Your credit score shapes your financial life in Canada. Lenders use it to decide whether you qualify for mortgages, car loans, and credit cards-and what interest rates you’ll pay.

We at Financial Canadian believe credit score monitoring in Canada isn’t optional. Regular checks help you catch errors, spot fraud early, and take control of your financial future.

How Your Credit Score Is Calculated in Canada

Your credit score in Canada comes from one of two main credit bureaus: Equifax Canada or TransUnion Canada. These companies track your borrowing and payment history, then use that data to generate a three-digit number that lenders rely on. TransUnion uses the VantageScore 3.0 model, which means your score reflects a specific calculation method, but lenders don’t always use the same scoring model when they assess you. Some use FICO-based scores while others use bureau-specific scores, so your actual score can vary depending on which lender pulls your file. This variation matters more than most people realize. A mortgage lender might see a different score than your credit card issuer, which is why relying on a single score check gives you an incomplete picture of how lenders view you.

What Actually Moves Your Score

Your payment history carries the most weight in your credit calculation. Consistent on-time payments build your score over months and years. Credit utilization comes next-how much of your available credit you use.

If you have a $5,000 credit limit and carry a $4,500 balance, that 90% utilization hurts your score far more than a $500 balance would. The length of your credit history also matters. Older accounts demonstrate stability, which is why closing your oldest credit card is often a mistake. New credit inquiries and recent account openings temporarily lower your score because lenders interpret them as financial desperation. Checking your own score through credit monitoring services doesn’t hurt you, but hard inquiries from lenders do.

How Your Score Affects Borrowing Costs

Your credit score determines whether you get approved for credit and what interest rate you pay. A score of 750 or higher typically qualifies you for the best rates on mortgages and car loans, potentially saving you thousands of dollars over the life of the loan. Below 650, and many lenders reject you outright or charge significantly higher rates. The difference between a 700 score and a 750 score can cost you tens of thousands in extra interest on a mortgage.

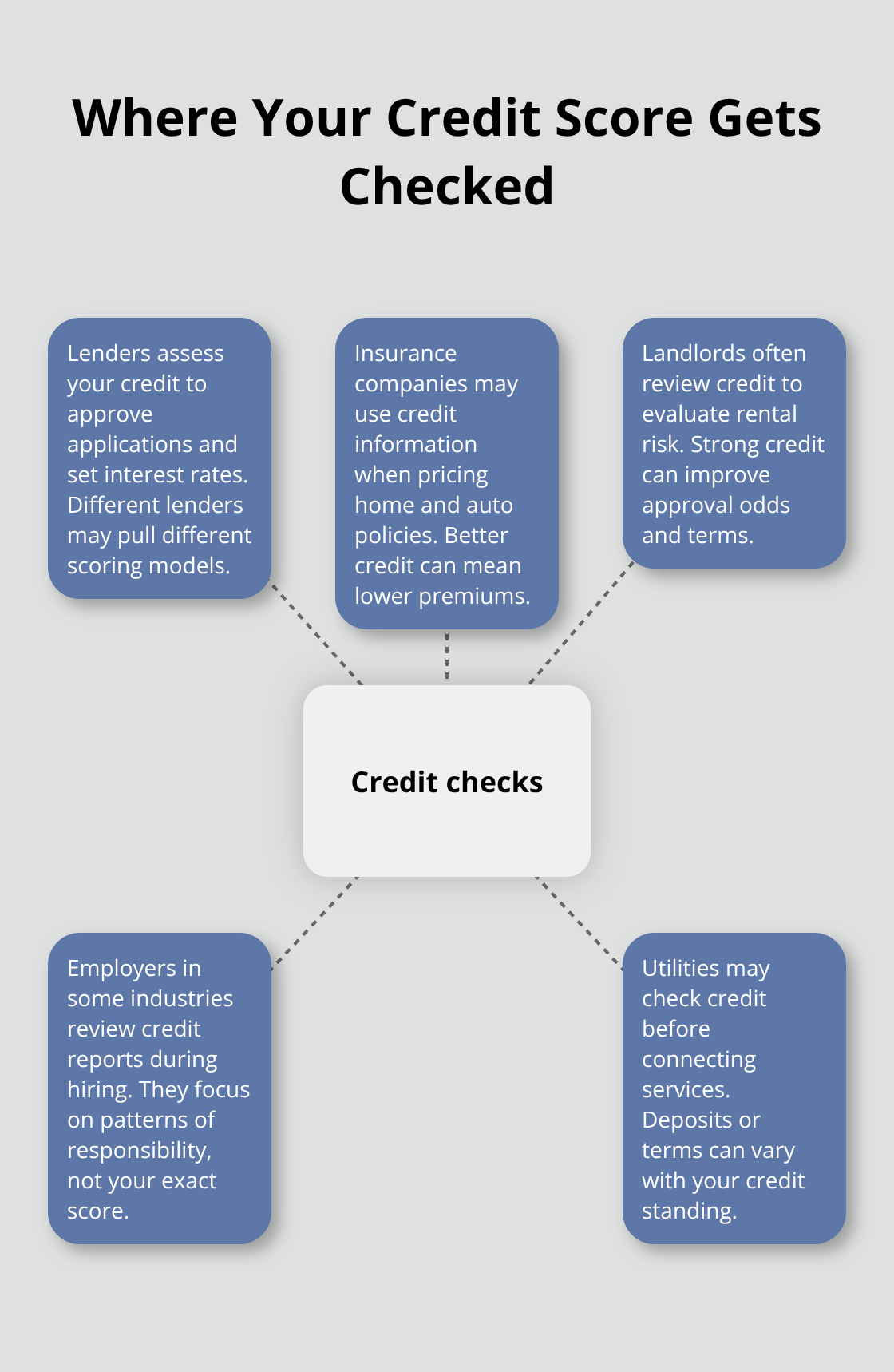

Beyond Loans: Where Your Score Matters

Lenders aren’t the only ones checking your score. Insurance companies use credit information to set premiums on home and auto policies. Landlords pull your credit before renting you an apartment. Employers in certain industries review credit reports during hiring.

Utility companies sometimes check your score before connecting services. This means a poor score ripples through your entire financial life, not just loan applications. The practical takeaway is simple: protecting your score isn’t about vanity-it’s about controlling your actual borrowing costs and access to essential services.

Now that you understand how your score works and why it matters, the next step is learning how to monitor it effectively and catch problems before they damage your financial health.

How to Monitor Your Credit Score Effectively

Check your score quarterly, and more frequently if you’ve recently applied for credit or suspect fraudulent activity. Free weekly online credit reports are available from Equifax, Experian and TransUnion at no cost and don’t impact your score. This serves as your baseline tool. Many Canadian banks and credit card issuers now offer free score monitoring through their apps-check what your financial institution already provides before paying for anything.

Choose the Right Monitoring Service for Your Needs

TransUnion’s subscription service costs $24.95 CAD per month plus tax and includes unlimited access to your full credit report, score updates, and alerts when key changes occur. The alerts matter more than the score itself because they catch fraud within days instead of months. If you prioritize protection, the service also includes up to $1,000,000 in expense reimbursement insurance for identity restoration costs and data compromise resolution assistance. Quebec residents can view their score and score factors for free through consumer disclosure, so check your provincial rules before subscribing.

When comparing monitoring services, prioritize clear privacy policies and transparency about data sharing. Some free apps sell your information to advertisers or third parties, which defeats the purpose of protecting your credit. Enable two-factor authentication on any monitoring account and use unique, strong passwords.

Build a Monitoring Routine That Works

Set a routine check after major financial events like opening a mortgage, applying for a car loan, or moving to a new address. This habit catches unauthorized activity quickly and prevents small problems from becoming major credit damage. Track when you check your score and what changes appear between checks.

Address Errors Immediately

Errors on your credit report are surprisingly common and directly damage your score. If you spot an incorrect account, wrong balance, or payment marked late when it wasn’t, contact the bureau that reported it immediately. You can start a dispute through TransUnion or Equifax Canada’s consumer assistance resources at no cost. The dispute process typically takes 30 days, and the bureau must verify the information with the creditor. If the creditor can’t confirm the error, it gets removed. Document everything in writing and keep copies of your dispute submissions-don’t rely on phone calls alone.

Respond to Fraudulent Activity

If fraudulent accounts appear, place a fraud alert with both TransUnion and Equifax Canada simultaneously to notify creditors to verify your identity before extending credit. You can add a free credit freeze to control who accesses your credit information and unfreeze it temporarily when you apply for legitimate credit. For serious identity theft, request a consumer disclosure to see your complete file, then dispute every fraudulent item systematically.

Now that you understand how to monitor your score and handle errors, the next step is learning how to recognize fraud before it happens and protect yourself from identity theft.

Protecting Your Credit from Fraud and Identity Theft

Fraud doesn’t announce itself. Most identity theft victims discover the problem months after criminals open accounts in their names, leaving devastating damage on their credit reports. The warning signs are subtle but unmistakable if you know what to look for. Unexpected credit inquiries appear when you haven’t applied for anything-lenders pull your file when someone applies for credit using your information. Accounts you don’t recognize show up on your credit report, ranging from small store credit cards to major loans. Bills arrive for services you never signed up for. Your credit score drops sharply without explanation. You stop receiving regular bills from legitimate creditors, which means fraudsters may have changed your mailing address. Creditors call about accounts you don’t have. You’re denied credit despite having good payment history. These aren’t minor inconveniences-they’re direct evidence that someone is using your identity to borrow money in your name. The longer fraud remains undetected, the more damage accumulates. This is why quarterly credit checks matter enormously. A fraud alert placed immediately with TransUnion and Equifax Canada can prevent criminals from opening new accounts, but only if you catch the fraud within weeks, not months.

Act Fast When Fraud Strikes

Speed determines whether you contain the damage or spend years cleaning it up. The moment you suspect fraud, contact both credit bureaus simultaneously to place a fraud alert, which forces creditors to verify your identity before extending credit. This single step stops most new fraudulent accounts from being opened. Next, obtain your complete credit report from both TransUnion and Equifax Canada to identify every fraudulent account and incorrect information. Start disputes for fraudulent items immediately through each bureau’s consumer assistance resources-the dispute process takes roughly 30 days, and bureaus must verify information with creditors. If creditors cannot confirm the fraudulent accounts, they get removed. For serious identity theft, consider a credit freeze, which prevents anyone from accessing your credit file without your explicit permission. You unfreeze temporarily when you apply for legitimate credit. TransUnion’s data compromise resolution assistance helps you navigate the bureaucratic nightmare of responding to data breaches, which often trigger identity theft. Contact the financial institutions where fraudulent accounts were opened and file reports with them directly. Request that fraudulent charges be reversed and accounts closed. Document everything in writing-emails, letters, dispute submissions-and keep copies organized by date and creditor. If you’ve been a victim of serious identity theft, TransUnion’s subscription service includes up to one million dollars in expense reimbursement insurance to cover costs of restoring your identity, which can include legal fees, credit monitoring, and lost wages from dealing with the aftermath.

Build Active Defenses Against Unauthorized Access

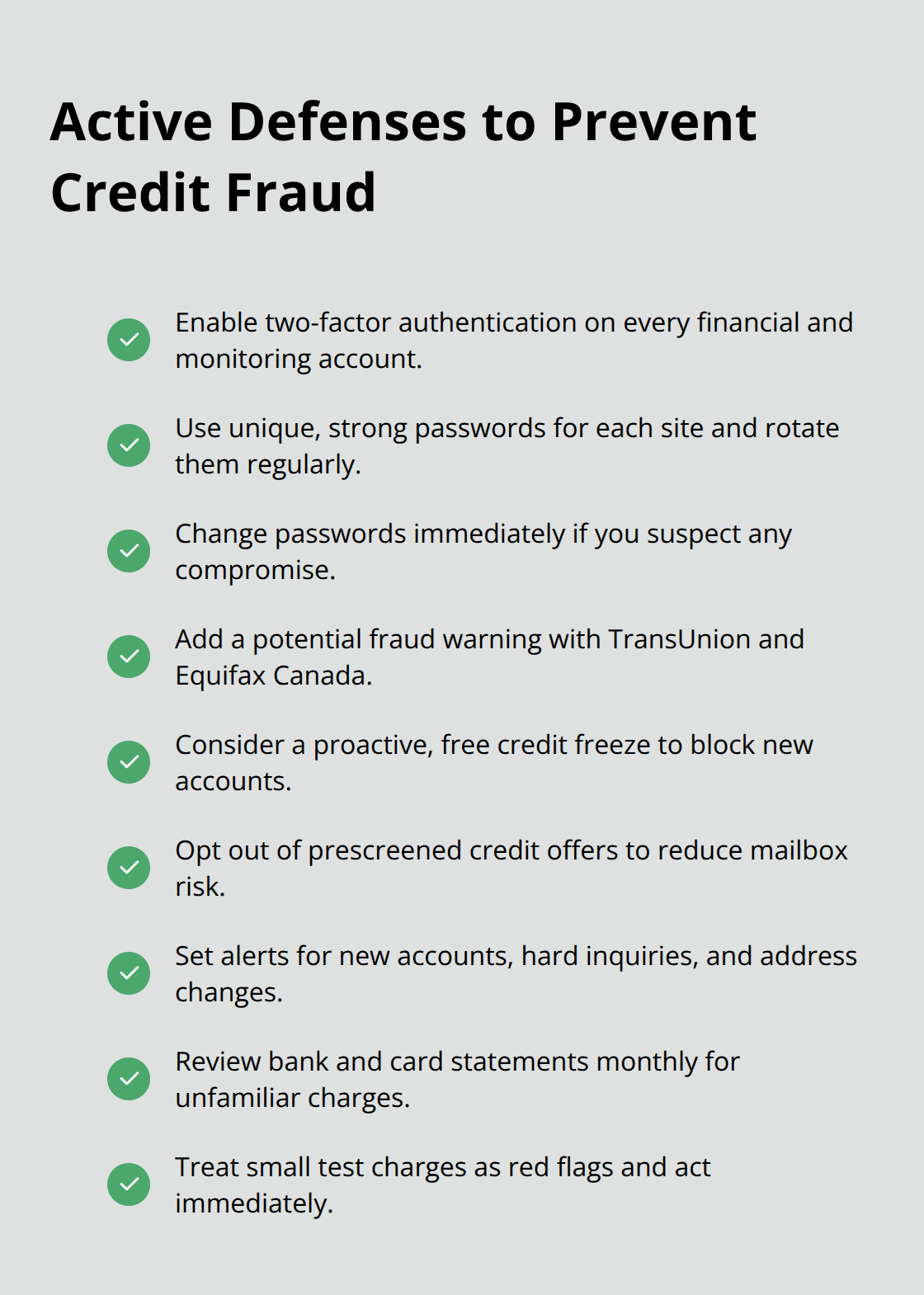

Passive monitoring catches fraud after it happens. Active defense prevents it from happening in the first place. Enable two-factor authentication on every financial account and credit monitoring service you use-this makes it exponentially harder for criminals to access your accounts even if they steal your password.

Use unique, strong passwords for each account rather than recycling the same password across multiple sites. Change passwords immediately if you suspect any account compromise. Add a potential fraud warning to your credit file with TransUnion and Equifax Canada to alert creditors to take extra verification steps. Consider a proactive credit freeze even if you haven’t experienced fraud-it’s free and prevents criminals from opening accounts during data breaches. Opt out of prescreened credit offers through Equifax and TransUnion, which reduces the number of offers criminals can intercept from your mailbox. Monitor your credit report quarterly and set alerts for key changes like new accounts, hard inquiries, and address changes. These alerts notify you within days of suspicious activity rather than weeks. Review your financial statements and credit card bills monthly, not just at year-end. Criminals often test stolen information with small charges first before making large purchases. Catching a five-dollar charge immediately prevents a five-thousand-dollar fraud from following.

Final Thoughts

Credit score monitoring Canada requires consistent action, not one-time effort. A single fraudulent account can tank your score by 100 points and lock you out of mortgages and car loans for years, which is why quarterly checks matter far more than most people realize. Free weekly reports from annualcreditreport.com provide a baseline snapshot, but alerts from paid monitoring services catch fraud within days instead of months-the difference between a quick fix and years of credit repair.

You control your credit narrative only when you actively monitor it. Two-factor authentication and strong passwords protect your accounts from unauthorized access, while fraud alerts and credit freezes stop criminals from opening new accounts in your name. Disputes remove fraudulent items systematically, and TransUnion’s subscription service costs $24.95 CAD monthly with up to one million dollars in expense reimbursement coverage for identity restoration. Set a quarterly reminder to review your score, enable alerts for key changes, and document everything in writing when you dispute errors.

We at Financial Canadian help you build a strong financial foundation through reliable credit guidance and resources. Check your credit report this week and set up monitoring through your bank’s app or a paid service that fits your protection needs. Start your defenses now, and you’ll catch problems before they become crises.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment