When you need cash fast, a Canada same day loan can feel like the only option. But speed shouldn’t come at the cost of your financial health.

At Financial Canadian, we believe fast borrowing and smart borrowing can go hand in hand. This guide walks you through how same day loans work, how they stack up against other quick credit options, and how to borrow responsibly.

How Same Day Loans Work in Canada

Application Process and Requirements

You can apply for a same day loan in Canada through a simple online process that takes just minutes. Most lenders require you to be at least 18 years old, have a valid bank account with online banking enabled, and show proof of employment income or benefits like Employment Insurance. You’ll provide basic personal information, employment details, and banking credentials to complete your application. Many lenders skip traditional credit checks entirely, which means your credit score won’t disqualify you from borrowing. This approach opens doors for people with poor credit or no credit history at all.

Approval Timeline and Funding Speed

Approval for a same day loan typically happens within a few hours to one business day, depending on when you apply and which lender you choose. PAY2DAY, for example, delivers funds via e-transfer within 1–2 hours after approval-genuinely fast compared to waiting days for a traditional bank loan. If you apply early in the business day, you could have money in your account by afternoon. Online applications remain available 24/7, so you can submit your request at midnight if needed, though approval may wait until business hours. Some lenders offer mobile apps that let you track your application status in real time, eliminating the uncertainty of wondering whether your request got lost.

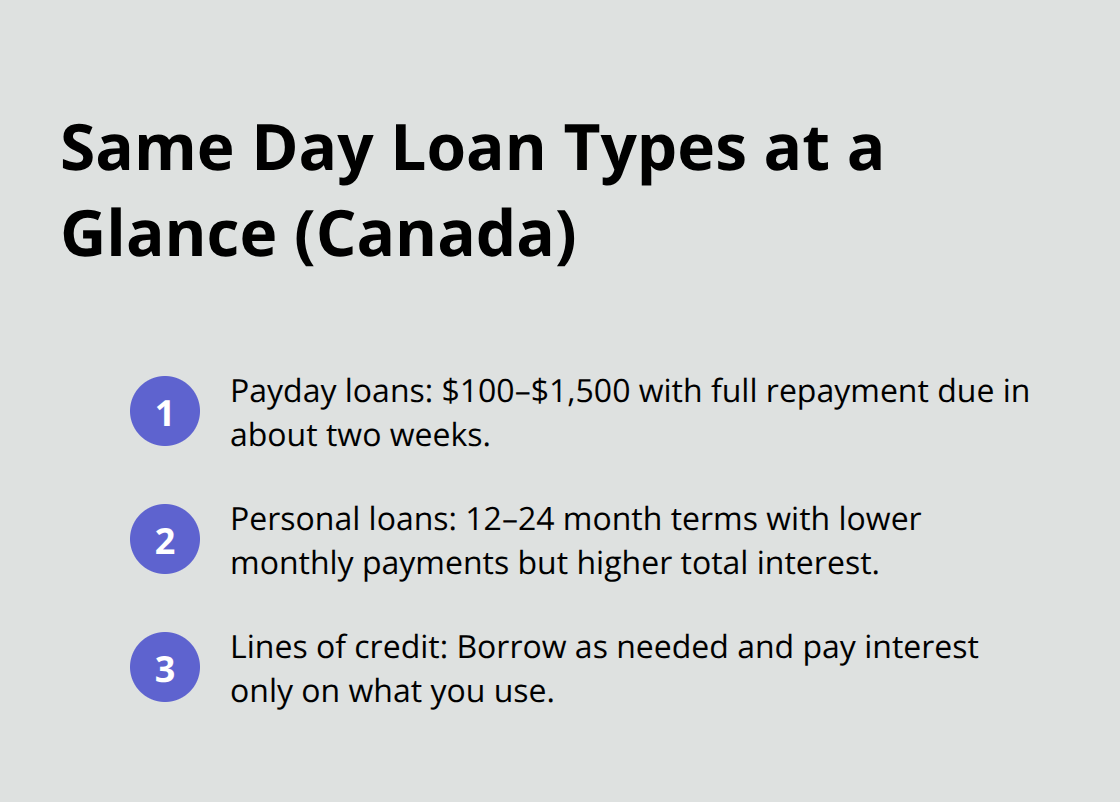

Types of Same Day Loans Available

Same day loans come in different forms depending on your province and lender. Payday loans represent the most common type, typically ranging from a few hundred to $1,500, and you must repay them in full within two weeks. In Ontario, payday loan interest rates cap at $14 per $100 borrowed, so a $500 advance costs $70 in interest over 14 days. Personal loans offered through some same day lenders feature longer repayment terms, sometimes stretching 12–24 months, which means lower monthly payments but higher total interest. Line of credit products work differently-you access funds as needed and only pay interest on what you actually use.

The key difference between these options lies in repayment flexibility. Payday loans demand full repayment by a specific date with no extensions or rollovers allowed, which makes them riskier if your income is unpredictable. Personal loans and lines of credit give you breathing room with scheduled payments over time.

You should assess whether you can repay the full amount on the due date before choosing a payday loan; if you cannot, a longer-term product makes more financial sense, even if the interest rate appears higher initially.

Understanding these loan types sets the stage for comparing them against other quick credit options available to Canadian borrowers.

Comparing Same Day Loans to Other Quick Credit Options

Payday Loans vs Personal Loans

Payday loans dominate the same day lending space, but they’re far from your only option for fast cash. Personal loans, credit card cash advances, and lines of credit each solve different financial problems, and choosing between them means understanding where your situation fits. A payday loan works best when you need $500 to $1,500 and can repay it within two weeks, but this rigid structure fails if your cash flow is unpredictable. Personal loans stretch repayment across months or years, lowering your monthly burden but costing significantly more in total interest over time.

A $1,500 payday loan in Ontario costs $210 in interest over 14 days, while a $1,500 personal loan over 12 months at 20% APR costs roughly $1,966 total-that’s $166 monthly but $466 in total interest. The monthly payment matters more than the APR when you’re living paycheck to paycheck, making personal loans genuinely safer for people whose income varies.

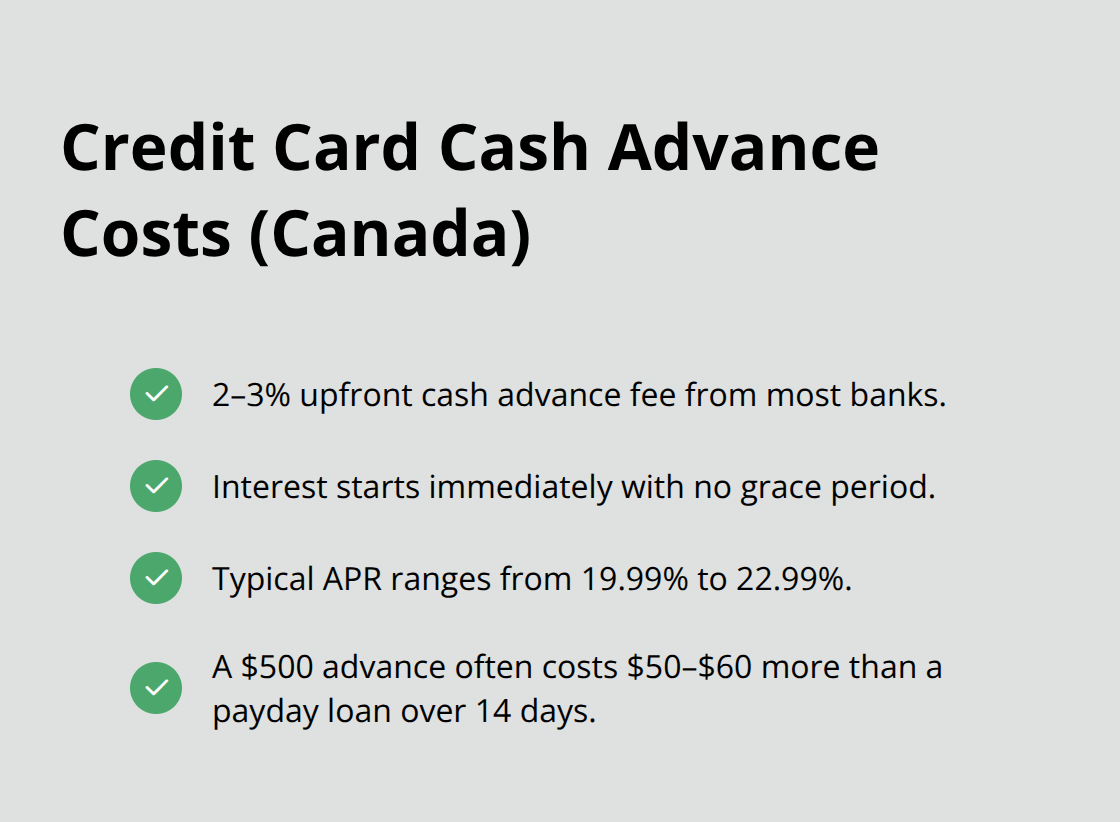

Credit Card Cash Advances vs Same Day Loans

Credit card cash advances seem convenient because you already have the card, but they’re deceptively expensive. Most Canadian banks charge 2–3% upfront fees plus daily interest starting immediately at rates between 19.99% and 22.99% APR, with no grace period unlike regular purchases. A $500 cash advance costs $10–$15 instantly, then accrues interest daily until repaid-withdrawing $500 on a credit card typically costs $50–$60 more than a payday loan over 14 days.

Lines of Credit as an Alternative

Lines of credit present a smarter alternative if you qualify, offering interest rates between 7% and 15% APR depending on your credit score and lender. You only pay interest on what you use, so a $5,000 available line costs nothing until you actually borrow $1,000 and gives you flexibility without the fee trap. The critical difference: lines of credit require decent credit to qualify, while payday loans accept anyone with employment income and a bank account.

If you have poor credit but need flexible repayment, a personal loan from a same day lender beats both credit card cash advances and payday loans, even if the interest rate looks higher on paper. This comparison reveals that your credit history and repayment timeline should drive your choice, not just the advertised interest rate. Understanding these distinctions prepares you to make a decision that actually fits your financial reality-which brings us to the practices that separate smart borrowing from reckless borrowing.

How to Know If You Can Actually Afford a Same Day Loan

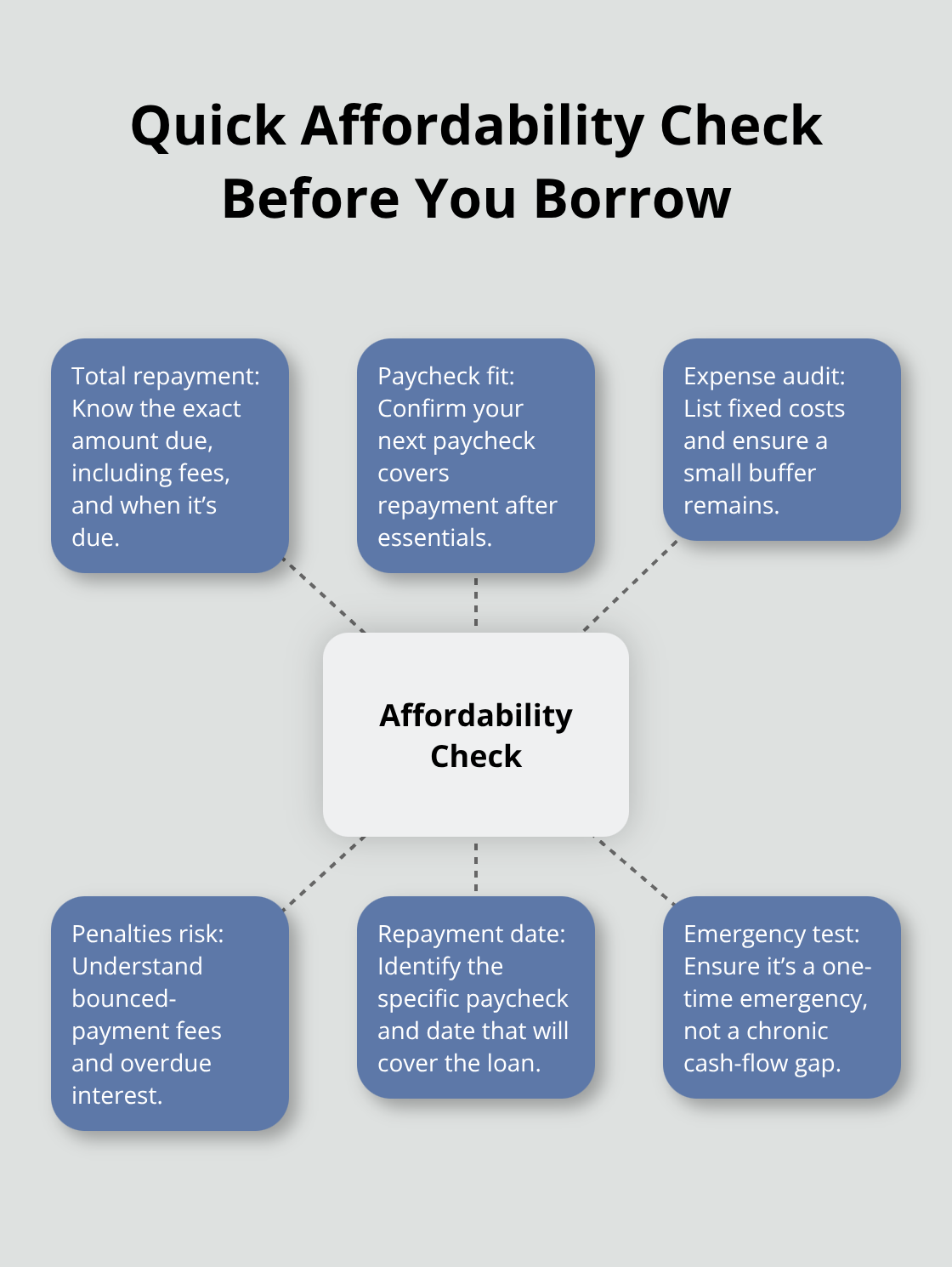

The moment before you click submit on a same day loan application is when most borrowers stop thinking clearly. Desperation clouds judgment, and lenders count on this. The smartest financial decision happens before you apply, not after approval arrives. You need to understand exactly what you’re paying, calculate whether your next paycheck covers repayment, and honestly assess whether borrowing solves your problem or just delays it.

Calculate Your True Cost

Start with the actual numbers, not the advertised APR. In Ontario, a $1,000 payday loan costs $140 in interest over 14 days, meaning you repay $1,140 total. That $140 isn’t theoretical-it comes directly from your next paycheck. If your paycheck is $2,000 and you owe rent of $1,200, utilities of $300, and food of $250, that $140 loan fee leaves you with only $110 for everything else. The math doesn’t work.

Most people who default on payday loans didn’t miscalculate the interest rate; they miscalculated their actual available income after essential expenses. Write down every fixed expense you have: rent, insurance, groceries, debt payments, childcare. Subtract that total from your expected income. If the remaining amount doesn’t cover the loan repayment plus a small buffer, you cannot afford this loan, regardless of how quickly you get approved.

Account for Late Payment Penalties

The second trap is underestimating how late payment penalties destroy your finances. PAY2DAY charges a returned item fee if your payment bounces, plus interest on the overdue amount. A $1,000 loan that goes unpaid for just 10 days costs additional fees and interest on top of the original $140 interest. Now you’re deeper in debt because you couldn’t repay on schedule.

This is why repayment certainty matters more than interest rates. A personal loan at 25% APR over 12 months costs $1,308 total on a $1,000 advance-higher total interest, but $109 monthly payments you can plan around. A payday loan costs $140 but demands the full $1,140 on a specific date, and missing that date triggers penalties that compound quickly. Before borrowing, identify exactly which paycheck will cover repayment and confirm that paycheck amount in writing from your employer. If you cannot name the specific date you’ll have the money, do not borrow.

Distinguish Emergency Borrowing from Chronic Borrowing

Your financial situation also determines whether a same day loan is the right tool or a symptom of a larger problem. If you borrow to cover a one-time emergency-a car repair or unexpected medical bill-a same day loan serves its purpose. You repay it and move forward. But if you borrow because your regular income doesn’t cover your regular expenses, a same day loan is a band-aid on a structural problem.

Borrowing $500 this month and $600 next month means you pay interest annually just to survive, which is money that could go toward increasing your income or reducing your expenses. Assess whether this is truly an emergency or a sign that your budget needs restructuring. Many people discover they borrow because of subscription services, dining out, or discretionary spending they didn’t realize was unsustainable.

Track Spending Before You Apply

Track your spending for 30 days before applying. If you find $300 in cuts, make those cuts first. If you still need to borrow after that, you make a clearer-eyed decision. This honest evaluation separates people who use same day loans strategically from people who use them as a permanent crutch that slowly crushes their finances.

Final Thoughts

A Canada same day loan solves real problems when you approach it with clear eyes and honest math. Speed matters only if you actually need the money today, not because borrowing feels easier than finding alternatives. We at Financial Canadian have seen borrowers transform their financial situations by making one decision differently: they assessed their ability to repay before applying, not after approval arrived.

Same day loans work best for genuine emergencies where you have a specific repayment date locked in. A car repair that costs $800 and you receive your paycheck in five days is a legitimate use case, while borrowing $500 because you overspent on groceries and subscriptions is not. Whether you have excellent credit or poor credit, the real question remains the same: can you repay this amount on this specific date without sacrificing essential expenses or triggering late payment penalties?

Finding a reputable lender matters because predatory operators exist alongside legitimate ones. Look for lenders licensed in your province, transparent about fees and interest rates, and willing to explain the total cost before you commit (PAY2DAY operates across multiple provinces with clear fee structures and 24/7 customer service, representing the standard you should expect). We at Financial Canadian can help you explore your borrowing options and find a lender that matches your actual financial situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment