Choosing a mortgage is one of the biggest financial decisions you’ll make. With so many mortgage options in Canada, understanding the differences between fixed-rate, variable-rate, government-backed, and specialized products can save you thousands of dollars.

At Financial Canadian, we’ve created this comparison guide to help you navigate your choices and find the mortgage that matches your financial situation.

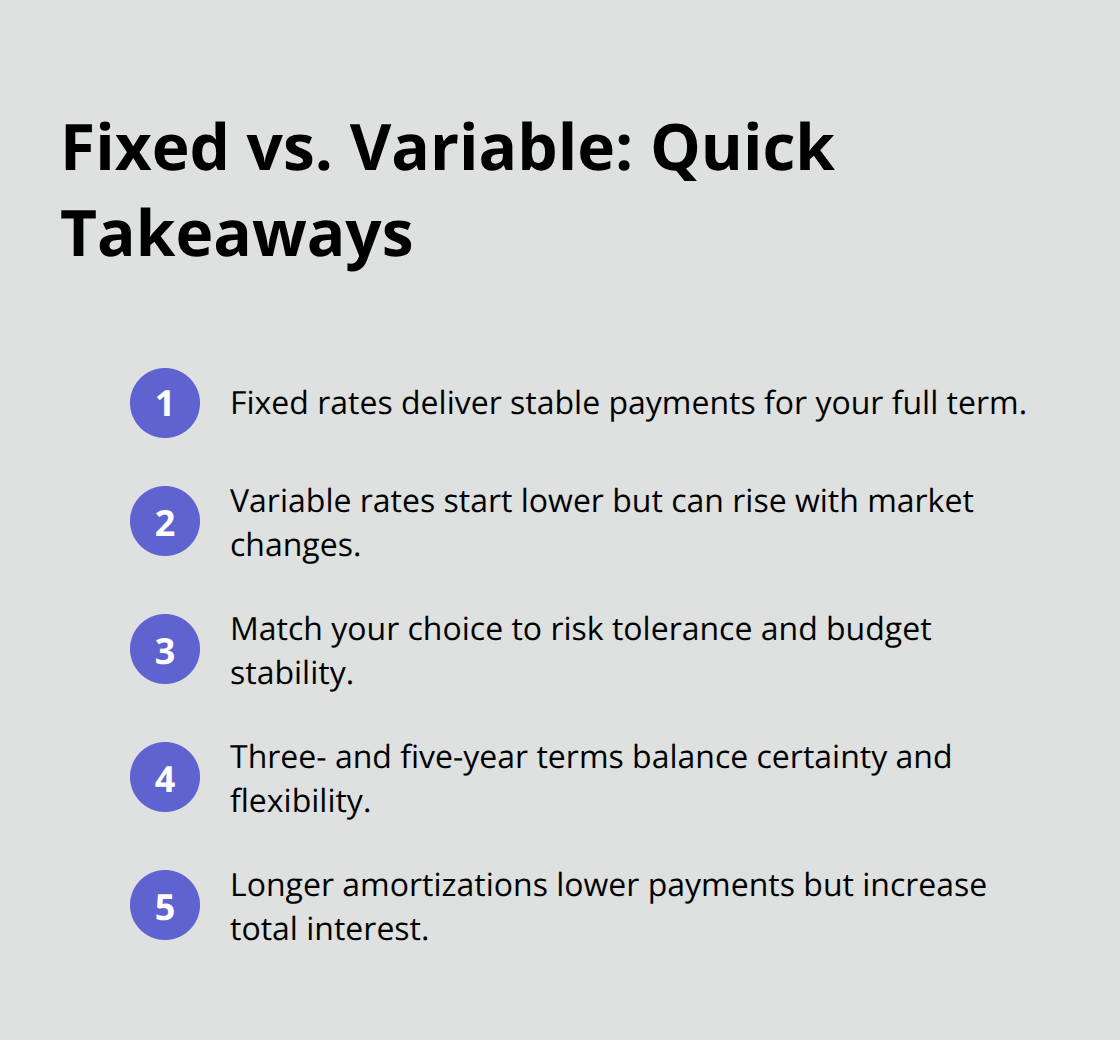

Fixed-Rate vs Variable-Rate Mortgages

How Fixed-Rate Mortgages Work and Their Stability

Fixed-rate mortgages lock in your payment for the entire term, so your principal and interest payment remains identical whether the Bank of Canada raises rates or cuts them. A 5-year fixed means you pay the same amount every month for five years, regardless of economic conditions. This stability appeals to homeowners who want budget certainty, especially those with pandemic-era mortgages facing significantly higher payments at renewal. The tradeoff is real: fixed rates typically start higher than variable rates. Right now, five-year fixed mortgages sit around 4.29–4.72%, while five-year variable rates hover near 3.35%. Over a 25-year mortgage, that difference compounds substantially. On a $400,000 mortgage, the fixed option costs roughly $60,000 more in interest over the full amortization compared to a variable rate that stays constant.

Variable-Rate Mortgages and Interest Rate Risk

Variable-rate mortgages start lower but fluctuate with the Bank of Canada’s overnight rate, which currently sits at 2.25%. When rates rise, your payment climbs; when they fall, you save money. TD research shows that a significant share of homeowners now expect mortgage payments to rise, prompting them to cut daily spending in preparation. This uncertainty drives many borrowers toward fixed-rate mortgages despite their higher initial cost. Economists broadly expect the Bank of Canada to hold rates steady through 2027, which means variable rates may not move much in the near term. However, geopolitical tensions and oil-price spikes present inflation risks that could change that outlook. If you have high risk tolerance and believe rates will stay low or fall, variable mortgages offer genuine savings potential.

Comparing Costs Over 25 and 30-Year Terms

The choice between fixed and variable mortgages becomes more complex when you factor in amortization length. A 30-year amortization spreads payments over a longer period, reducing monthly costs but increasing total interest paid. Fixed-rate mortgages eliminate guesswork about future payments, while variable options reward patience if rates decline. Three- and five-year terms currently offer the best balance between rate certainty and flexibility, allowing you to reassess your options more frequently than longer terms while avoiding the volatility of ultra-short two-year products. If rates rise significantly, that variable mortgage becomes increasingly expensive, potentially costing you thousands in additional interest. Your choice ultimately depends on whether you prioritize payment predictability or potential savings from rate stability.

Government-Backed vs Conventional Mortgages

Understanding High-Ratio Mortgages and CMHC Insurance

If your down payment falls below 20%, you’ll need mortgage insurance to qualify for a high-ratio mortgage. CMHC insurance is the most common option in Canada, and it protects the lender if you default, not you. The insurance premium gets added to your mortgage balance, so you finance the cost over your entire amortization period. On a $600,000 home with a $100,000 down payment (16.7%), mortgage insurance typically costs between $18,000 and $24,000, depending on your credit score and lender. That’s money you pay but never see again.

Many borrowers assume government programs like CMHC reduce their borrowing power, but the opposite is true-CMHC insurance actually expands your options by allowing you to purchase with a smaller down payment. The real cost arrives later when you renew. Lenders sometimes charge higher rates to insured mortgages, and you can’t drop the insurance until you’ve built 20% equity in your home.

Rate Premiums on Insured Mortgages

Real-time rate tracking across lenders shows insured mortgages currently run higher than conventional options, compounding the expense over time. This premium reflects the lender’s additional risk and the cost of insurance protection. On a $400,000 insured mortgage at a higher rate, you’ll pay more per year in interest alone. Over a 25-year amortization, that difference accumulates significantly.

Conventional Mortgages and the 20% Down Payment Advantage

Conventional mortgages require 20% down and eliminate mortgage insurance entirely, which appeals to borrowers who’ve saved aggressively or are purchasing properties worth $1.5 million or more. You qualify immediately for lower rates and avoid the insurance premium that inflates your mortgage balance. The approval timeline for conventional mortgages is typically faster because lenders face less risk-you’ve proven you can save a substantial amount before borrowing.

However, conventional mortgages aren’t always better. If you have $80,000 saved for a $500,000 home, insuring your mortgage at 16% down might cost less in total interest than waiting another two years to scrape together $100,000. Run the numbers on both paths before deciding.

Comparing Current Rates and Long-Term Costs

Current five-year fixed rates for conventional mortgages sit around 4.04% to 4.29%, while insured options average 4.39% to 4.72%. The gap matters most on large balances and longer amortizations. If you’re renewing soon, consider whether your equity position has shifted-once you hit 20% equity, refinancing into a conventional mortgage could save you thousands in reduced rates and eliminated insurance costs going forward.

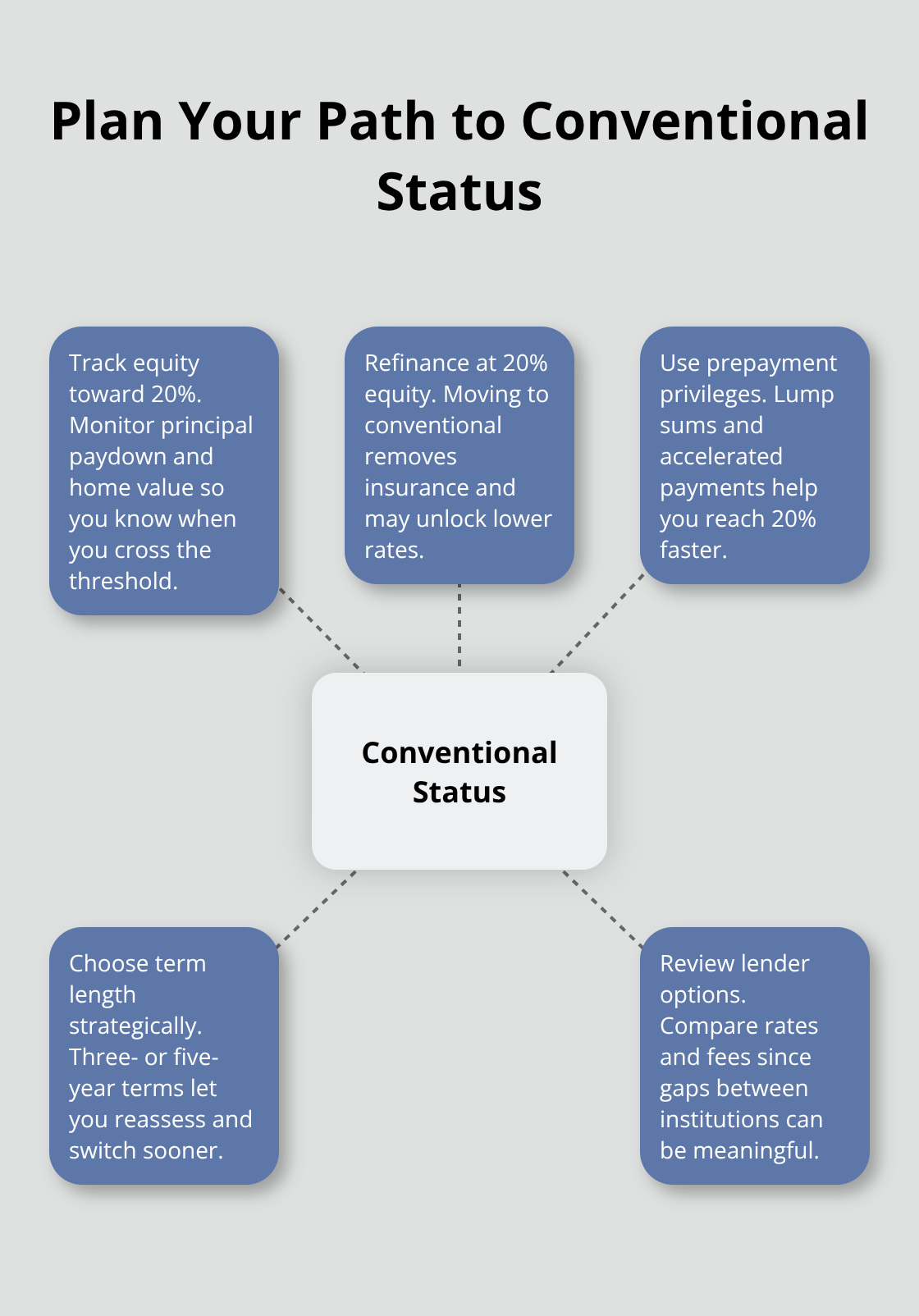

Planning Your Path to Conventional Status

Your mortgage choice today shapes your options at renewal. Borrowers with insured mortgages should track their equity buildup and plan to refinance into conventional status as soon as they reach 20% ownership. This transition eliminates the insurance premium and unlocks access to lower rates available only to conventional borrowers. Specialized mortgage products-open mortgages, closed mortgages, and reverse mortgages-offer additional flexibility for borrowers with different priorities and timelines.

Flexibility vs Penalties in Mortgage Repayment

Open Mortgages and the Cost of Freedom

Open mortgages sacrifice rate advantage for repayment freedom, allowing you to pay down your balance without penalties whenever you choose. This flexibility matters most if you expect a windfall, inheritance, or bonus within your term. The tradeoff is substantial: open mortgages typically carry rates 0.5% to 1% higher than closed options. On a $400,000 mortgage, that premium costs $2,000 to $4,000 annually in extra interest. Open mortgages make sense only if you’re certain you’ll use that flexibility to pay down principal faster, offsetting the higher rate through accelerated repayment. Most borrowers benefit more from closed mortgages paired with prepayment privileges that allow lump-sum payments without penalties, giving you flexibility at a lower cost.

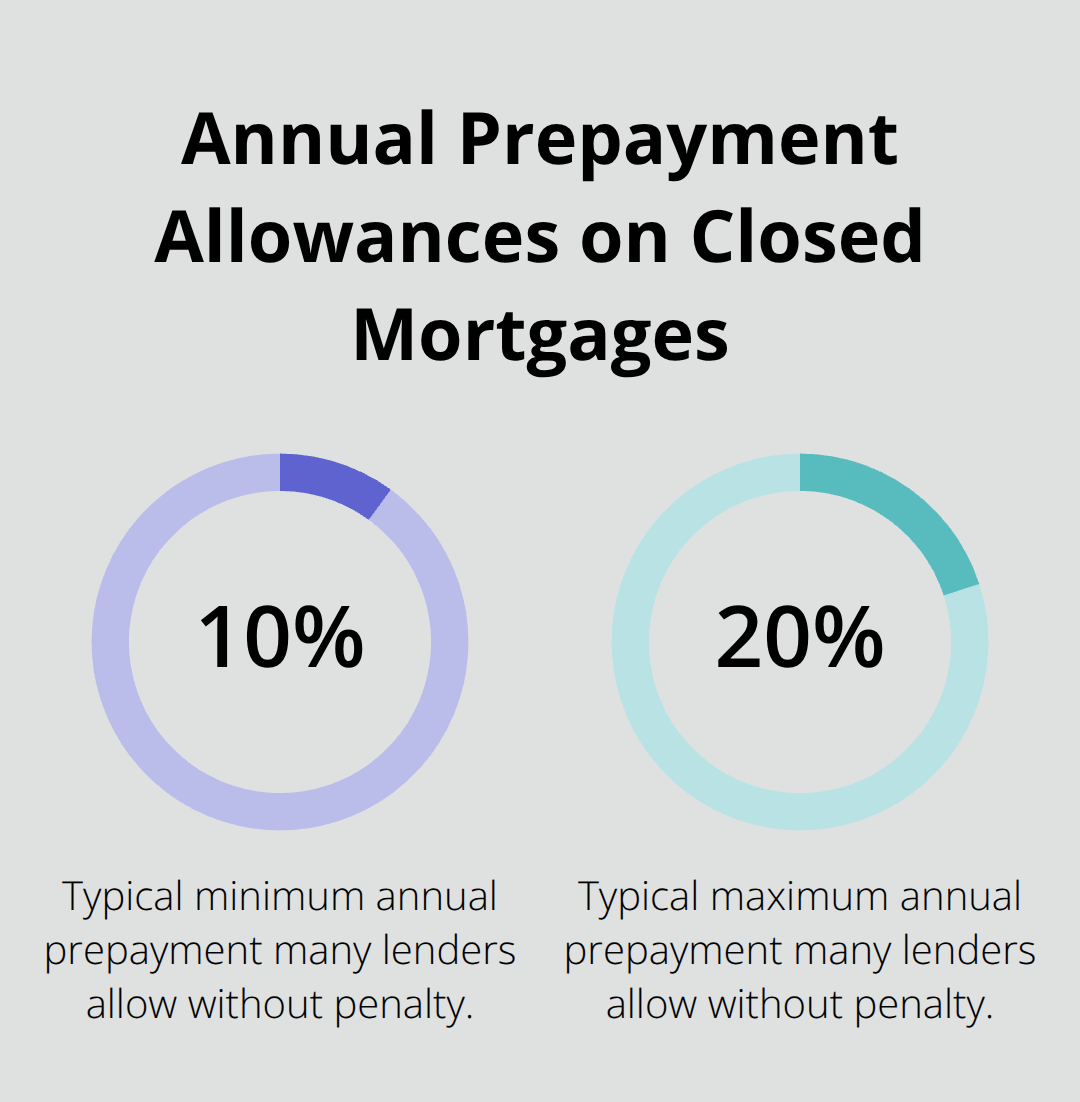

Closed Mortgages and Prepayment Penalties

Closed mortgages lock you into a rate and term with strict prepayment limits, but they offer substantially lower rates in exchange. Most lenders allow 10% to 20% annual prepayment without penalty, enough for most households to accelerate payoff if needed. Breaking a closed mortgage early triggers penalties that can run thousands of dollars, calculated either as three months’ interest or as an interest rate differential depending on whether rates have risen or fallen. If rates dropped since you signed, the interest rate differential penalty could exceed $10,000 on a large balance.

This is why locked-in rates feel comfortable only if you’re confident you won’t need to exit early. Convertible mortgages bridge this gap by letting you switch from open to closed at a lower rate during your term, offering a safety valve if circumstances change without the full penalty of breaking a closed mortgage outright.

Reverse Mortgages for Homeowners 55 and Older

Reverse mortgages serve homeowners aged 55 and older who want to unlock home equity without selling or downsizing. You borrow against your property’s appraised value up to roughly 55%, with interest accruing throughout the term. No payments are required until you move, sell, or pass away, making this product attractive for retirees managing fixed incomes. The catch is substantial: rates run 1% to 2% higher than conventional mortgages, and accruing interest means your debt grows every month you don’t pay. On a $600,000 home, borrowing $330,000 at 6% interest compounds to over $500,000 in debt by year ten if you make no payments. This erodes the inheritance your heirs receive and reduces your home’s equity dramatically. Reverse mortgages work best as a last resort for seniors with significant home equity, no other borrowing options, and no plans to leave the property to heirs. Before signing, compare the cost against alternatives like downsizing, home equity lines of credit on properties where you have at least 20% equity, or selling and renting instead.

Final Thoughts

Your mortgage choice depends on three core factors: your financial situation, your risk tolerance, and your timeline. A closed fixed-rate mortgage at current rates around 4.04% to 4.72% provides predictability if you have stable income and plan to stay in your home for five years or longer. A variable-rate mortgage starting near 3.35% could save thousands if you believe rates will stay low and can absorb payment increases, while CMHC insurance lets you buy now rather than wait years to accumulate 20% equity-though you’ll pay higher rates and insurance premiums until you refinance into conventional status.

Consult a mortgage advisor now, not at renewal, to model scenarios specific to your income, credit score, and property type. They will show you the actual dollar difference between options over your full amortization and help you compare rates across multiple lenders, since the gap between institutions often exceeds 0.25% (translating to thousands in savings on a $400,000 balance). Mortgage calculators help you compare payments across term lengths and rate types to validate your advisor’s recommendations.

Our mortgage options Canada comparison guide equips you with the knowledge to make informed decisions that shape your finances for decades. Take time to design your mortgage strategy now and prevent costly mistakes later.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment