Getting approved for a payday loan in Canada depends on meeting specific eligibility requirements that lenders use to assess your application. At Financial Canadian, we’ve seen countless borrowers confused about what lenders actually look for and how to improve their chances of approval.

The good news is that payday loan eligibility in Canada isn’t mysterious-it comes down to a few key factors like income, employment status, and credit history. Understanding these requirements upfront helps you prepare a stronger application.

What Income Do Payday Lenders Actually Require?

Most payday lenders in Canada set a baseline net monthly income around $1,000, though the exact threshold varies by lender and province. This isn’t arbitrary-lenders use this figure to confirm you can repay the loan without financial hardship.

The Ontario government allows lenders to advance no more than 50% of your net monthly income per loan, which means someone who earns $1,000 monthly can borrow up to $500.

Income Sources Lenders Accept

Government benefits count as valid income, including Ontario Works, disability support, employment insurance, and child tax benefits. Self-employment income qualifies too, though lenders typically require three months of consistent bank statements that show regular deposits to verify stability. Lenders care less about where your income comes from and more about whether it’s stable and verifiable.

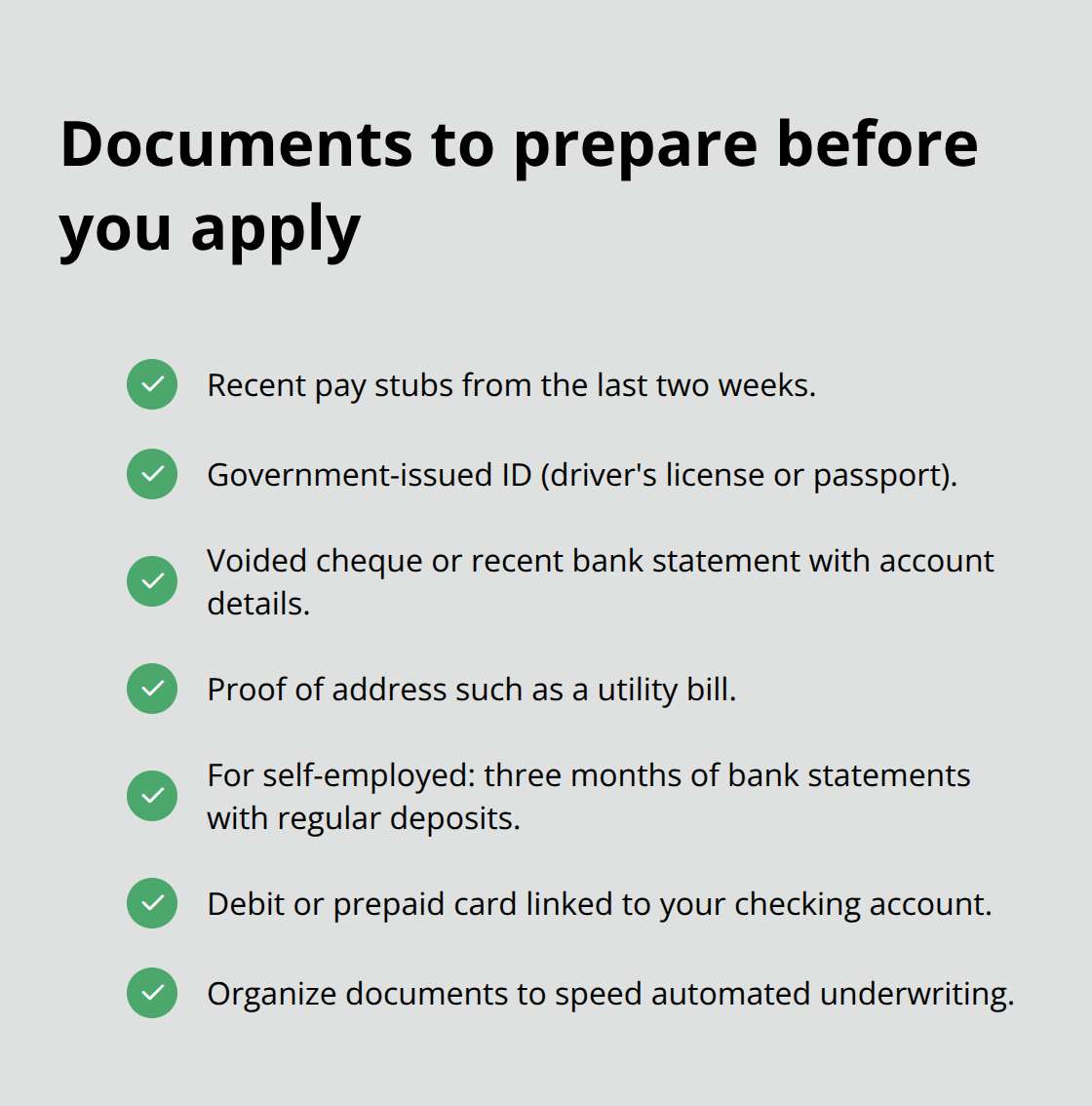

Documents You Need to Prepare

Have these documents ready before you apply: recent pay stubs (usually the last two weeks), a government-issued ID like a driver’s license or passport, a voided cheque or recent bank statement that shows your account details, and proof of address such as a utility bill. If you’re self-employed, prepare three months of bank statements that clearly show regular income deposits.

Lenders verify banking history and may require a debit or prepaid card linked to your checking account for fund transfers. The stronger your document package, the faster automated underwriting runs-many approvals happen within hours when everything is organized.

What Lenders Look for in Your Banking History

Lenders want to see clean banking history with no recent overdrafts or suspicious account activity. If you’ve had overdraft fees or returned payments, address these before you apply because they signal repayment risk to lenders. Lenders cross-check your bank statements against your stated income to spot inconsistencies. If you claim $3,000 monthly income but your account shows irregular $500 deposits, the application gets flagged.

How Lenders Verify Your Information

Some lenders use third-party verification services to confirm employment directly with your employer or validate government benefit payments through provincial databases. This verification typically happens within 24 hours. Provide accurate information throughout your application-misrepresenting income is grounds for immediate rejection and potential legal consequences. Lenders also look at deposit frequency; weekly or biweekly deposits suggest stable employment, while sporadic large deposits raise questions about income reliability.

Your employment status and job history matter just as much as your income level. Lenders assess whether you’ve held your position long enough to demonstrate stability and whether your work situation suggests you’ll earn that income consistently through your loan’s repayment period.

Credit History and Credit Score Considerations

Why Payday Lenders Skip Traditional Credit Checks

Here’s the reality that surprises most borrowers: payday lenders in Canada rarely perform hard credit checks during approval. This is fundamentally different from traditional bank loans. Instead of obsessing over your credit score, lenders focus on income verification and banking history because they want to confirm you can repay within weeks, not years. Some lenders do run soft credit inquiries that don’t impact your score, and a few check credit reports to spot patterns of serial borrowing or recent defaults. The Ontario government’s regulations don’t mandate credit checks, which means approval hinges primarily on income stability and employment status rather than past credit mistakes.

If you have poor credit or no credit history, you won’t face automatic disqualification from payday loan approval in Canada. Your credit score matters far less than your current ability to repay.

What Actually Signals Repayment Risk to Lenders

What damages your payday loan application is a history of unpaid payday debts or recent collection activity. Lenders use credit reports to identify borrowers who defaulted on previous payday loans or have active collection accounts, as these signal genuine repayment risk. If you missed payments on a payday loan within the last 12 months, most lenders will reject your application because they view you as a high-risk repeat offender.

Lenders also watch for patterns of rapid loan cycling-applying for multiple payday loans within 30 days-which suggests financial desperation rather than a temporary cash gap. The Ontario government’s extended payment plan rule requires lenders to offer installment options after three loans within 63 days, and lenders dislike managing these arrangements.

How to Strengthen Your Application Before You Apply

Your best strategy is to maintain clean banking activity between now and your application. Avoid overdrafts, stop frequent loan applications, and resolve any outstanding collection accounts before you apply. If past financial problems exist, address them directly in conversations with lenders rather than hoping they won’t notice.

Employment status and job history matter just as much as your income level, which is why lenders assess whether you’ve held your position long enough to demonstrate stability and whether your work situation suggests you’ll earn that income consistently through your loan’s repayment period.

Employment Stability and Your Payday Loan Approval

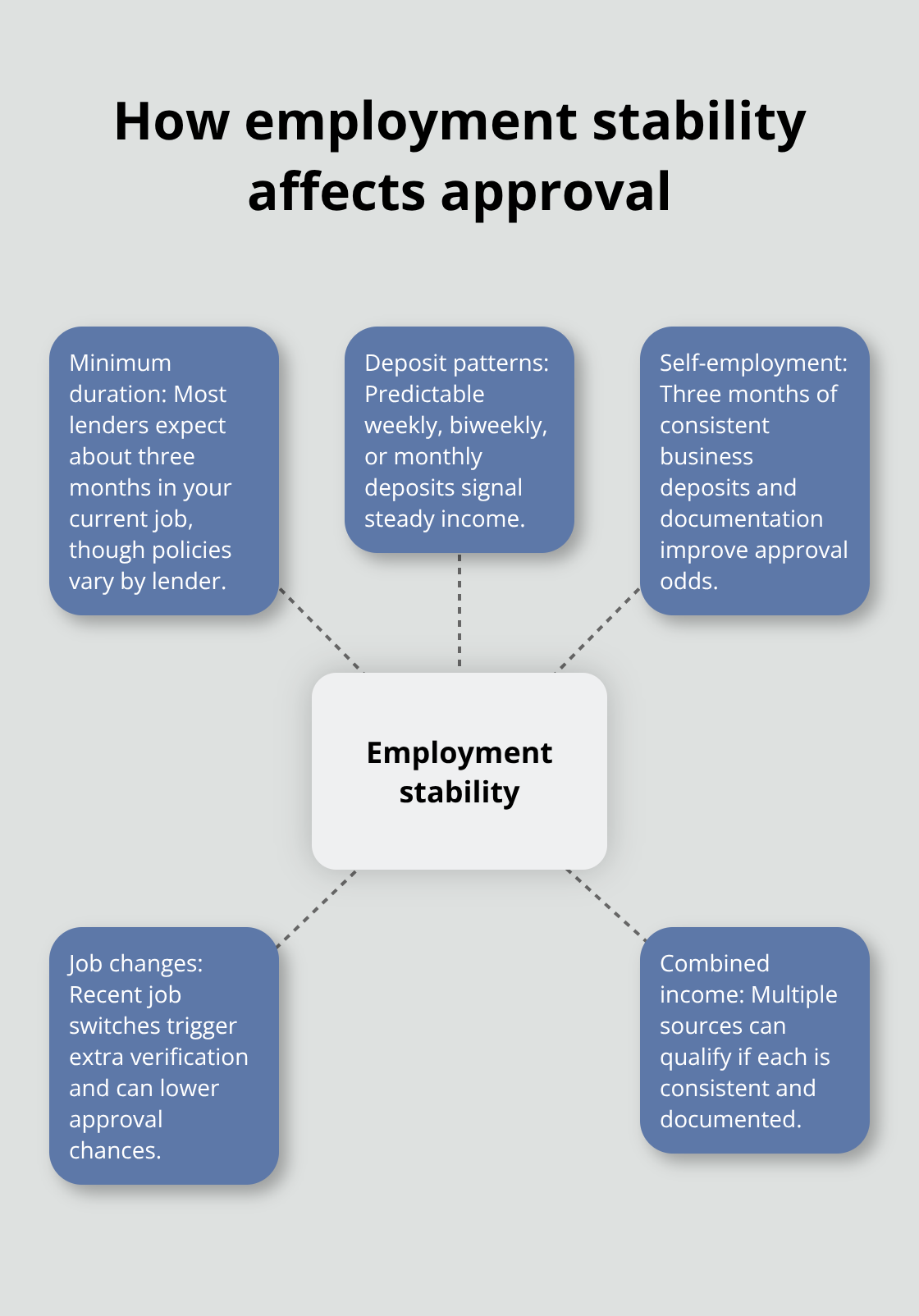

Lenders assess employment status differently than traditional banks do, and this works in your favor. You don’t need a perfect job history or a prestigious position to qualify. What lenders actually want is proof that you’ll earn consistent income through your loan’s repayment period, which typically spans two to four weeks.

Minimum Employment Duration Requirements

Most payday lenders require three months of continuous employment at your current job, though this threshold varies by lender. If you’ve been employed for less than three months, some lenders will still approve you if you can demonstrate prior employment history or show that you’re receiving regular income from government benefits. The Ontario government doesn’t mandate a minimum employment duration, so some lenders may approve applicants with just weeks on the job if their banking history looks clean.

The reality is that lenders care far less about job prestige and far more about income consistency. You could work part-time, full-time, or in contract positions and still qualify, provided your deposits show regular patterns.

Income Consistency and Deposit Patterns

A lender reviewing your bank statements wants to see deposits arrive on predictable schedules. Weekly paycheques, biweekly deposits, or monthly benefit payments all signal stability because they’re predictable.

Sporadic deposits or irregular amounts raise red flags because they suggest your income isn’t reliable enough to guarantee repayment.

Self-employed borrowers face stricter scrutiny but aren’t shut out entirely. Most lenders require three months of consistent bank statements showing regular business deposits before they’ll approve a self-employment application. The key word is consistent-if your deposits fluctuate wildly or show months with no income, expect rejection. Lenders verify self-employment income through business registration checks or tax documentation, so have your most recent Notice of Assessment ready.

Self-Employment and Alternative Income Sources

Contract workers, gig economy participants, and freelancers should track deposits carefully because irregular income patterns work against you. If you receive income from multiple sources (part-time work plus freelance projects plus government benefits), document all of them with separate statements showing deposit frequency. Some lenders accept combined income sources if each one demonstrates consistency.

The harsh truth is that lenders reject applications from self-employed borrowers far more often than salaried employees, not because of bias but because income volatility creates genuine repayment risk. If your self-employment income dropped recently or you’re in a seasonal business with months of zero revenue, apply during your strongest income months.

Job Changes and Employment Transitions

Switching jobs within the past three months triggers additional scrutiny because lenders can’t verify your new income with certainty. If you just started a new position, your previous employer’s pay stubs plus your new offer letter or first paycheque from the new employer can sometimes satisfy lenders, but approval odds drop significantly. Avoid job-hopping before applying for a payday loan because rapid job changes signal instability regardless of your actual reliability.

Final Thoughts

Payday loan eligibility in Canada comes down to three core factors that lenders prioritize above everything else: stable income around $1,000 monthly that you can document with recent pay stubs or bank statements, clean banking history with no recent overdrafts or suspicious activity, and consistent employment whether that’s three months at your current job or regular deposits from self-employment or benefits. The fastest path to approval involves preparing your documents before you apply-gather your last two pay stubs, government-issued ID, a voided cheque showing your account details, and proof of address so lenders can run automated underwriting quickly and often approve you within hours.

If your application gets rejected, ask the lender for the specific reason since common rejections stem from insufficient income, high debt-to-income ratios, unverifiable income sources, negative banking history, or inconsistent information on your application. Address these issues directly before reapplying with a different lender, and contact professional credit counseling services if you need help evaluating your options or understanding payday loan eligibility Canada.

Before you commit to a payday loan, explore cheaper alternatives first because credit unions often offer personal loans with lower rates and longer repayment periods, small-bank installment loans and existing lines of credit may cost significantly less, and borrowing from family or friends with a written agreement beats paying payday loan fees. We at Financial Canadian recommend comparing all your options before applying to confirm that a payday loan truly fits your situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment