenders require documentation proving the money is a gift, not a loan you’ll need to repay.

Calculate Your Debt-to-Income Ratio

Your debt-to-income ratio caps at roughly 44 percent of your gross household income for mortgage qualification. This means all your debts (car loans, credit cards, student loans, plus your new mortgage payment) cannot exceed 44 percent of what you earn annually. A $100,000 household income supports roughly $44,000 in total annual debt payments.

Calculate this before applying by adding up all monthly obligations and multiplying by 12, then comparing that figure to your annual income. If you’re close to this limit, paying down existing debts strengthens your application and increases your approved mortgage amount. This step separates applicants who get approved from those who face rejection or lower loan offers.

With your finances in order and your credit profile strengthened, you’re ready to move into the mortgage application process itself-where pre-approval becomes your first concrete step toward homeownership.

Moving From Pre-Approval to Final Approval

Pre-approval is where most first-time buyers should start, and it’s non-negotiable if you want to move quickly when you find the right property. A pre-approval letter from your lender confirms the maximum mortgage amount you qualify for and locks in an interest rate for roughly 120 days. This rate hold protects you from market swings during your home search and strengthens your position when making an offer because sellers know you have financing backing. The pre-approval process takes one to three business days and requires basic income verification through recent pay stubs and tax returns. You’ll also need to provide proof of your down payment source, whether that’s savings, RRSP withdrawals via the Home Buyers’ Plan, or family gifts. Pre-approval prevents you from falling in love with a property you can’t actually afford. Once you’ve found your home and your offer is accepted, you move into final approval, which is far more rigorous. Your lender will order a property appraisal to confirm the home’s value matches the purchase price, conduct a thorough title search, and verify every detail you provided during pre-approval. This stage typically takes seven to ten business days and requires additional documentation like proof of homeowner’s insurance quotes and confirmation that you haven’t taken on new debt since pre-approval. Lenders can and do back out during final approval if your credit score drops, you lose your job, or the property appraisal comes in lower than expected.

Collect Your Documents Before You Apply

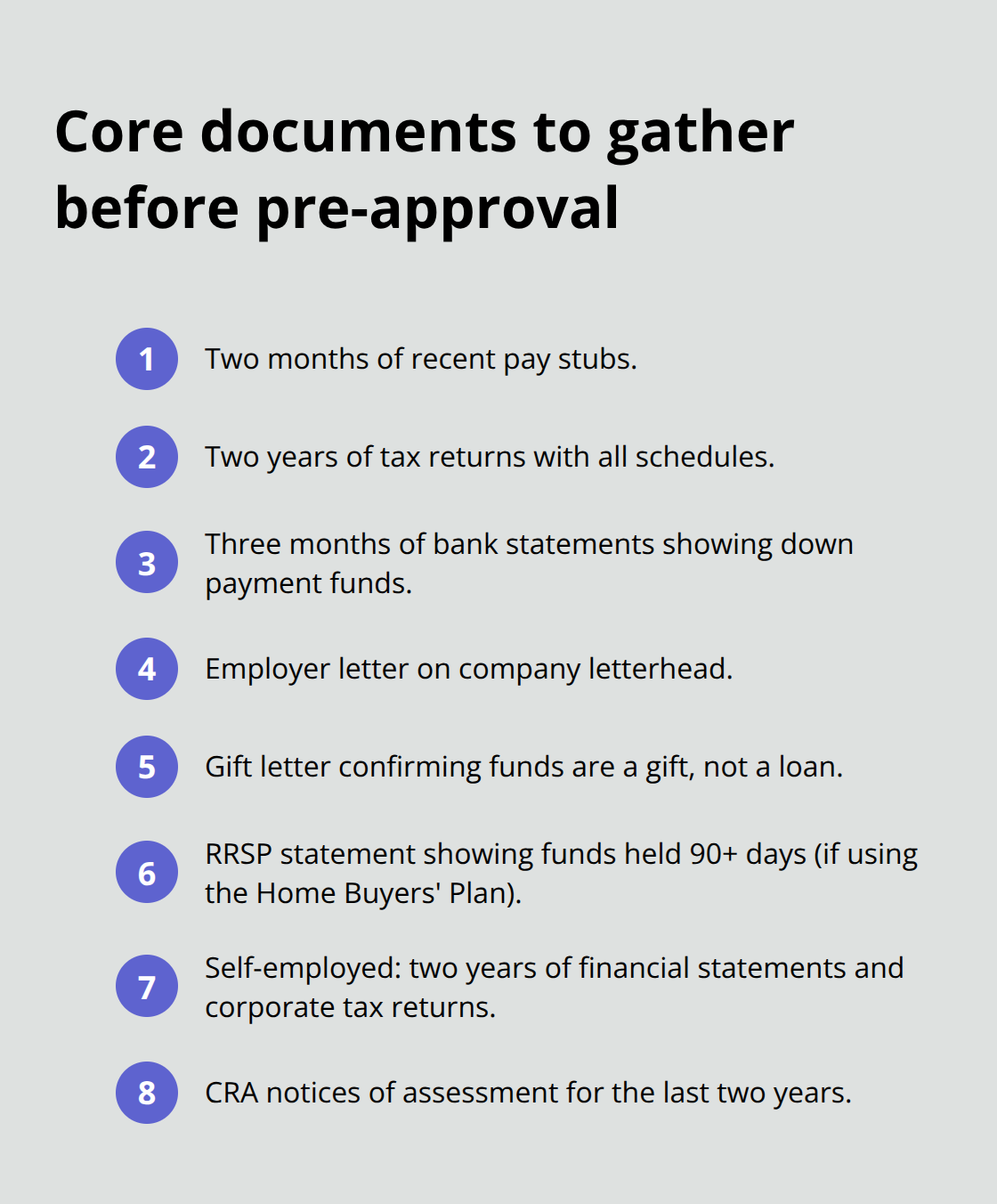

Most first-time buyers underestimate how many documents lenders demand, and delays in providing them can push your closing date back weeks. Start collecting these items before you even apply for pre-approval: two months of recent pay stubs, two years of tax returns with all schedules, three months of bank statements showing your down payment funds, proof of employment from your employer on letterhead, and documentation of any gifts including a signed letter from the gift-giver confirming it’s a gift, not a loan. If you use RRSP funds through the Home Buyers’ Plan, you’ll need your RRSP statement showing the account balance and confirmation that funds have been in the plan for at least 90 days before withdrawal.

Self-employed borrowers face steeper requirements-you’ll need two years of financial statements, corporate tax returns, and notice of assessments from the Canada Revenue Agency. Having these documents organized in one folder before applying accelerates everything and signals to your lender that you’re serious and prepared. Third-party verification takes time, so submitting everything at once rather than trickling documents in over weeks prevents unnecessary delays that could cost you your rate hold or a competitive offer on your chosen property.

Compare Brokers and Direct Lenders

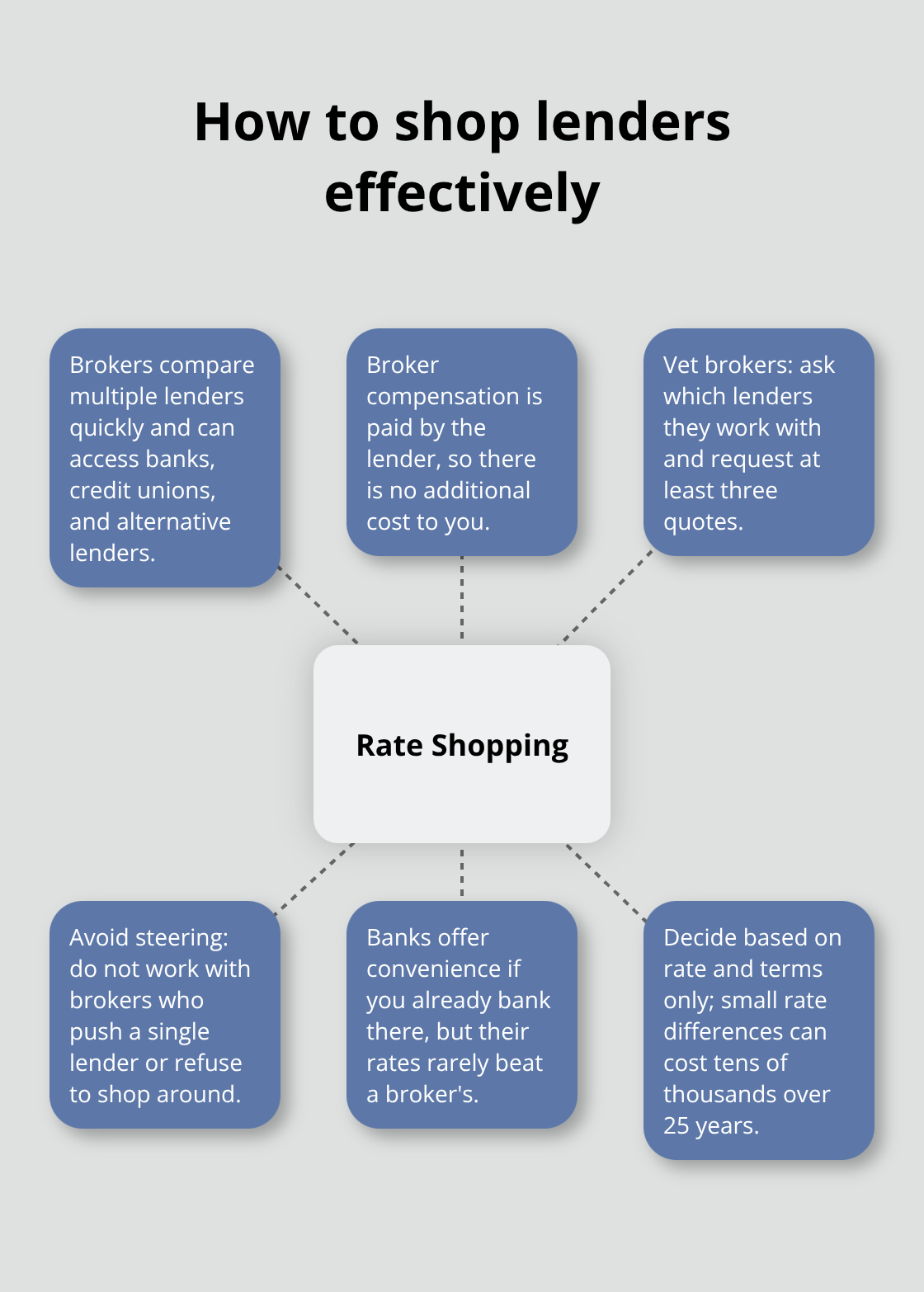

Working directly with a bank feels straightforward but often locks you into that single lender’s rates and terms, which may not be your best option. Mortgage brokers access multiple lenders simultaneously and can compare rates across banks, credit unions, and alternative lenders in hours rather than days. A broker’s compensation comes from the lender, not from you, so there’s no additional cost to using one.

However, not all brokers are equal-some push you toward lenders that pay higher commissions rather than the one offering you the best rate. Interview brokers by asking what lenders they work with and requesting rate quotes from at least three different sources before committing. If a broker refuses to shop around or pressures you toward a specific lender, find someone else. Banks offer convenience if you already have accounts there, but their rates rarely beat what a broker can secure. Your decision should hinge entirely on rate and terms, not loyalty or convenience. The difference between a 4.5 percent fixed rate and a 4.9 percent rate on a $400,000 mortgage costs roughly $15,000 more in interest over 25 years, making rate shopping non-negotiable regardless of which path you choose.

Final Thoughts

Securing your first time mortgage in Canada requires discipline across three core areas: understanding your mortgage options, preparing your finances thoroughly, and executing the application process strategically. Most first-time buyers stumble because they skip the preparation phase and rush into applications unprepared. Your credit score, down payment size, and debt-to-income ratio determine everything about your mortgage approval and interest rate.

Common mistakes derail otherwise qualified buyers. Opening new credit accounts or making large purchases on credit during your mortgage process tanks your score and can trigger lender rejection. Accepting the first mortgage offer you receive without shopping rates across multiple lenders costs you tens of thousands in unnecessary interest, so compare brokers and direct lenders before committing to any single option.

Property taxes, home insurance, maintenance costs, and utilities now fall on you instead of a landlord after your mortgage closes. Budget for annual maintenance at roughly one percent of your home’s purchase price to cover unexpected repairs, and your mortgage advisor should follow up during the first year to discuss payment adjustments if your circumstances change. We at Financial Canadian are here to support your journey with expert guidance and resources tailored to your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment