Personal loans for Canadians can range from $500 to $50,000, with interest rates varying between 6% and 32% depending on your credit score and lender. The difference between choosing the right lender versus a poor fit can cost you thousands in unnecessary interest and fees.

At Financial Canadian, we’ve reviewed dozens of lenders to help you navigate this decision. This guide walks you through the types of loans available, what to compare, and how to negotiate the best terms for your situation.

What Type of Personal Loan Fits Your Situation

Canada’s personal loan market offers three distinct structures, and picking the wrong one costs money. Unsecured personal loans don’t require collateral, making them accessible for most borrowers, but lenders offset that risk by charging higher rates-typically 15% to 32% APR depending on your credit profile. These loans work best when you need quick cash and own no assets worth pledging. Secured personal loans flip this equation: you pledge collateral like a car or savings account, which lets lenders reduce rates to competitive levels around 6% to 15% APR. The trade-off is real-default and you lose what you put up. Non-mortgage loans totaled $553.1 billion in Q3 2023, up 13.7% from Q1 2020, reflecting Canada’s growing reliance on personal borrowing. If you’re self-employed or have inconsistent income, secured loans often become your only viable path since traditional banks scrutinize income stability heavily. Lines of credit operate differently: instead of receiving a lump sum, you access funds as needed up to a credit limit, paying interest only on what you draw. This structure suits ongoing expenses like renovations or seasonal business costs far better than one-time needs.

When to Choose an Unsecured Loan

Unsecured personal loans make sense when speed matters and you lack collateral. Online lenders and private lenders approve applications in hours or days, not weeks. You’ll pay higher rates for this convenience and flexibility, but the monthly payments stay fixed throughout your term. Major banks like Scotiabank typically offer unsecured personal loans starting around 6% to 10% APR only to well-qualified borrowers with excellent credit and stable employment. Most borrowers face rates between 15% and 25%. Origination fees commonly run 0.5% to 8% of your loan amount, so a $10,000 loan might cost you $50 to $800 upfront. Read the fine print because some lenders deduct fees from your disbursement, meaning you receive less than you borrow.

When Secured Loans Make Financial Sense

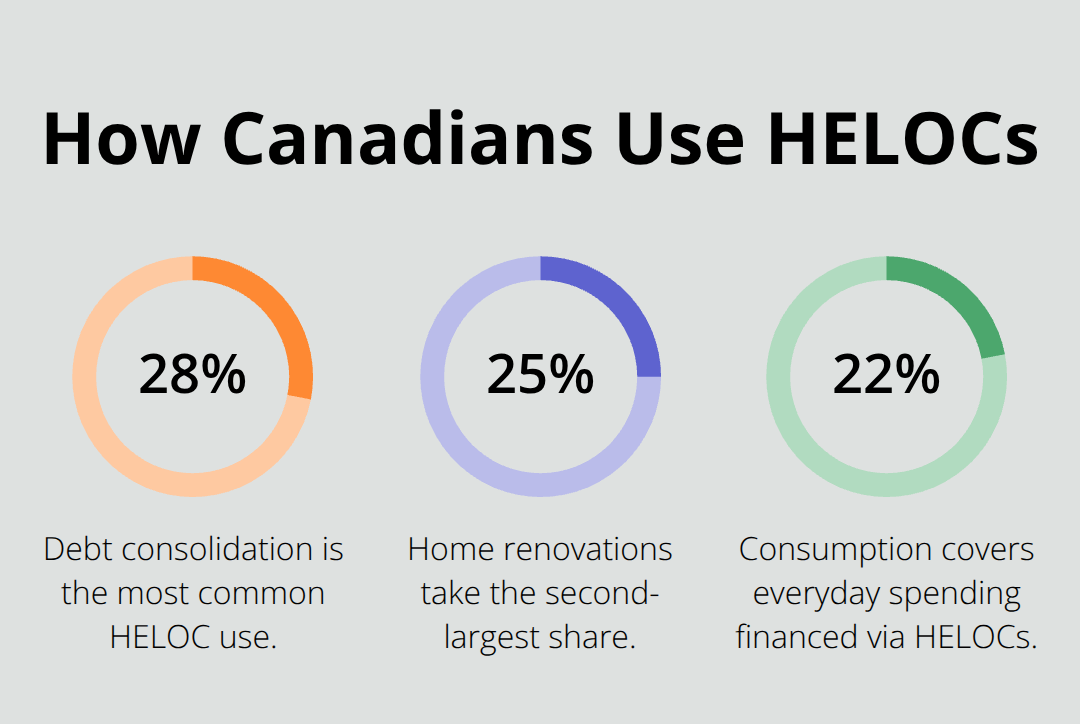

Secured personal loans deliver meaningfully lower rates when you can pledge collateral. A homeowner with home equity can access funds at 6% to 10% APR through a secured loan or HELOC, versus 20%+ for unsecured options. Statistics Canada reports HELOC balances outstanding reached around $176 billion in 2022–2023, with homeowners borrowing up to roughly 65% of their home equity. Most HELOCs fund debt consolidation (28%), home renovations (25%), consumption (22%), and investments (22%).

If you own a vehicle with equity, some lenders accept it as collateral for personal loans. The approval process moves faster because your collateral reduces lender risk substantially. However, never borrow secured unless you’re confident about repayment-losing your home or car over a personal loan defeats the purpose.

Lines of Credit for Flexible Access

A line of credit works like a credit card with better terms: you draw what you need, pay interest on the balance, and reuse available credit. Interest-only payments keep costs low initially, though some lenders require you to pay down principal periodically. These suit homeowners particularly well since secured lines of credit typically charge 5% to 8% APR. Self-employed individuals and business owners prefer lines of credit because variable income doesn’t disqualify them-lenders focus on home equity or business cash flow instead.

The downside: without discipline, a line of credit enables overspending. You’ll need stronger financial habits to avoid accumulating debt across multiple draws.

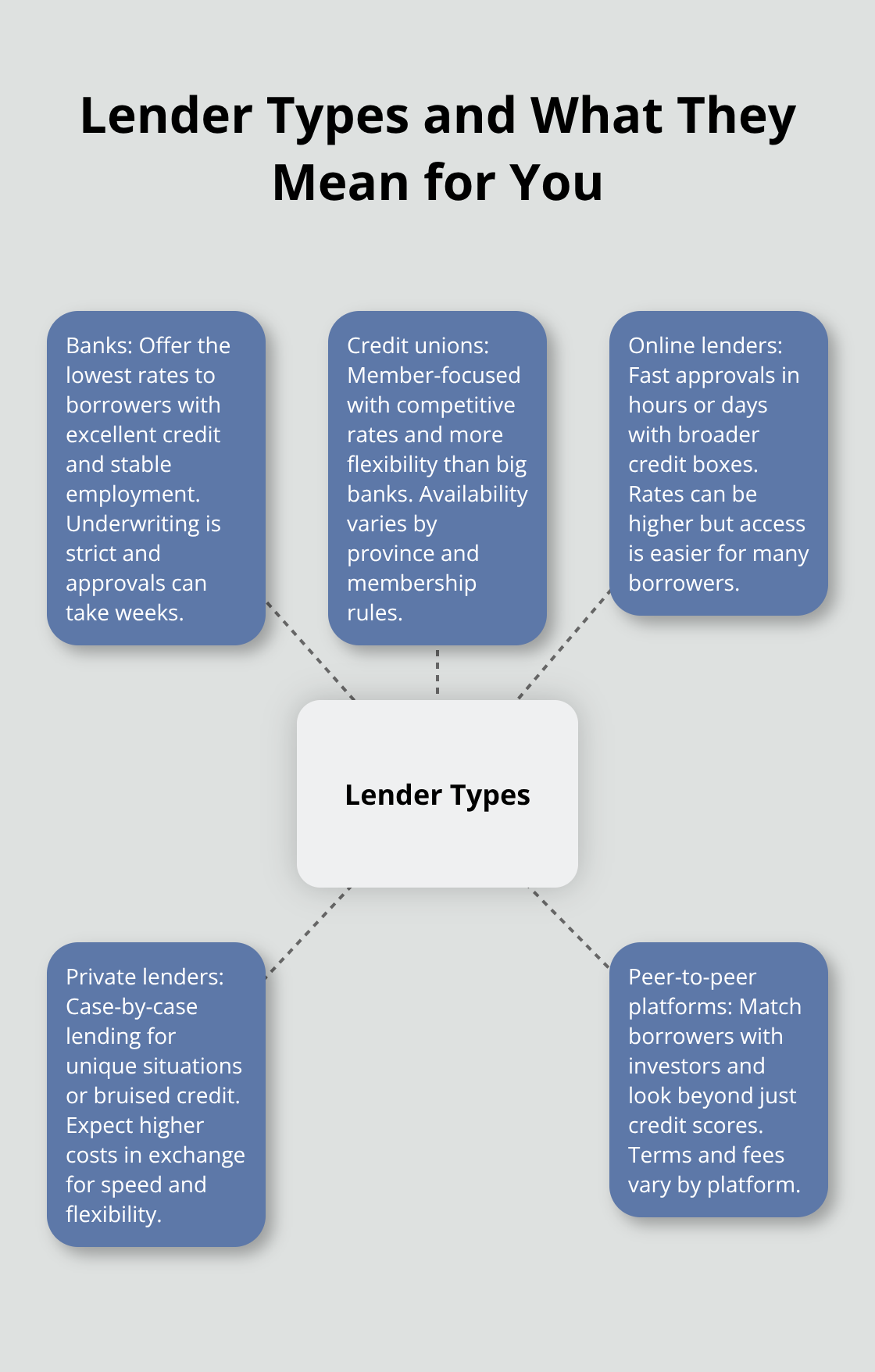

How Lender Type Shapes Your Options

Your choice of lender type-bank, credit union, online platform, or private lender-directly impacts which loan structures you can access and at what cost. Traditional banks restrict secured and unsecured loans to borrowers with strong credit scores and stable employment, making them inaccessible for many Canadians. Alternative lenders (online platforms, peer-to-peer lenders, and private mortgage brokers) have expanded rapidly since 2025, offering more flexible lending rules and faster approvals than banks. These lenders often look beyond credit scores, weighing income, job stability, and your overall financial picture more heavily. Self-employed workers, people with bad credit, and newcomers to Canada benefit most from this flexibility. The trade-off: alternative lenders sometimes charge higher rates than banks, though competitive options exist. Comparing interest rates, terms, and customer reviews across lender types reveals which structure and provider actually fit your situation best.

Key Factors to Compare When Choosing a Lender

Focus on APR, Not the Interest Rate

APR is the only number that matters when comparing personal loans, yet most borrowers fixate on the wrong figure. The advertised interest rate sounds lower than the actual cost because it excludes fees, but APR captures everything-interest plus origination fees plus any other charges baked into the loan. A lender advertising 8% interest with a 3% origination fee on a $10,000 loan doesn’t cost you 8%; it costs closer to 11% APR when you factor in that $300 upfront fee.

Scotiabank charges roughly 6% to 10% APR for well-qualified borrowers, but most Canadians qualify for 15% to 25% APR depending on credit history and income stability. Origination fees typically range from 0.5% to 8% of your loan amount, so you must compare the all-in cost across lenders before you sign anything. A $15,000 loan at 12% APR with no fees costs substantially less over five years than a $15,000 loan at 10% APR with a 5% origination fee ($750 upfront), even though the second option sounds cheaper.

Evaluate Approval Speed and Loan Flexibility

Approval speed and loan flexibility matter far more than most borrowers realize, yet they rarely compare these elements properly. Online lenders fund loans within hours or days while banks take weeks, which becomes critical when you face emergencies or time-sensitive expenses. Loan amounts range wildly across lenders-some offer as little as $100 while others max out at $200,000-so you should verify that your target lender actually provides your needed amount before applying.

Terms typically span six months to five years, but this matters less than whether the lender allows extra payments without penalties. Some lenders charge prepayment fees that offset your interest savings if you pay faster, while others encourage early repayment. You should check whether your lender offers fixed-rate or variable-rate terms; fixed rates keep payments constant while variable rates track the Bank of Canada’s prime rate and move monthly.

Assess Your Debt-to-Income Ratio and Income Type

Debt-to-income ratio heavily influences approval odds and the rate you receive-lenders want your total monthly debt payments below 40% of gross income, though alternative lenders apply this less rigidly. Self-employed borrowers should confirm that the lender accepts tax returns or business financials as income proof, since many traditional banks reject nontraditional income sources entirely. The Bank of Canada held the overnight rate at 2.25% in March 2026, which influences variable-rate loan pricing but doesn’t directly affect fixed-rate loans you’ll likely take.

Before you apply anywhere, you should check your credit reports with Equifax Canada and TransUnion Canada to identify errors that might lower your score unnecessarily. This step takes minutes but prevents you from qualifying for worse rates due to inaccurate information. Once you understand your credit position and debt obligations, you can move forward with confidence toward comparing actual lender offers.

Verify Lender Legitimacy and Compare Offers Strategically

Confirm Your Lender Holds Proper Licensing

Applying to an illegitimate lender wastes time and exposes your personal information to fraud. Start by confirming that your lender holds proper licensing and registration in Canada. Banks and credit unions operate under federal or provincial regulation with public oversight, while private lenders and online platforms vary widely in accountability. Verify lender legitimacy through regulatory databases maintained by the Financial Consumer Agency of Canada. For provincial lenders, check your provincial financial regulator’s website-Ontario has the Financial Services Regulatory Authority, British Columbia has the Financial Institutions Commission, and each province maintains similar oversight bodies.

Online reviews matter, but trust verified sources over anonymous comments; look for patterns across multiple platforms rather than isolated complaints. Search the lender name plus words like “scam” or “complaint” to surface serious issues. A lender with consistent five-star ratings everywhere and zero complaints anywhere signals either fake reviews or a brand new operation with minimal customer history.

Legitimate lenders display transparent contact information, physical addresses, and published fee structures on their websites. If you cannot find these details or the website looks poorly maintained, walk away. Alternative lenders surged partly because traditional banks rejected borrowers with nontraditional income, but this growth also attracted predatory operators. Avoid any lender that pressures you to decide quickly or requests payment upfront before funding your loan.

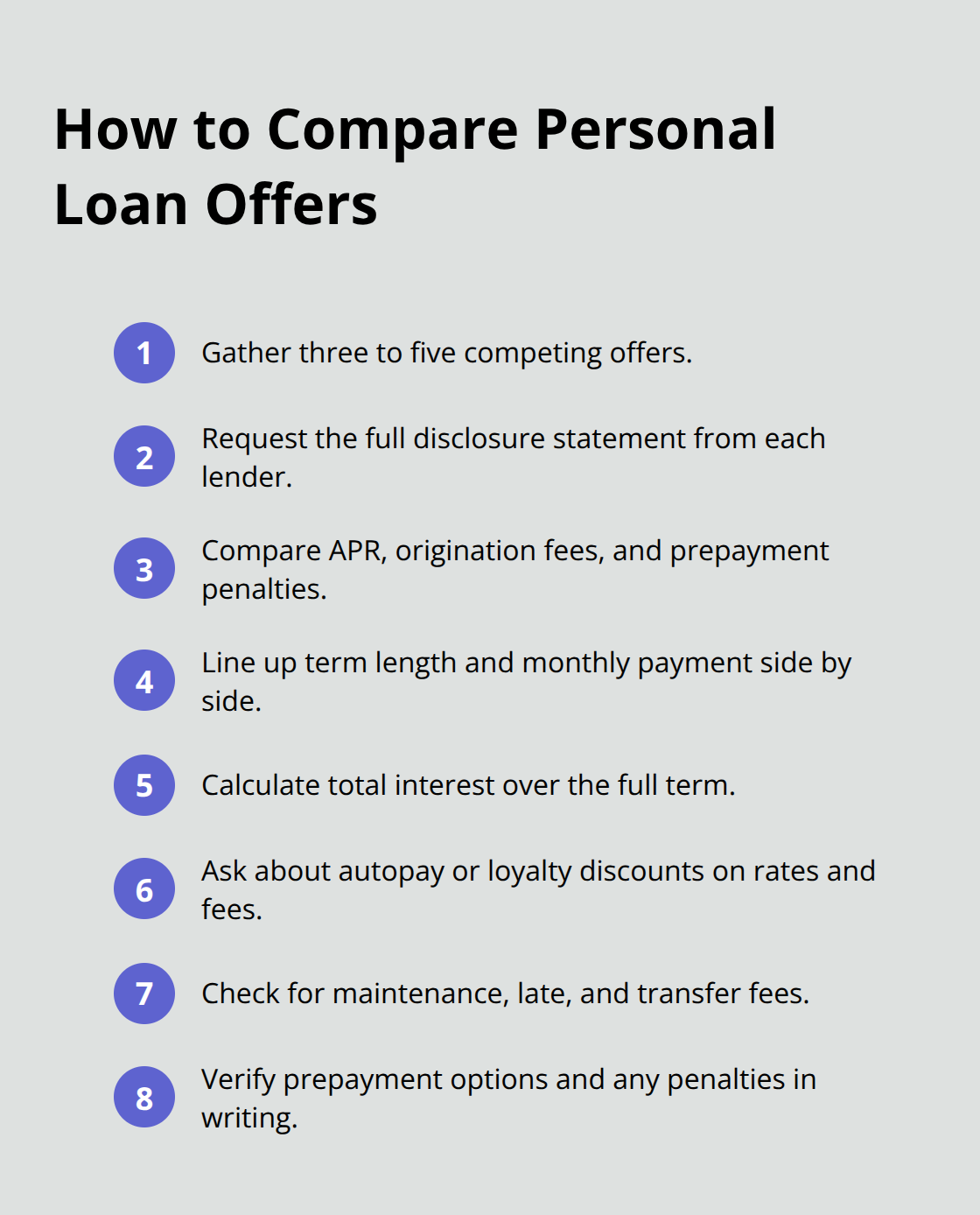

Collect Multiple Offers and Compare Systematically

Collecting three to five competing offers takes a few hours but typically saves hundreds or thousands in interest. When you apply, lenders pull your credit report and provide a detailed disclosure statement showing APR, fees, monthly payment, and total cost over the loan term. Request this disclosure from every lender-it’s legally required in Canada-and arrange them side by side in a spreadsheet comparing APR, origination fees, prepayment penalties, term length, and monthly payment.

A lender offering 12% APR with no origination fee might cost less overall than one charging 10% APR with a 5% upfront fee, depending on your loan amount and term. Calculate the total interest paid across the full term, not just the monthly payment, since a longer term spreads cost differently. Some lenders waive origination fees for borrowers with excellent credit or who set up automatic payments, so ask about these discounts explicitly-they rarely volunteer them.

Check whether the lender charges monthly maintenance fees, late payment fees, or fees for balance transfers. A lender advertising the lowest rate often hides costs elsewhere. Compare multiple loan offers systematically across APR fees and total cost-current personal loan interest rates in Canada typically range from 6% to 35% APR depending on your creditworthiness and the lender. Your debt-to-income ratio influences which lenders will approve you at their advertised rates, so don’t assume every quoted rate applies to your situation.

Negotiate Terms Before You Sign

Most borrowers accept the first offer without negotiating, leaving money on the table. Lenders build flexibility into their pricing because they compete for good borrowers. If you have stable income and solid credit, mention competing offers and ask whether the lender will match or beat the terms. Request written confirmation of any verbal promises about rate reductions, waived fees, or flexible repayment options-verbal agreements disappear when disputes arise.

Some lenders offer rate discounts for setting up automatic payments, linking your chequing account, or maintaining other products with them; ask directly rather than waiting for them to mention it. Before signing, ensure the contract matches every term you discussed-loan amount, APR, fees, payment schedule, prepayment rules, and what happens if you miss a payment.

Read the Fine Print Carefully

Read the entire contract word by word, not just the summary page, because important details hide in subsections. Look specifically for clauses about variable-rate adjustments, whether your rate can change mid-term, and what triggers payment increases. Confirm whether you can pay extra toward principal without penalty, since this option lets you escape the loan faster and save interest.

Request a copy of the fully executed contract immediately after signing and store it safely; you’ll need it if questions arise later. Never let a lender pressure you into signing before you’ve reviewed everything thoroughly or consulted someone you trust.

Final Thoughts

Choosing the right lender for personal loans for Canadians comes down to three concrete actions: comparing APR across multiple offers, verifying lender legitimacy, and reading contracts thoroughly before signing. The difference between a well-chosen lender and a poor fit often amounts to thousands of dollars in unnecessary interest and fees over your loan term. Unsecured loans suit borrowers who prioritize speed and flexibility, secured loans deliver lower rates when you have collateral, and lines of credit work best for ongoing expenses.

APR matters far more than advertised interest rates, and alternative lenders offer genuine advantages for self-employed workers and those with nontraditional income. Prepayment penalties can eliminate your savings if you pay faster, so you must confirm your lender’s policies before signing. Gather three to five competing offers from different lender types, arrange them in a spreadsheet comparing APR and fees, then negotiate with your top choice before committing.

Check your credit reports with Equifax Canada and TransUnion Canada first so you understand your starting position, and verify that any lender you consider holds proper licensing through the Financial Consumer Agency of Canada or your provincial regulator. Request written disclosure statements from every lender and calculate the total interest you’ll pay across the full term. Once you’ve selected your lender, read the entire contract word by word, confirm prepayment options, and explore our resources to support your borrowing decisions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment