Your credit score shapes your financial life in Canada. It determines whether you qualify for loans, what interest rates you’ll pay, and how much you can borrow.

At Financial Canadian, we’ve created this guide to help you understand Canada credit score basics and take control of your financial future. We’ll show you exactly how scores work, what damages them, and how to improve yours fast.

How Your Credit Score Gets Calculated in Canada

The Two Bureaus and Scoring Models That Matter

In Canada, your credit score is a three-digit number that lenders use to assess how likely you are to repay borrowed money. Equifax Canada and TransUnion Canada calculate these scores based on your financial behavior. Your credit report tracks every loan, credit card, and payment you make, and the scoring models these bureaus use (including VantageScore) weight different factors to produce your final number.

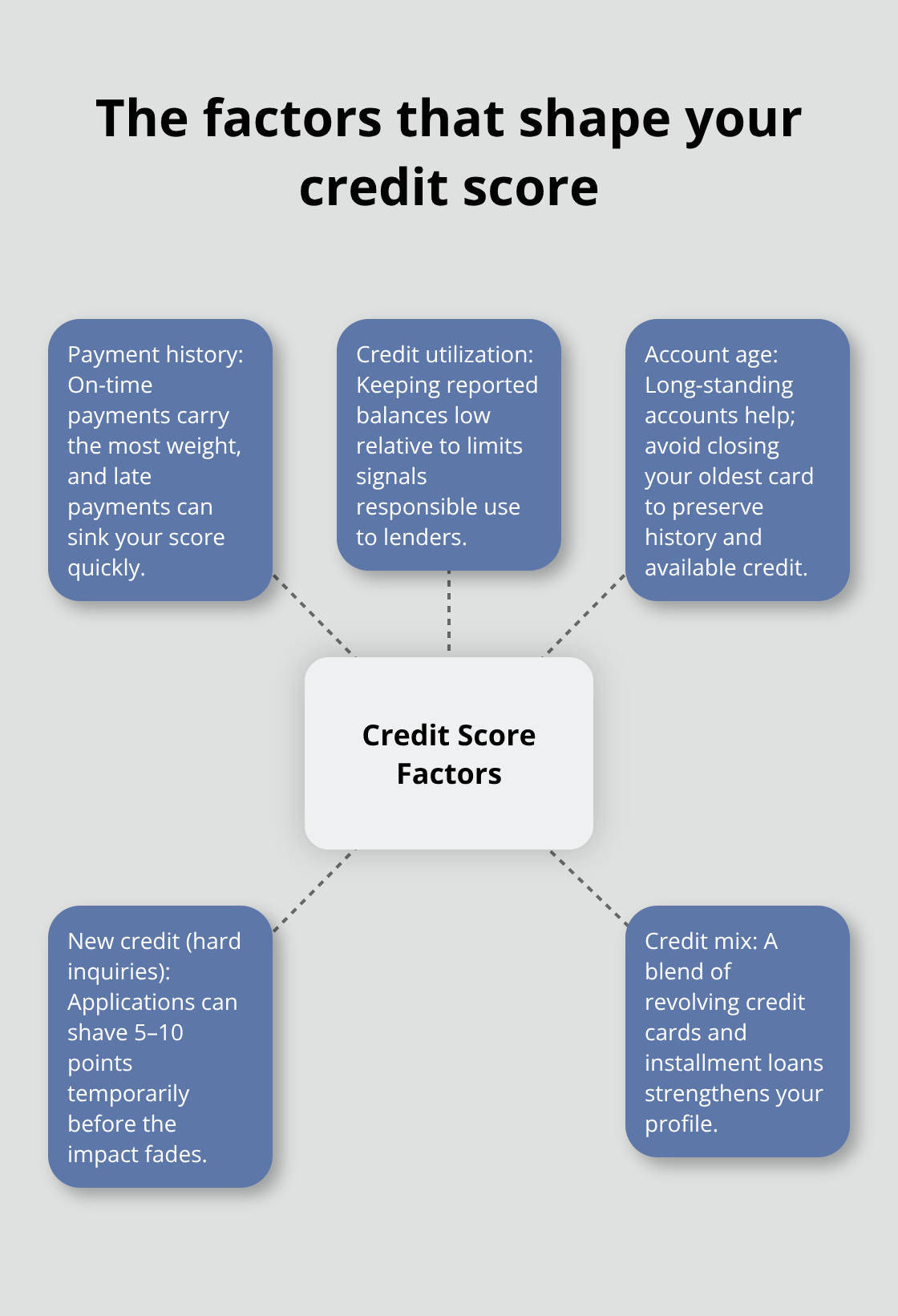

Payment History: The Factor That Dominates Your Score

Payment history is the single most influential factor in your credit score, accounting for the largest portion of your overall rating. A single missed payment can damage your score more than other negative events. To protect this critical component, set up autopay on your accounts so you never miss a due date. This one habit alone will have the biggest impact on your score improvement.

Credit Utilization, Account Age, and Credit Mix

Credit utilization-the percentage of your available credit that you currently use-is the second most important factor. Try to keep this ratio at 30% or below, though lower is always better. The length of your credit history also matters significantly, which is why closing old credit accounts after you pay them off actually hurts your score rather than helps it. New credit inquiries, called hard inquiries, temporarily lower your score when you apply for loans or credit cards. Having a mix of different types of credit, such as both credit cards and installment loans, strengthens your profile.

Understanding Your Score Range

Canada credit scores range from 300 to 900. A score of 800 to 900 is considered excellent and signals the best loan terms and widest credit options available to you. Scores between 720 and 799 are very good, meaning you’ll typically have many credit choices and favorable terms from lenders.

A score of 650 to 719 is good to lenders, usually accessible for credit, though the lowest rates may not be available. Scores between 600 and 649 are fair, where your history of debt repayment becomes especially important to demonstrate responsibility. Anything below 600 is poor, and you’ll likely face higher rates and more difficulty obtaining new credit.

Most lenders set minimum score thresholds around 680 for approvals, while others target 700 or higher for the best terms. Reaching 700 is widely viewed as a strong baseline for favorable lending outcomes. The difference between your scores at Equifax and TransUnion can be substantial-some users report gaps of around 100 points-so checking both bureaus matters.

How Your Score Translates Into Real Financial Costs

Your credit score directly affects your borrowing costs and the types of financial products you can access. A higher score qualifies you for lower interest rates on mortgages, auto loans, and personal loans, saving you thousands of dollars over the life of the loan. The difference between a 650 score and a 750 score on a mortgage could mean tens of thousands in additional interest paid over 25 years. Your score also determines your credit limits, which affects your ability to make major purchases or handle emergencies. Lenders also consider other factors like income, employment, and total debt, but your score is the first filter they use.

Most lenders report to the credit bureaus monthly, so your scores typically update on a monthly cycle, though timing varies by lender. This means improvements in your score often take 30 to 45 days for initial changes to show up. Understanding these timelines helps you set realistic expectations as you work to raise your score. Now that you know how scores work and what they mean, the next step is learning exactly where to check your score and what specific actions will raise it fastest.

What Damages Your Credit Score Most

Payment History: Your Most Powerful Tool

Payment history is non-negotiable. Late payments stay on your credit report for seven years, and this is why setting up autopay protects your score more effectively than any other action you can take. If you have a history of missed payments, bring all accounts current immediately to start reversing the damage. One missed payment hurts far more than any other factor, so this single habit matters more than anything else you can do.

Credit Utilization: The Second Most Important Factor

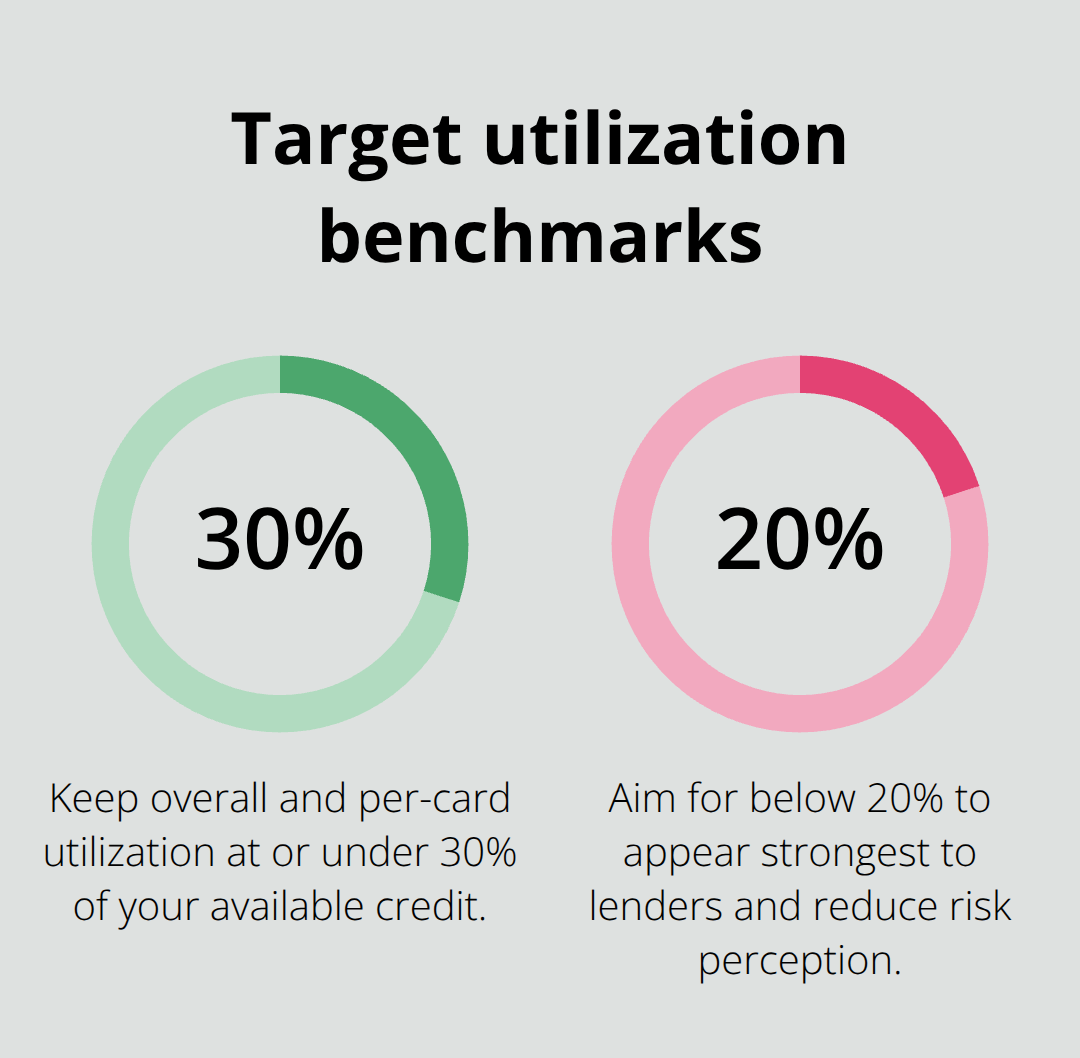

Your credit utilization ratio determines how lenders perceive your debt management. Try to keep your balance below 30% of your available credit, though going below 20% positions you more favorably with lenders. If you have a $5,000 credit limit, staying below $1,500 in balance shows disciplined borrowing.

The practical way to lower utilization fast is to pay down balances before your statement closes, not just at the end of the month. Some people pay multiple times monthly specifically to keep reported utilization low. Requesting higher credit limits also reduces your ratio instantly without requiring extra payments, though this triggers a hard inquiry that temporarily lowers your score by a few points.

Account Age and Credit Mix: Building Long-Term Strength

Your credit history’s age works against you if you close old accounts. Keep your oldest credit card open and active, even with small purchases, to preserve account age and available credit simultaneously. Closing that card after paying it off actually hurts your score because available credit drops, pushing your utilization ratio higher. Hard inquiries from new credit applications lower your score temporarily, typically by five to ten points, and the impact fades within three to six months. However, multiple inquiries within 14 days for the same type of credit usually count as one inquiry, so spacing out different types of applications matters. If you have limited credit history, open a secured credit card or credit-builder loan to add diversity to your profile and build age over time.

The Reality of Score Improvement

The long-term path to a strong score requires consistent on-time payments, low utilization, and patience. No quick fix lasts, and any product claiming rapid score jumps without behavior change sells false promises. Your actions today compound over months and years, which is why understanding what damages your score helps you avoid costly mistakes. With these factors in mind, the next step is learning exactly where to check your score and what specific actions will raise it fastest.

Check Your Score and Fix Errors Before They Cost You

Access Your Score From Banks and Credit Bureaus

Your first move is pulling your actual score from the two bureaus that matter in Canada. Major banks including BMO, RBC, and Scotiabank offer free online credit score checks through their online banking platforms, so if you already bank with one of them, log in and pull your score today. Equifax Canada and TransUnion Canada also provide free annual credit reports through their websites, though accessing your score directly through these bureaus sometimes requires a fee unless you’ve been denied credit recently. The gap between your Equifax and TransUnion scores can reach 100 points, which means checking only one bureau leaves you blind to how lenders actually see you.

Dispute Errors on Your Credit Report

Once you have both scores, examine your full credit report line by line because errors on your report directly tank your score and fixing them delivers faster gains than any other action. Dispute inaccuracies immediately through the bureau’s online portal or by mail, and corrections often appear within 30 days, meaning meaningful score jumps happen without you changing a single financial behavior. Most people waste months trying to improve their score when a simple error correction could have saved them that time.

Lower Your Credit Utilization Ratio Fast

Your next practical move targets your credit utilization ratio if it sits above 30 percent because this is the second fastest lever you control. Pay down balances before your statement closing date rather than waiting until month-end, or request a credit limit increase from your existing cards to drop your ratio instantly without extra payments. Hard inquiries from limit increase requests lower your score by a few points temporarily, but the utilization drop outweighs that cost. If you carry balances across multiple cards, prioritize paying down the card closest to its limit first because that concentrated utilization hurts more than spread utilization.

Protect Your Score With Autopay and Smart Habits

Set up autopay for at least the minimum payment on every account immediately because one late payment erases months of score improvement, and this single habit prevents more damage than any other protective measure. Avoid closing accounts after paying them off, avoid applying for multiple new credit products in short windows, and avoid maxing out cards even temporarily because these habits trigger the exact damage patterns that keep scores trapped in the fair or poor ranges.

Final Thoughts

Your credit score in Canada moves based on your actions every single month, which means you control your financial future starting today. The Canada credit score basics we’ve covered show that three habits matter most: paying on time without fail, keeping your utilization below 30 percent, and protecting your account history by never closing old cards. These three actions compound over time and deliver measurable results within 30 to 45 days.

Pull your scores from both Equifax and TransUnion this week because the gap between them could be substantial. Check your full credit reports for errors and dispute any inaccuracies immediately, since corrections often boost your score without requiring any behavior change. Then set up autopay on every account and request a credit limit increase to drop your utilization ratio fast.

Monitor your progress monthly through your bank’s free credit score tool or a dedicated monitoring service that tracks changes to your report. Lower interest rates on mortgages and auto loans save you tens of thousands of dollars over time, and better credit limits give you flexibility for emergencies and major purchases. We at Financial Canadian help you establish a strong financial foundation through our comprehensive resources and guidance to keep you informed and protected.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment