When your savings fall short and unexpected expenses hit, guaranteed loans in Canada offer a practical way to access funds quickly. We at Financial Canadian know that traditional lenders often turn away applicants with less-than-perfect credit, leaving many Canadians stuck.

Guaranteed loans work differently. They’re backed by government programs or co-signers, which means approval doesn’t depend solely on your credit score.

In this guide, we’ll walk you through how these loans work, their real costs and benefits, and exactly how to apply.

Understanding Guaranteed Loans in Canada

Guaranteed loans in Canada aren’t actually guaranteed in the way the name suggests. No lender can truly guarantee approval regardless of your financial situation. What these loans actually offer is a higher likelihood of approval because a third party-typically a government program or co-signer-backs part of the risk. The Trade Expansion Lending Program (TELP), for example, helps you access more working capital from your financial institution through Export Development Canada, allowing your business to pursue international growth. For personal borrowing, the mechanism differs. Lenders offering what they market as guaranteed loans approve based on factors beyond your credit score, such as income stability, employment history, and the loan amount requested. This approach opens doors for Canadians with fair or poor credit who would otherwise face rejection from traditional banks. The reality is that approval still depends on your ability to repay, but lenders assess this more flexibly than major financial institutions do.

What Guaranteed Loans Actually Cover

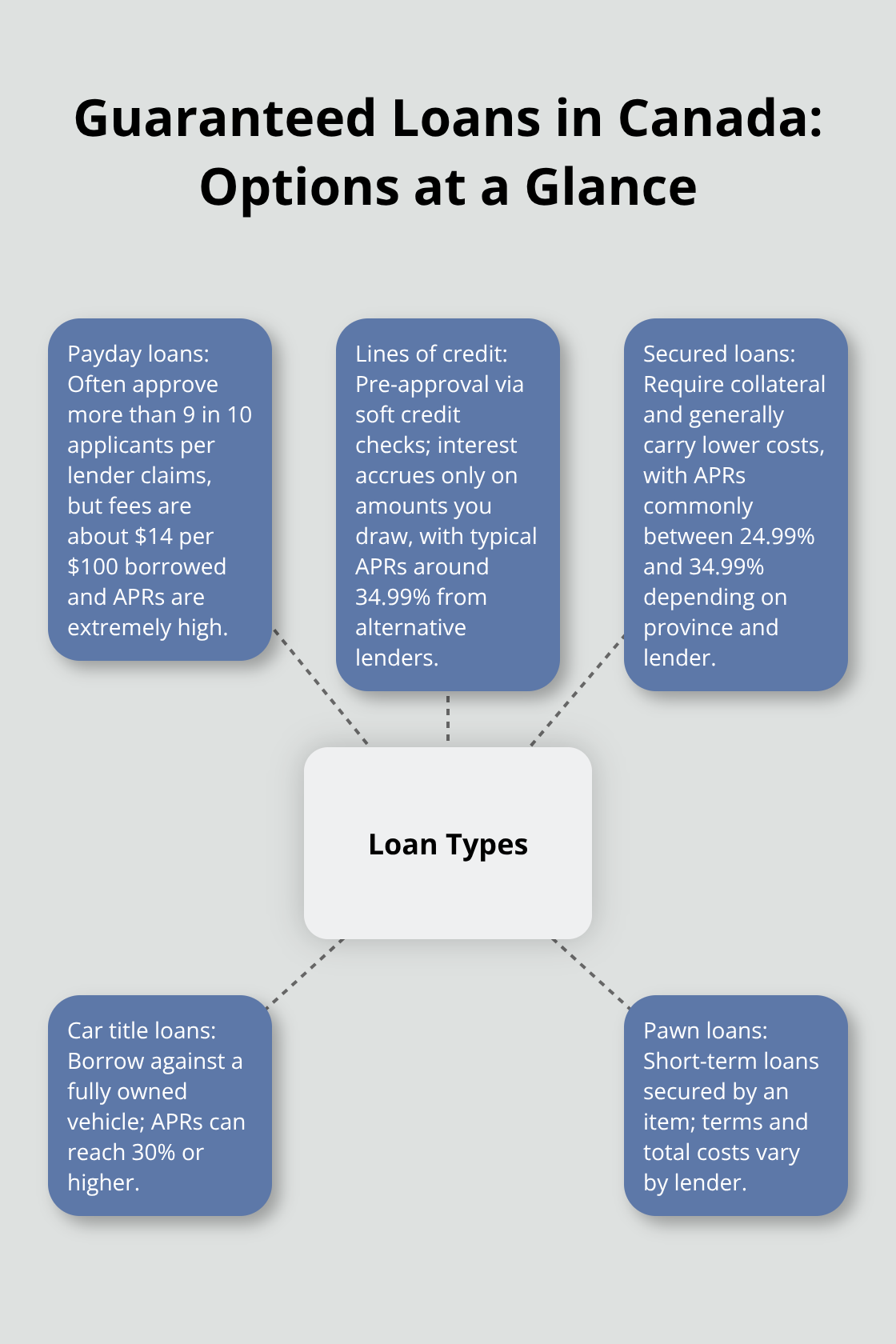

In Canada, you’ll encounter several loan types marketed with language suggesting easier approval. Payday loans approve more than 9 in 10 applicants according to lender claims. These are unsecured, meaning no collateral is required, and funds come directly from the lender rather than through an employer. Lines of credit and secured loans offer another route, with pre-approval available through a soft credit check that doesn’t impact your credit score.

Car title loans let you borrow against a fully owned vehicle, typically carrying APRs up to 30%. Pawn loans are short-term secured options where an item serves as collateral. Each carries different costs and terms, so comparing specific APRs matters more than relying on marketing language about guaranteed approval.

Who Actually Qualifies

Lenders offering these products focus on income stability and loan history rather than credit score alone. You’ll typically need to be 18 or older, have valid identification, steady income, an open chequing account, and a home address. Low or no credit may still lead to approval, though the loan amount might be smaller than the maximum offered. Provincial regulations significantly impact eligibility and costs. Provincial regulations payday loans Canada impose a federal limit of $14 per $100 borrowed across provinces. Before you apply anywhere, confirm your province’s specific regulations and read the loan agreement carefully. Transparency about fees, repayment schedules, and consequences of late payments separates legitimate lenders from predatory ones.

What Separates Real Lenders from Predatory Ones

The difference between a trustworthy lender and a predatory one comes down to how they handle disclosure. Legitimate lenders clearly state all fees, APRs, and repayment terms upfront. They don’t hide charges or surprise you with unexpected costs after approval. Predatory lenders, by contrast, obscure their terms or impose enormous fees that make repayment nearly impossible. They may double-charge or mishandle payments, leaving borrowers trapped in cycles of debt. When you compare offers, look for lenders who explain exactly what you’ll owe and when. Ask about late payment consequences and whether the lender reports to credit bureaus like Equifax Canada. Responsible use of these loans can actually help you build credit history, but only if the lender operates transparently. Now that you understand what these loans are and who qualifies, the next step is learning how to actually apply and what to expect from lenders during the approval process.

The Real Cost of Quick Access to Funds

Guaranteed loans in Canada force you to accept a fundamental trade-off that lenders rarely emphasize upfront. Speed and accessibility come at a price, often a steep one. Payday loans charge approximately $14 per $100 borrowed, translating to an APR around 365% in most provinces and 425.83% in Manitoba. A $500 loan for 14 days in Ontario costs $70 in fees alone, meaning you repay $570 total. Lines of credit from alternative lenders typically charge 34.99% APR, while secured loans range from 24.99% to 34.99% APR depending on your province and lender. Car title loans can reach 30% APR or higher. These rates far exceed traditional bank personal loans, which carry much lower percentages. The speed of funding matters when you face genuine emergencies, but the cost compounds quickly if you cannot repay within the initial term. A $2,000 payday loan becomes $2,280 after two weeks, and rolling it over creates a debt spiral that traps many borrowers.

When Speed Actually Justifies the Cost

Legitimate reasons exist for accepting high-cost loans, but they remain narrower than lenders suggest. If you face an immediate financial emergency and possess a concrete repayment plan within weeks, not months, the temporary cost may prove worthwhile. Government programs like the Trade Expansion Lending Program help you access more working capital from your financial institution through a guarantee. Pre-approval processes through lenders offering lines of credit or secured loans take hours or days, not weeks, and funding arrives within 15 minutes via Interac e-Transfer according to lender timelines. This speed matters if you face a deadline, but only if you’ve confirmed you can repay before interest compounds. The approval advantage for applicants with fair or poor credit is real-more than 9 in 10 applicants reportedly receive instant approval for payday loans-but this accessibility masks the structural problem. Lenders approve more people precisely because the fees generate income regardless of whether borrowers can afford repayment. Your ability to access funds does not mean the funds won’t cost you significantly more than alternatives.

The Hidden Danger of Multiple Borrowing

Most Canadians with imperfect credit do not take one loan and repay it cleanly. They roll over payday loans, take multiple advances, or apply to several lenders simultaneously. Each additional loan adds fees and creates overlapping repayment obligations that your income cannot support. Provincial regulations cap individual loans but do not prevent someone from owing money to five different lenders at once. If you borrow $1,500 across three payday loans, your total fees approach $210 within two weeks. Missing payments triggers late fees and credit damage that makes future borrowing even more expensive. This pattern explains why guaranteed loans, despite their marketing language, often worsen financial situations rather than improve them.

How to Avoid the Debt Trap

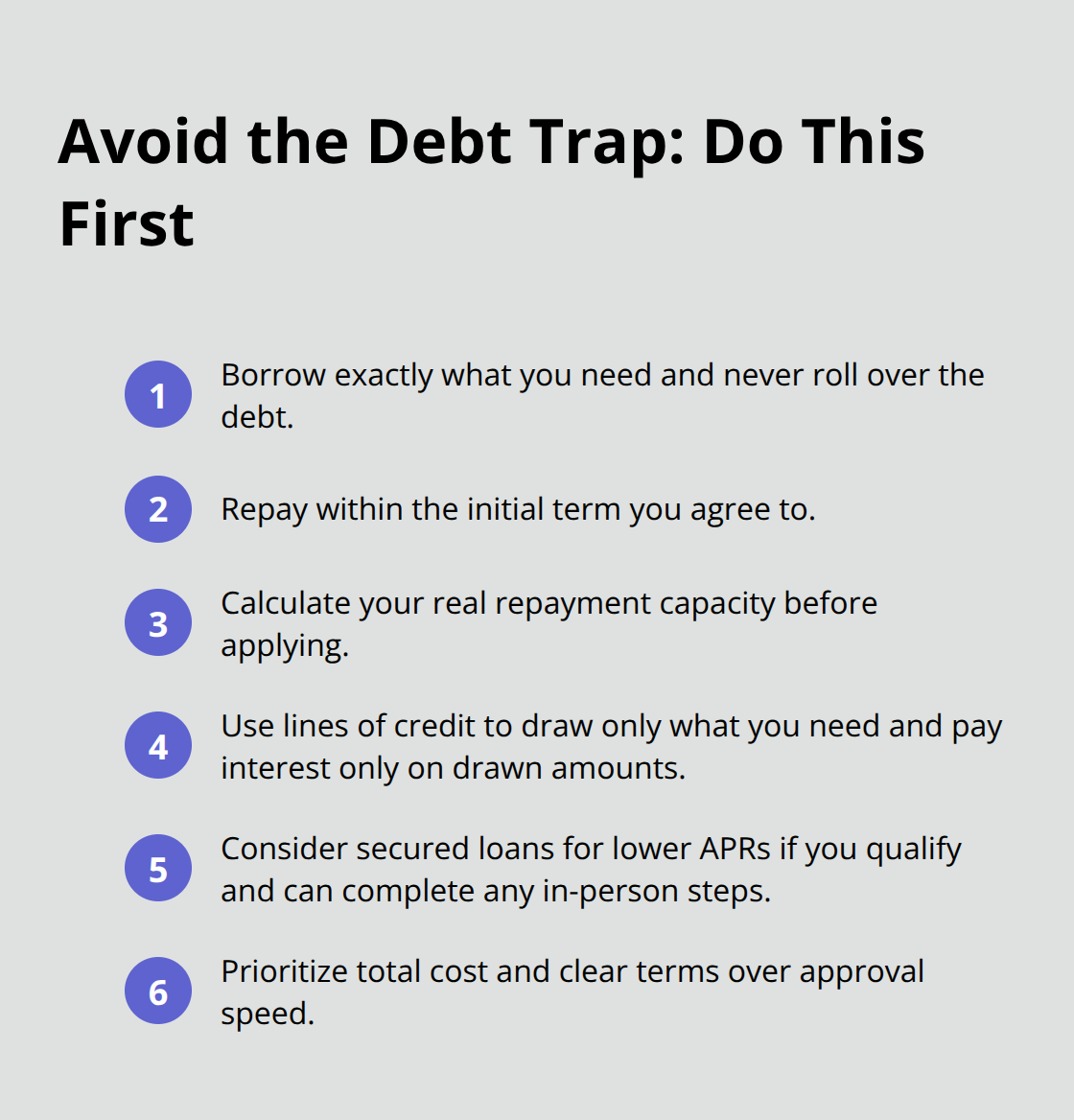

The real advantage comes only if you use these products strategically-you borrow exactly what you need, repay within the initial term, and never roll over the debt. That requires discipline that the lender’s business model actively works against. Before you apply, calculate your exact repayment capacity and confirm you can meet the deadline without additional borrowing. Lenders offering lines of credit allow you to draw only what you need and pay interest solely on drawn amounts, which reduces costs compared to payday loans where you pay fees on the full amount upfront.

Secured loans require collateral (typically a vehicle) but offer lower APRs, sometimes as low as 24.99%, making them cheaper if you qualify and can afford the branch visit that many lenders require. Understanding these distinctions between loan types matters far more than chasing approval speed alone. Now that you know what these loans actually cost and when they make sense, the next step involves learning how to apply strategically and what lenders assess during their approval process.

How to Actually Apply for a Guaranteed Loan

Prepare Your Documents and Calculate Your Needs

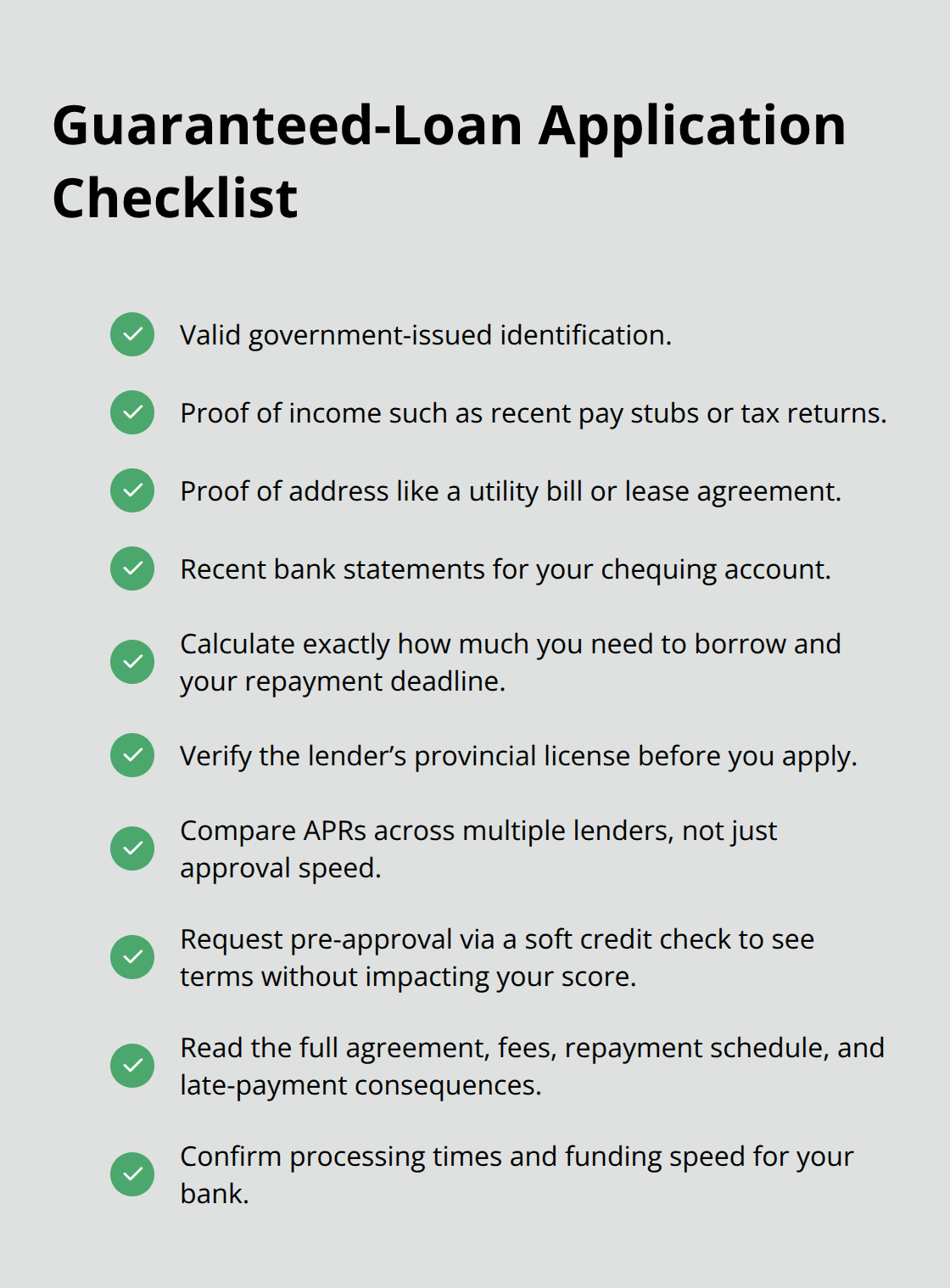

Preparing your application correctly separates borrowers who receive approval quickly from those who face rejection or worse terms. Start by gathering the specific documents lenders require: valid identification, proof of income (recent pay stubs or tax returns), proof of address (utility bill or lease agreement), and bank statements showing your chequing account.

Lenders assess income stability more heavily than credit score, so if you’re self-employed or have variable income, prepare documentation showing consistent earnings over the past 6 to 12 months.

Next, calculate exactly how much you need to borrow. Overborrowing costs you significantly more in fees-a $1,500 loan costs $210 in fees over two weeks, while a $2,000 loan costs $280. Know your repayment deadline before you apply. If you cannot realistically repay within the initial term, do not proceed with a payday loan.

Verify Lender Licensing and Provincial Rules

Check your province’s specific regulations and lender licensing before you apply anywhere. Payday lenders in British Columbia operate under License #52546, Ontario under License #4721539, Alberta under License #342618, Nova Scotia under License #241843061, Saskatchewan under License #511325, and Manitoba under License #67816. Verify that your chosen lender holds the appropriate license for your province. This single step eliminates most predatory operators who work without proper authorization.

Compare APRs Across Multiple Lenders

Finding the right lender requires comparing actual APRs across multiple providers rather than chasing approval speed alone. Lines of credit and secured loans offer competitive rates depending on your collateral and province. Payday loans universally charge around 365% APR except in Manitoba where the rate reaches 425.83%. Comparing rates across lenders helps you identify the most cost-effective option for your situation.

Request Pre-Approval and Review Terms Carefully

Apply for pre-approval first through soft credit checks that do not impact your credit score. Most lenders provide pre-approval decisions instantly during business hours or within 48 hours after you submit required documents. This step shows you exactly what terms each lender will offer before you commit.

When you receive approval offers, read the loan agreement completely. Legitimate lenders clearly state all fees, repayment schedules, late payment consequences, and whether they report to credit bureaus like Equifax Canada. If a lender rushes you or refuses to explain fees clearly, walk away. Approval timelines vary significantly by lender and province, so confirm expected processing times before submitting your application.

Receive Funds and Complete Your Borrowing

Once you’ve chosen a lender and submitted your final application, funding arrives remarkably fast-some lenders disburse funds within 15 minutes via Interac e-Transfer, though most take several hours or one business day depending on your bank’s processing speed.

Final Thoughts

Guaranteed loans Canada serve a specific purpose: they provide access to funds when traditional lenders reject you. That access comes with real costs that demand careful consideration before you apply. The approval advantage is genuine, but it exists because lenders profit from high fees regardless of whether you can comfortably repay.

The core decision boils down to timing and repayment capacity. If you face a genuine emergency, possess a concrete plan to repay within weeks, and have calculated the exact fees you’ll pay, guaranteed loans make sense. A $1,500 payday loan costs $210 in fees over two weeks, which is expensive but manageable if you’ll receive income to cover it. Lines of credit at 34.99% APR or secured loans at 24.99% to 34.99% APR offer lower costs if you have time to apply and can provide collateral.

Before you apply anywhere, verify your lender’s provincial license, read the loan agreement completely, and compare APRs across multiple providers. Legitimate lenders disclose all fees upfront and explain late payment consequences, while predatory lenders obscure terms and trap borrowers in cycles of debt. Your next step is simple: gather your documents, verify lender licensing for your province, and request pre-approval from multiple lenders to compare actual terms before committing to anything.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment