Debt weighs on millions of Canadians, but you don’t have to figure out your way forward alone. Free debt advice in Canada is more accessible than ever, with non-profit counsellors, government programs, and practical tools ready to help.

We at Financial Canadian have put together this guide to show you exactly how to assess your situation, find the right resources, and build a concrete plan to regain control of your finances.

Map Out Your Debt Before Taking Action

Collect All Your Debt Information

You cannot fix what you don’t measure. Most Canadians underestimate their total debt because they never add up all their obligations in one place. Pull together statements from every creditor-credit cards, lines of credit, personal loans, car payments, and student loans. Write down the balance, interest rate, and minimum payment for each one. This single exercise often reveals which debts actually drain your finances the fastest.

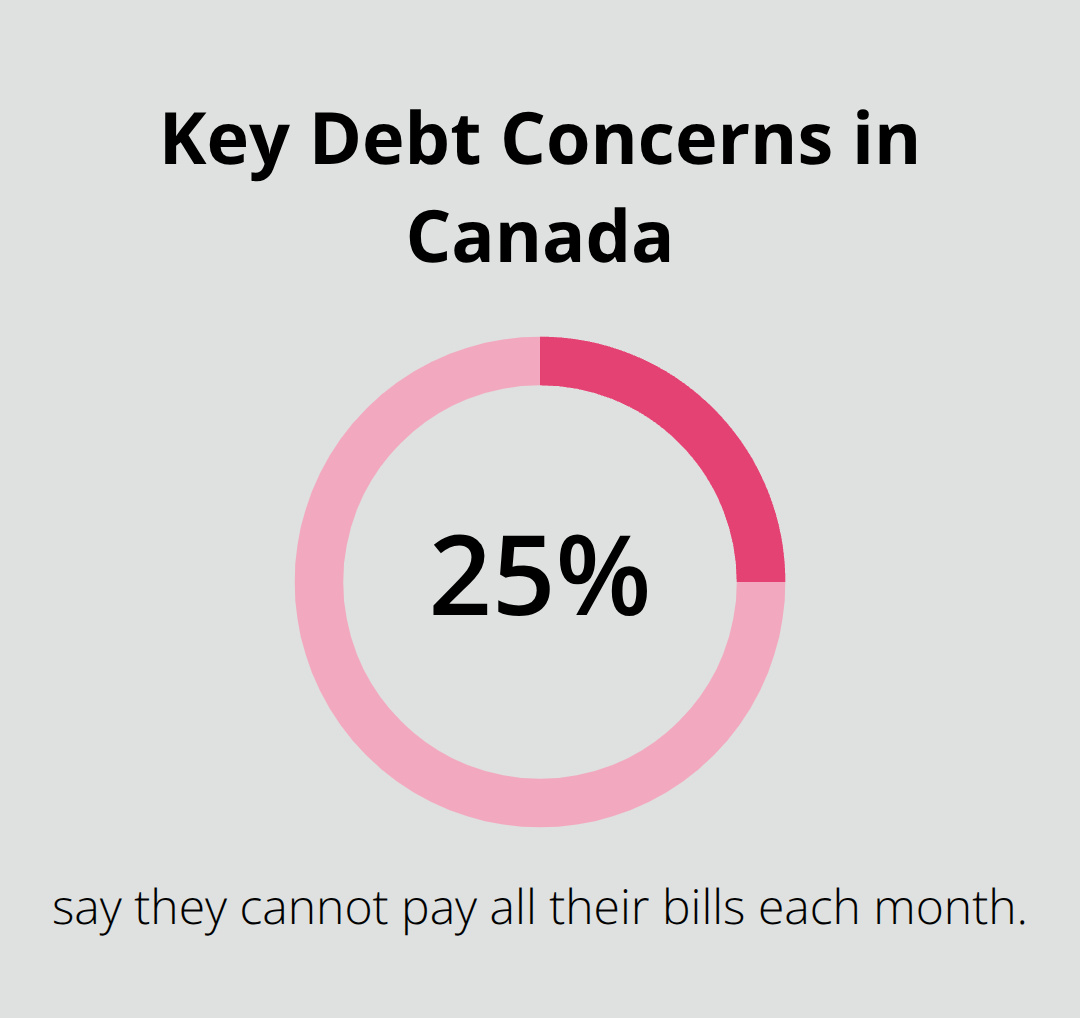

High-interest credit card debt costs far more than a car loan at 6-7%, yet many people focus on paying off the car first. Statistics Canada data shows that almost half of Canadians feel concerned about the amount of debt they carry, and 25% say they cannot pay all their bills each month. These numbers suggest most people have not taken the time to see their full financial picture.

Calculate the True Cost of Minimum Payments

Calculate the total interest you will pay on each debt if you only make minimum payments-this number shocks most people into action. A $5,000 credit card balance at 20% interest with a $100 monthly payment takes over six years to pay off and costs nearly $2,200 in interest alone. That interest represents money you could have used for other goals.

Review Your Monthly Spending Patterns

Next, examine your monthly spending to understand where your money actually goes. Track your expenses for 30 days across groceries, utilities, subscriptions, transportation, and discretionary purchases. You will likely find recurring charges you forgot about-streaming services, gym memberships, or insurance policies that have not been reviewed in years.

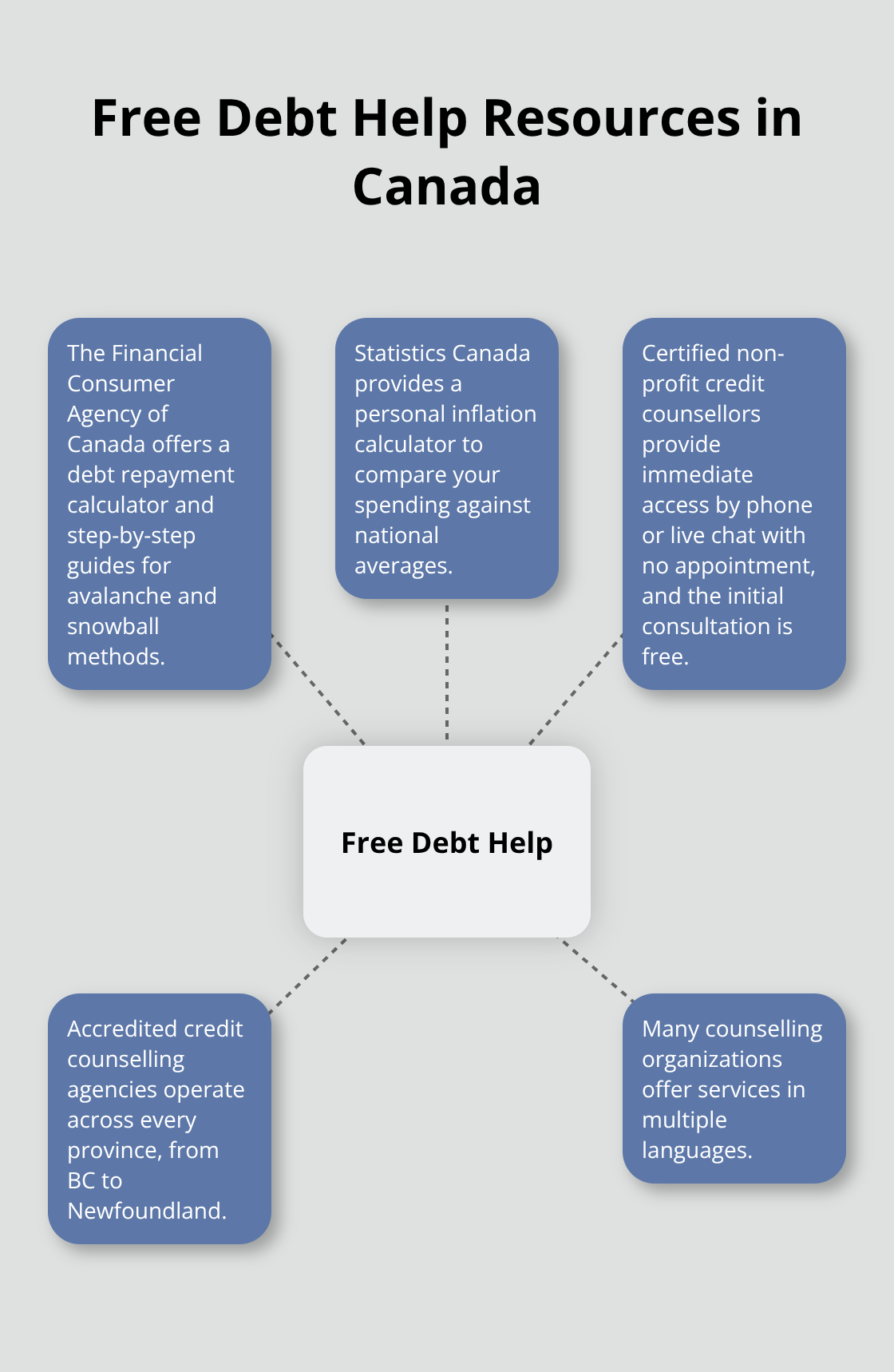

The Financial Consumer Agency of Canada recommends distinguishing between needs and wants to prioritize essential spending and cut non-essentials. This is where most people find quick wins without major lifestyle changes. A subscription audit alone often frees up $50-150 per month that you can redirect toward debt repayment.

Choose Your Repayment Strategy

Once you map your debt and spending, you have the foundation to choose a repayment strategy. The avalanche method targets your highest-interest debts first, saving the most money on interest. The snowball method tackles your smallest balances first, creating psychological momentum through quick wins. Neither approach works without seeing your complete situation first.

If organizing this information feels overwhelming, non-profit credit counsellors across Canada offer free consultations to help you build a personalized assessment. They review your income, expenses, debts, and assets to create a realistic plan tailored to your specific situation, not generic advice that does not fit your life. With your debt mapped and your spending understood, you are ready to explore the free resources available to support your repayment journey.

Where to Find Free Debt Help Right Now

Canada has built a robust network of non-profit credit counselling agencies specifically designed to help people escape debt without charging fees. Credit Counselling Canada accredits these organizations, and they operate across every province from BC to Newfoundland. When you call one of these services, a certified counsellor reviews your complete financial picture-income, expenses, debts, and assets-to build a plan that actually fits your life instead of forcing you into a generic solution.

Access Certified Counsellors at No Cost

The Credit Counselling Society has already helped over 1 million Canadians find their way out of debt, which speaks to how effective this approach is. You receive immediate access via phone or live chat with no appointment needed, and the initial consultation costs nothing. These counsellors explain your options clearly: debt management programs that consolidate multiple payments into one affordable monthly amount, consumer proposals that let you pay a percentage of what you owe, or other strategies based on your specific situation.

Many people avoid calling because they assume counsellors will judge them or push expensive solutions, but these are non-profits with a mission to get you debt-free, not to extract money from you. A counsellor’s role is to listen to your situation and present realistic paths forward tailored to your circumstances.

Use Free Government and Non-Profit Tools

The Financial Consumer Agency of Canada provides free tools including a debt repayment calculator and detailed guides on getting out of debt that walk you through the avalanche and snowball methods step by step. Statistics Canada offers a personal inflation calculator so you can measure your actual spending against national averages and spot where your costs run higher than expected.

These tools work best when combined with a counsellor’s guidance rather than used alone, because tools show you the math while counsellors help you stay committed to the plan when motivation fades. If you speak another language, many counselling organizations provide services in multiple languages.

Take Action This Week

The fastest way forward is to call a non-profit counsellor this week rather than spending months gathering information on your own. You already have the debt mapped from the previous section, so you have everything a counsellor needs to get started immediately. Once you understand your options and select a repayment strategy with professional guidance, you can move into the practical phase of actually executing your plan and tracking your progress toward financial freedom.

How to Pick the Right Debt Payoff Strategy

The avalanche method and snowball method represent two fundamentally different approaches to debt repayment, and the avalanche method delivers superior financial results for most Canadians. With the avalanche method, you attack your highest-interest debts first while maintaining minimum payments on everything else. This approach saves the most money on interest charges over time. If you carry a credit card at 20% interest alongside a car loan at 6%, the avalanche method directs extra payments toward the credit card first, preventing that 20% rate from compounding your debt further.

The snowball method tackles smallest balances first regardless of interest rate, which creates psychological wins through quick payoffs but costs significantly more in total interest. The Financial Consumer Agency of Canada shows that people using the avalanche method save thousands of dollars compared to the snowball approach when debts span multiple interest rates. The math is clear: prioritize interest rate, not balance size, if you want to eliminate debt efficiently.

Negotiate Lower Rates with Your Creditors

Most Canadians never attempt to negotiate lower interest rates with creditors, yet this single conversation can redirect thousands of dollars toward your principal instead of interest payments. Call your credit card company, line of credit lender, or bank directly and ask for a rate reduction. Explain your situation honestly: you have made consistent payments, your financial circumstances are stable, and you want to accelerate repayment.

Credit card companies often reduce rates for customers with decent payment history, especially if you threaten to transfer your balance elsewhere. A rate reduction from 20% to 16% on a $5,000 balance saves over $800 in interest during a three-year repayment period. For car loans and mortgages, your lender has less flexibility, but refinancing with a different institution at a lower rate remains possible if market conditions favor you. Non-profit credit counsellors can also negotiate on your behalf as part of a debt management program, reducing rates further when you commit to a structured repayment plan through their organization.

Create a Realistic Repayment Timeline

Creating a repayment timeline requires brutal honesty about what you can actually afford monthly, not what you wish you could afford. After mapping your budget in the previous section, identify how much extra money you can direct toward debt beyond minimum payments. Most people find $100–300 monthly through expense cuts, and some discover more through negotiating recurring bills.

Use this amount consistently rather than sporadically. A $5,000 credit card balance at 18% interest paid with $200 monthly payments takes 30 months to eliminate, while $300 monthly payments reduce that to 20 months and save $900 in interest.

The Financial Consumer Agency of Canada offers a credit card payment calculator that shows exactly how interest and timeline connect so you understand the real cost of different payment amounts. Set a specific payoff date and track progress monthly against that target.

Most people underestimate how motivating a concrete end date becomes compared to open-ended repayment. If your timeline stretches beyond five years for unsecured debt, consider a consumer proposal or debt consolidation program through a non-profit counsellor, as those options may reduce the total amount you owe and shorten your timeline significantly.

Final Thoughts

Getting out of debt requires sustained effort and realistic expectations rather than quick fixes. Once you execute your repayment plan for several months, momentum builds naturally as balances shrink and interest charges decline. Start setting aside even small amounts into an emergency fund alongside your debt payments, because financial stability requires both debt repayment and savings protection (aim for three to six months of essential expenses in a separate account).

Track your progress monthly by reviewing your total debt balance against your target payoff date. Celebrate concrete milestones like paying off your first credit card or reaching the halfway point on your largest debt, because these moments reinforce that your strategy works and financial freedom sits within reach. Many people abandon their plans because they fail to see progress clearly, so make your wins visible through a simple spreadsheet or app that shows your declining balance over time.

The habits you build during debt repayment become the foundation for long-term financial health. When you finish paying off your debts, redirect that monthly payment amount into savings and investments rather than increasing your spending. If you need ongoing support beyond what debt advice Canada free offers, we at Financial Canadian provide resources to help you build a strong financial foundation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment