Buying a home in Canada means navigating mortgage options, rates, and approval processes that can feel overwhelming. We at Financial Canadian created this guide to break down what you actually need to know.

From fixed and variable rates to stress testing requirements, we’ll walk you through the decisions that matter most for your financial situation.

Types of Mortgages Available to Canadian Homebuyers

Fixed-rate mortgages lock in your interest rate for the entire term, so your payment stays the same whether rates rise or fall. This stability appeals to borrowers who want predictable monthly payments and protection against future rate increases. If you plan to stay in your home for several years and prefer knowing exactly what you’ll pay each month, a fixed rate removes the guesswork from your budget. The trade-off is that fixed rates are typically higher than the initial rate on variable mortgages, so you pay for that certainty.

When Variable Rates Make Sense

Variable-rate mortgages tie your payment to the prime rate, which moves with Bank of Canada policy decisions. The prime rate is currently steady at 4.45%, with markets pricing the Bank of Canada at 2.25% through July of 2026. This discount reflects lender competition to attract borrowers, and it represents a real incentive worth considering. If the Bank of Canada cuts rates over the next year or two-which becomes more likely as inflation cools-your payment could drop significantly. A borrower who locks in a variable rate would see immediate savings if rates fall, potentially saving thousands over the mortgage term. The risk is that if rates climb, your payment increases, which requires budget flexibility. Variable mortgages work best if you have emergency savings to cover payment increases and you expect rates to decline.

Open Versus Closed Mortgages

Closed mortgages restrict your ability to pay off the mortgage early without penalties, but they offer lower interest rates in exchange for that commitment. Most Canadian homebuyers choose closed mortgages because the rate savings outweigh the flexibility loss. Open mortgages let you prepay or refinance without penalty, making them useful if you expect a windfall or plan to sell soon, but lenders charge 0.5–1% higher rates to compensate for that freedom. Unless you have a specific reason to need prepayment flexibility, a closed mortgage delivers better value.

The current market shows that the rate gap between open and closed mortgages makes closed the stronger choice for buyers who plan to hold their mortgage for several years.

Your mortgage type shapes your financial stability for years to come, which is why understanding these options matters before you approach a lender. The next step involves learning what factors actually influence the rate you’ll receive.

Key Factors That Affect Your Mortgage Rate

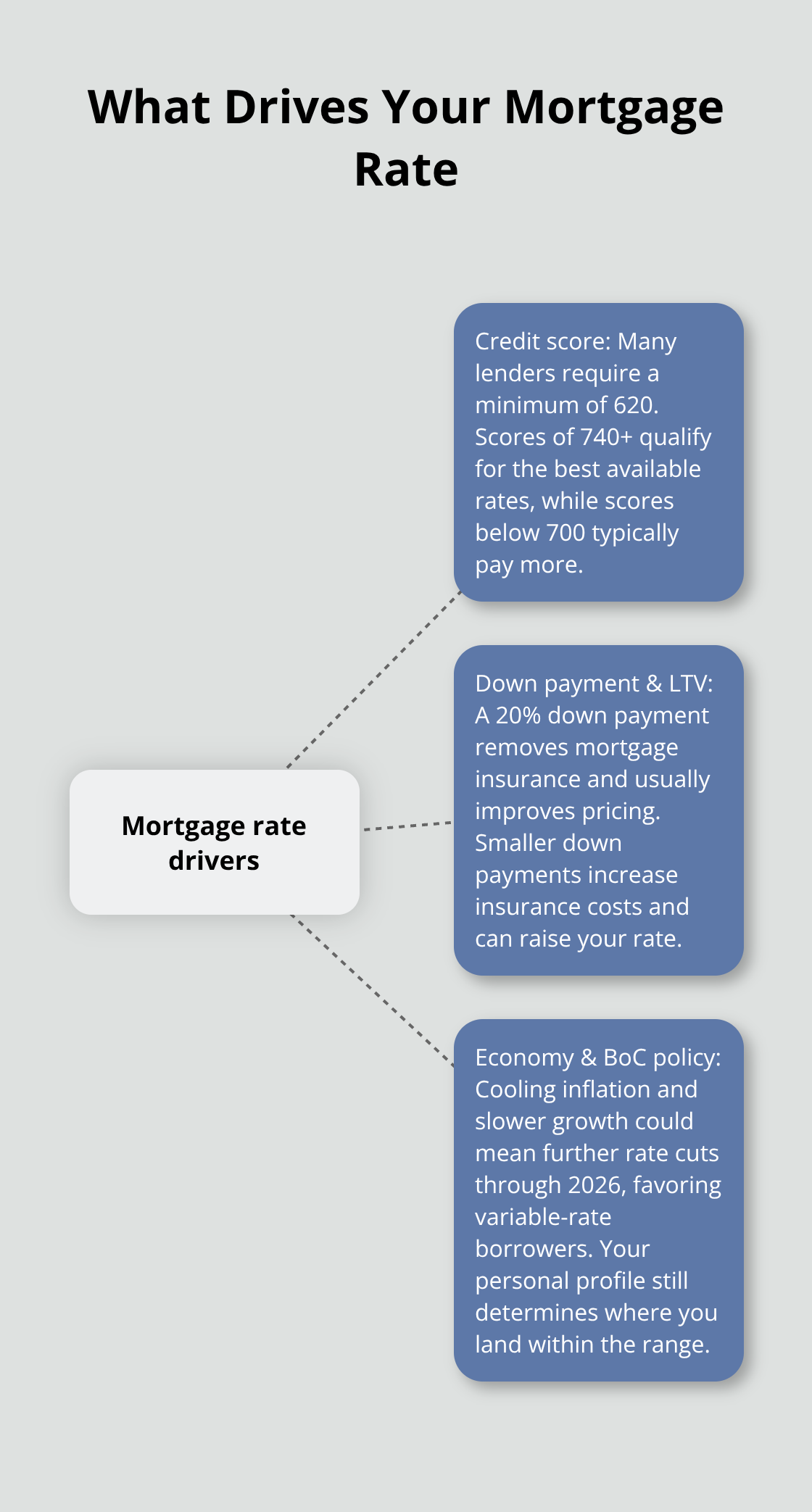

Credit Score: Your Most Powerful Lever

Your credit score is the single most important factor lenders examine, and it directly translates to the rate you’ll pay. Lenders in Canada typically require a minimum credit score of 620 to qualify for a mortgage, but scores below 700 result in significantly higher rates. If your score sits between 620 and 679, you can expect to pay 0.5–1.5% more than borrowers with excellent credit. A score of 680–739 puts you in the standard range, while 740 and above qualifies you for the best available rates.

Your payment history over the last two years matters most-recent defaults or missed payments hurt you far more than older issues. If you plan to buy within six months, make every payment on time and pay down existing debt to boost your score before you apply. Check your credit report through Equifax or TransUnion at no cost to see exactly where you stand.

Down Payment Size and Loan-to-Value Ratio

Your down payment size and the resulting loan-to-value ratio shape both your rate and your insurance costs. A down payment of 20% or more eliminates mortgage insurance entirely and typically qualifies you for the best rates available. If you put down 15–19%, you’ll pay mortgage insurance but still access competitive rates.

Down payments below 15% trigger higher insurance premiums that add thousands to your total cost. A 5% down payment on a $500,000 home costs roughly $20,000 in insurance fees alone. This difference means that increasing your down payment from 10% to 15% often saves you more money than negotiating a lower interest rate.

Economic Conditions and Bank of Canada Policy

The Bank of Canada’s policy decisions and current economic conditions create the backdrop for all mortgage pricing, but your personal situation determines where you land within that range. With inflation cooling and economic growth slowing, the Bank of Canada has signaled that further rate cuts are possible through 2026, which benefits variable-rate borrowers. However, your credit profile and down payment remain the levers you actually control.

Lenders apply stress testing rules that require you to qualify at a rate 2% higher than your actual mortgage rate. This means improving your credit score and increasing your down payment directly improves your approval odds and reduces the rate you’ll pay. Understanding these three factors positions you to take concrete action before you approach a lender-and that preparation determines whether your application sails through or faces obstacles.

Getting Approved for a Mortgage in Canada

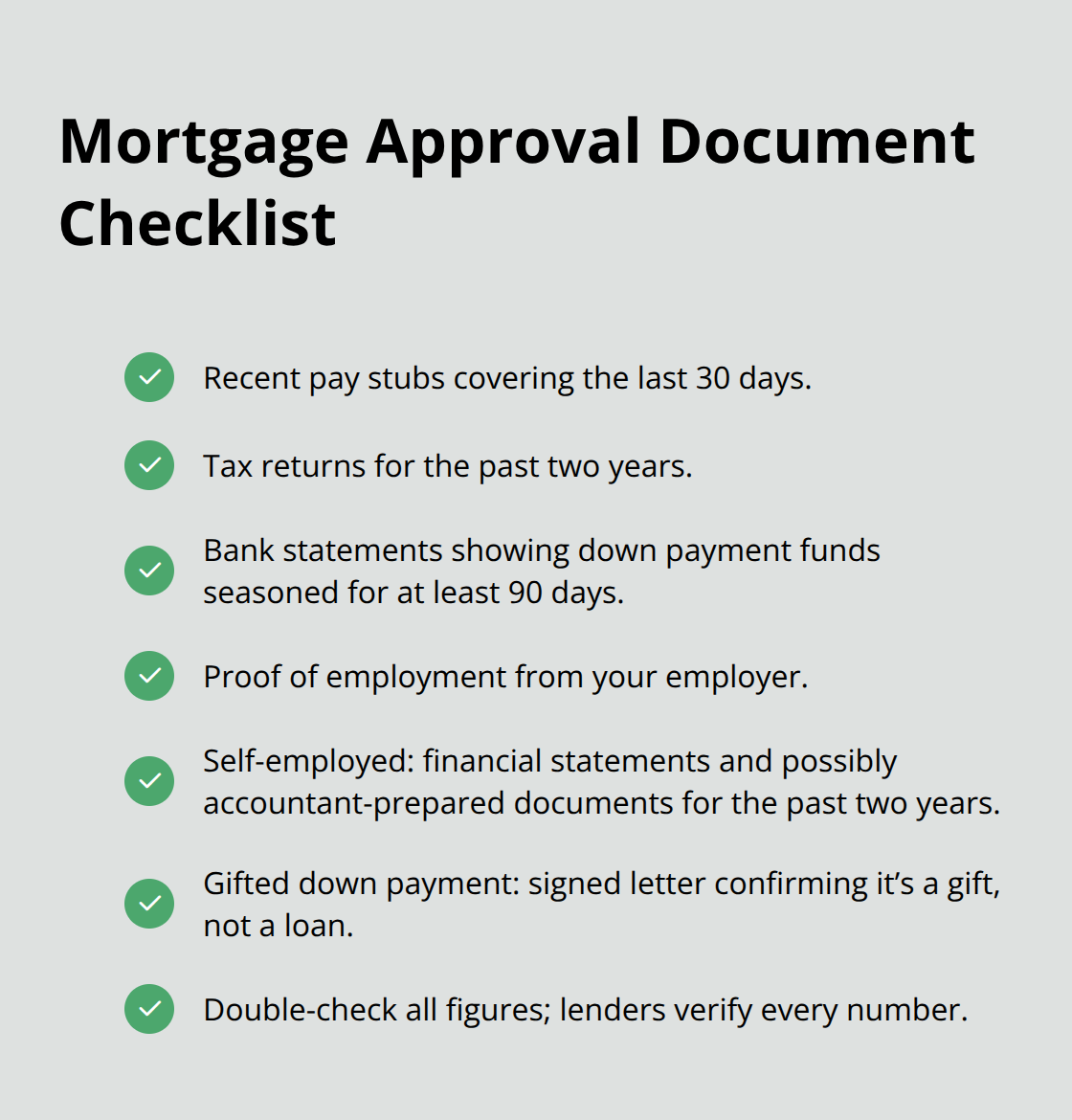

Lenders require substantial documentation before they approve your mortgage, and submitting everything correctly the first time accelerates your application. You’ll need recent pay stubs covering the last 30 days, tax returns for the past two years, bank statements showing your down payment savings for at least 90 days, and proof of employment from your employer. If you’re self-employed, you must provide financial statements and possibly accountant-prepared documents for the past two years. Lenders verify every number because mortgage fraud costs the industry millions annually, and they’re legally required to confirm your income matches what you claim.

Start organizing these documents now, even if you’re not applying immediately-this preparation saves weeks later. One detail many borrowers miss: if you received a gift for your down payment, the lender needs a signed letter from the gift-giver stating it’s a gift and not a loan. Without this letter, lenders treat the gift as debt against you, which destroys your debt-service ratios and may disqualify you entirely.

How Stress Testing Works

Stress testing is where many qualified borrowers stumble, and understanding this rule changes how you should approach your mortgage application. Canadian lenders must qualify you at a rate 2.25% higher than your actual mortgage rate. This means your monthly payment must fit within lender limits at that higher hypothetical rate, not at your actual rate. The government introduced this rule after 2016 to prevent borrowers from overextending themselves, but it’s now the main barrier blocking otherwise credit-worthy buyers.

Improving Your Stress-Test Position

If you’re earning $80,000 annually with excellent credit but only $15,000 saved for a down payment, stress testing will likely reject you because your debt-service ratios fail at the stress-test rate. The practical solution involves increasing your down payment before applying-every percentage point higher reduces the mortgage amount and immediately improves your stress-test numbers. Alternatively, you can pay down existing debts like car loans or credit cards to shrink your total debt load and create more room in your ratios.

Many applicants don’t realize they can improve their approval odds by spending two months eliminating $5,000 in credit card debt rather than waiting to save another $10,000 for the down payment. Work backwards from your target mortgage amount, calculate what the stress-test rate means for your monthly payment, and confirm you fit within the lender’s guidelines before you formally apply.

Final Thoughts

The mortgage decisions you make today shape your financial stability for the next 15 to 25 years, which is why rushing through this process costs money you can’t recover. You now understand how fixed and variable rates work, what lenders actually examine, and how stress testing affects your approval odds. The next step involves comparing actual offers from multiple lenders rather than accepting the first rate quoted to you.

When you receive mortgage offers, compare the interest rate, the term length, and the total cost over the full amortization period. A lender offering 3.94% on a 5-year fixed might cost you thousands more than a competitor at 3.99% if their fees are lower or their prepayment terms are more flexible. Request written offers from at least three lenders and ask each one to explain their fees, penalties for early repayment, and any conditions attached to the rate.

The mortgage landscape in Canada rewards borrowers who prepare thoroughly and compare options carefully. Your credit score, down payment size, and debt levels are levers you control right now, and Financial Canadian offers responsive web design with SEO optimization to help you reach more buyers in your market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment