Your credit score is the number that lenders, landlords, and employers use to decide whether to trust you with money or opportunities. A weak score can cost you thousands in higher interest rates or lock you out of housing and jobs entirely.

At Financial Canadian, we’ve seen how quickly people can turn their finances around once they understand the mechanics of credit building. This guide shows you exactly how to build your credit Canada score, starting from wherever you are today.

Why Your Credit Score Actually Matters

Your credit score determines whether lenders will approve you for a mortgage, car loan, or credit card-and at what interest rate. You generally need a credit score of at least 580 to qualify for a mortgage, and a score of 760 or higher to get the best interest rate. On a $400,000 mortgage over 25 years, that difference in rates costs roughly $56,000 more in total interest payments. Banks and lenders use your score to assess risk, and a lower score signals higher risk to them. This isn’t theoretical-it’s how the Canadian lending system actually works, and it affects your wallet immediately.

How Your Score Affects Housing and Employment

Landlords increasingly pull credit reports before they rent apartments to tenants. A low score can result in a rejected application or demands for a larger security deposit. Some employers, particularly in financial services or positions requiring security clearances, also review credit reports as part of their hiring process. A damaged credit history can cost you job opportunities in these sectors. Beyond that, utilities companies and phone providers check your credit when you sign up for service. A poor score might mean you pay deposits upfront before they activate your account, or face denial of service altogether. These barriers compound quickly-if you can’t secure housing or a phone plan, stability becomes exponentially harder to achieve.

The Real Cost of Waiting

Every month you carry a high balance on a credit card at 28% interest costs you money that could go toward savings or investments. According to TransUnion, payment history is the single most important factor in credit scoring, and a single late payment can damage your score for years. The longer you wait to build good credit, the longer you stay stuck paying premium rates or facing credit denials entirely. Someone who starts building credit at 25 with consistent on-time payments will have a significantly stronger financial position by age 35 than someone who ignores their score until age 30. The compounding effect of lower interest rates, access to better credit products, and fewer financial barriers makes the difference between building wealth and staying stuck in debt.

Now that you understand what’s at stake, the next section shows you exactly how to build your credit score from scratch-whether you’re new to Canada or starting over after past financial setbacks.

How to Build Your Credit File from Scratch

Open a Secured Credit Card First

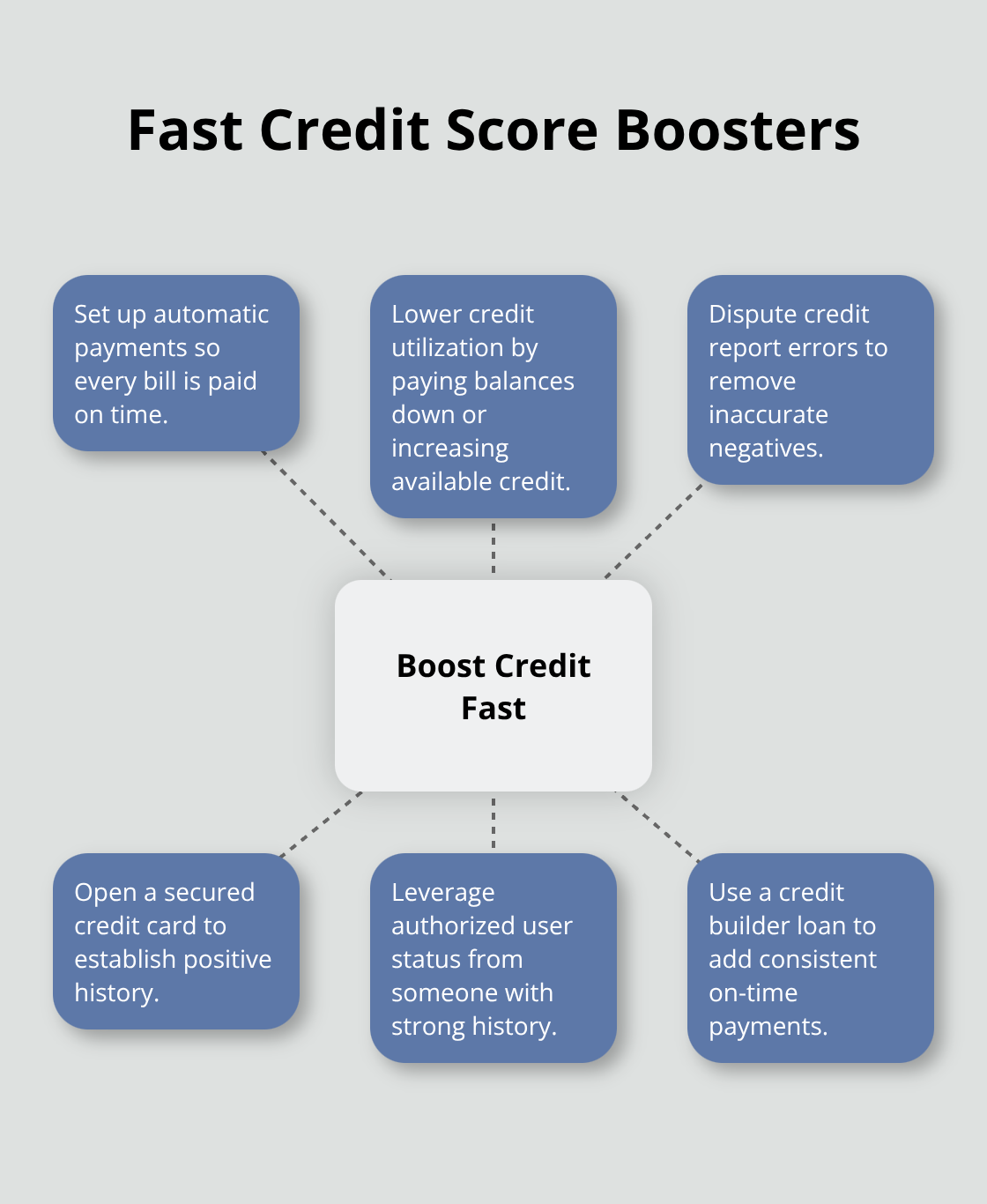

The fastest way to build credit from nothing is to open a secured credit card within your first month in Canada or immediately after deciding to rebuild. A secured card requires a cash deposit, which becomes your credit limit. TransUnion and Equifax both report secured card activity, so every on-time payment gets recorded on your credit file. The deposit sits in a separate account and doesn’t disappear-it’s collateral that protects the lender while you prove you can handle credit responsibly.

Most people see their first score appear within 30 to 90 days of opening the account, and that initial number matters less than the trajectory. Use the card for one small recurring purchase like a coffee or gas, then pay the full balance before the statement due date every single month. Keep your balance below 35 percent of the limit (so on a CAD 500 limit, never carry more than CAD 175). This single habit accelerates score growth faster than almost anything else you can do.

Leverage Authorized User Status

Ask someone you trust-a parent, partner, or close friend-to add you as an authorized user on their existing credit card if they have strong payment history and low utilization. You don’t even need to use the card; the account history transfers to your credit file once the card issuer reports it to the bureaus. This borrowed history gives your score an instant boost because you inherit years of on-time payments without creating any new debt.

Avoid becoming an authorized user on accounts with high balances or late payments, as that damage transfers too. If nobody close to you qualifies, skip this step and focus on your secured card instead.

Consider a Credit Builder Loan

A third option is a credit builder loan through some credit unions or online lenders like Koho or Borrowell, which work differently than traditional loans. You borrow a small amount, but the lender holds the funds in a locked savings account while you make monthly payments. After 12 months of on-time payments, you receive the money plus any interest earned, and your payment history gets reported to both TransUnion and Equifax.

This approach suits people who want structure and accountability because the loan forces discipline. The downside is that you pay interest on money you already have, but the credit file boost justifies the cost if you’re starting completely from zero. Whichever method you choose, consistency beats perfection-on-time payments matter more than waiting for the perfect product.

Now that you’ve established your initial credit file, the next section shows you how to accelerate your score growth through targeted actions that produce measurable results in weeks, not months.

Practical Actions to Improve Your Score Quickly

Make Automatic Payments Your Foundation

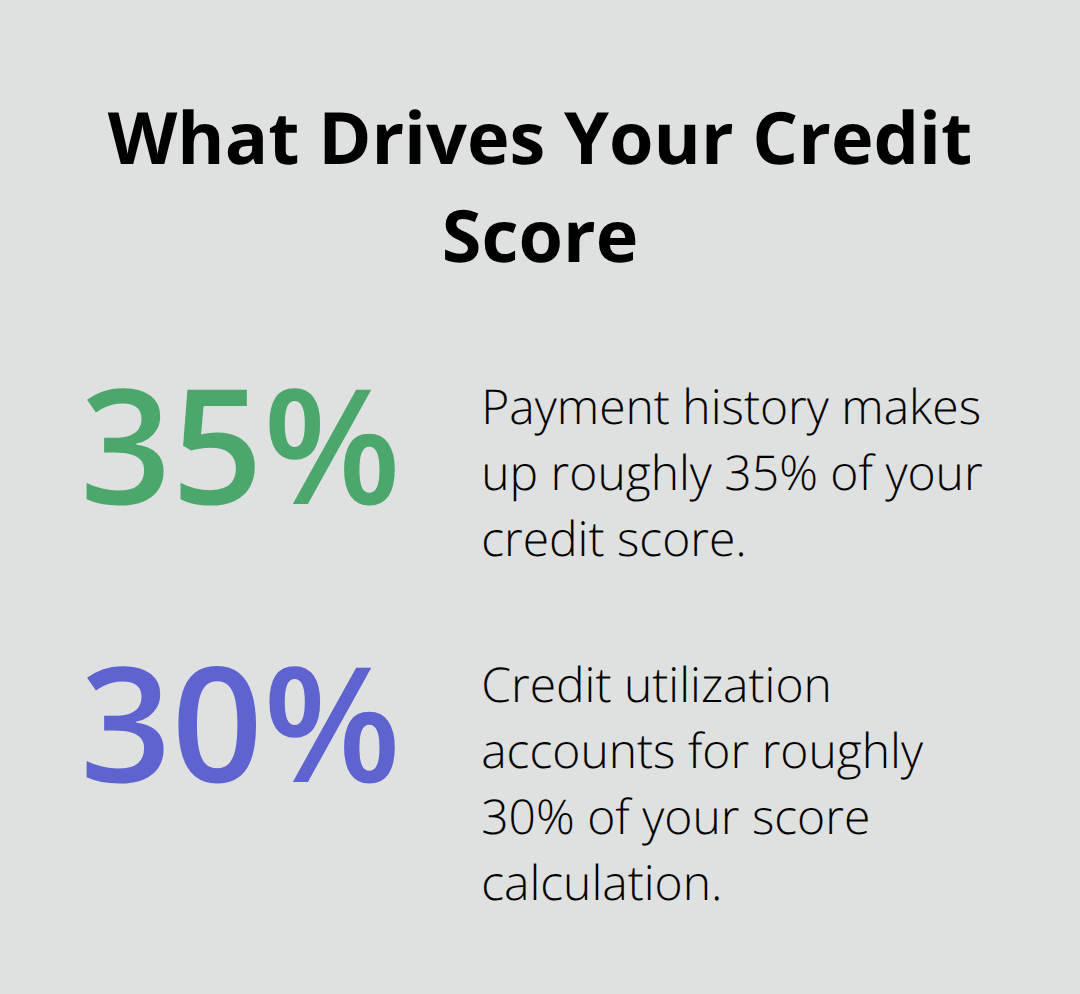

Automatic payments represent the single most effective move you can make right now. According to TransUnion, payment history accounts for roughly 35 percent of your credit score, making it the dominant factor in how lenders assess your creditworthiness. One missed payment can drop your score by 50 to 100 points depending on how recent it is, and that damage lingers on your credit file for six years.

Configure automatic payments for every credit card, loan, and bill the moment you open the account. Set them to pay on the statement due date, not earlier, because the payment needs to post to your statement before the due date to register as on-time. If you carry a CAD 5,000 balance on a credit card at 28 percent interest and miss even one payment, you lose not only the score points but also pay roughly CAD 116 in interest that month alone. Automatic payments eliminate human error and guarantee that your payment history stays pristine, which is how you build momentum toward a higher score.

Lower Your Credit Utilization Ratio

Reducing your credit utilization ratio produces visible results within 30 days. TransUnion identifies utilization as the second-most important scoring factor after payment history, accounting for roughly 30 percent of your score calculation. If you have a CAD 1,000 limit and carry a CAD 600 balance, your utilization sits at 60 percent, which actively drags your score down. Lower that balance to CAD 300 and your utilization drops to 30 percent, triggering an immediate score improvement that you can track within weeks. A credit utilization ratio at or below 30% can be an asset to your credit scores. Pay down your highest-utilization card first while maintaining automatic minimum payments on others, or open a second credit card to spread your balance across a larger available credit pool, which lowers your overall utilization ratio without requiring you to pay down debt.

Dispute Errors on Your Credit Report

Check your credit report for errors at least twice per year by requesting free reports from TransUnion and Equifax. Inaccurate accounts, duplicate entries, or fraudulent activity can artificially suppress your score, and disputing these errors takes 30 days on average to resolve. One person discovered a closed account still reporting as active with a CAD 2,000 balance, which inflated their utilization ratio and masked their actual creditworthiness until they filed a dispute. These mistakes happen more often than most people realize, and correcting them can produce a noticeable score jump without any additional effort on your part.

Final Thoughts

Most people see measurable improvement within 30 to 90 days of implementing these tactics. Your first score typically appears within three months of opening your first credit product, and from there, consistent on-time payments compound your progress month after month. Someone starting from zero can realistically reach a 650 score within 12 months if they stick to automatic payments and keep utilization below 30 percent, while reaching 720 or higher usually takes 18 to 24 months of disciplined behavior.

If you’re rebuilding after past damage, older negative marks gradually lose their impact as years pass, so patience becomes your advantage. A late payment from 2021 still affects your score today, but its weight diminishes continuously, and every on-time payment you make now strengthens your file and pushes those old marks further into the background. Your timeline depends on your starting point, but the direction matters more than the speed.

Open a secured credit card this week if you don’t have one, set up automatic payments for everything, and request your free credit reports from TransUnion and Equifax to identify any errors. Track your progress monthly by checking your score through your bank or a free service, and when you’re ready to strengthen your overall financial position, visit Financial Canadian to explore how we support your financial growth.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment