Finding the right financing when you need it fast matters. Online loans in Canada have become a practical way to access funds without the lengthy approval processes traditional banks demand.

At Financial Canadian, we’ve created this guide to help you navigate your online loans Canada options and find flexible financing that fits your situation. Whether you’re comparing interest rates, understanding eligibility requirements, or preparing your application, we’ll walk you through each step.

What Online Loan Types Work Best for Your Situation

Personal Loans: Predictable Payments for Planned Expenses

Personal loans from online lenders typically range from $500 to $40,000, with interest rates starting as low as 9.99% and terms stretching from 12 to 84 months. These loans work well for consolidating debt, covering home repairs, or funding planned expenses because you know exactly what you’ll pay each month. The approval process is straightforward: you complete an online form, receive an instant decision without a hard credit pull affecting your score, and funds arrive via Interac e-Transfer in as little as 15 minutes or through direct deposit. This speed matters when you’re comparing options against traditional banks that demand weeks of processing.

Lines of Credit: Flexibility for Ongoing Needs

Lines of credit operate differently and offer more flexibility than fixed-term personal loans. You access up to $10,000 whenever you need it without reapplying, paying interest only on what you actually borrow. Once you repay, your available credit refreshes automatically, making a line of credit useful for ongoing expenses or unpredictable costs. The tradeoff is higher interest rates-typically 34.99% APR-but you gain control over when and how much you use.

Short-Term and Secured Loans: Speed Versus Cost

Short-term financing and payday loans represent the fastest but most expensive route. About 2 million Canadians use payday loans annually, with roughly 1,400 locations across the country offering loans from $100 to $1,500 repaid within 14 to 30 days. These require no credit check, which appeals to people with poor credit, but interest rates are punishing. Installment loans offer a smarter middle ground: you borrow $500 to $5,000 and repay over 12 to 24 months with interest rates substantially lower than payday loans. Title loans use your vehicle as collateral, letting you access up to 50% of its value with repayment terms from 3 months to 3 years, though provincial rules vary significantly.

Secured loans from online lenders require in-branch application and vehicle collateral but can approve you for up to $25,000 with APRs ranging from 24.99% to 34.99% depending on verification. When you face an emergency, the temptation to grab the fastest option is strong, but the math works against payday loans. A $1,500 payday loan costs far more over time than an installment loan or personal loan with structured repayment.

Making Your Choice: Timeline and Repayment Ability

The key decision comes down to your timeline and repayment ability. If you need funds immediately and can repay within weeks, payday loans exist as an option, but if you have any flexibility, personal loans or lines of credit deliver better long-term value. Understanding which loan type matches your situation sets the stage for the next critical step: comparing the actual lenders and providers available to you.

Comparing Lenders: What Actually Matters

Interest Rates: What You See Versus What You Get

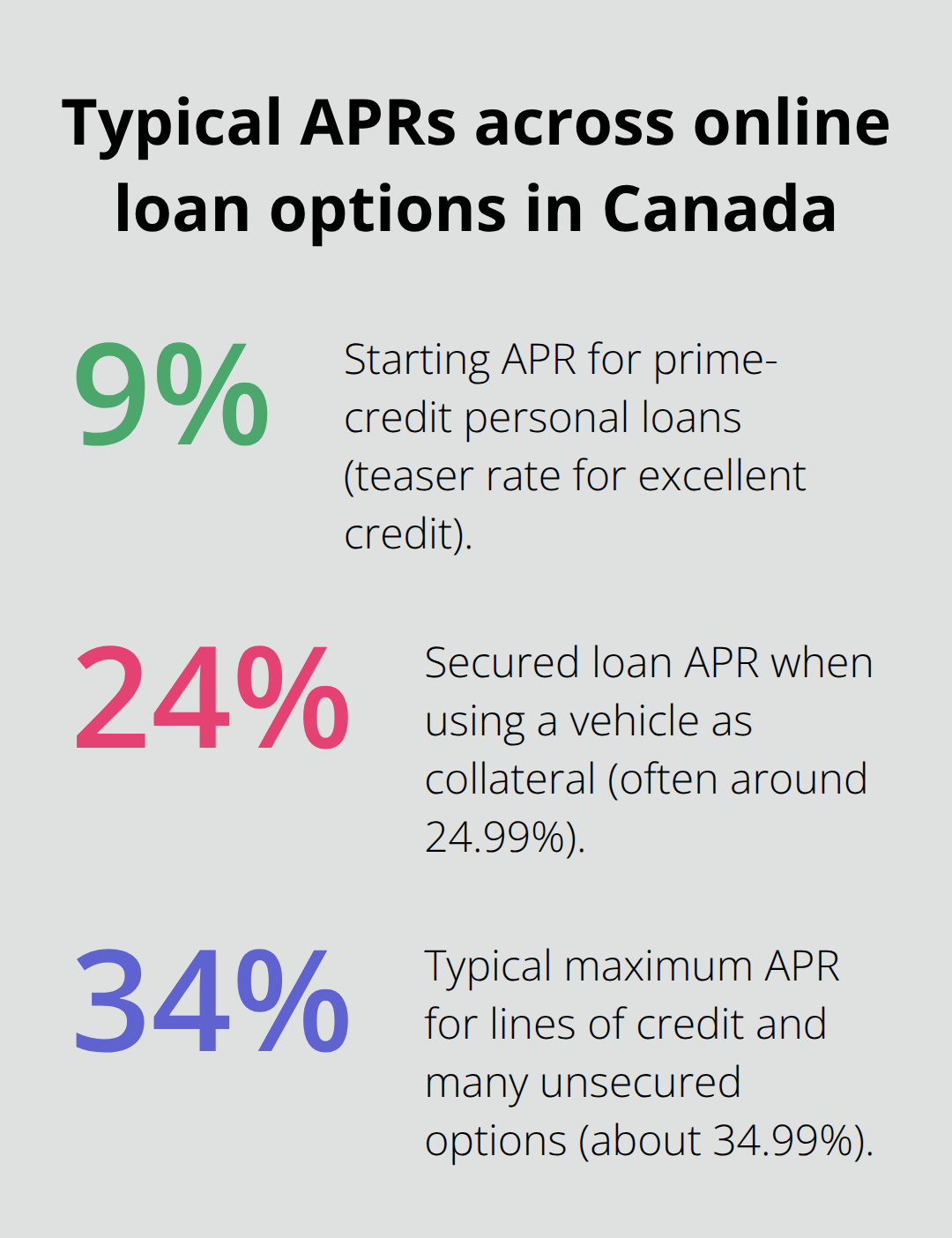

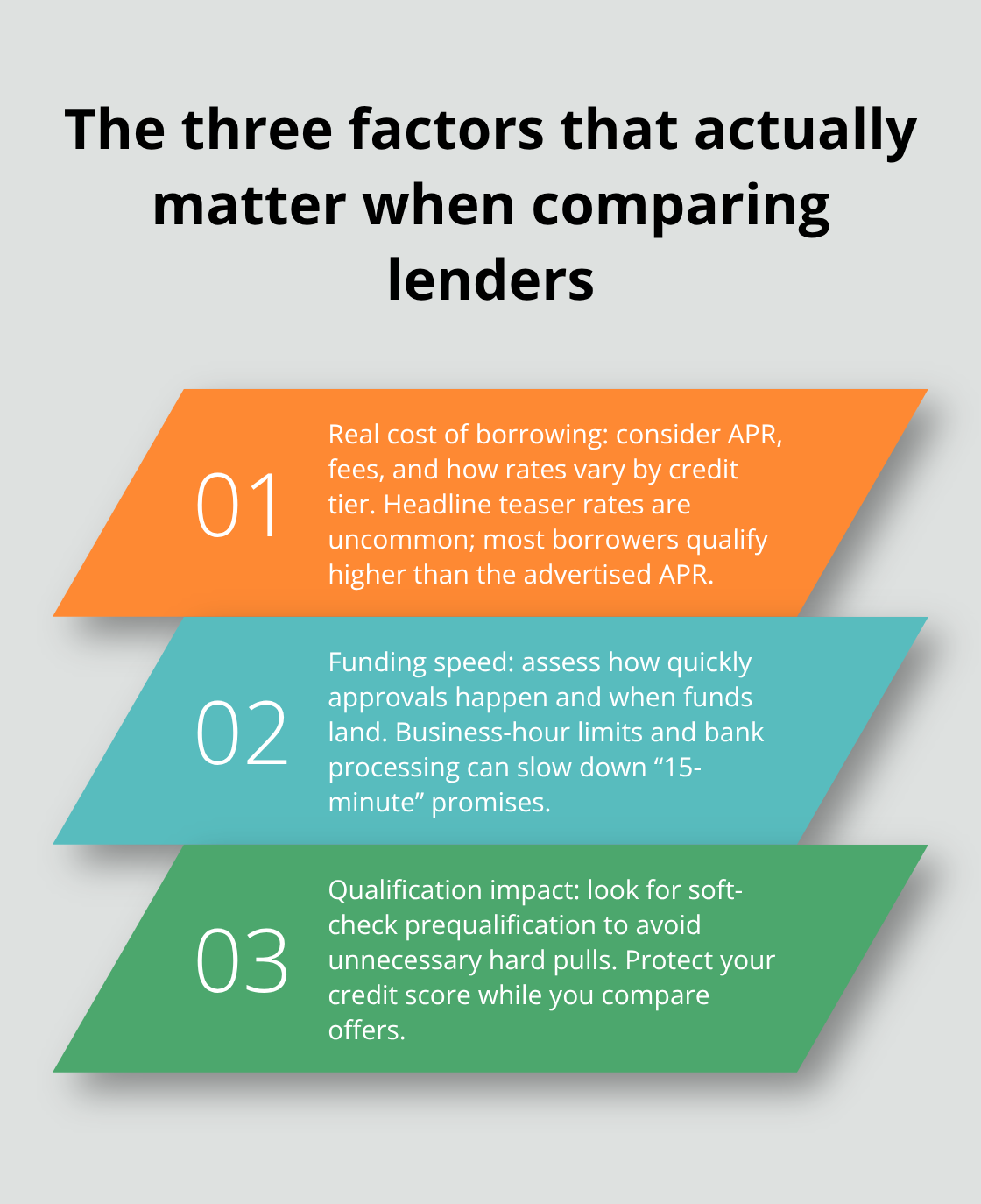

Comparing online loan providers means looking past marketing claims and focusing on three concrete factors that directly impact your wallet: the real cost of borrowing, how fast you actually receive funds, and whether you’ll qualify without unnecessary credit damage. Most borrowers fixate on interest rates alone, but that’s only one piece of the equation. A lender advertising 9.99% APR on personal loans might sound attractive until you discover that rate applies only to applicants with excellent credit, while most people qualify at 19.99% or higher.

The APR you actually get depends on borrower-specific qualification factors including your credit score and loan-to-value ratio.

Start by checking what rate range each lender publishes for your credit profile, not their headline rate. Some lenders require in-branch applications and vehicle collateral, which adds friction but can lower your rate to 24.99% APR compared to 34.99% for unsecured options. Lines of credit typically max out at 34.99% APR across most Canadian lenders, so if you’re comparing that product type, you’re essentially comparing approval speed and customer service rather than rate differences.

Funding Speed and Approval Timeline

Funding speed matters more than most people realize, especially when you’re comparing online options. Many lenders promise funds in 15 minutes via Interac e-Transfer, but that’s only possible if you apply during business hours and your bank processes the transfer immediately. Direct deposit funding takes longer but works reliably across all banks. The real differentiator is approval timeline: extensive documents and lengthy approval reviews can result in wait times spanning weeks or months. If you’re dealing with an emergency, that extended timeline could mean missing a payment or losing an opportunity.

Eligibility Requirements and Credit Impact

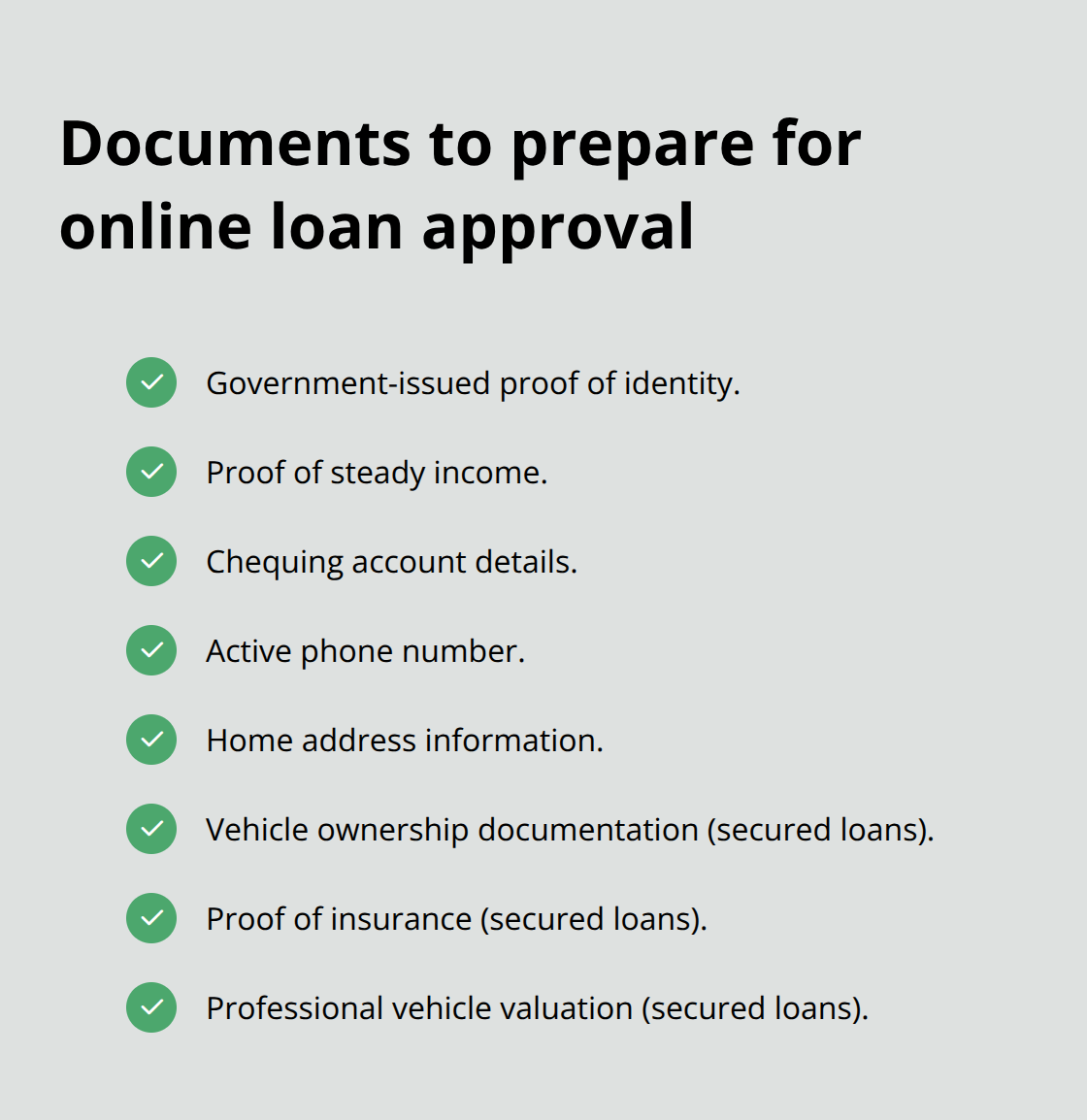

Eligibility requirements vary significantly across lenders. Most online lenders require proof of identity, steady income, a chequing account, a phone number, and a home address for unsecured loans. Secured loans demand additional verification including in-branch application, vehicle ownership documentation, proof of insurance, and a professional vehicle valuation. The credit score impact differs substantially: prequalification uses a soft credit check that doesn’t touch your score, but accepting an offer triggers a hard inquiry that temporarily lowers your score by 5 to 10 points.

If you’re shopping multiple lenders within two weeks, those inquiries stack up and compound the damage. Some lenders are more selective about income verification, requiring recent pay stubs or tax returns, while others accept employment letters. Lines of credit at 34.99% APR refresh your available credit automatically as you repay, but that flexibility costs you in interest rates.

Choosing Between Loan Types for Your Situation

Short-term installment loans from $500 to $5,000 over 12 to 24 months generally carry lower rates than payday loans but higher rates than personal loans, making them the pragmatic middle ground for people with damaged credit who need faster approval than traditional banks offer. The decision ultimately hinges on your actual financial situation: if you have decent credit and time to wait, personal loans deliver the lowest cost; if your credit is poor and you need speed, installment loans or lines of credit make more sense than payday options despite higher rates. Once you’ve narrowed down which lender matches your needs, the next step involves preparing your application materials and understanding exactly what lenders verify before they approve you.

Getting Approved for an Online Loan

Documents You Need to Prepare

Preparing your application correctly makes the difference between approval and rejection. Most online lenders require proof of identity, steady income, a chequing account, a phone number, and a home address for unsecured loans like personal loans and lines of credit. For secured loans using vehicle collateral, you’ll also need vehicle ownership documentation, proof of insurance, and a professional vehicle valuation.

The income requirement varies by lender-some accept recent pay stubs or tax returns while others take employment letters, but lenders may verify your income through employer contact or tax records rather than relying solely on your documentation. If you’re self-employed, prepare your last two years of tax returns and recent business financial statements because lenders scrutinize self-employment income more heavily than W-2 employment.

Have your chequing account information ready since lenders use direct deposit or Interac e-Transfer to fund approved loans, and they verify the account belongs to you before releasing funds. Gather these materials before you apply because delays in submitting documents can push your approval timeline from 48 hours to several days or longer.

What Lenders Verify During Approval

The approval process moves faster than traditional banks but requires you to understand what lenders verify at each stage. After you submit your online form, lenders verify your identity using government-issued ID, confirm your income through employer contact or tax records, and validate your chequing account through micro-deposits or instant verification services.

For secured loans, they’ll order a professional vehicle valuation and conduct a lien search to confirm you own the vehicle free and clear or have permission from your lienholder to use it as collateral. Lien searches and security fees vary by province-Ontario and Quebec charge different amounts than British Columbia or Saskatchewan, so ask about these costs upfront.

Most lenders provide approval decisions within 48 hours after documents arrive, but funding speed depends on your bank’s processing time. Interac e-Transfer works fastest when you apply during business hours and your bank processes transfers immediately, potentially delivering funds in 15 minutes, while direct deposit typically takes one business day.

Credit Impact and Application Strategy

One critical detail most borrowers overlook: soft credit checks during prequalification don’t impact your score, but accepting a loan offer triggers a hard inquiry that temporarily lowers your score by 5 to 10 points. If you’re comparing multiple lenders, space your applications across at least two weeks to avoid stacking hard inquiries, which compounds credit damage and signals financial desperation to lenders.

To improve your approval odds, ensure your income documentation is current and matches the income you report on your application-lenders flag discrepancies and request clarification, which delays approval. If you have poor credit but stable income, highlight your employment history and avoid applying for multiple loans simultaneously.

Maximizing Your Rate and Terms

Secured loans offer better rates because collateral reduces lender risk, so if you own a vehicle outright, using it as collateral can lower your APR from 34.99% to 24.99%, saving hundreds in interest over your loan term. This strategy works particularly well when you need larger amounts or face tight approval timelines with unsecured lenders.

Final Thoughts

Choosing the right online loans Canada option comes down to matching your financial situation with the loan type that minimizes cost while meeting your timeline. Personal loans work best when you have decent credit and can wait a few days for approval, since rates starting at 9.99% APR beat lines of credit at 34.99% by a significant margin. Lines of credit make sense if you face unpredictable expenses and value flexibility over rate savings. Payday loans and short-term financing should be your last resort because the interest compounds quickly, turning a temporary fix into a debt spiral that costs far more than installment loans or secured options.

The most common mistake borrowers make involves applying to multiple lenders simultaneously without understanding how hard credit inquiries stack up and damage your score. Space your applications across two weeks minimum, and use soft prequalification checks to compare rates without triggering hard pulls. Another frequent error involves ignoring provincial differences in fees and terms-lien searches and security fees for secured loans vary between Ontario, Quebec, British Columbia, and Saskatchewan, so ask about these costs before committing. If you own a vehicle outright, secured loans can cut your rate from 34.99% to 24.99%, saving hundreds in interest.

Your next step is straightforward: gather your identity documents, income proof, and chequing account information, then apply to lenders whose online loans Canada options match your needs. Check approval timelines and funding methods to confirm they align with your situation. We at Financial Canadian offer resources to support your financial journey as you move toward the flexible financing that works for your circumstances.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment