Need cash without putting up collateral? Unsecured personal loans in Canada offer a straightforward way to borrow money based on your creditworthiness and income alone.

At Financial Canadian, we’ve put together this guide to help you understand how these loans work, what lenders expect from you, and how to find the best rates available.

How Unsecured Personal Loans Work in Canada

An unsecured personal loan gives you access to cash based on your ability to repay, not on pledging an asset as collateral. Lenders assess your creditworthiness through your credit score, income stability, and existing debt levels. You then repay the loan in fixed monthly installments over a set term, typically ranging from 6 to 60 months, though some lenders extend to 84 months. The interest rate you receive depends heavily on your credit profile. Unsecured personal loans represent a significant portion of consumer borrowing, reflecting their widespread use across the country. Canadians commonly use these loans for debt consolidation, home renovations, emergency expenses, and other flexible needs. The key advantage is speed and simplicity-online lenders can approve and fund your loan within 24 to 48 hours, compared to traditional banks which often require longer processing times and in-branch visits.

Why unsecured loans cost more than secured alternatives

Unsecured loans carry higher interest rates than secured options because lenders have no asset to seize if you default. Rates typically range from 6% to 35% depending on your credit score and the lender type. Borrowers with good to excellent credit (roughly 660 or higher) can access rates around 6% to 21%, while those with fair or poor credit face rates from 21% to 35%.

Major Canadian banks like Scotiabank offer personal loans at 6% to 10%, BMO at 8.99% to 22.99%, and TD at 8.99% to 23.99%, while online lenders like Spring Financial and goPeer provide broader ranges from 9.99% to 34.95% with faster approvals. Beyond interest rates, origination fees typically add 0.5% to 5% of your loan amount, and you may face late fees, NSF charges, prepayment penalties, or optional loan protection insurance around 2.5% monthly. APR (Annual Percentage Rate) matters more than advertised interest rates-APR includes all fees and reflects your true cost.

The trade-off: convenience versus collateral risk

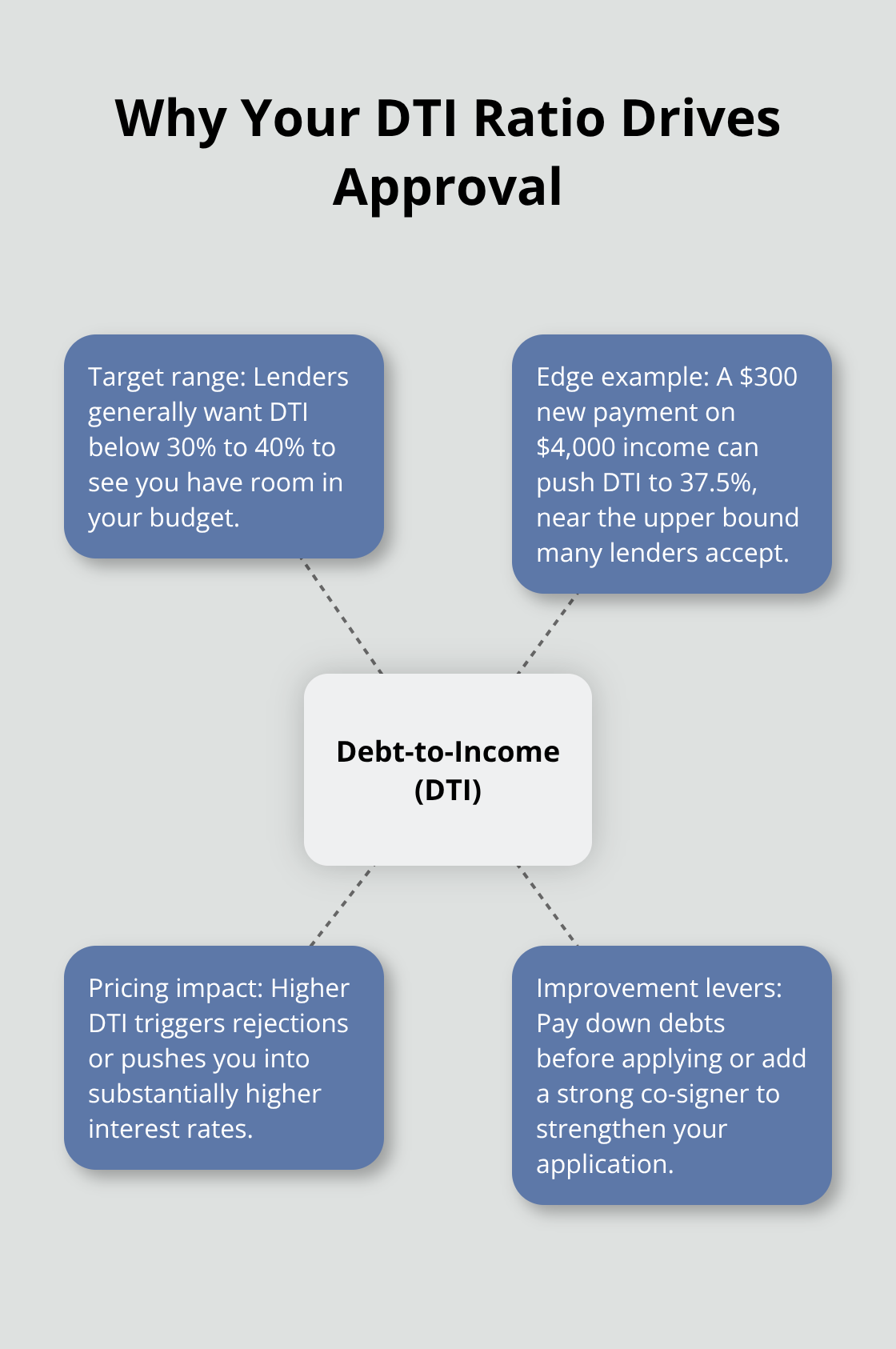

Unsecured loans avoid putting your home, vehicle, or other assets at risk, which is their primary appeal. However, this convenience comes with smaller borrowing limits and stricter approval requirements. Most lenders cap unsecured personal loans at $25,000 to $35,000, whereas secured loans tied to home equity can reach $100,000 or more. Your debt-to-income ratio significantly influences approval odds and pricing. Lenders prefer seeing your monthly debt payments consume less than 30% to 40% of your gross monthly income. If you have a stable job with documented income, you qualify at competitive rates far more easily. A co-signer with strong credit and income can improve your approval odds if you fall short, though both parties become equally responsible for repayment. Canada’s 2025 regulatory cap of 35% APR on criminal lending provides a ceiling you should never exceed-if a lender quotes higher rates, walk away immediately.

What happens next in your application

Your lender will request proof of income, employment verification, and a review of your existing debts to calculate your debt-to-income ratio. This assessment determines whether you qualify and at what rate. Processing timelines vary significantly-online lenders typically complete approvals within 24 to 48 hours, while traditional banks may take several business days or longer. Once approved, funds transfer directly to your bank account, and you start repayment on your scheduled date. Understanding these steps helps you prepare the right documentation and choose a lender whose timeline matches your cash needs.

What Lenders Actually Look For When You Apply

Your credit score matters, but it’s not the only factor that determines approval and your interest rate. Lenders at banks, credit unions, and online platforms evaluate three core elements: your creditworthiness, ability to repay, and your existing debt load. A credit score of 600 or higher opens doors to reasonable rates, but the real sweet spot sits around 660 and above-borrowers in this range typically qualify for rates between 6% and 21% rather than the punishing 21% to 35% rates reserved for those with lower scores.

Check Your Credit Before You Apply

Errors on your credit report occasionally drag down your score unfairly. Check your credit report through Equifax Canada or TransUnion Canada before you submit an application. Correcting mistakes takes time, so start this process early if you plan to apply soon. Beyond the number itself, lenders want proof that you earn stable income. Most require tax returns, recent pay stubs, and employment verification to confirm you won’t disappear mid-loan. CIBC, for example, sets a minimum gross annual income around $17,000, though larger loans from major banks typically demand higher thresholds.

Income Verification Speeds Vary by Lender Type

This verification step takes time at traditional banks but happens almost instantly with online lenders. Spring Financial and goPeer can fund loans within 24 to 48 hours while your local branch takes days or weeks. Online platforms automate income checks through digital systems, whereas banks conduct manual reviews that require staff time. If you need cash urgently, this speed difference matters significantly. Traditional banks offer lower rates but sacrifice convenience; online lenders trade higher rates for rapid access to funds.

Your Debt-to-Income Ratio Determines Approval or Rejection

Your debt-to-income ratio is where approval often succeeds or fails, yet most borrowers ignore it entirely. This ratio measures your monthly debt payments against your gross monthly income-lenders prefer seeing it below 30% to 40%. If you earn $4,000 monthly and already owe $1,200 in car payments, credit card minimums, and student loan installments, adding a $300 personal loan payment pushes you to 37.5%, which sits at the edge of acceptable. High debt-to-income ratios trigger either rejection or substantially higher rates because lenders view you as stretched thin.

The fastest way to improve your odds is paying down existing debts before you apply-even eliminating one credit card reduces your ratio meaningfully and can unlock better rates. A co-signer with strong credit and documented income strengthens your application if your own profile falls short, but understand that both of you become legally responsible for the full loan amount if you default.

Timeline From Application to Funding

The application itself moves quickly once you submit documents. Online lenders typically approve within hours, while banks may take several business days for manual review. Approval doesn’t mean immediate funding-expect another 24 to 48 hours for money to land in your account once you’ve signed final paperwork. Understanding these timelines helps you plan your cash needs realistically.

With approval secured and funds transferred, you now face the critical decision of which loan terms and repayment structure actually fit your financial situation-a choice that separates borrowers who thrive from those who struggle under the weight of their debt.

Which Lender Offers the Best Rate for Your Situation

Compare APR, Fees, and Monthly Payments

Shopping for unsecured personal loans requires comparing three concrete numbers: the APR, all fees included, and your actual monthly payment under different term lengths. The APR matters far more than the advertised interest rate because it captures origination fees, which typically run 0.5% to 5% of your loan amount. A bank advertising 8% interest might charge a 2% origination fee that gets added to your balance, effectively raising your true cost. Spring Financial quotes rates from 9.99% to 34.95%, while goPeer ranges from 8.99% to 34.99%, and major banks like Scotiabank offer 6% to 10% for their best borrowers. The gap between these options is enormous. A $10,000 loan at 6% over five years costs roughly $1,064 in interest, while the same loan at 25% costs $6,873. That $5,809 difference determines whether you make smart financial progress or dig yourself deeper into debt.

Your credit score directly controls which rates you actually qualify for, not the advertised range. If Scotiabank shows 6% to 10%, only their top-tier borrowers with credit scores above 750 see 6%. Anyone below 700 gets pushed toward 9% or 10%. Online lenders cast a wider net and approve borrowers with lower credit scores, but they charge substantially more for that flexibility.

Fixed Rates Versus Variable Rates

CIBC, TD, and BMO all tie their variable-rate loans to the Bank of Canada prime rate, which currently sits at 2.25% as of January 2026, meaning your rate adjusts if the central bank changes policy. Fixed-rate loans from these same banks remove that uncertainty but typically cost 0.5% to 1% more upfront. The choice between fixed and variable depends on your comfort with payment fluctuations. Fixed rates protect you from rising costs; variable rates offer lower initial payments but expose you to increases if the prime rate climbs.

Speed Versus Cost: The Core Trade-Off

The real decision hinges on how quickly you need money versus how much you’re willing to pay. Banks offer their lowest rates but demand minimum loan amounts around $5,000 and funding timelines of several business days. Online lenders fund within 24 to 48 hours but charge 3% to 10% higher rates for that speed. A $15,000 loan illustrates this trade-off: at a bank’s 8% fixed rate over five years, your monthly payment is $304. At an online lender’s 18% rate for the same term, you pay $396 monthly-that’s $92 extra every month or $5,520 over the loan’s life.

Prepayment penalties also vary wildly. Some lenders let you pay off early without penalty, while others charge 2% to 5% of the remaining balance if you settle early. If you expect a bonus or inheritance that could let you clear the debt faster, a lender with no prepayment penalty saves you thousands.

Term Length and Total Interest Paid

Loan terms range from one month to seven years, and the math is counterintuitive: longer terms feel easier because monthly payments drop, but total interest paid climbs sharply. A $10,000 loan at 15% costs $1,604 over three years but $2,451 over seven years. Calculate your payment under at least two different term lengths before committing, because most borrowers pick the longest term and regret the extra interest later. Use a loan calculator to plug in your actual numbers rather than relying on rough estimates. The Bank of Canada website and most lender sites offer free calculators that show your exact monthly payment and total interest.

Credit unions deserve mention because they often approve borrowers with weaker credit than banks and charge less than online lenders, but they’re province-specific and require membership. If you belong to one, compare their rates before looking elsewhere.

Final Thoughts

Unsecured personal loans in Canada offer genuine flexibility when you need cash without risking collateral, but they demand careful comparison before you commit. The difference between a 6% loan and a 25% loan on a $10,000 balance is nearly $5,800 in extra interest-a gap that determines whether borrowing accelerates your financial goals or derails them. Your credit score, income stability, and debt-to-income ratio control your approval odds and pricing, so improving any of these before applying directly lowers your costs.

Banks offer the lowest rates but demand longer processing times and higher minimum loan amounts, while online lenders approve within 24 to 48 hours at substantially higher rates. Credit unions often split the difference if you have membership. Compare the APR across at least three lenders, calculate your monthly payment under two different term lengths, and check for prepayment penalties before signing anything.

Pull your credit report from Equifax Canada or TransUnion Canada, calculate your debt-to-income ratio, and gather your recent pay stubs and employment verification. Request quotes from at least one bank, one online lender, and one credit union if available. We at Financial Canadian understand that navigating unsecured personal loans in Canada requires clear information and practical guidance-visit our site to explore how we support your financial journey.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment