Getting a personal loan in Canada means navigating interest rates, fees, and lender options that can significantly impact your finances. We at Financial Canadian have put together Canada personal loan tips to help you understand what’s available and how to secure the best terms for your situation.

The right loan depends on your credit score, income, and how much you need to borrow. This guide walks you through the key decisions you’ll face.

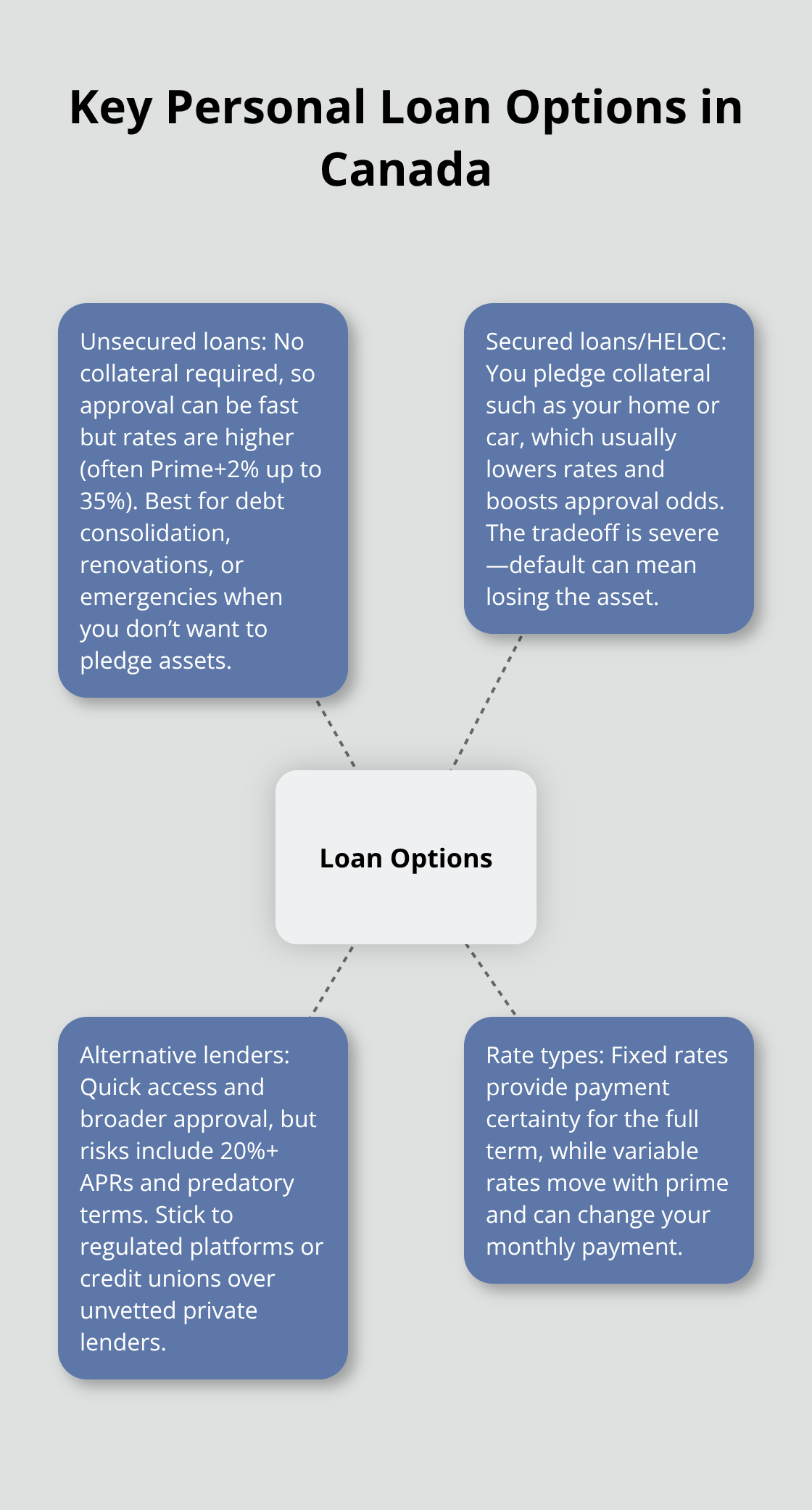

Which Personal Loan Type Matches Your Situation

Unsecured Personal Loans: Speed Over Security

Unsecured personal loans from banks and credit unions don’t require collateral, which makes them accessible but expensive. Interest rates range from Prime+2% to 35% depending on your credit score and income. A borrower with a credit score above 600 and stable employment can expect rates closer to the lower end of that range, though your actual rate depends entirely on your financial profile. CIBC, for example, lists a minimum gross annual income requirement around $17,000, and most lenders evaluate your debt-to-income ratio heavily. The lower your DTI, the better your rate will be.

Unsecured loans work well for debt consolidation, home renovations, or emergencies when you need funds quickly and don’t want to pledge assets. You access money fast without putting property at risk, which appeals to borrowers who lack significant collateral or prefer to keep their assets untouched.

Secured Personal Loans: Lower Rates Through Collateral

Secured personal loans flip this equation-you pledge collateral like your home or car, which dramatically improves your approval chances and cuts your interest costs. A HELOC offers flexibility and access to larger sums if you have the home equity to back it up, with rates typically lower than unsecured loans because the lender’s risk drops when they hold security against your property. The tradeoff is brutal: default and you lose the asset.

Origination fees typically run 0.5%–8% across all loan types, and some lenders deduct these upfront while others add them to your balance, so compare the total dollar cost, not just the rate. This fee structure can swing your decision between two otherwise similar offers.

Alternative Lenders: Speed With Caution

Alternative lenders and online platforms have exploded in Canada over the past five years, targeting borrowers rejected by traditional banks or those seeking speed. These options range from peer-to-peer lending networks to private lenders, but they carry real dangers-some charge 20%+ APRs and bury predatory terms in fine print. You should stick with regulated platforms or credit unions rather than unvetted private lenders.

Rate Types and Terms That Shape Your Payments

When comparing any offer, focus on APR (which includes interest plus fees), not the advertised rate alone. The Bank of Canada held the overnight rate at 2.25% in January 2026, which has kept variable-rate personal loans relatively stable for now, but this can shift. Fixed-rate loans give you payment certainty; variable-rate loans move with the prime rate set by lenders.

Loan terms typically run 1–5 years, with some lenders extending to 7 years-longer terms reduce monthly payments but increase total interest paid significantly. Check prepayment policies before signing: some lenders allow extra payments or lump-sum prepayments without penalties, while others penalize early repayment. Your choice between secured and unsecured hinges on whether you own assets, how urgently you need funds, and whether you can tolerate the risk of losing collateral.

Now that you understand which loan type fits your situation, the next step involves comparing actual offers side-by-side to find the best rate for your financial profile.

How to Compare Personal Loans Before You Apply

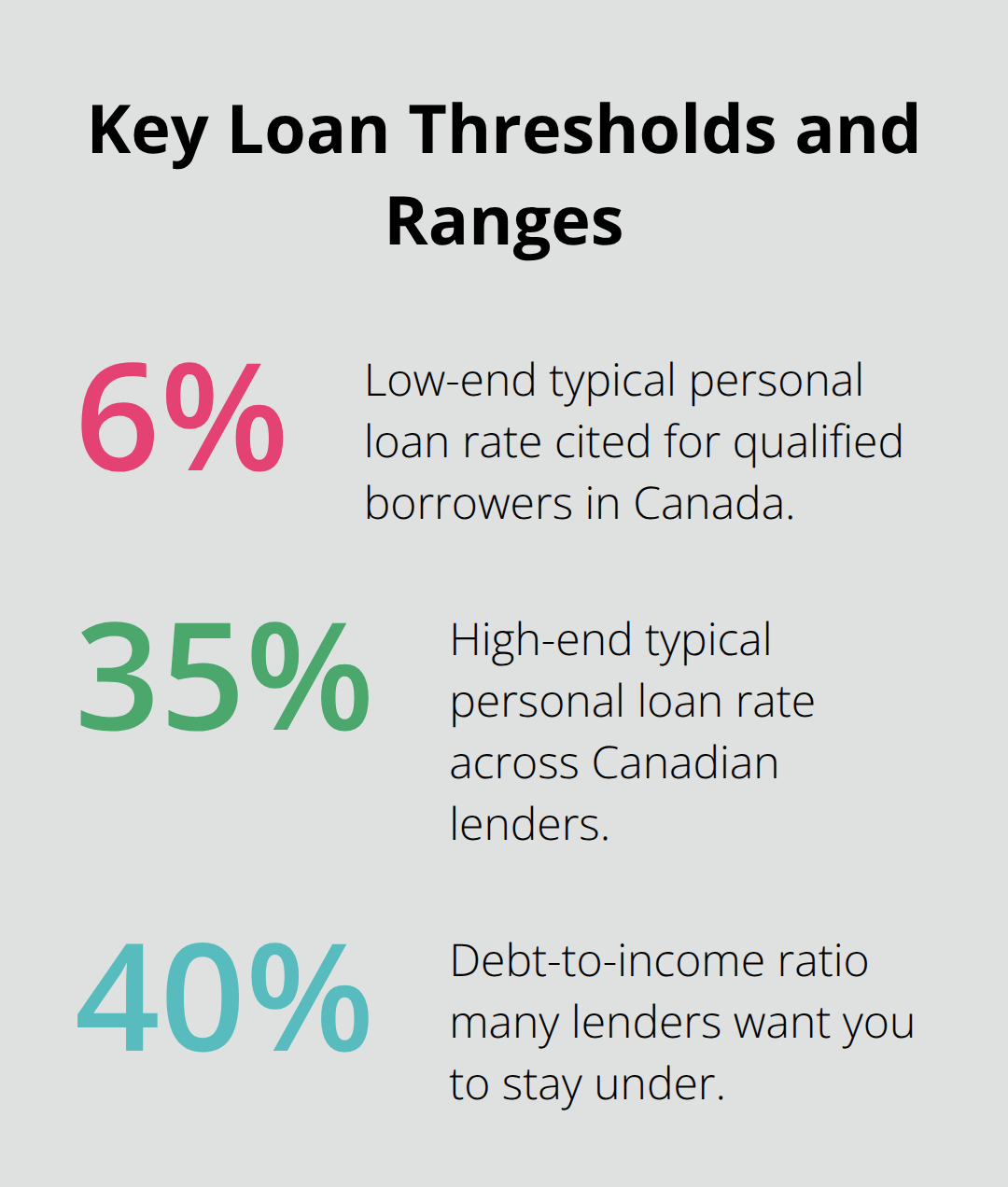

APR is the only number that matters when comparing personal loans, and most borrowers fixate on the advertised interest rate instead. According to Ratehub.ca, typical personal loan rates in Canada range from 6% to 35%, but that headline rate doesn’t reflect origination fees, which typically sit between 0.5% and 8% depending on your lender. Some lenders deduct the fee upfront from your disbursement, which means you receive less cash than you borrowed, while others add it to your loan balance, increasing total interest paid over the life of the loan. A $10,000 loan at 8% APR with a 3% origination fee costs you differently depending on how the fee is structured, so always request the total dollar amount you’ll pay across the full term before signing anything.

Understanding Total Cost, Not Just Rate

Most borrowers make expensive mistakes by comparing advertised rates without accounting for fees, then sign paperwork shocked by their actual monthly payment. Pull APR figures from at least three lenders and calculate your total interest paid across the full term. If one lender charges 8% with a 2% origination fee and another charges 9% with no origination fee, the second option might actually cost less depending on your loan amount and term length. Loan terms commonly run 1 to 5 years, with some extending to 7 years, so a longer term reduces monthly payments but dramatically increases total interest paid. A $15,000 loan at 10% APR costs roughly $1,600 in interest over three years but $2,700 over five years, according to standard amortization calculations.

Prepayment Flexibility Saves Thousands

Check prepayment policies before committing: some lenders allow you to pay extra without penalties, which lets you exit the loan faster and save thousands in interest, while others charge penalties for early repayment. Tools like Ratehub’s LoanFinder show personalized offers in about 60 seconds without impacting your credit, letting you compare personal loan options side by side. This flexibility matters more than most borrowers realize-the ability to make lump-sum payments or accelerate your schedule can cut years off your repayment timeline.

Fixed Rates Versus Variable Rates

Variable-rate loans track the Bank of Canada’s prime rate, which moved to 2.25% in January 2026 and affects what your lender charges you. This matters because if rates rise, your monthly payment rises too, making budgeting harder. Fixed-rate loans lock your payment in place for the entire term, giving you absolute certainty about what you’ll owe each month. Most borrowers should choose fixed rates unless they’re confident rates will drop or they plan to pay off the loan within a year.

Your Debt-to-Income Ratio Controls Your Actual Rate

Your debt-to-income ratio directly influences which rates you’ll actually qualify for, not just which rates are available. Lenders want to see your DTI below 40%, meaning your total monthly debt payments shouldn’t exceed 40% of your gross monthly income. If you earn $4,000 monthly and carry $1,200 in existing debt payments, a new loan payment of more than $400 pushes you outside acceptable range for most lenders.

Lower your DTI before applying by paying down credit cards or waiting to apply when you’ve received a raise. Once you’ve compared offers and understand your actual borrowing costs, the next step involves gathering the documentation lenders require to move your application forward.

How to Qualify for Better Personal Loan Terms

Your Credit Score Opens or Closes Doors

Your credit score is the single most important factor determining whether you’ll qualify and what rate you’ll actually receive. Pull your credit report from Equifax Canada or TransUnion Canada before applying anywhere. Hard inquiries from multiple lenders within 14 days count as one inquiry, so timing matters, but unnecessary checks tank your score. A score of 600 or higher opens doors to favorable rates; below 600 and you’ll face either rejection or predatory pricing from alternative lenders. If your score sits below 600, spend two to three months paying down revolving debt and making on-time payments before applying.

Calculate Your Debt-to-Income Ratio

Your debt-to-income ratio matters equally to your credit score. Most mortgage lenders in Canada look for a debt-to-income ratio under 42% when deciding if you can handle a loan. Calculate this ruthlessly: if you earn $4,000 monthly and already owe $1,200 in car payments, credit cards, and other loans, adding a $500 personal loan payment pushes you to 42.5%, which most traditional lenders reject outright. The fix is brutal but simple: pay down existing debt or wait for a raise before applying.

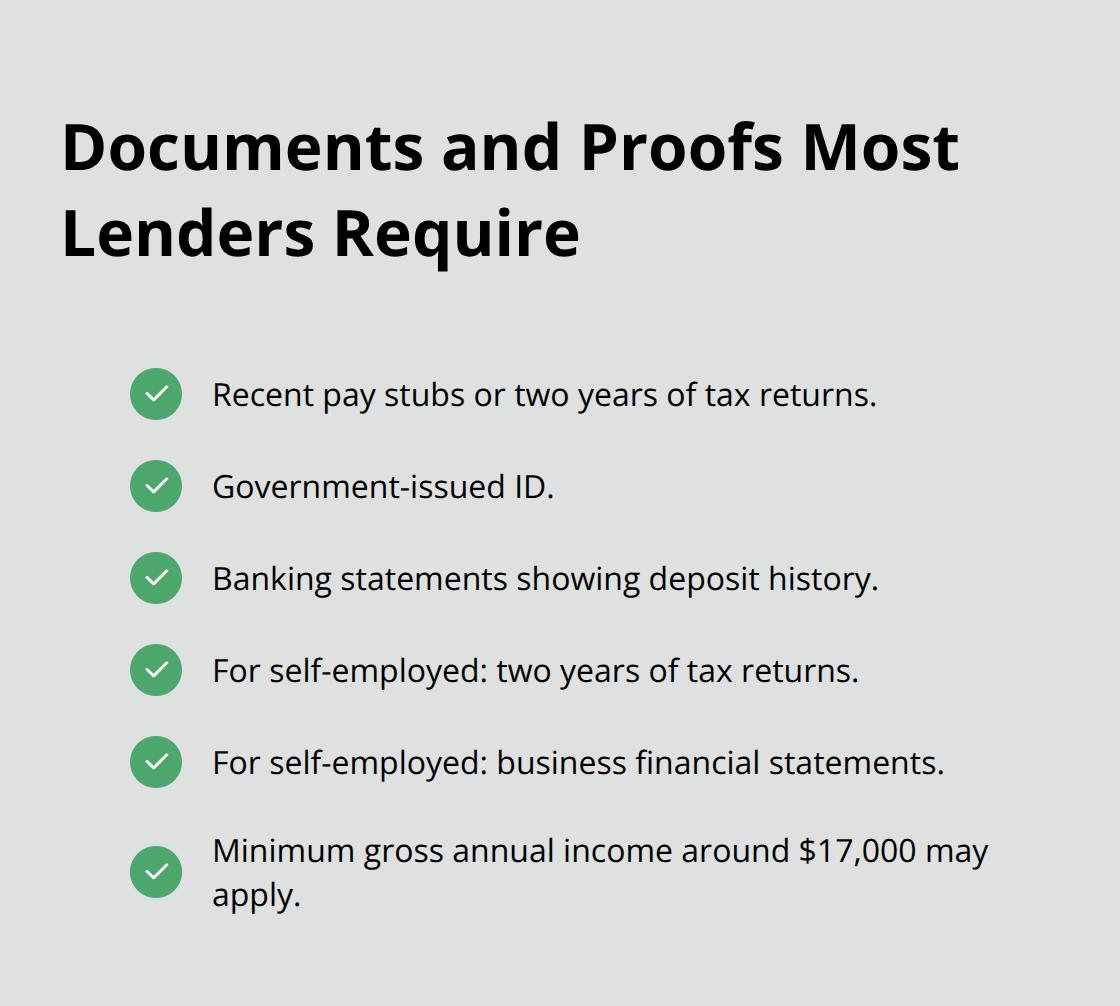

Assemble Your Documentation First

Gather your documentation before contacting any lender. Banks require proof of income (recent pay stubs or tax returns for the past two years), government-issued ID, and banking information showing deposit history. Self-employed borrowers face steeper scrutiny; have two years of tax returns and business financial statements ready. CIBC, for example, lists a minimum gross annual income of around $17,000, which most employed Canadians exceed, but alternative lenders may demand higher thresholds.

Apply to Multiple Lenders Within 14 Days

Contact at least three lenders simultaneously within a 14-day window-this is critical because multiple inquiries in that timeframe register as a single hard pull on your credit. Comparing offers from banks, credit unions, and online platforms reveals the true spread in available rates for your specific financial profile. One lender might offer 9% fixed while another quotes 12%, and the difference on a $15,000 loan over five years amounts to roughly $1,100 in extra interest.

Compare Total Cost, Not Just the Rate

Never accept the first offer; your credit score and income qualify you for multiple options, and lenders price risk differently based on their own criteria. Ask each lender for their APR calculation, total interest paid across the full term, and whether prepayment penalties apply. This comparison takes 30 minutes and saves thousands.

Final Thoughts

Securing the right personal loan requires discipline and comparison, not impulse. The most expensive mistake borrowers make is accepting the first offer without checking APR across multiple lenders-your credit score and debt-to-income ratio determine your actual rate, not the advertised one. Pull your credit report before applying, calculate your DTI ruthlessly, and if either number is weak, spend two to three months improving them before submitting applications.

Contact at least three lenders within 14 days to register as a single hard inquiry, then compare total interest paid across the full term, not just the monthly payment. Avoid fixating on advertised rates instead of APR, ignoring origination fees that range from 0.5% to 8%, and failing to check prepayment policies-a loan that allows penalty-free extra payments can save thousands in interest if you accelerate your schedule. Fixed-rate loans provide payment certainty, while variable rates expose you to increases if the Bank of Canada raises its overnight rate from the current 2.25%.

Start your application by gathering documentation: recent pay stubs or tax returns, government-issued ID, and banking information (self-employed borrowers need two years of tax returns and business financials). Most lenders require a minimum gross annual income around $17,000, which most employed Canadians exceed. Apply these Canada personal loan tips, and explore our resources to guide your decision-making as you move forward with your loan application.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment