An instant cash advance in Canada can bridge the gap when unexpected expenses hit hard. We at Financial Canadian know that emergency funds aren’t always sitting in your account when you need them most.

This guide walks you through how instant cash advances work, how they stack up against other borrowing options, and the real costs involved. We’ll help you decide if this option makes sense for your situation.

How Instant Cash Advances Work in Canada

Instant cash advances reach your account fast because most lenders skip the traditional credit check. Instead, they verify your income directly through your bank account, which takes minutes rather than days. The application itself is paperless and entirely online-you answer basic questions about your income, employment status, and banking details, then submit your information through a secure portal. Most providers deliver a decision within minutes, and funds hit your account via bank transfer or Interac e-Transfer shortly after you sign the contract. Some e-Transfers arrive in as little as one minute, though your bank may add a slight delay depending on their processing speed.

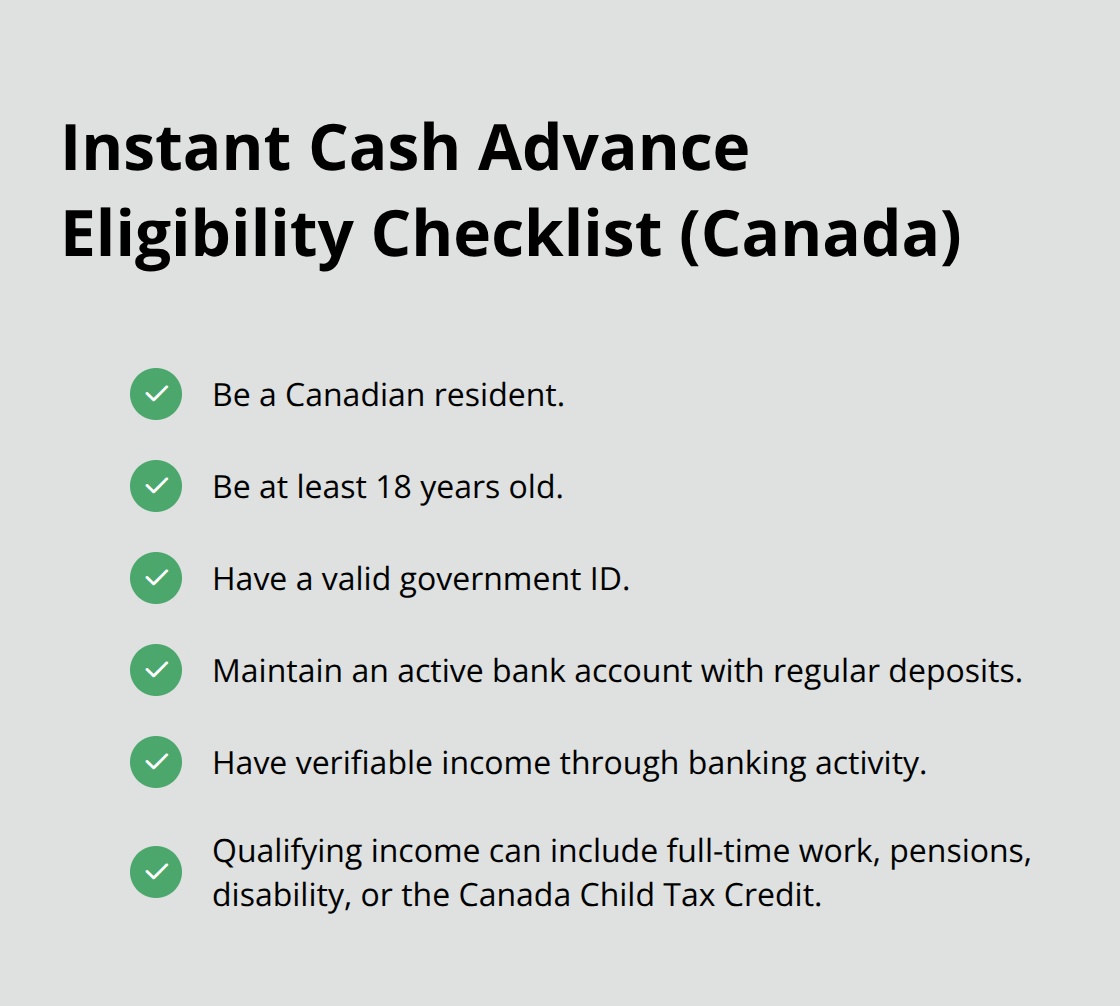

Who Qualifies for an Instant Cash Advance

Eligibility remains straightforward because lenders focus on income rather than credit history. You need to be a Canadian resident, at least 18 years old, with a valid government ID and an active bank account that receives regular deposits. Employment types that qualify include full-time work, pensions, disability payments, and the Canada Child Tax Credit.

If you’ve been employed for less than two months, most lenders will ask you to wait until you hit the two-month mark before applying. Providers verify income through your banking activity, meaning a damaged credit score won’t automatically disqualify you. This income-first approach is why approval rates remain high-lenders care about whether you’ll have money to repay, not your past borrowing mistakes.

The Speed-Versus-Size Trade-Off

The amount you can borrow directly impacts how fast you receive the money. Cash advance apps typically offer smaller limits-Bree maxes out at $750 while KOHO covers up to $250-but deliver funds within minutes to an hour. Payday-style lenders push higher amounts up to $1,500 but still complete the entire process from application to funding in under two hours. The trade-off is real: larger advances often come with higher fees and stricter repayment terms. A $750 advance from Bree costs a flat $2.99 monthly membership with zero interest, while a $1,500 payday loan might charge $14 per $100 borrowed depending on your province and loan term. Before you apply anywhere, use the lender’s instant loan calculator to estimate your total repayment cost, then decide whether the speed justifies the expense.

What Happens After Approval

Once you receive approval, the lender transfers funds to your bank account within minutes (though some banks or credit unions may delay slightly). You’ll need to verify your bank account details and sign the contract electronically-no paperwork or in-person visits required. The automated process means you avoid queues and lengthy approval meetings. Most lenders use bank-level encryption to protect your personal information, so your data stays secure throughout the transaction. After funds arrive, you’ll have a set repayment date based on your loan term, typically ranging from 14 to 62 days depending on the lender and your province.

Understanding how these advances work sets the stage for comparing them to other borrowing options available to Canadian consumers. Each alternative carries different costs, approval timelines, and repayment structures that may suit your situation better than an instant cash advance.

Comparing Instant Cash Advances to Other Borrowing Options

Personal Loans: Lower Cost, Longer Wait

Personal loans from banks and credit unions offer lower costs but demand patience and a solid credit score. A typical personal loan from a credit union carries an APR around 28 percent, compared to cash advance apps charging zero percent interest or payday lenders hitting 365 percent APR on 14-day loans.

The catch is approval time-personal loans take five to ten business days, while instant cash advances fund within minutes. If your emergency can wait a week, a personal loan saves you hundreds in fees and interest. Most banks require a minimum credit score around 650, which eliminates anyone recovering from financial trouble. Instant cash advances ignore your credit history entirely, making them the only option if your score has taken a hit.

The real question isn’t which option costs less in isolation-it’s which option you can actually access right now. If you have time and decent credit, personal loans win decisively on cost. If you need money today and your credit is damaged, instant cash advances become your realistic choice.

Credit Card Advances and Payday Loans: The Expensive Alternatives

Credit card cash advances and payday loans represent the other end of the spectrum, and both cost significantly more than instant cash advance apps. Credit card cash advances typically charge 20 to 30 percent APR plus an upfront fee of two to five percent, meaning a $500 advance costs $10 to $25 immediately plus daily interest charges starting that same day. Payday lenders charge $14 per $100 borrowed for loans in the 42 to 62 day range, translating to an 82.4 percent APR for a 62-day loan-brutal but less predatory than their 14-day offerings at 365 percent APR.

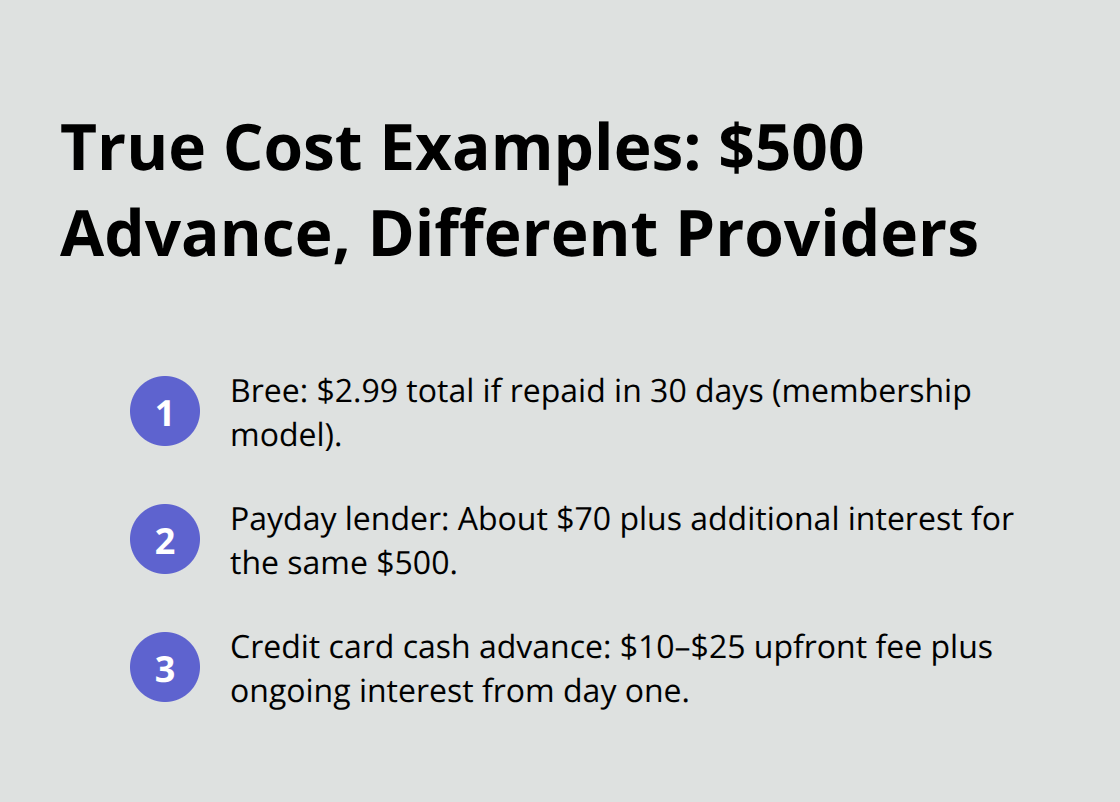

Instant cash advance apps like Bree undercut both options with zero percent interest, a flat $2.99 monthly membership, and 90 days to repay up to $750. The math is straightforward: a $500 advance from Bree costs $2.99 total if repaid within 30 days, while the same amount from a payday lender costs $70 plus interest, and a credit card advance costs $10 to $25 plus ongoing interest.

Why Payday Loans Create Debt Cycles

Payday loans trap borrowers in cycles because the 365 percent APR on 14-day terms forces renewal-you can’t afford to repay the full amount when it’s due, so you borrow again, and debt multiplies. Cash advance apps structure repayment differently, allowing 90-day terms that match actual cash flow patterns. If you’re choosing between payday loans and instant cash advances, the decision should be automatic: apps like Bree cost a fraction of what payday lenders charge and give you three months instead of two weeks to repay.

Understanding these comparisons reveals which borrowing option fits your timeline and financial situation. The next section examines the risks and costs that accompany instant cash advances, helping you weigh whether this solution aligns with your emergency needs.

Risks and Costs Associated with Instant Cash Advances

Understanding the True Cost Beyond Interest Rates

Instant cash advance apps advertise zero percent interest, but that headline masks the full picture of what you’ll actually pay. Bree charges a $2.99 monthly membership fee, KOHO requires account maintenance costs, and Wagepay adds an 8 percent flat fee plus 24 percent APR on top of its $1,500 advance limit. The math shifts dramatically depending on loan size and repayment speed. A $500 advance from Bree repaid in 30 days costs only $2.99 total, making it genuinely cheap. That same $500 from Wagepay costs $40 upfront plus interest charges that accumulate daily, pushing total cost toward $70 to $90 over two weeks.

The supposed zero percent interest becomes misleading when monthly fees and subscription costs enter the equation.

Before you apply anywhere, calculate your exact repayment timeline and compare total cost across providers rather than fixating on APR percentages. Most cash advance apps won’t damage your credit score since they don’t report payment activity to credit bureaus, which means on-time repayment builds nothing and missed payments harm nothing-a genuine advantage over traditional loans. However, Nyble deliberately reports payments to credit bureaus as a credit-building feature, so your choice of lender determines whether this advance helps or ignores your credit history entirely.

When Instant Cash Advances Become a Recurring Problem

The real danger with instant cash advances emerges when you treat them as recurring solutions rather than genuine emergencies. Users doubled their borrowing frequency within the first year of tracked usage, creating a pattern where you perpetually pay fees and repayment obligations that consume money you should direct toward actual expenses. A borrower who takes a $500 advance every month pays $2.99 to $35 monthly depending on the provider, which adds $36 to $420 annually-money that compounds into genuine financial stress. The debt trap potential differs sharply from payday loans because repayment terms stretch across 90 days instead of 14, but the trap still exists if you habitually renew advances before the previous one clears.

If you find yourself considering a second advance before the first is repaid, stop immediately and contact a nonprofit credit counseling service like Credit Canada to assess your budget. These services work free or low-cost and help identify spending leaks that make emergencies feel constant. The critical distinction is this: instant cash advances solve genuine one-time emergencies, but they destroy finances when used as a crutch for chronic cash shortfalls.

Building Protection Against Future Emergencies

Use this option once, repay it fully, then build an emergency fund so the next crisis doesn’t force you to borrow at all. Even small contributions-$25 to $50 monthly-accumulate into a buffer that prevents you from needing advances repeatedly. Start by tracking your spending for one month to identify where money actually goes, then redirect discretionary expenses toward savings. Most Canadians find $100 to $200 monthly in unnecessary subscriptions, dining out, or impulse purchases that could fund an emergency account instead. The goal isn’t perfection; it’s progress toward financial stability that makes instant cash advances unnecessary.

Final Thoughts

An instant cash advance in Canada makes sense only when you face a genuine emergency and need funds within hours, not days. If your car breaks down, a medical bill arrives unexpectedly, or you face an eviction notice, cash advance apps like Bree deliver money faster than any traditional lender. The zero percent interest and flexible 90-day repayment terms beat payday loans decisively, and speed matters when your situation demands immediate action.

Before applying for any advance, contact your employer about an advance on your next paycheck, reach out to family or friends for a short-term loan, or check whether your bank offers overdraft protection. If you’re facing housing insecurity, food shortages, or utility shutoffs, local community resources like rent banks and food banks provide immediate help without debt. These options cost nothing and don’t create repayment obligations that strain your budget further, making them worth exploring first.

If an instant cash advance is genuinely your only option, borrow only what you absolutely need rather than the maximum available, set a specific repayment date and treat it like a non-negotiable bill, and build an emergency fund immediately after repayment so the next crisis doesn’t force you to borrow again. Understanding your borrowing options empowers better financial decisions when life happens unpredictably. We at Financial Canadian believe that strategic use of instant cash advances followed by financial planning creates the foundation for long-term stability.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment