Buying your first home is one of the biggest financial decisions you’ll make. At Financial Canadian, we know that navigating first time mortgages in Canada can feel overwhelming, especially when you’re facing down payments, interest rates, and endless paperwork.

This guide breaks down the entire process into manageable steps. You’ll learn how to assess your readiness, secure pre-approval, and close on your new home with confidence.

Understanding Your Mortgage Readiness

Before you start house hunting, you need an honest assessment of your financial position. Your credit score is the first checkpoint. Lenders check this score to determine your interest rate and whether they’ll approve you at all. A score above 680 typically qualifies you for better rates, while scores below 600 make borrowing significantly more expensive or impossible.

Check Your Credit Score and Financial Health

Pull your credit report from Equifax or TransUnion to see exactly what lenders see. If errors exist, dispute them immediately-even small inaccuracies can cost you thousands in higher interest rates over a 25-year mortgage. Beyond your score, calculate your actual borrowing capacity using a mortgage affordability calculator. The federal stress test requires you to qualify at either 2% above your offered rate or 5.25%, whichever is higher. This means if a lender offers you 4.5%, you must prove you can afford payments at 6.5%. Federally regulated lenders enforce this stress test without exception, and it separates what banks will lend you from what you can actually handle monthly.

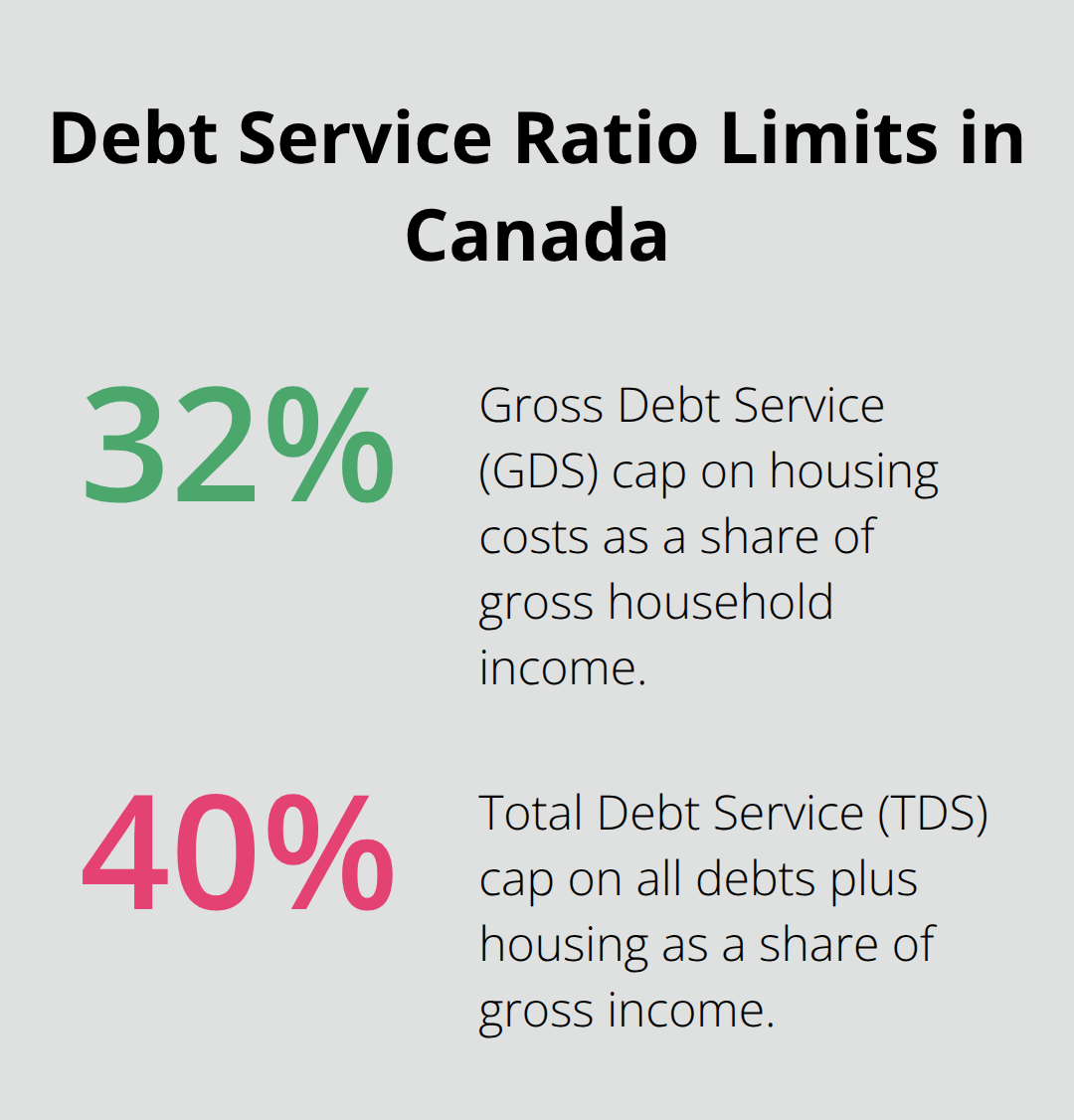

Understand Your Debt Service Ratios

Lenders examine your debt service ratios carefully. Your gross debt service ratio cannot exceed 32% of gross household income, meaning all housing costs combined cannot surpass that threshold. Your total debt service ratio cannot exceed 40%, which includes your mortgage, property taxes, utilities, condo fees if applicable, and all other debts like car loans and credit cards. A household earning $100,000 annually can carry roughly $32,000 in annual housing costs.

Add existing debt obligations and that number shrinks fast. Don’t focus solely on your gross income-lenders look at what remains after your obligations.

Determine Your Down Payment Strategy

The minimum down payment in Canada is 5% for insured mortgages, but this creates a false sense of affordability. At 5% down, you pay mortgage insurance premiums that add substantially to your costs. CMHC, Sagen, and Canada Guaranty are the primary insurers, and their premiums vary based on your down payment percentage and loan-to-value ratio. A 10% down payment reduces insurance costs meaningfully compared to 5%. At 20% down, you eliminate mortgage insurance entirely, which is the most significant financial advantage available. Try reaching 20% if you have access to a larger down payment.

The government’s Home Buyers’ Plan allows tax-free withdrawal of up to $60,000 from your RRSP if you’re a first-time buyer. The First Home Savings Account lets you contribute up to $8,000 annually with tax deductions and tax-free growth, with a lifetime limit of $40,000. These tools directly reduce the gap between your savings and your down payment target. Provincial programs add another layer. Ontario offers up to $4,000 in land transfer tax refunds for first-time buyers, while British Columbia provides up to $8,000 in land transfer tax relief. Quebec’s Home Purchase Assistance Program in Montreal reaches up to $15,000.

Gifted down payments from family members are permitted but come with documentation requirements. Lenders need proof the money is a gift, not a loan requiring repayment. Put this in writing with the gift giver to avoid complications at closing. Your down payment strategy directly determines your monthly payment, total interest paid, and whether you qualify at all.

Once you’ve assessed your credit, calculated your borrowing capacity, and mapped out your down payment sources, you’re ready to move forward with pre-approval-the next critical step that locks in your purchasing power.

Getting Pre-Approved and Finding the Right Mortgage

Pre-approval is not optional-it’s your financial baseline before you make any offer. A pre-approval letter from a lender shows sellers you’re serious and tells you exactly how much you can borrow. The process takes 1 to 3 business days and requires documentation: getting pre-approved for a mortgage in Canada involves providing identification, proof of employment, and proof you can pay for the down payment and closing costs. Lenders verify your income, check your credit report, and run the stress test calculation, which helps determine if borrowers will be able to afford their mortgages even if interest rates rise. The pre-approval remains valid for 120 days, giving you a window to house hunt without losing your rate hold. Many lenders offer rate holds during pre-approval, which locks in your quoted rate for that period. This matters because rates fluctuate daily. If rates rise 0.5% before you close, that difference costs you thousands annually. Get the rate hold in writing.

Compare Lenders and Mortgage Brokers

When comparing lenders, don’t stop at the first bank. Federally regulated lenders all enforce the same stress test, but their actual lending criteria vary. One bank might approve you at a higher amount than another, or offer better rates based on your specific profile. A mortgage broker accesses multiple lenders simultaneously, which saves you time and often reveals better options than calling banks individually. Brokers don’t charge you directly-lenders pay them-so use this advantage.

A mortgage broker is your advocate, not the lender’s. Brokers shop your application to 20+ lenders and present you with multiple options. Banks only show you their own products. If your credit is below 700 or your income is self-employed, brokers often find solutions banks immediately reject. However, brokers work best when you already have pre-approval documentation ready. Walk in organized.

Lenders scrutinize self-employed income closely-they want to see two years of tax returns and business financials. Recent graduates with limited credit history benefit from brokers because brokers know lenders who specialize in thin-file applicants. The stress test applies everywhere, but brokers negotiate better terms because they move volume. Banks prefer to stick with their standard rates, while brokers have flexibility to match competing offers.

Choose Between Fixed and Variable Rates

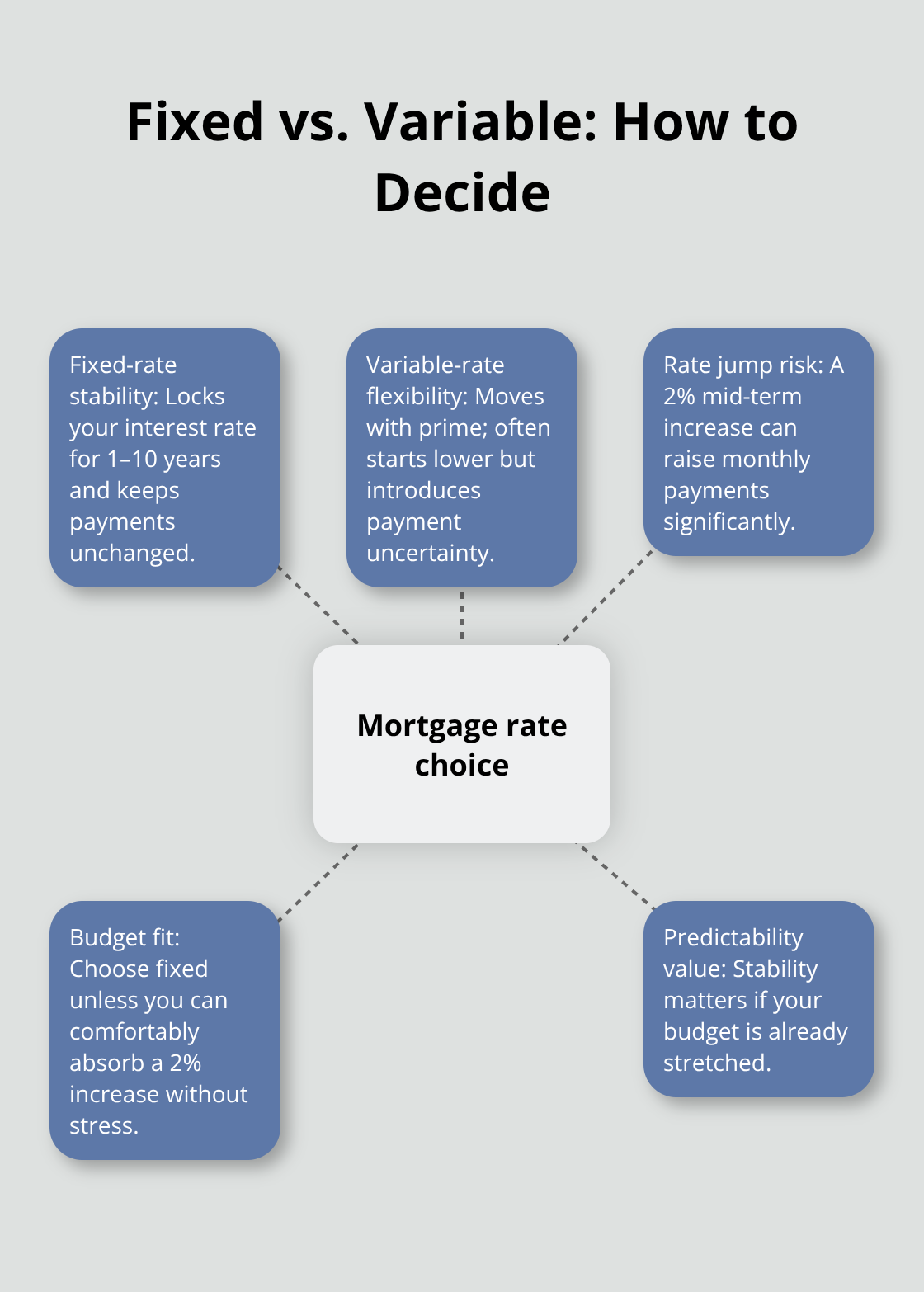

Mortgage types fall into fixed and variable categories. A fixed-rate mortgage locks your rate for the entire term, typically 1 to 10 years. You pay the same amount every month regardless of market changes.

A variable-rate mortgage fluctuates with the prime lending rate, usually offering a lower initial rate than fixed but carrying payment uncertainty. First-time buyers often feel drawn to variable rates because they start lower, but the risk is real. If rates jump 2% mid-term, your monthly payment can increase significantly.

Fixed rates provide predictability, which matters when you’re already stretching your budget. That low initial savings disappears quickly if rates climb. Choose fixed unless you have genuine flexibility in your budget and can absorb a 2% rate increase without stress.

Evaluate Terms and Portability

Shop around before committing. Get pre-approvals from at least two lenders or one bank plus one broker. Compare not just the rate but the fees, penalties for early repayment, and whether the lender allows porting your mortgage if you sell and buy again. A portable mortgage saves you from breaking your current mortgage early, which triggers significant penalties. That flexibility is worth investigating before you sign anything.

With pre-approval locked in and your mortgage type selected, you move into the application phase-where documentation and verification determine whether your offer becomes a binding commitment.

Submitting Your Application and Managing the Final Verification

Once you have pre-approval and an accepted offer, the lender’s underwriting team takes over. This phase typically lasts 10 to 15 business days and involves verifying everything you declared on your application. They pull your credit report again to catch any new debt you may have taken on, request recent pay stubs to confirm employment stability, and review your down payment source documentation. Do not open new credit accounts or make large purchases during this period. A new car loan or credit card approval tanks your debt service ratios and can kill your mortgage. Lenders see all credit inquiries within days.

Prepare for Underwriting Scrutiny

If you’re self-employed, prepare for additional scrutiny. Underwriters examine two years of tax returns, corporate financial statements, and notice of assessments from the CRA. They want to see consistent or growing income, not declining revenue. Any unexplained gaps in employment require a written explanation. Provide it immediately rather than waiting for them to ask. The faster you respond to document requests, the faster you close. Most delays happen because applicants are slow to provide paperwork.

Schedule Your Home Inspection

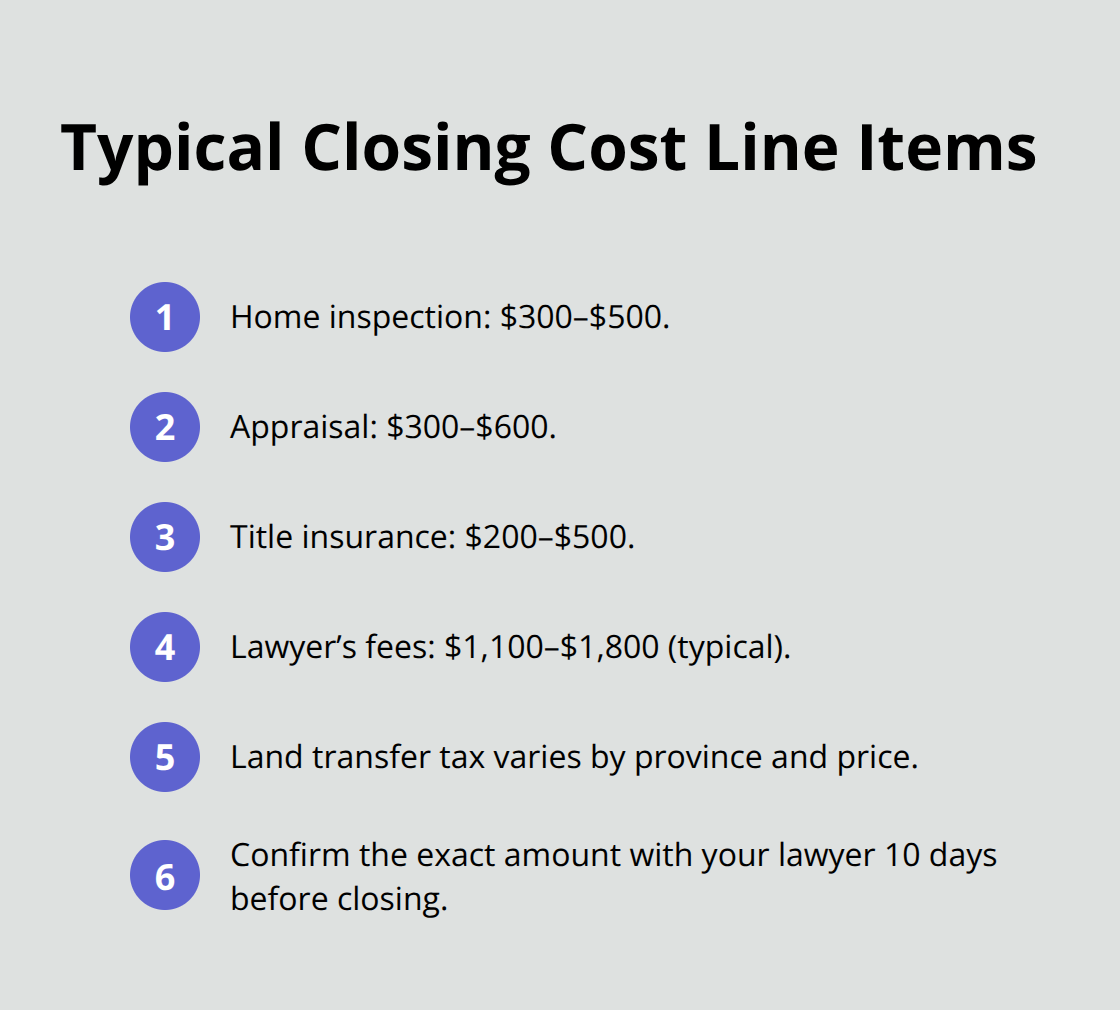

Your home inspection happens during the underwriting window and costs anywhere from $300 to $500. This step is your chance to uncover structural issues, roof problems, foundation cracks, or major system failures before you commit. Schedule a licensed home inspector through your real estate agent or independently. Do not skip this step regardless of the home’s age or condition. A thorough inspection identifies hidden defects that could cost tens of thousands to repair.

Understand the Appraisal Process

The appraisal, ordered by your lender and costing $300 to $600, ensures the home’s value supports the mortgage amount. If the appraisal comes in below your purchase price, you have a problem. The lender will only finance based on the appraised value, not what you agreed to pay. This means you either need to increase your down payment or renegotiate the price with the seller. Low appraisals happen in soft markets or overpriced neighbourhoods. Request a copy of the appraisal report to understand the lender’s valuation.

Handle Title Insurance and Legal Requirements

Your real estate lawyer handles the title search and insurance, costing $200 to $500. Title insurance protects you if someone later claims ownership rights to the property. It’s non-negotiable and your lender requires it. Your lawyer also prepares the mortgage documents, reviews the purchase agreement, calculates closing costs, and coordinates the final walkthrough.

Calculate and Plan for Closing Costs

Closing costs typically total 3 to 4 percent of the purchase price for resale homes. Land transfer tax, your largest closing cost, varies by province. Ontario charges 4 percent on homes over $475,000 but offers first-time buyer rebates reducing this substantially. British Columbia applies a 5 percent tax on purchases over $500,000 with a first-time home buyers’ program that reduces or eliminates property transfer tax. Calculate your exact closing costs using your province’s tax rates and your lawyer’s fee estimate ($1,100–$1,800 is typical). Do not assume you can cover these costs with your remaining savings.

Many first-time buyers discover closing costs exceed their cash reserves by closing week. Plan ahead and confirm the exact amount with your lawyer 10 days before closing.

Final Thoughts

Buying your first home through first-time mortgages in Canada requires discipline, preparation, and honest self-assessment. The path from pre-approval to closing involves multiple checkpoints, each designed to protect both you and your lender. You’ve now seen how credit scores determine your rates, how stress tests verify affordability, and how closing costs can surprise you if you don’t plan ahead.

The most common mistake first-time buyers make is stretching their budget to the absolute maximum the lender approves. Just because a bank will lend you $500,000 doesn’t mean you should borrow it. Your actual comfort zone should sit 10 to 15 percent below your maximum approval, which protects you when unexpected repairs arise, interest rates climb at renewal, or your income fluctuates.

Pull your credit report today and dispute any errors. Calculate your actual borrowing capacity using a mortgage affordability calculator, research your provincial down payment assistance programs, and contact at least two lenders or a mortgage broker to begin pre-approval conversations. We at Financial Canadian help financial professionals communicate clearly with clients facing these exact decisions through our financial content services, and we’re here to support your journey toward homeownership.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment