Getting your first mortgage in Canada is competitive. Lenders receive dozens of applications weekly, and they’re looking for applicants who stand out through financial discipline and preparation.

At Financial Canadian, we’ve seen firsthand what separates approved borrowers from rejected ones. It’s not luck-it’s having your finances organized, your credit solid, and your documentation ready before you walk through the door.

Your Credit Score Matters More Than You Think

Check Your Credit Report for Errors

Your credit score is the first filter lenders use to decide whether to move your application forward. In Canada, scores range from 300 to 900, and most lenders want to see 660 or higher before they’ll seriously consider you. Equifax and TransUnion are the two credit bureaus that manage Canadian scores, and you must pull your report from both before you apply.

Many borrowers find errors on their reports that actively hurt their approval chances. You should check yours immediately and look for accounts you don’t recognize, incorrect payment histories, or duplicate entries. These mistakes happen more often than you’d think, and disputing them takes 30 days or more, which is why you need to start early.

Reduce Your Debt-to-Income Ratio

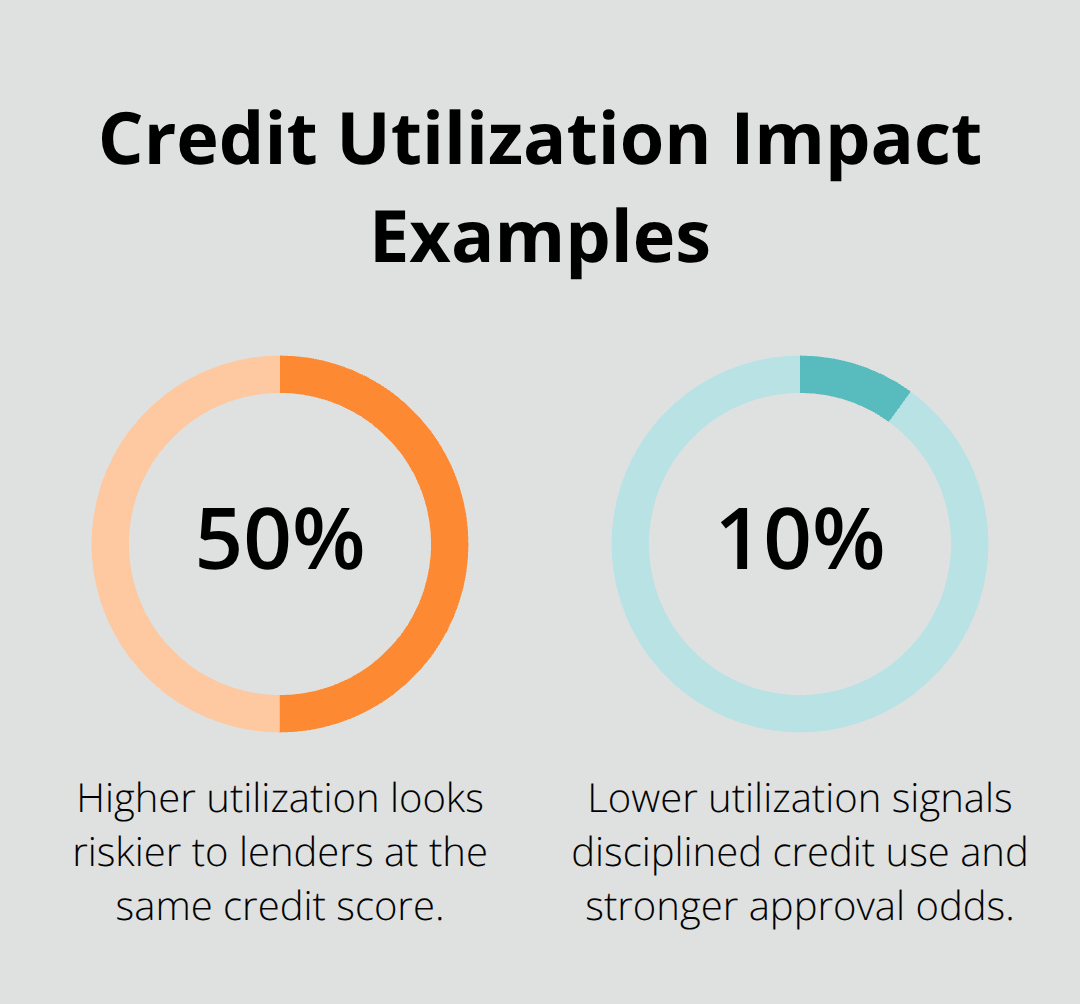

Your debt-to-income ratio directly influences what lenders offer you. If you carry credit card balances, car loans, or other debts, you should pay them down before applying to strengthen your position significantly. A borrower with a 700 credit score but 50% credit utilization looks riskier than someone with the same score using only 10% of available credit.

Lower debt means more borrowing power for your mortgage. You should start with high-interest debt first, as this reduces both your utilization rate and the total interest you’re paying. The math is straightforward: lenders see less risk when you demonstrate control over existing obligations.

Avoid New Credit Applications Before Applying

You must resist the temptation to open new credit accounts in the months before your mortgage application. Each new application triggers a hard inquiry that temporarily lowers your score, and lenders view new accounts as increased risk. This means no new credit cards, no store financing, and no car loans during your pre-approval period (typically 90 to 120 days).

Your goal is to show stability and restraint, not activity. Lenders want to see that you’ve prepared deliberately for this moment. With your credit report cleaned up and your debt reduced, you’re ready to demonstrate the financial discipline that separates strong applicants from weak ones-and that starts with the next critical step: building a down payment that lenders can’t ignore.

What Down Payment Size Actually Gets You Approved

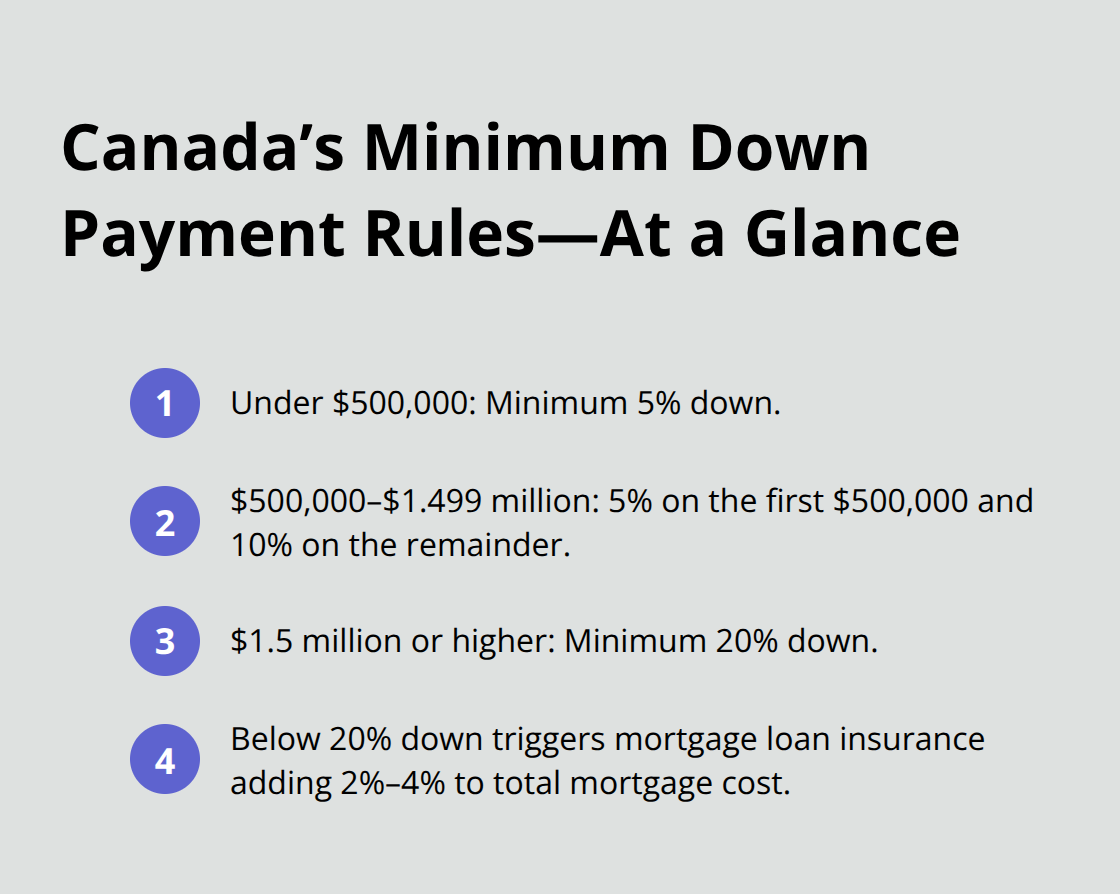

Your down payment is your most powerful weapon when lenders evaluate your application. A 5% down payment on a $500,000 home means $25,000, but a 20% down payment means $100,000-and that difference transforms how lenders see your risk profile. Canada’s minimum down payment rules are straightforward: properties under $500,000 require 5% down, properties between $500,000 and $1.499 million require 5% on the first $500,000 and 10% on the remainder, and properties $1.5 million or higher require 20%. Anything below 20% triggers mortgage loan insurance, which adds 2% to 4% to your total mortgage cost depending on your down payment size. This means a $25,000 down payment on that $500,000 home could add $10,000 to $20,000 in insurance premiums spread across your mortgage term. The math is brutal, which is why lenders view larger down payments as proof you’re serious and capable of saving.

Calculate Your Target Down Payment Now

Start calculating backward from your target home price right now. If you want to buy a $600,000 property in Alberta, you need at least $30,000 down to hit the 5% minimum, but $120,000 down puts you at 20% and eliminates insurance entirely. The difference in your monthly payment could be $200 to $400, which compounds over 25 years into tens of thousands of dollars.

Many first-time buyers focus only on the down payment percentage, but lenders care more about the absolute dollar amount because it shows you’ve disciplined yourself to save consistently.

Employment Stability Matters More Than Income Level

Lenders want to see two things in your employment history: consistency and longevity. A $100,000 annual salary with five years at the same employer beats a $150,000 salary with two job changes in three years. Most lenders prefer full-time employment for at least two years with your current employer, though some will accept one year if you’re in the same industry. Self-employed applicants face stricter scrutiny and typically need two to three years of tax returns showing consistent or growing income to qualify.

If you’ve changed jobs recently, wait at least 90 days before applying for a mortgage-lenders need to see paystubs and employment letters confirming you’re still employed. Income fluctuations are red flags. Bonus income, commissions, or overtime can be included in your application, but lenders average these over two years, so a year with no bonus hurts your numbers significantly. Keep your employment situation stable during the entire pre-approval and closing process. One job change during underwriting can trigger a full reassessment of your file, adding weeks to your timeline.

Organize Your Financial Records Now

Your bank statements are evidence that you can actually afford the mortgage you’re applying for. Lenders want to see three to six months of statements showing your savings, regular deposits, and spending patterns. They’re looking for red flags like large unexplained deposits, frequent overdrafts, or sudden account closures. Start collecting statements from every account you own right now-checking, savings, investment accounts, RRSPs.

If you received a gift for your down payment from family members, expect lenders to ask for a statutory declaration confirming it’s a gift and not a loan you’ll need to repay. Your tax returns for the past two years are mandatory, and if you’re self-employed, you’ll need three years. Pay stubs from the past 30 days prove your current income level. Keep everything organized in one folder (digital and physical copies) because your mortgage broker or lender will request specific documents multiple times throughout the process. Missing a single document can delay your approval by weeks.

If you have irregular income, gaps in employment, or unusual financial situations, gather additional documentation now that explains them clearly. A letter from your employer confirming your position, start date, and salary takes five minutes to request but can save your application if questions arise later. With your down payment strategy locked in and your financial records organized, you’re ready to move into the final phase: preparing your mortgage application materials and securing pre-approval from a lender who understands your situation.

Securing Pre-Approval and Professional Guidance

Gather Your Documentation First

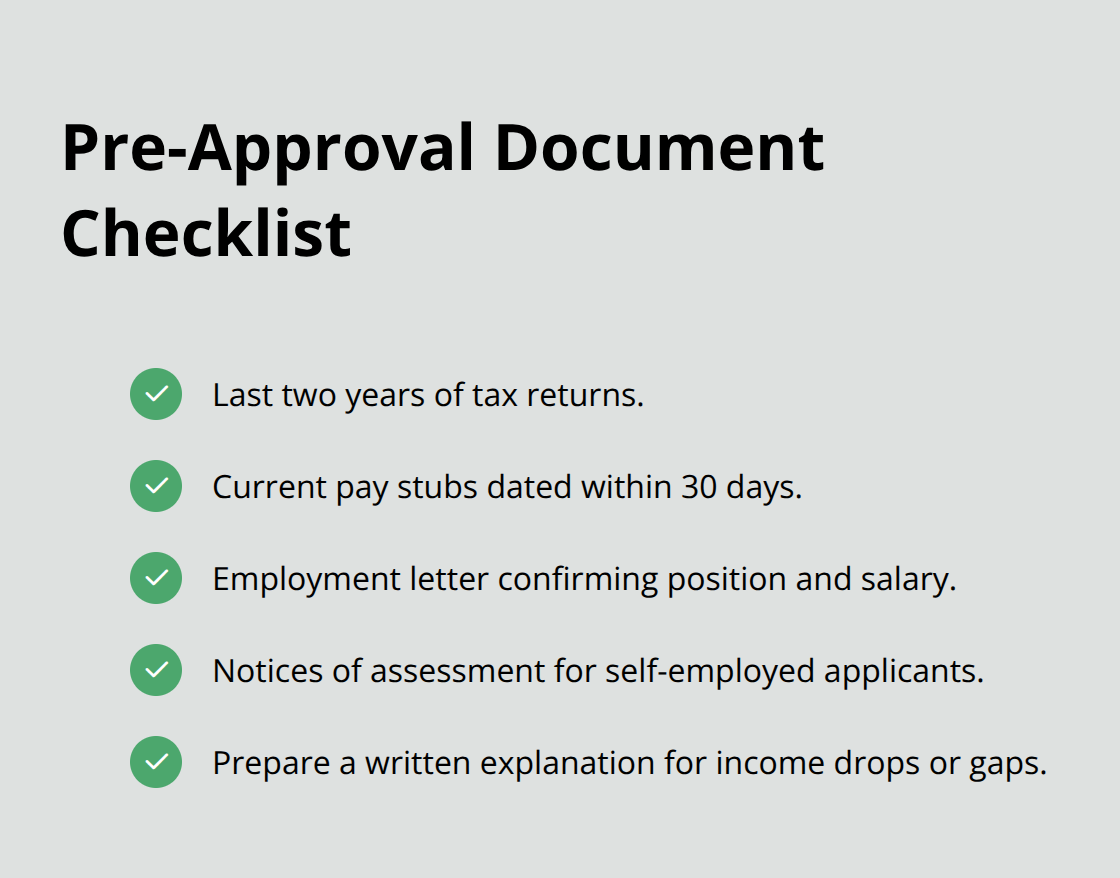

Your tax returns and pay stubs are non-negotiable documents that lenders require before they commit to lending you money. Most Canadian lenders want your last two years of tax returns, current pay stubs (within 30 days), and employment letters confirming your position and salary.

Self-employed applicants must provide notices of assessment from the Canada Revenue Agency. Lenders scrutinize these documents for consistency, so if your income dropped significantly in any year or you have unexplained gaps in employment, prepare a written explanation now rather than scrambling during underwriting.

Understand What Pre-Approval Actually Means

A pre-approval is a lender’s written commitment to lend you a specific amount at a specific rate for a specific term, typically valid for 90 to 120 days. This document transforms your mortgage hunt from speculation into strategy because you know exactly what you can afford and lenders take you seriously when you make offers. Getting pre-approved before house hunting also prevents you from falling in love with properties outside your actual budget, which is surprisingly common among first-time buyers who overestimate their borrowing power. Most lenders can deliver a pre-approval within 24 to 48 hours once you submit documents, so speed matters when you’re ready to make an offer.

Choose Between Fixed and Variable Rates

Your mortgage broker should explain whether you qualify for fixed or variable rates and help you model monthly payment scenarios using Ratehub.ca calculators so you understand the real cost difference between options before committing. Lock in your pre-approval rate for the full 120-day period if rates are falling, but if rates appear to be rising, a 90-day lock gives you flexibility to renegotiate if conditions change. Fixed rates protect you from payment increases over your term, while variable rates fluctuate with the prime lending rate. The choice depends on your risk tolerance and your predictions about future rate movements.

Work with a Mortgage Broker, Not Just Banks

Mortgage brokers access multiple lenders and negotiate on your behalf at no cost to you. Banks compete for your business through brokers, which means better rates and terms than walking in alone. A mortgage broker also identifies which lenders accept your specific situation, whether that’s recent employment changes, self-employment income, or lower credit scores. When comparing rates across brokers or banks, ask for the same amortization period and down payment percentage so numbers are actually comparable. Ratehub.ca provides rate comparisons across lenders, but a broker’s job is to find the lender most likely to approve you at the best price.

Final Thoughts

Getting approved for your first mortgage in Canada requires deliberate preparation, not luck. The steps we’ve outlined-cleaning up your credit, building a substantial down payment, documenting your financial stability, and securing pre-approval from the right lender-separate applicants who get approved from those who face rejection or unfavorable terms. Lenders evaluate hundreds of applications monthly and look for borrowers who demonstrate financial discipline through organized records, stable employment, and proof they can save consistently.

When you arrive at pre-approval with your credit score above 660, your debt paid down, your down payment saved, and your documentation complete, you stand out as the borrower lenders want to work with. Start taking action immediately by pulling your credit reports from Equifax and TransUnion this week and disputing any errors you find. Calculate your target down payment based on your desired home price, begin tracking your savings progress, and gather your tax returns, pay stubs, and bank statements so they’re ready when you contact a mortgage broker.

The timeline matters because building Canadian credit, saving your down payment, and organizing your finances takes months, not days. If you’re planning to buy within the next year, start now (if you’re buying within six months, accelerate these steps immediately). At Financial Canadian, our web design service helps you establish a strong digital footprint that reflects your commitment to excellence as you prepare for your first mortgage in Canada.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment