Finding a home in Canada means moving fast. When you spot the right property, you need proof that you’re a serious buyer-and that’s where home loan preapproval comes in.

At Financial Canadian, we know that preapproval can be the difference between winning a bidding war and watching your dream home slip away. This guide walks you through exactly how to get preapproved and what happens next.

What Preapproval Actually Does for Your Offer

A home loan preapproval is a lender’s written statement that you can borrow a specific amount of money at a specific rate. It is not a loan commitment-it’s a detailed evaluation based on your income, debts, credit score, and down payment funds. The Financial Consumer Agency of Canada distinguishes preapproval from final approval, which happens after you’ve made an offer and the lender has appraised the property. Preapproval typically takes 2 to 3 business days and locks in your rate for 30, 45, or 60 days, depending on the lender. This matters because sellers see a preapproval letter as proof you can close, which strengthens your negotiating position when bidding against other buyers. Without preapproval, you’re shopping blind-you don’t know your actual budget, and sellers won’t take your offer seriously.

The speed advantage in competitive markets

In markets like the Greater Toronto Area, preapproval speed directly affects your ability to compete. Most Canadian lenders deliver preapproval within 24 to 48 hours if your file is straightforward and your documents are complete. Some lenders process applications the same day. A week-long delay from your broker can cost you listings because other buyers with preapproval move faster. The difference between preapproval in 24 hours versus 5 days can mean losing the property to a faster offer. Your responsiveness matters too-if you don’t return documents quickly or miss communication, the clock keeps ticking. When you’re ready to make an offer, you need preapproval already in hand, not pending.

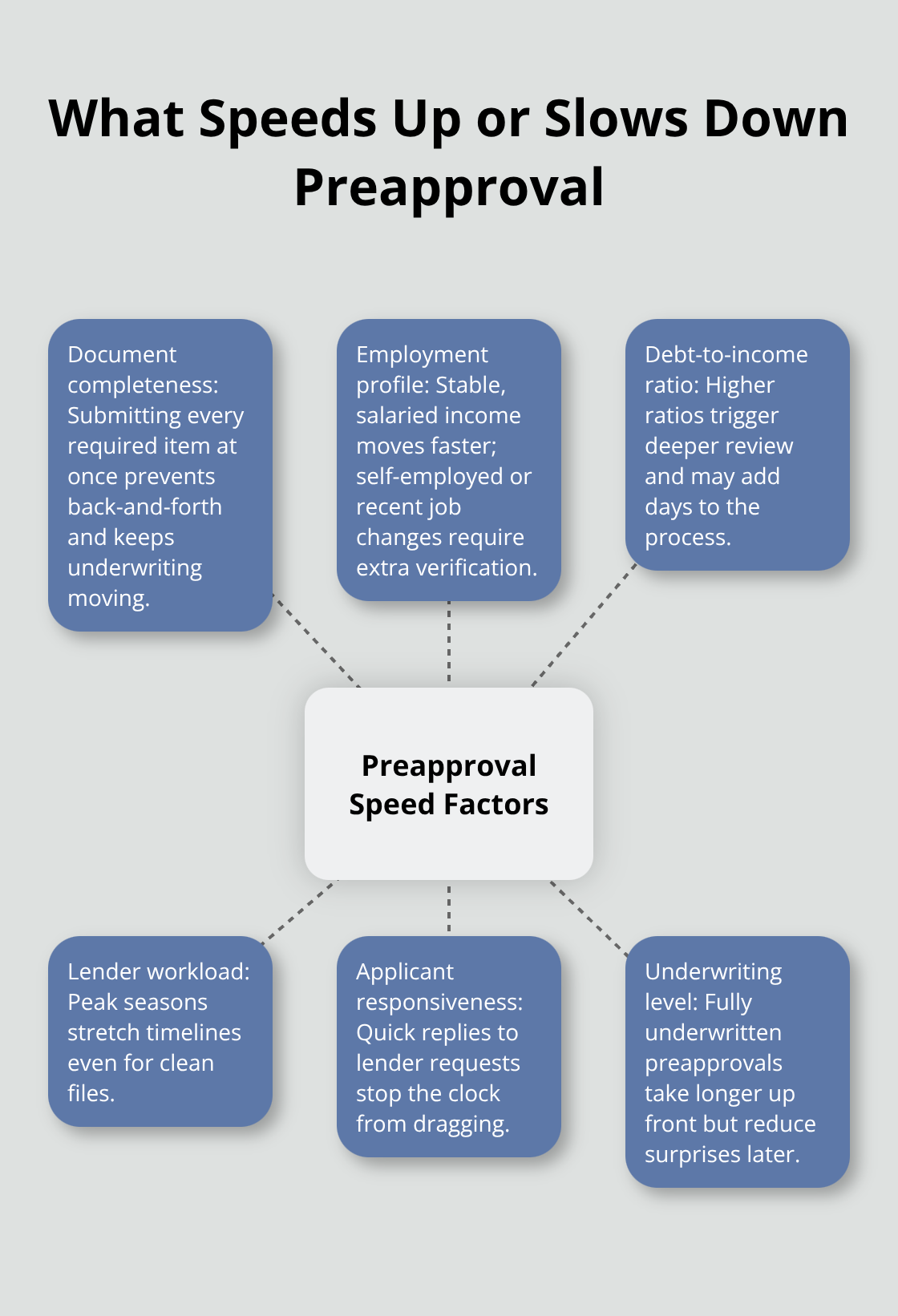

What speeds up or slows down your approval

Straightforward files move faster than complex ones. If you’re employed with stable income, have minimal debt, and a solid credit score, you’ll hit the 24 to 48 hour range. Self-employed income, recent job changes, or high debt-to-income ratios create delays because lenders need more documentation and scrutiny. Lender workload also affects timing-busy periods mean slower processing. The single biggest controllable factor is document completeness. Prepare your pay stubs, Notices of Assessment (if self-employed), recent bank statements, proof of down payment funds, and a list of current debts before you apply.

Missing even one document restarts the clock. You should also avoid taking on new credit or making large purchases before applying, as these actions trigger additional review and can lower your credit score, which may reduce your approved amount.

Timing your application strategically

Once preapproval expires, you’ll need updated documentation to renew it, so timing your application matters when you’re actively house hunting. If you apply too early, your preapproval expires before you find the right property. If you apply too late, you miss the competitive window when homes are listed. The best approach is to apply for preapproval once you’ve decided to start serious house hunting within the next 30 to 60 days. This positions you to move quickly when you find a property without waiting for renewal. Your lender can also discuss rate-lock options and whether an underwritten preapproval (which takes longer but provides stronger certainty) makes sense for your timeline. With preapproval locked in and your documents organized, you’re ready to shift focus to what lenders actually require once you’ve made an offer.

The Home Loan Preapproval Process in Canada

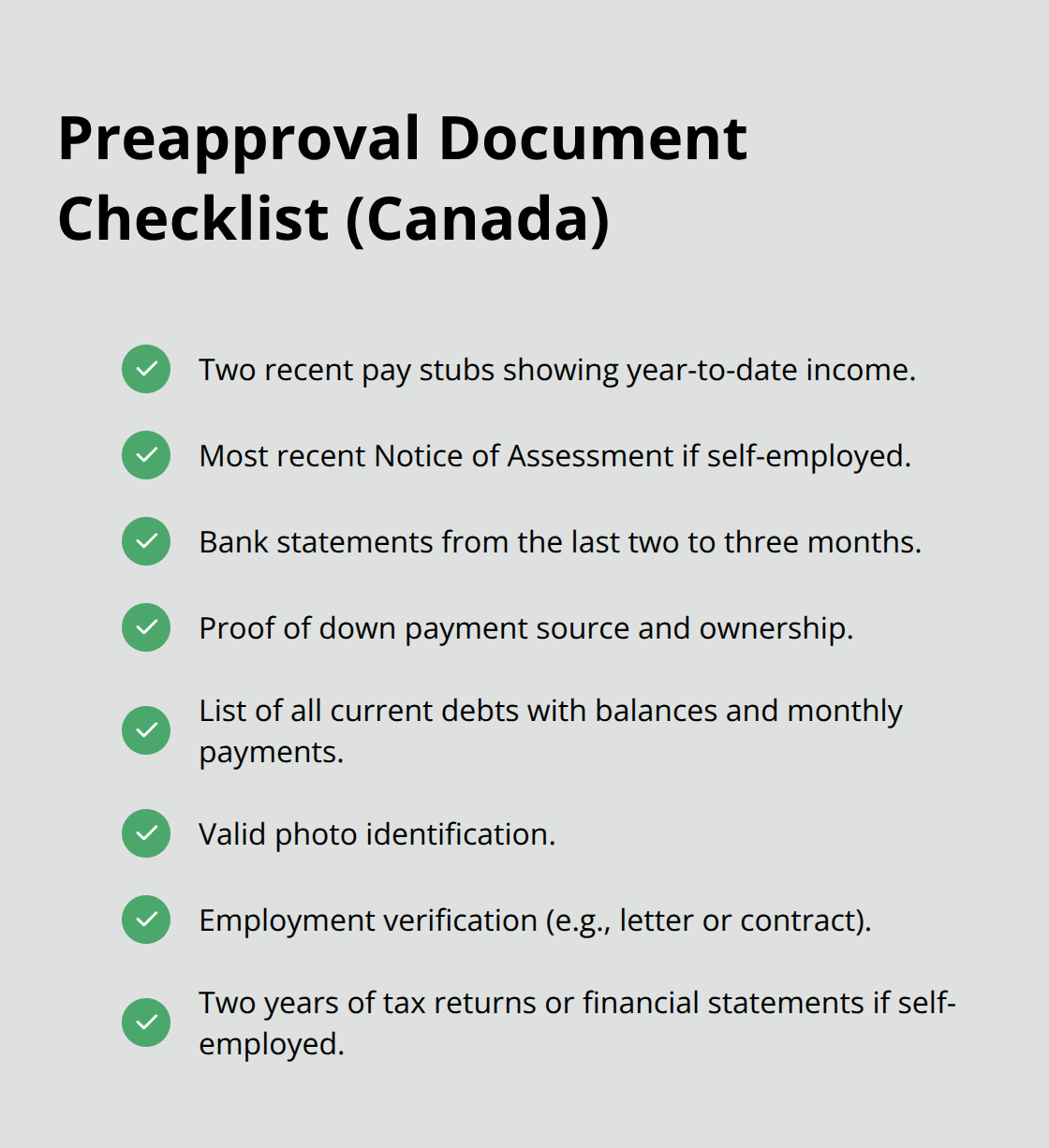

Lenders request specific documents not to create obstacles, but to verify your income, assess your debt obligations, and confirm your down payment is legitimate. When you apply for preapproval, organize these materials before you submit your application: two recent pay stubs (or your last two months of income if you’re paid differently), your most recent Notice of Assessment from the Canada Revenue Agency if you’re self-employed, bank statements from the last two to three months showing your down payment funds, and a written list of all current debts including credit cards, car loans, student loans, and lines of credit with their balances and monthly payments. You’ll also need photo identification and proof of employment. If you’re self-employed, lenders typically want two years of financial statements or tax returns to confirm income stability. Missing even one document forces your broker to follow up, which adds unnecessary days to your timeline. The Financial Consumer Agency of Canada notes that incomplete applications rank among the primary reasons preapproval takes longer than 48 hours. Organize these documents in a single folder before you contact a lender, then you can submit everything at once instead of trickling information over several days.

How Lenders Assess Your Credit and Finances

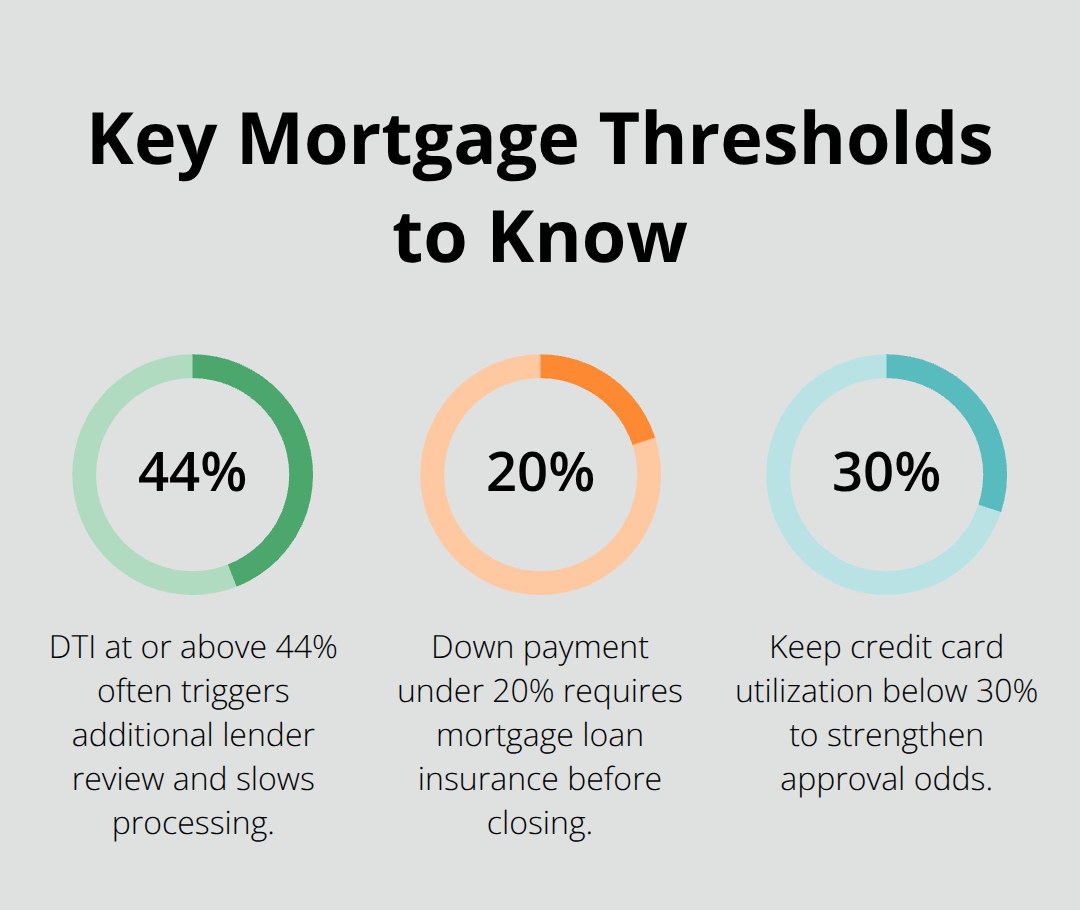

Your credit score determines whether you qualify and what rate you’ll receive. Most Canadian lenders pull a hard credit inquiry when you apply for preapproval, which temporarily lowers your score by a few points. The good news is that if you shop for rates with multiple lenders within a 14 to 45 day window, those inquiries count as a single hard check according to Equifax, so your score impact stays minimal. Lenders also calculate your debt-to-income ratio by dividing your total monthly debt payments by your gross monthly income. If your debt-to-income ratio exceeds 44 percent, many lenders flag your file for additional review, which slows processing. Someone earning $5,000 monthly with $2,200 in debt payments hits that threshold and should expect more scrutiny. Try to lower that ratio before applying by paying down credit cards or eliminating other debts. Lenders also verify employment stability because recent job changes or gaps in employment history raise red flags. If you changed jobs within the last three months, some lenders require a letter from your new employer confirming your position and salary. Self-employed applicants face stricter scrutiny because income fluctuates, so lenders examine two full years of tax returns and may apply a discount to your stated income.

Processing Speed and Validity Periods

Straightforward preapprovals typically complete within 24 to 48 hours if your documents are complete and your file is simple. Complex situations (self-employment, recent job changes, high debt levels) add two to five additional business days. After lenders complete their assessment, your preapproval remains valid for 60 to 120 days depending on the lender, though 90 days is most common. That validity period matters because rates fluctuate. If you find a property after 90 days pass, your preapproval expires and you’ll need updated income verification and financial documents to renew it. Plan your application timing accordingly. If you’re actively house hunting, apply for preapproval when you’re ready to make an offer within the next 30 to 60 days. If your preapproval is set to expire and you haven’t found a property, renew it before it lapses so you don’t lose your rate lock. Some lenders allow rate extensions at no cost, while others require a new application with fresh documentation. Ask your lender about renewal options upfront so you understand the process if you need to extend. With your preapproval locked in and your documents organized, you’re positioned to move quickly when you find a property. The next step involves preparing your financial profile to maximize your chances of approval and securing the best possible rate.

Get Your Financial Profile Ready Before You Apply

Check and Improve Your Credit Score

Your credit score is the first thing lenders examine, and improving it before applying for preapproval directly affects both approval odds and the rate you receive. Most Canadian lenders pull a hard credit inquiry during preapproval, which temporarily lowers your score by a few points, but the impact is temporary and recovers within months. More importantly, your current score determines your eligibility and rate tier. If your score sits below 620, many mainstream lenders will decline you or offer rates 1 to 2 percentage points higher than borrowers with scores above 700.

Check your credit report from Equifax or TransUnion at least 30 days before applying. Look for errors, late payments, or high credit card balances. Pay down credit card balances to below 30 percent of your limit before applying because high utilization signals financial stress to lenders. If you spot errors on your report, dispute them immediately with the credit bureau. Avoid opening new credit accounts or making large purchases in the 30 days before applying, as these actions lower your score and trigger additional lender scrutiny.

If you’re carrying high debt relative to your income, focus on paying down the highest-interest accounts first. Dropping your debt-to-income ratio to 40 percent or below removes friction from the approval process. A mortgage pre-approval will help you determine how much you may be able to borrow for your home.

Organize Your Documents Before You Submit

Document preparation is where most applicants lose time. Collect everything your lender needs before you submit your application rather than sending documents over several days.

You need two recent pay stubs showing year-to-date income, your most recent Notice of Assessment from the Canada Revenue Agency if you’re self-employed, bank statements from the last two to three months proving your down payment funds exist and are yours, a detailed list of all current debts with balances and monthly payments, and valid photo identification plus employment verification.

Self-employed applicants must prepare two full years of tax returns or financial statements because lenders scrutinize income stability. Missing even one document forces your broker to chase you for follow-up, adding unnecessary days to processing. Organize everything in a single folder before contacting lenders so you can submit the complete package at once.

Compare Preapproval Offers Strategically

When shopping for rates across multiple lenders, consolidate your applications within a 14 to 45 day window so multiple hard credit inquiries count as a single check, minimizing score damage. This strategy lets you compare preapproval offers from three to five lenders without stacking credit hits.

As you review offers, don’t fixate solely on interest rate. Compare the rate-lock period (30, 60, or 90 days), any fees charged for preapproval, whether the lender offers underwritten preapproval for stronger certainty, and the lender’s actual processing speed based on recent customer feedback. Some lenders advertise fast processing but deliver slowly during peak seasons, while others maintain consistent 24 to 48 hour turnarounds year-round. Ask each lender directly how many applications they’re processing and when you can expect a decision.

Final Thoughts

Home loan preapproval Canada gives you the competitive edge you need when speed determines outcomes. After you receive your preapproval letter, coordinate with a real estate agent to search within your approved budget and loan type, which eliminates wasted time viewing properties outside your reach. When you find a property and make an offer, submit your preapproval letter immediately to strengthen your negotiating position against competing buyers.

Your lender then moves into final approval, which requires a full application, updated income verification, proof of your down payment, detailed property information, and typically a property appraisal (this stage usually takes one to two weeks, though appraisal delays can extend that timeline). Before closing, your lender requires active home insurance, and if your down payment is under 20 percent, mortgage loan insurance becomes necessary. Factor these costs into your budget planning.

At Financial Canadian, we help you build a strong digital foundation for your financial decisions with resources and tools designed for clarity and action. Consult the Financial Consumer Agency of Canada and Canada Mortgage and Housing Corporation for authoritative guidance on mortgage processes and regulations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment