Canada personal loan rates are climbing, and most borrowers have no idea what they’ll actually pay. At Financial Canadian, we’ve seen too many people accept the first rate offered without understanding what they qualify for or how to negotiate better terms.

This guide cuts through the confusion. We’ll show you the current rate landscape, how your credit score determines your price, and the concrete strategies that actually work to lower what you pay.

Canada Personal Loan Rates: What You Can Expect This Year

Current Rate Environment and Bank of Canada Policy

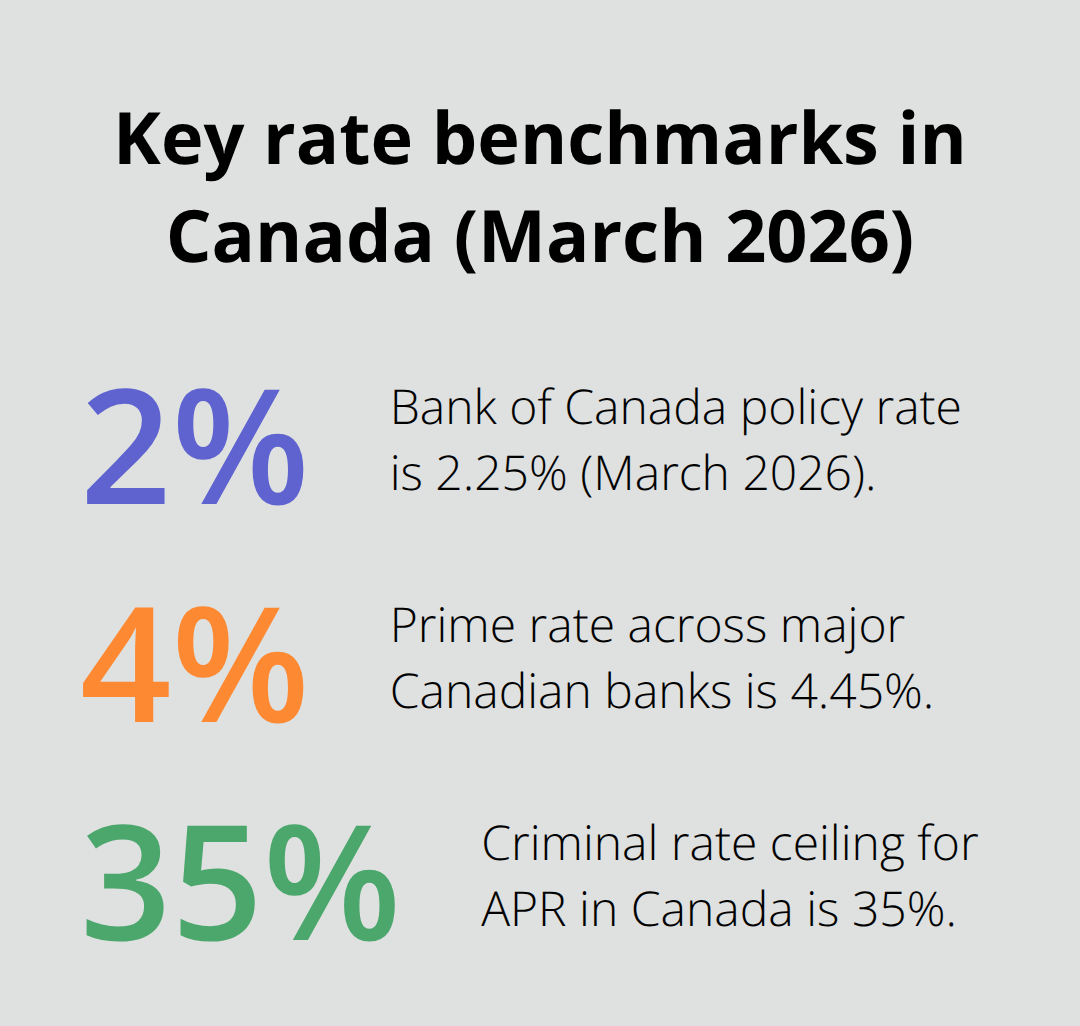

The Bank of Canada policy rate sits at 2.25% in March 2026, and this decision ripples directly into what you’ll pay for a personal loan. The prime rate across Canada’s major banks sits at 4.45%, which serves as the foundation for most personal loan pricing. When the Bank of Canada moves, lenders adjust their rates within days. Right now, the rate environment is stable, but that stability won’t last forever.

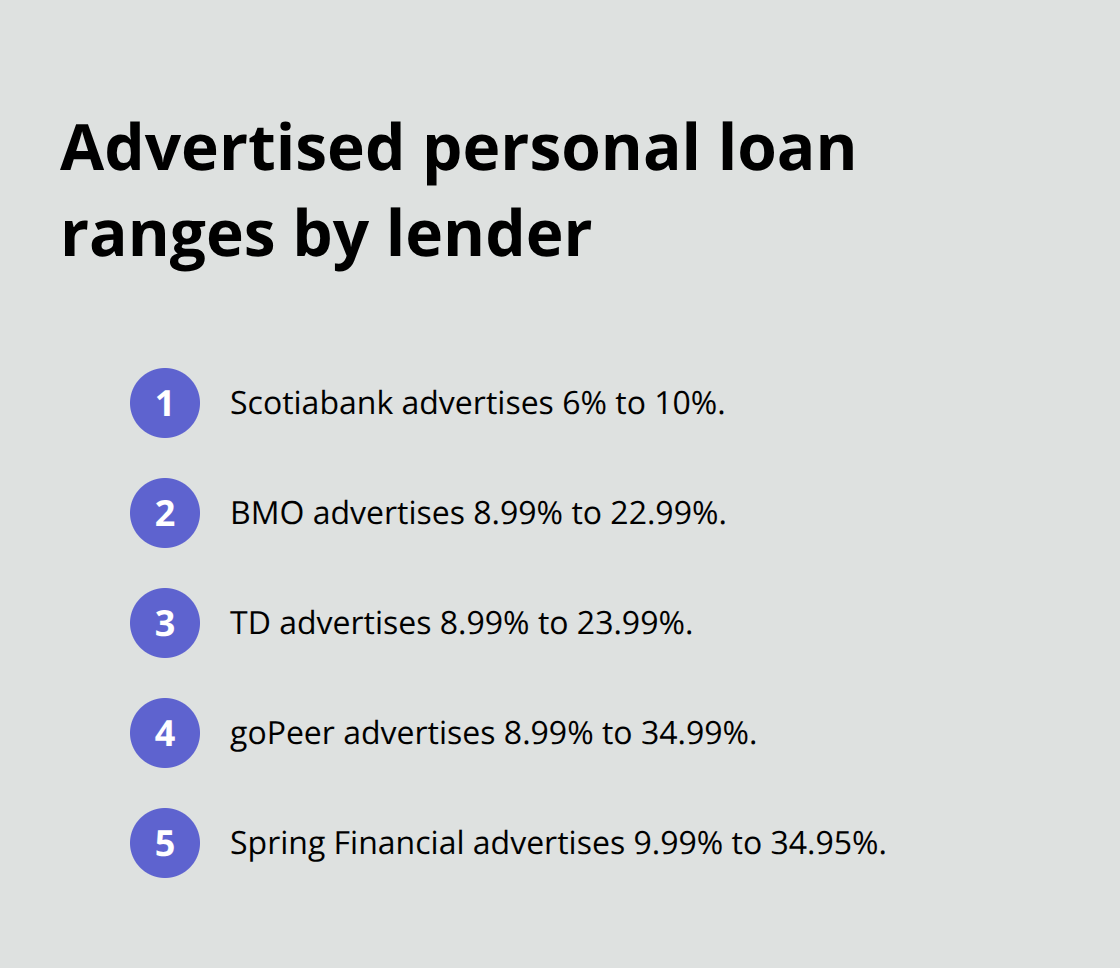

Major banks advertise rates in wildly different ranges. Scotiabank quotes 6% to 10%, while BMO goes from 8.99% to 22.99%, and TD spans 8.99% to 23.99%. The gap exists because your credit score, income, and debt levels determine where you land within each lender’s range. Online lenders cast a wider net, with goPeer offering 8.99% to 34.99% and Spring Financial at 9.99% to 34.95%.

How Lenders Price Your Loan

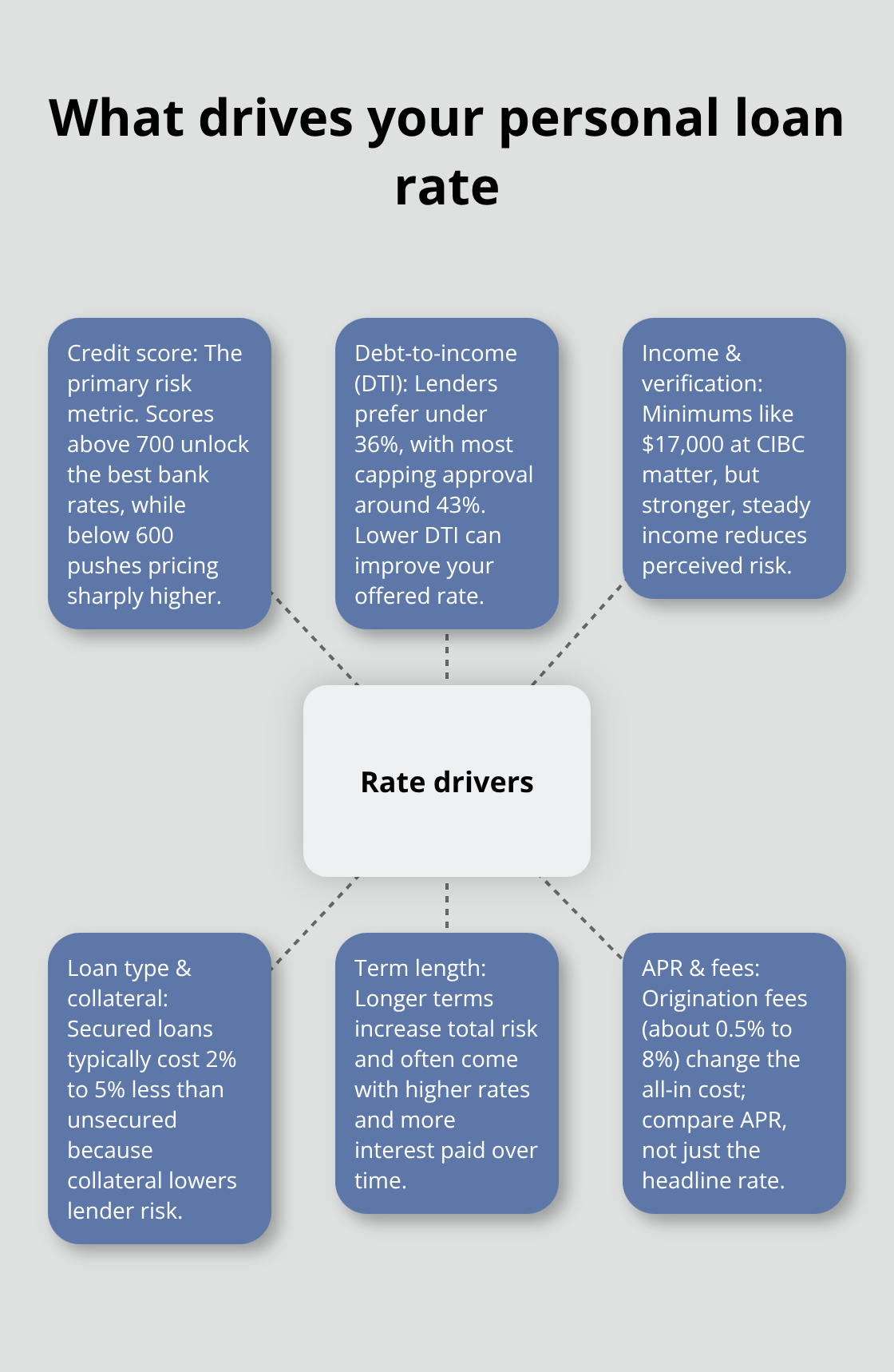

Lenders price loans based on risk, and they measure your risk through credit score, debt-to-income ratio, and income verification. A credit score of 600 or higher opens doors to reasonable rates, but scores above 700 unlock the best terms. Most mortgage lenders in Canada look for a debt-to-income ratio under 42% when deciding if you can handle a loan.

CIBC requires a minimum gross annual income of $17,000, while loan maximums vary significantly-Scotiabank caps at around $75,000, TD at roughly $50,000, and CIBC extends to $200,000. The type of loan also shifts pricing. Secured loans backed by collateral like a vehicle cost less because lenders recover their money if you default. Unsecured personal loans carry higher rates because lenders have no asset to claim.

When you compare offers, focus on APR rather than the advertised rate, since APR includes origination fees that typically run 0.5% to 8% of your loan amount. A $10,000 loan with a 2% origination fee means you receive $9,800 upfront, not the full amount.

Loan Structure and Rate Type Decisions

The duration of your loan matters significantly; longer terms mean more risk and higher rates. Fixed-rate loans lock your payment regardless of what the Bank of Canada does next, while variable-rate loans fluctuate with the prime rate. If you anticipate rate increases, fixed rates insulate you from future hikes. The Bank of Canada warned in early 2026 that economic uncertainty could push rates in either direction, so locking a fixed rate now protects you against potential increases later in the year.

Economic Conditions Shaping 2026 Rates

Canada’s economy contracted 0.6% in the fourth quarter of 2025, signaling weaker momentum heading into 2026. The Bank of Canada projects GDP growth above 1% this year and around 1.5% next year, hardly robust growth. This slowdown affects personal loan demand and how aggressively lenders compete for business. Energy price volatility from Middle East conflicts adds another layer of unpredictability that lenders factor into their pricing.

The criminal rate ceiling in Canada sits at 35% APR, so no lender can charge beyond that threshold regardless of your credit profile. Most borrowers won’t approach that ceiling, but it establishes the outer boundary. The data from early 2026 shows inflation at 1.8% in February, which suggests the Bank of Canada may hold steady, but geopolitical tensions and tariff threats create uncertainty that lenders price into their margins.

Taking Action in Today’s Rate Environment

Shopping across all six major banks plus at least two online lenders takes two hours but saves hundreds of dollars over your loan term. The rate environment in 2026 favors borrowers willing to do the legwork because competition remains fierce and lenders still need customers. Lock a fixed-rate loan if you expect rates to rise later in 2026, and apply when you have the strongest possible credit score and lowest debt levels. Understanding how your credit score determines your rate helps you take concrete actions to improve it before you apply.

How Your Credit Score Determines What You Pay

The Credit Score Gap That Costs Thousands

Your credit score separates borrowers paying 6% from those paying 24% on identical loan amounts. Lenders use your score as a shorthand for risk, and the math is brutal: a 100-point difference in your score costs you thousands of dollars over a five-year loan term. Scores above 700 unlock rates in the 6% to 12% range from major banks, while scores between 600 and 650 push you into the 15% to 22% territory. Below 600, online lenders charge 20% to 35%, assuming you qualify at all.

The Bank of Canada’s prime rate of 4.45% sets the floor, but your credit score determines how much lenders add on top. A score of 750 or higher means lenders add 1.5% to 3% to the prime rate. A score between 650 and 700 means they add 6% to 10%. A score below 600 means add-ons jump to 15% or higher. Lenders price risk mathematically, and your score is their primary risk metric.

Debt-to-Income Ratio: The Second Gatekeeper

Your debt-to-income ratio appears on your credit report and lenders scrutinize it closely. Lenders prefer debt-to-income ratio limits lower than 36%, and the highest DTI ratio that most lenders will consider is 43%. This threshold matters more than many borrowers realize because it determines not just approval odds but also the rate you receive within a lender’s range.

Concrete Steps to Improve Your Score Before Applying

Pay down existing debt aggressively for 60 to 90 days before applying. This action lowers your DTI and signals financial responsibility to lenders. Stop opening new credit accounts or making hard inquiries for at least three months before applying-each inquiry dings your score slightly, and multiple inquiries signal desperation to lenders.

If you have missed payments in your history, older missed payments hurt far less than recent ones. Focus on perfect payment behavior for the next 90 days. Secured loans backed by collateral like a vehicle or savings account offer 2% to 5% lower rates than unsecured loans, so if you have assets, leveraging them before improving your score makes financial sense.

Income Requirements and Fee Structures

CIBC’s minimum income requirement of $17,000 annually is the lowest threshold among major banks, but meeting that baseline means nothing if your credit score sits at 580. The origination fees ranging from 0.5% to 8% also matter significantly. A lender quoting 10% with a 0.5% fee beats one quoting 9.5% with a 5% fee, so always compare the all-in APR figure rather than the advertised rate alone.

Ready to Shop for Your Best Rate

Your credit score and DTI determine your starting position in the lending market, but they don’t determine your final rate. Shopping across multiple lenders reveals which ones value your profile most favorably, and negotiating with your bank can shift terms in your favor.

How to Actually Get the Best Rate

Gather Quotes from Multiple Lenders

Comparing personal loan offers from multiple lenders is non-negotiable if you want the best rate, but most borrowers comparison shop poorly. You need to obtain real quotes from at least five lenders within a short timeframe-ideally one or two days-because rates shift weekly. Contact Scotiabank, BMO, TD, CIBC, and RBC directly, then add two online lenders like goPeer or Spring Financial. Request a formal rate quote rather than just asking about advertised ranges; formal quotes show you the actual APR you qualify for based on your credit profile. This matters enormously because the difference between BMO’s advertised 8.99% and the 22.99% ceiling could mean $50 or $500 monthly depending on your creditworthiness.

Once you have five to seven quotes, compare the APR figures side by side-not the advertised rate-because APR includes origination fees that can add thousands to your total cost. Ratehub aggregates many of these offers, but calling lenders directly often reveals better promotional rates not listed online.

Negotiate With Your Current Bank

Your current bank holds more flexibility than you realize, especially if you maintain a decent account history. Call your relationship manager or visit a branch and tell them you have competing offers at lower rates; most banks have discretionary authority to beat competitor quotes by 0.5% to 1.5%. Banks value keeping customers more than acquiring new ones, so they’ll often adjust terms rather than lose you to a competitor. If your bank refuses to budge, take the better offer elsewhere.

Explore Credit Unions and Alternative Lenders

Credit unions typically undercut major banks by 1% to 3% on personal loans because they operate as member-owned cooperatives without shareholder pressure. Alternative lenders including peer-to-peer platforms offer flexibility that traditional banks reject, but their rates climb to 20% to 35% because they accept borrowers with poor credit histories. Only use alternative lenders if major banks and credit unions deny you outright; the higher cost rarely justifies the convenience.

Leverage Collateral to Lower Your Rate

Secured loans backed by your vehicle or savings account typically cost 2% to 5% less than unsecured loans from the same lender because collateral reduces their risk exposure. If you own a vehicle free and clear or have $5,000 or more in savings, securing your loan with that asset genuinely saves money over a five-year term.

Choose Between Fixed and Variable Rates

Fixed-rate loans prevent payment surprises when the Bank of Canada eventually raises rates again, while variable-rate loans track the 4.45% prime rate and could climb if economic conditions improve. Lock a fixed rate now unless you plan to repay the loan within 12 months; the economic uncertainty through 2026 makes variable-rate exposure unnecessarily risky for most borrowers.

Final Thoughts

Canada personal loan rates in 2026 hinge on the Bank of Canada’s 2.25% policy rate and the resulting 4.45% prime rate, but your actions determine whether you pay 6% or 24%. The rate environment remains stable now, but economic uncertainty means this window won’t stay open indefinitely. Lock a fixed-rate loan to protect yourself against future increases, and shop aggressively across major banks and online lenders to save thousands over your loan term.

Your credit score and debt-to-income ratio act as gatekeepers to better rates. Spend 90 days improving both before you apply, and you shift from the 18% to 22% tier into the 8% to 12% range at major banks. That difference compounds to real money over five years. Pay down existing debt, avoid new credit inquiries, and secure your loan with collateral if you own assets-all these actions move the needle significantly.

Gather formal quotes from Scotiabank, BMO, TD, CIBC, and RBC, then add two online lenders to your comparison. Compare APR figures side by side, not advertised rates, and call your current bank with competing offers to ask them to match or beat the best rate. We at Financial Canadian help borrowers like you navigate personal loan options with clarity and confidence, so you find the rate that actually fits your financial situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment