Mortgage rates shift constantly, and what made sense five years ago might cost you thousands today. At Financial Canadian, we’ve seen homeowners leave money on the table simply because they didn’t know when to refinance their mortgage in Canada.

The difference between refinancing and staying put can mean tens of thousands of dollars over your loan’s lifetime. This guide walks you through the exact moments when refinancing works in your favour-and when it doesn’t.

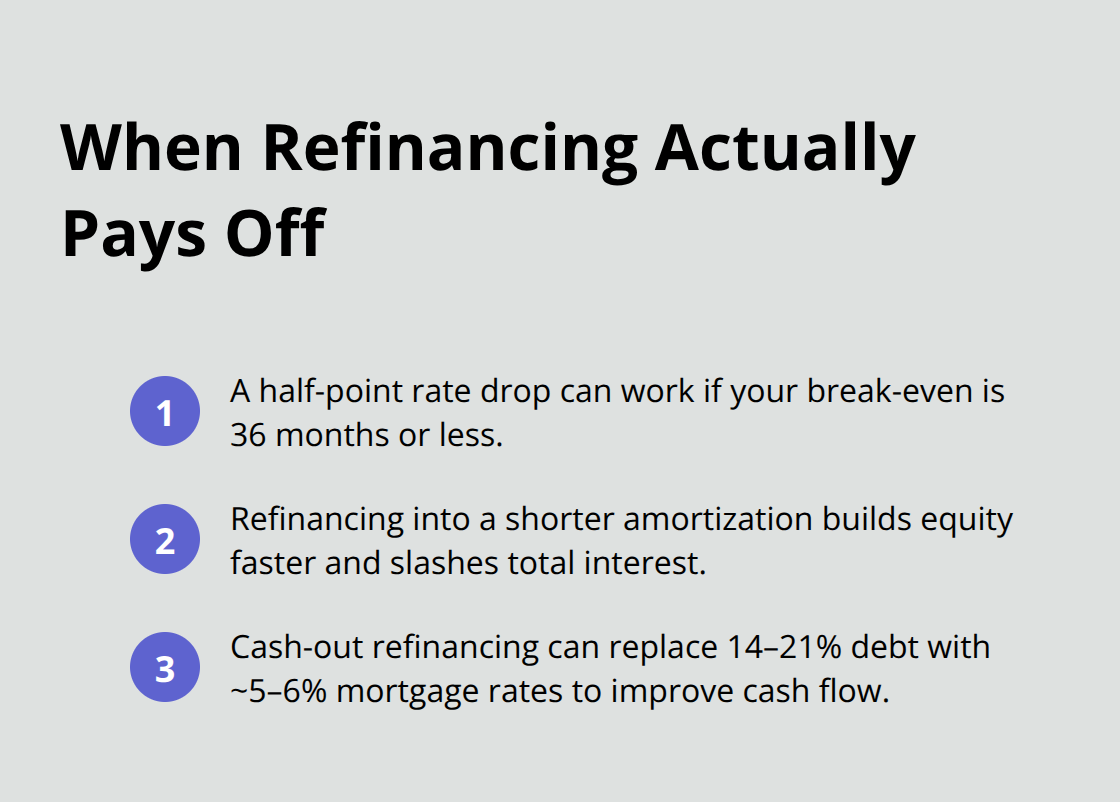

Three Scenarios Where Refinancing Actually Pays Off

The Half-Point Rate Drop That Adds Up

A rate drop of just 0.5 percent sounds modest until you do the math. On a $200,000 mortgage, that difference saves roughly $67 per month or about $804 annually. Over a 25-year remaining term, you’re looking at $20,000 in savings before closing costs. The industry standard suggests refinancing when rates fall by at least 1 percent, but we disagree.

If your break-even point-the time it takes to recoup closing costs through monthly savings-is under three years, refinancing at even 0.5 percent makes sense.

Calculate this yourself: divide your total refinancing costs (typically $2,000 to $3,500 in Canada) by your monthly savings. If the result is 36 months or less, move forward.

Accelerating Equity Through Shorter Amortization

Refinancing to a shorter amortization period works best when interest rates stay stable or decline. Switching from a 30-year to a 15-year mortgage accelerates equity building and slashes total interest paid. A homeowner with a $300,000 balance at 4 percent over 30 years pays roughly $215,000 in interest. Compress that to 15 years and interest drops to roughly $110,000-a $105,000 difference.

The trade-off is higher monthly payments, jumping from approximately $1,432 to $2,145. This strategy only makes sense if your income is stable and your budget absorbs the increase without stress.

Cash-Out Refinancing for Debt Consolidation

Accessing home equity for debt consolidation transforms refinancing from defensive to offensive. If you carry credit card debt at 14 to 21 percent interest, refinancing to pull out equity at 5 to 6 percent is mathematically unbeatable. Take a concrete example: a household with a $355,000 home purchased at 2.9 percent now faces rising living costs, paused bonuses, and high-interest credit card balances.

A cash-out refinancing of $40,000 at 5.8 percent increases the monthly payment modestly but eliminates 14 percent credit card debt and funds an emergency buffer plus home improvements. The decision hinges on whether consolidating debt and gaining liquidity justifies moving away from that exceptional 2.9 percent rate. High-interest debt destroys wealth faster than a low mortgage rate preserves it. If refinancing also funds a basement renovation that adds $50,000 to home value, the financial case strengthens further.

Verify with your lender whether minimum lump-sum requirements or other restrictions apply-some lenders impose thresholds that affect your ability to recast or refinance. Shop offers from three to five lenders before committing; compare annual percentage rates, not just rates, since APR includes fees and reveals true borrowing costs. The numbers tell you whether this move makes sense, but the costs and risks attached to refinancing demand equal attention before you sign anything.

Current Mortgage Rates and Refinancing Costs in Canada

Where Five-Year Fixed Rates Stand Today

Canada’s mortgage landscape in March 2026 reflects a market shaped by persistent inflation pressures and cautious central bank positioning. As of March 2026, the best five-year fixed insured rate is closer to 3.89%, while the best five-year variable rate is around 3.35%. Variable-rate mortgages sit around 5.5 to 5.95 percent, making fixed-rate products more attractive for borrowers who want payment certainty. The spread between lenders has widened, meaning your current bank’s renewal offer might be 0.3 to 0.5 percent higher than what a competing lender or mortgage broker can secure. This gap matters enormously-on a $300,000 mortgage, a 0.4 percent difference equals roughly $100 per month or $1,200 annually.

How Lender Competition Creates Opportunity

The competitive pressure is real, and lenders know homeowners shop around more aggressively than they did five years ago. Major lenders like TD, RBC, and Scotiabank publish rates daily on their websites, but these posted rates are almost never what you’ll actually pay-expect discounts of 0.5 to 1 percent off posted rates for borrowers with clean payment histories and at least 20 percent equity. Mortgage brokers access institutional lenders and alternative funding sources that retail banks don’t advertise, often finding rates 0.2 to 0.4 percent lower than Big Five banks. Comparing three to five lenders takes roughly two hours of work and could save you thousands over your mortgage term, making the effort genuinely worthwhile before you commit to anything.

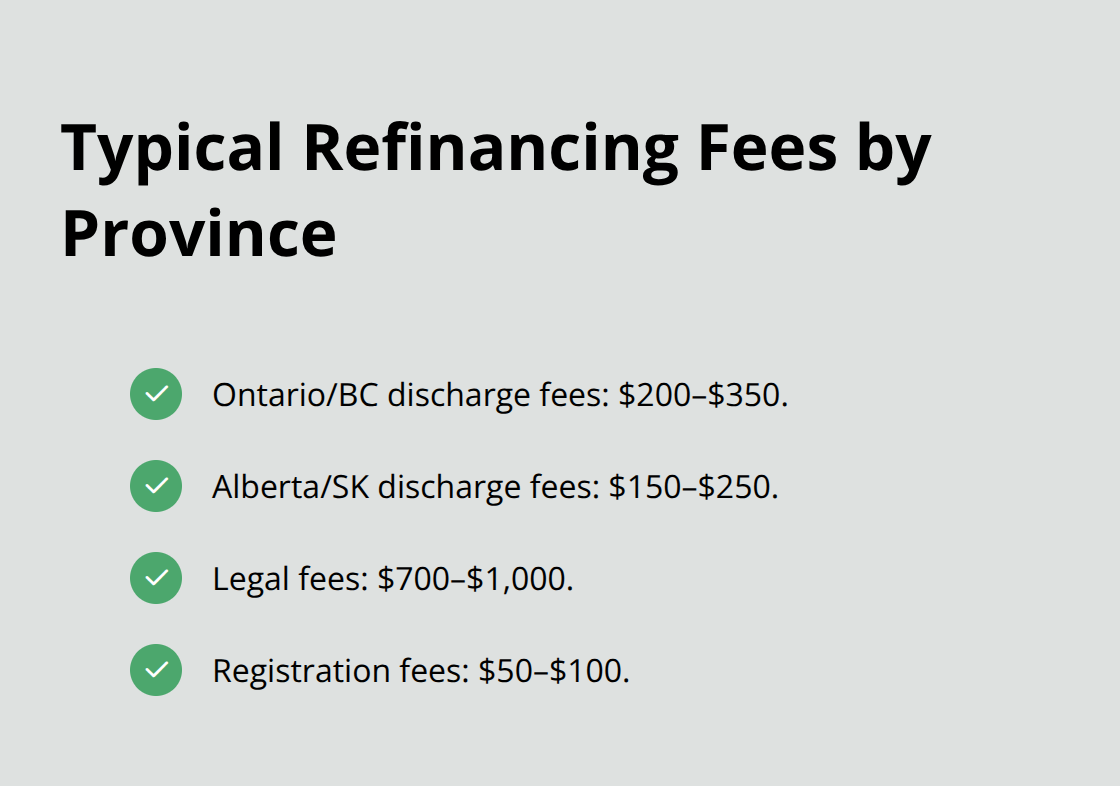

Provincial Variations in Discharge and Legal Fees

Provincial costs for refinancing vary significantly due to discharge fees, legal requirements, and registration charges that differ across jurisdictions. Ontario and British Columbia typically charge $200 to $350 for mortgage discharge, while Alberta and Saskatchewan run slightly lower at $150 to $250. Legal fees range from $700 to $1,000 depending on whether your lender covers them, with larger loan balances over $200,000 more likely to have fees absorbed.

Registration fees to place a new mortgage on title add another $50 to $100 per province.

Regional Advantages for Rate Negotiation

Western Canada’s lenders tend to be more aggressive on rate discounts for switch refinances, sometimes offering rate holds of 120 days compared to Ontario’s typical 90-day window. This means if you’re in Alberta or Saskatchewan with a strong credit profile, you have more negotiating leverage. The differences in provincial regulation create pockets where refinancing costs less and rate competition runs hotter, rewarding homeowners who understand their regional advantages. These cost variations and competitive dynamics set the stage for understanding when refinancing actually pencils out financially-and when the fees eat away your potential savings.

What Refinancing Actually Costs You

Prepayment Penalties That Catch You Off Guard

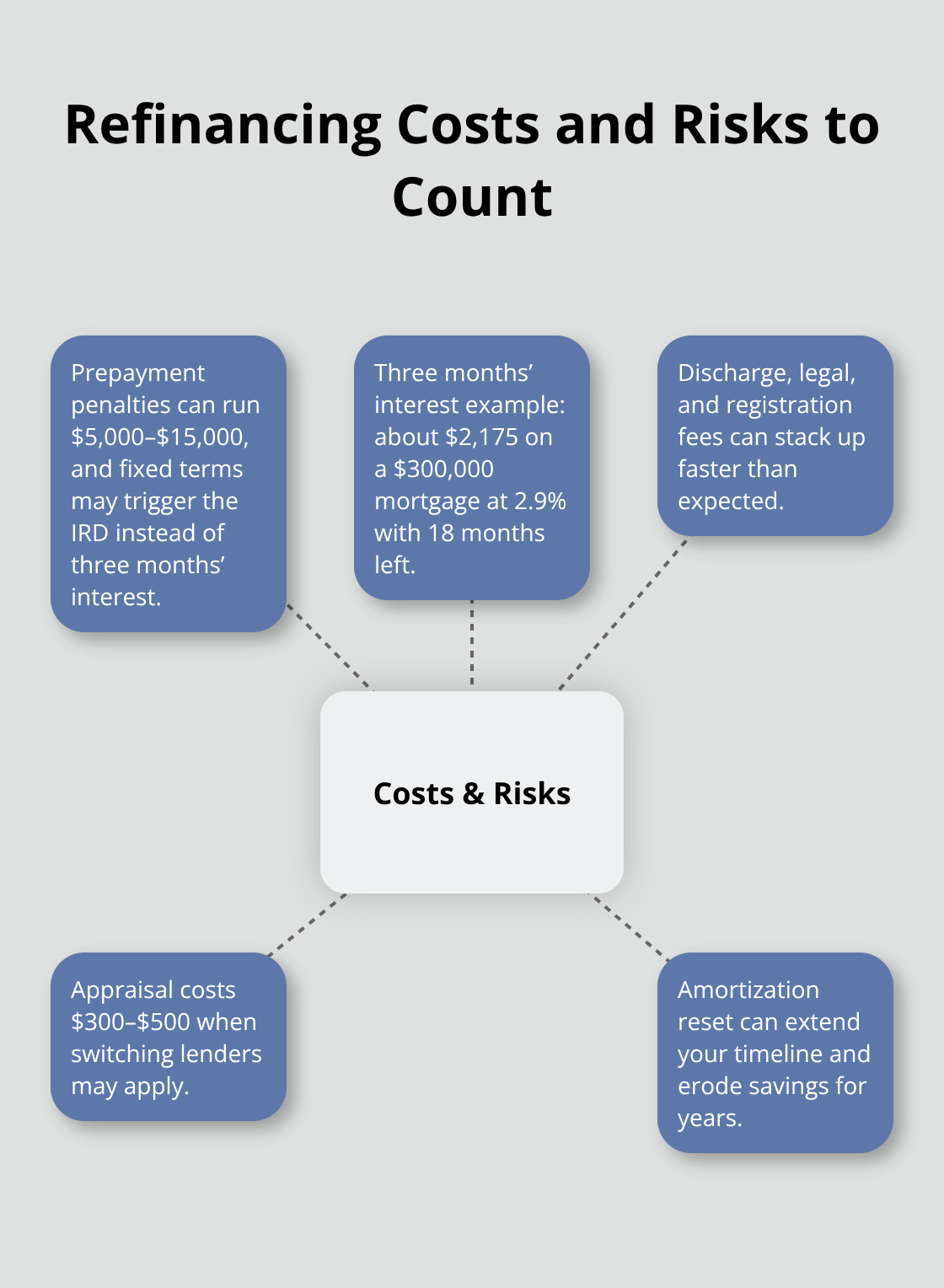

Refinancing fees blindside most homeowners. Your lender won’t volunteer that a prepayment penalty could cost $5,000 to $15,000, or that legal fees, discharge charges, and registration costs stack up faster than expected. If you break a fixed-rate mortgage early, you pay either three months’ interest or the interest rate differential, whichever is greater. On a $300,000 mortgage at 2.9 percent with 18 months left on your term, three months’ interest alone runs roughly $2,175.

The interest rate differential calculation proves more complex. Your lender compares your current rate against what they could lend that money for today, then charges you the difference multiplied by your remaining balance and term length. In a rising rate environment, this penalty balloons quickly. Variable-rate mortgages carry a simpler penalty: three months’ interest, period.

Discharge, Legal, and Registration Fees

Discharge fees from your current lender typically range from $200 to $350 depending on your province, with Alberta and Saskatchewan sitting at the lower end around $150 to $250. Ontario and British Columbia push toward $300 to $350. Legal fees for refinancing run $700 to $1,000 unless your new lender covers them, which happens more often with balances exceeding $200,000. Registration to place your new mortgage on title adds another $50 to $100.

Appraisals are often waived for refinances with established lenders, but switching institutions may require one, costing $300 to $500. Total costs easily reach $3,500 to $5,000 before you see a single payment reduction.

The Amortization Reset That Costs Thousands

The real damage happens when refinancing resets your amortization clock. Switching from year eight of a 25-year mortgage to a fresh 25-year term means you add seven years of payments back onto your timeline, even if your rate drops. That 0.5 percent savings evaporates if you now pay interest for an extra seven years.

The break-even calculation changes entirely when you factor in the amortization reset. If you refinance, insist on keeping your original amortization end date-amortization reset refinancing into a 17-year term instead of 25 years to match when you’d have paid off the original loan. This costs more monthly but prevents extending your debt timeline. Some lenders resist shorter amortizations because it reduces their interest income, so you may need to shop aggressively or work with a mortgage broker to find one willing to match your original payoff date.

Why Amortization Extension Destroys Your Savings

The math is unforgiving: resetting your amortization can cost you $30,000 to $50,000 in additional interest over your mortgage lifetime, obliterating any rate savings you thought you’d gained. Before signing anything, calculate your break-even point using your actual closing costs divided by monthly savings, then verify whether the amortization stays the same or resets. If it resets and extends past your original payoff date, walk away unless you’re consolidating high-interest debt where the math still wins.

Final Thoughts

Refinance mortgage Canada decisions require three conditions to align: your break-even point sits under three years, your amortization doesn’t reset past your original payoff date, and monthly savings justify the upfront costs. Start by gathering your current mortgage details-balance, rate, remaining term, and original amortization end date-then contact three to five lenders for written quotes that show the actual rate, closing costs broken down by line item, and the new amortization period. Compare annual percentage rates rather than just rates, since APR reveals true borrowing costs including fees, and a mortgage broker can access lenders your bank won’t show you, often uncovering rates 0.2 to 0.4 percent lower than Big Five institutions.

Hold off on refinancing if your break-even exceeds four years, your current rate sits below 3.5 percent with no sign of further drops, or you plan to move within the next two to three years. If refinancing forces your amortization to extend beyond your original payoff date and you’re not consolidating high-interest debt, walk away, since the additional interest you’ll pay destroys any rate savings. The two-hour effort to shop rates typically saves thousands, but only if the math actually works in your favour.

The decision ultimately rests on your specific situation: your income stability, your timeline in the home, and whether you’re solving a rate problem or a cash flow problem. We at Financial Canadian believe homeowners should make this decision armed with concrete numbers, not guesses, and our financial planning resources can help you organize your situation and explore how refinancing fits into your broader strategy. The refinancing decision is yours to make, but make it with clarity and confidence.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment