Your credit score shapes whether you get approved for mortgages, car loans, and credit cards-and what interest rates you’ll pay. A low score can cost you thousands in extra interest over your lifetime.

At Financial Canadian, we’ve created this guide to help you build credit in Canada with concrete, actionable steps. You’ll learn exactly what damages your score, how to fix it, and which free tools track your progress.

How Your Credit Score Actually Works in Canada

Credit scores in Canada range from 300 to 900, and every point matters when lenders decide whether to approve you. TransUnion and Equifax, Canada’s two major credit bureaus, compile your credit report and calculate your score based on five key factors. Payment history carries the most weight at roughly 35 percent of your score, which means a single missed payment can drop your score by 50 to 100 points depending on how recent it is.

Credit utilization accounts for about 30 percent of your score, and this is where most people make costly mistakes. If you have a $5,000 credit limit and carry a $3,500 balance, you’re using 70 percent of your available credit, which signals to lenders that you’re financially stretched. Lenders prefer to see utilization below 30%, so a $1,500 balance on that same card would work in your favor.

The length of your credit history makes up 15 percent of your score, credit mix adds 10 percent, and new inquiries account for the final 10 percent. This breakdown shows you exactly where to focus your effort for the fastest improvement.

What Damages Your Score Most

Missed payments cause the most immediate damage because payment history dominates your score calculation. A payment 30 days late will hurt less than one 60 days late, but both stay on your report for six years and continue to damage your score long after you catch up. Multiple hard inquiries within a short period signal that you’re desperately seeking credit, and each application can lower your score by a few points according to Aman Anand from TransUnion.

Collections accounts and bankruptcies are score killers that can reduce your score by 100 points or more, but they also fade over time as they age on your report. Closing old credit cards seems smart on the surface but actually hurts your score because it reduces your total available credit and shortens your average account age.

How Balances and Utilization Compound the Problem

Carrying high balances across all your cards damages your score more than concentrating debt on one card, even if the total owed is identical, because utilization is calculated across your entire portfolio. High utilization combined with missed payments creates a devastating combination that can drop your score below 600 and lock you out of decent interest rates for years.

Understanding these damage patterns helps you prioritize which actions will move your score fastest. The next section covers the specific steps that actually work to rebuild your credit.

How to Fix Your Credit Fast

Payment history accounts for 35 percent of your score, making it the fastest lever to pull for improvement. Set up automatic payments on every bill you owe, not just credit cards. According to Aman Anand from TransUnion, autopay removes the risk of forgetting a payment and demonstrates reliability to lenders. If you’ve already missed a payment, contact your lender immediately and ask about a goodwill adjustment or a plan to catch up. Lenders sometimes remove late payments from your report if you explain the circumstances and show you’re now paying on time. Once you establish three to six months of consecutive on-time payments, you’ll see meaningful score improvements, typically within 30 to 45 days of each positive report to the credit bureaus.

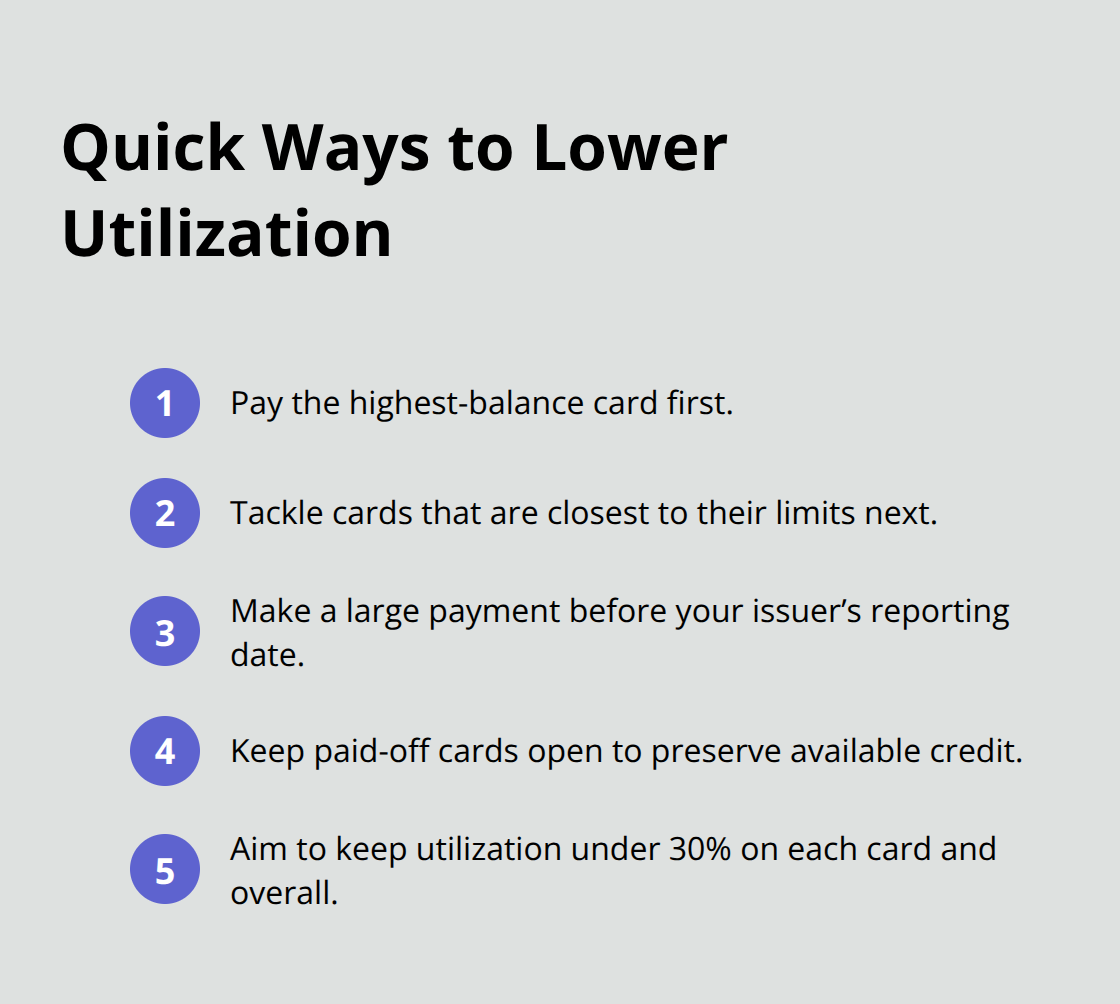

Slash Your Utilization Ratio Right Now

Reducing credit card balances delivers faster results than waiting for payment history to improve because utilization changes are reported monthly. If you carry $8,000 across multiple cards with a combined $15,000 limit, you’re at 53 percent utilization and your score suffers.

Dropping that to 30 percent utilization aligns with lender preferences and can boost your score by 20 to 50 points within weeks. The most practical approach is to pay down the card with the highest balance first, then focus on cards approaching their limit. Timing matters too: if your card issuer reports balances to the credit bureaus on the 15th of each month, make a large payment before that date so the lower balance gets reported. Don’t close paid-off cards because that reduces your total available credit and makes remaining balances appear higher by comparison.

Dispute Errors Before They Cost You Points

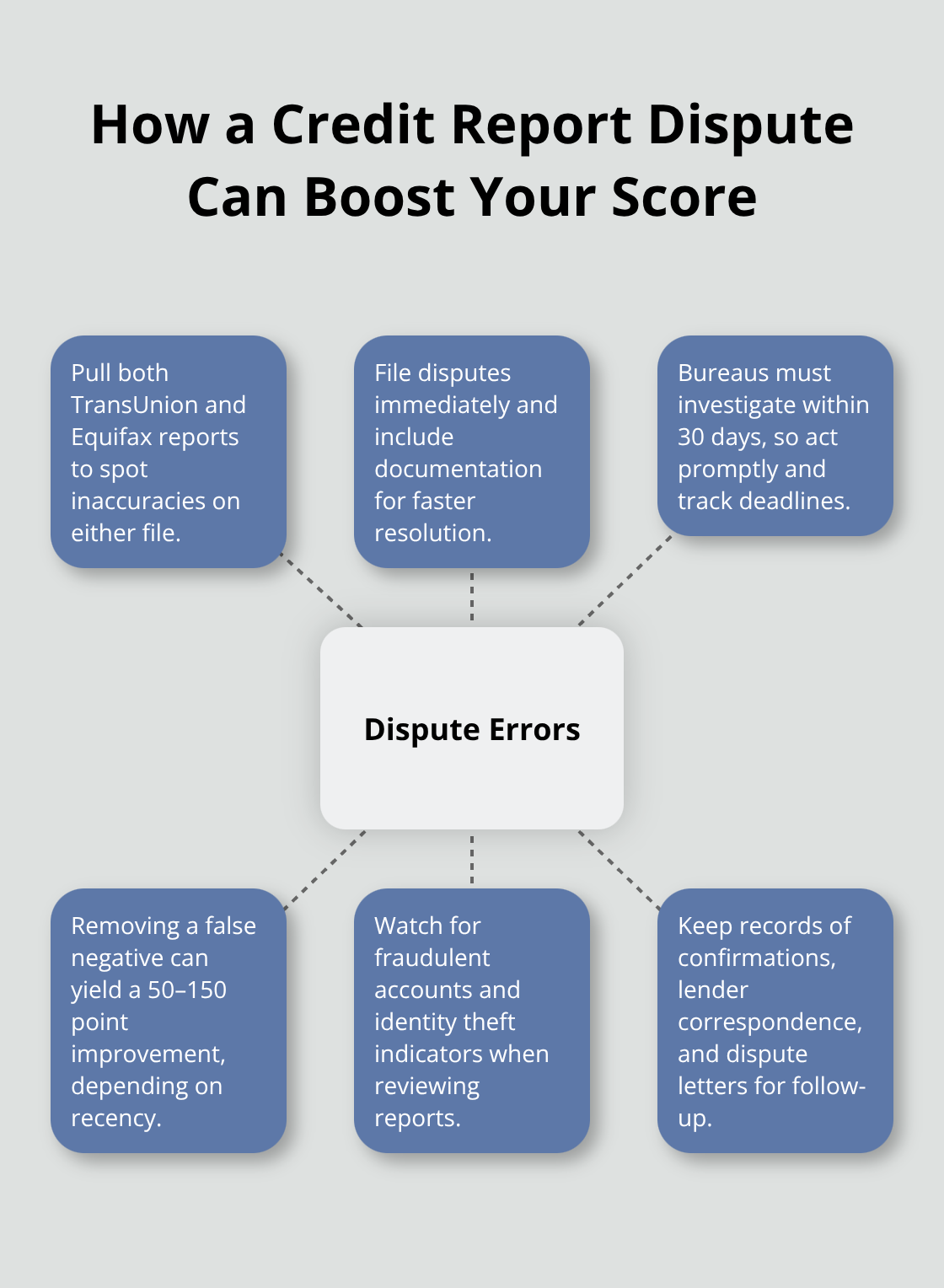

Pull your credit reports from both TransUnion and Equifax because lenders sometimes report incorrect information, missed payments that were actually made, or accounts that don’t belong to you. You can access these reports free annually at each bureau’s website. Mistakes happen frequently enough that disputing inaccuracies is worth your time. If you find a late payment that was actually paid on time, or a collection account you don’t recognize, file a dispute immediately. The bureaus must investigate within 30 days, and removing a false negative item can improve your score by 50 to 150 points depending on how recent the error is. Keep records of everything: payment confirmations, correspondence with lenders, and dispute letters.

One person discovered a fraudulent account opened in their name was destroying their score; removing it jumped their score from 580 to 640 in one dispute cycle.

Space Out New Credit Applications Strategically

Each hard inquiry from a credit application can lower your score by a few points, so resist the urge to apply for multiple cards or loans within a short timeframe. If you need new credit, apply for everything within a 14-day window because the major bureaus treat multiple inquiries as a single event when they fall within that period. This matters most when you shop for a mortgage or auto loan where you need multiple lender quotes. After applying, wait at least three to six months before your next application so inquiries age off your report and your score recovers. Hard inquiries stay on your report for three years but stop affecting your score after about six months, so timing your applications around major financial decisions keeps you in control. With payment history fixed, utilization lowered, errors removed, and applications spaced strategically, you’re ready to monitor your progress with the right tools.

Monitor Your Credit Progress With Free Tools

Check Your Score Monthly Without Paying for It

Equifax Core Credit gives you real-time access to your score and report without subscription fees, letting you check whenever you want instead of waiting for your annual free pull. You can obtain your credit report for free once per year from both Equifax and TransUnion through their official websites, but Equifax Core Credit removes the waiting game entirely. The tool shows exactly which accounts are being reported, payment status on each one, and how your utilization ratio trends month to month. After you implement the fixes from the previous section, you need to monitor whether your score actually moves. Most score changes appear within 30 to 45 days after lenders report information to the bureaus, so checking monthly gives you enough time to see real movement without obsessing over daily fluctuations. Set a calendar reminder for the same date each month to track progress consistently.

Use Rapid Rescoring for Time-Sensitive Situations

If you’re applying for a mortgage or major loan soon, Equifax offers rapid rescoring through participating lenders. This process works by having lenders report updated information immediately rather than waiting for the next monthly cycle. Rapid rescoring matters when you’ve just paid down balances or corrected errors and need lenders to see your improved profile right away. The speed advantage can make the difference between approval and rejection when timing is tight.

Pull Both Credit Reports and Hunt for Errors

Access your full credit reports from both bureaus at least once yearly because errors appear more frequently than most people realize, and catching them early prevents months of unnecessary score damage. TransUnion and Equifax maintain separate files, so a fraudulent account might appear on one report but not the other. When you pull your reports, look specifically for accounts you don’t recognize, payment statuses that don’t match your records, and collection items that shouldn’t be there. One person discovered a fraudulent account opened in their name was destroying their score; once removed, their score jumped from 580 to 640 in a single dispute cycle.

Set Up Alerts to Catch Identity Theft Early

Equifax Complete and similar monitoring products send alerts when new inquiries hit your file or accounts are opened in your name, which catches identity theft before it spirals into a major problem. The alerts arrive via email, giving you immediate notice to investigate suspicious activity. After you dispute errors or pay down balances, check your reports again in 30 to 45 days to confirm the changes were actually reported. Tracking these changes keeps you accountable and shows exactly which actions moved your score most.

Final Thoughts

Payment history remains your biggest lever for improving your credit score-set up autopay today and watch your score climb within weeks. Utilization drops come next; paying down balances before your card issuer reports to the bureaus can boost your score by 20 to 50 points monthly. Dispute any errors you find because removing false negatives often delivers the biggest single improvement to your overall score.

Most people see meaningful movement within 30 to 45 days of implementing these steps, though building a truly strong credit score in Canada takes six to twelve months of consistent action. Hard inquiries fade after six months, missed payments lose impact after two years, and older negative items matter less as time passes. Your score will fluctuate month to month as lenders report new information, but the trend should move upward if you stick to the fundamentals (keep utilization below 30 percent, never miss a payment, and space out new credit applications strategically).

Once your score improves, the real work starts: maintaining it through consistent habits that become automatic over time. A strong credit score opens doors to better mortgage rates, lower insurance premiums, and approval for credit products you actually want. Visit Financial Canadian to explore resources designed to support your financial journey as you build credit Canada.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment