Carrying multiple debts drains your finances and mental energy. The good news is that debt consolidation Canada options exist-and choosing the right one can save you thousands in interest while accelerating your payoff timeline.

We at Financial Canadian have reviewed the main strategies available to Canadian borrowers. This guide walks you through consolidation loans, balance transfers, debt management programs, and consumer proposals so you can match your situation to the best path forward.

Debt Consolidation Loans vs. Balance Transfer Credit Cards

How Consolidation Loans Work in Canada

A consolidation loan bundles multiple debts into one with a single monthly payment, typically at a lower interest rate than credit cards. In Canada, traditional banks like TD, RBC, BMO, and Scotiabank offer these loans to borrowers with stable income and reasonable credit. The process involves a credit check that temporarily impacts your score, but on-time payments rebuild it as your overall debt shrinks.

The real advantage emerges when you compare numbers. If you owe $15,000 across credit cards at 20% interest and pay minimums, you’ll spend roughly $27,563 in total interest over the repayment period. That same debt consolidated into a loan reduces total interest significantly-a difference of thousands of dollars. Your monthly payment also drops significantly because you spread repayment over a fixed term, usually 3 to 7 years.

However, consolidation loans work best if you stop accumulating new debt. Many borrowers refinance high-interest balances only to rebuild credit card debt afterward, ending up worse off than before.

Balance Transfer Credit Cards: The Promotional Window

Balance transfer credit cards offer a promotional window where you pay 0% interest on transferred balances. This strategy makes sense if you can pay down the principal aggressively during that window and have the discipline to avoid new purchases.

The catch is brutal: once the promotional period ends, the remaining balance faces standard interest rates of 19% to 22%. If you transfer $10,000 and pay $833 monthly for 12 months, you clear the debt before rates spike. But transfer $10,000 and pay only $500 monthly, and you’ll owe $4,000 when the 0% period ends-then interest accelerates the debt growth.

Balance transfers also trigger a 1% to 3% upfront fee, so a $10,000 transfer costs $100 to $300 immediately. This fee reduces your available credit and adds to your total cost.

Which Option Wins for Most Canadians

Consolidation loans win for most Canadians because they lock in a fixed rate for the entire term, eliminate the pressure of a ticking promotional clock, and simplify budgeting. Balance transfers suit only those with strong payment discipline and the ability to clear debt within the promotional window.

Understanding these two paths sets the stage for exploring more specialized options. Debt management programs and consumer proposals offer additional routes for borrowers who face barriers to traditional loans or need legal protection from creditors.

Debt Management Programs and Consumer Proposals

How Debt Management Programs Work

Debt management programs offer a path forward for borrowers who cannot qualify for a consolidation loan or whose debt exceeds what traditional lenders will accept. A non-profit credit counsellor negotiates directly with your creditors to reduce or freeze interest on unsecured debts like credit cards and personal loans. You make one monthly payment to the counselling agency, which then distributes funds to creditors according to a repayment plan that typically takes 24 to 48 months to complete.

The real appeal lies in interest relief. Many creditors agree to stop charging interest entirely while you remain enrolled in the program, meaning every dollar you pay attacks principal instead of feeding the interest machine. This approach works best if you owe between $5,000 and $15,000 across multiple creditors and have stable income to sustain monthly payments.

The limitations matter. Not all creditors participate, and payday loans, tax debts, and student loans typically fall outside these programs. You must surrender your credit cards and close accounts, which temporarily impacts your credit score, but the damage remains far less severe than bankruptcy.

Consumer Proposals: A Legal Alternative

A consumer proposal is a legal process administered by a Licensed Insolvency Trustee under the Bankruptcy and Insolvency Act. You formally offer to repay a portion of your unsecured debts through fixed monthly payments spread over up to five years. Creditors vote on the proposal, and once accepted, it becomes legally binding and stops all collection actions immediately.

The government’s Office of the Superintendent of Bankruptcy reported 24,043 consumer proposals filed in Q3 2023, making this path increasingly common for Canadians facing serious debt. You can settle debts for as little as 30 to 50 percent of what you owe, and interest charges stop completely. Consumer proposals cover most unsecured debts but exclude mortgages, secured loans, and child support.

The credit impact is real-you receive an R7 rating on your credit report-but this recovers faster than bankruptcy’s R9 rating and disappears from your credit report three years after completion.

Choosing Between These Two Paths

Try a debt management program if you want to avoid legal proceedings and can stick to a structured repayment schedule with creditor cooperation. Try a consumer proposal if debts exceed $10,000, you cannot qualify for a loan, creditors refuse to negotiate, or you need immediate legal protection from wage garnishments and collection calls.

Both paths require working with a credit counsellor or Licensed Insolvency Trustee to evaluate which fits your income, assets, and debt load. Your specific debt types and financial situation determine which option makes sense-and that’s where the next section becomes critical, as different debts respond differently to each consolidation strategy.

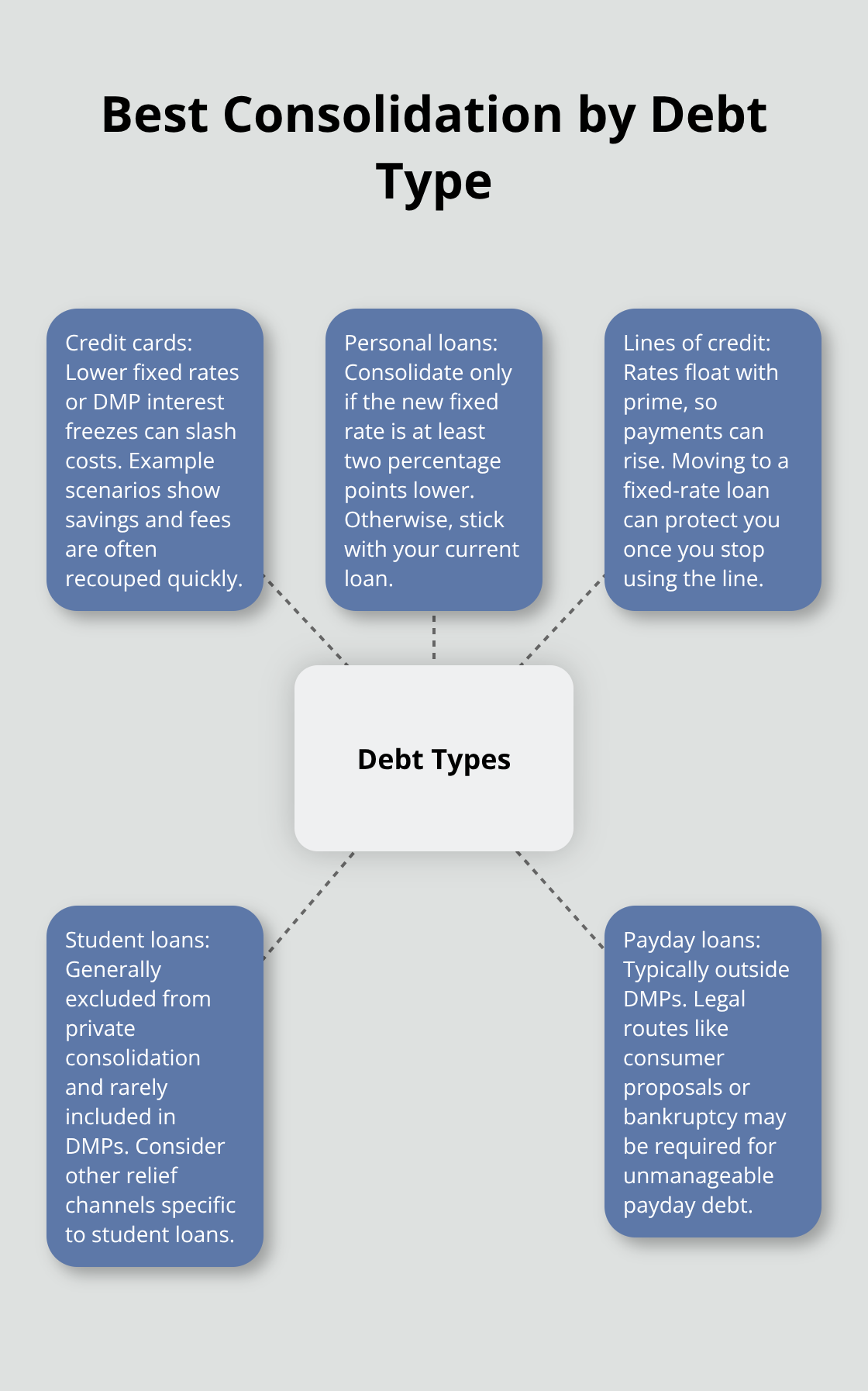

Consolidation Strategies for Different Debt Types

Credit Card Debt: The Consolidation Sweet Spot

Credit card debt consolidates beautifully because it responds directly to lower interest rates. If you carry $8,000 across three cards at 19.99% interest, consolidating into a loan at 8% cuts your total interest cost by roughly 60%. The math is straightforward: consolidation works when the new rate undercuts your current rate significantly enough to justify any fees involved. A consolidation loan typically costs $200 to $500 in origination fees, but that expense vanishes within the first few months of interest savings on high-rate credit card balances.

Credit card debt also consolidates well through debt management programs because creditors frequently accept interest freezes on card balances, turning your $8,000 debt into a fixed repayment with zero additional interest charges. The key is acting before credit cards reach maximum limits-consolidation becomes harder once you’ve maxed out multiple cards and your credit score has tanked.

Personal Loans and Lines of Credit: A Selective Approach

Personal loans already carry fixed rates between 7% and 15%, so consolidating them into a new loan only makes sense if the new rate drops at least two percentage points below your current rate. Lines of credit present a trickier situation because their interest rates fluctuate with prime rate changes. If prime rates rise, your line of credit payments climb automatically, which means consolidating into a fixed-rate loan actually protects you from future payment shocks.

However, most people consolidate lines of credit too late, after already carrying balances for years. The practical move is to consolidate a line of credit the moment you stop using it for new purchases-treat it as a completed debt rather than an ongoing credit source.

Student Loans and Payday Loans: Limited Consolidation Options

Student loans and payday loans sit outside standard consolidation options for solid reasons. Federal and provincial student loans cannot be included in private consolidation loans, and including them in a debt management program typically fails because student loan providers rarely participate. Payday loans also fall outside debt management programs, making consumer proposals or bankruptcy the only legal routes for borrowers drowning in payday debt.

If you carry $3,000 in payday loans alongside credit card debt, consolidate the credit cards through a loan or program first, then address payday loans separately through a Licensed Insolvency Trustee. Payday loan debt demands immediate action because interest rates are capped at $14 per $100 borrowed-waiting costs you hundreds monthly. The Financial Consumer Agency of Canada warns that debt settlement companies often target payday loan borrowers with false promises, so avoid any service charging upfront fees before negotiating with lenders.

Final Thoughts

Your debt profile determines which debt consolidation Canada option works best for your situation. If you carry high-interest credit card balances and have stable income with reasonable credit, a consolidation loan from TD, RBC, BMO, or Scotiabank delivers the fastest payoff and lowest total cost. If your credit score has suffered or you owe more than $10,000 across multiple creditors, a debt management program through a non-profit counsellor offers interest relief without legal proceedings. If creditors refuse to negotiate and debts feel unmanageable, a consumer proposal provides legal protection and potential debt reduction of up to 50 percent.

Add up all unsecured debts, note the interest rates on each, and estimate how long you would take to pay everything off at current rates. Then compare that timeline against what a consolidation loan, debt management program, or consumer proposal would cost. The difference often shocks borrowers-thousands of dollars in interest savings appear when you move from minimum payments to a structured repayment plan.

Contact a Licensed Insolvency Trustee or certified credit counsellor for a free assessment of your debt situation. They review your specific situation, separate myths from facts, and recommend which option fits your income and assets. Many agencies offer confidential consultations at no cost, and this conversation clarifies whether you need a loan, a program, or legal protection.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment