When unexpected expenses hit, many Canadians turn to payday loans for quick cash. These short-term loans can provide funds within hours, but they come with steep costs that trap borrowers in cycles of debt.

At Financial Canadian, we break down how emergency payday cash works in Canada, what alternatives exist, and when these loans actually make sense for your situation.

How Emergency Payday Loans Work in Canada

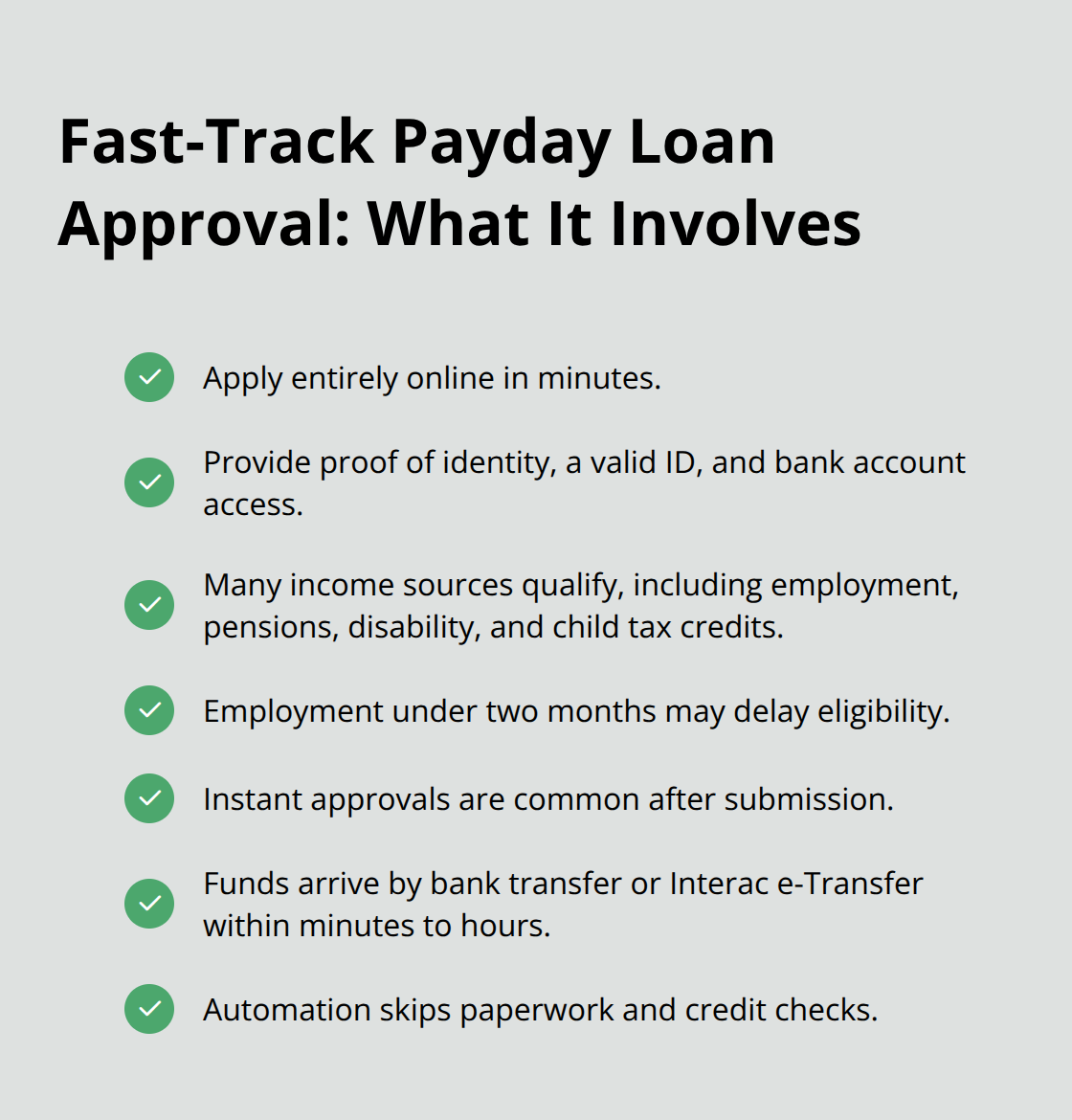

The Application and Approval Process

Getting approved for a payday loan in Canada takes minutes, not days. The application happens entirely online through your computer or phone, and you provide proof of identity, a valid ID, and access to a bank account. Lenders accept various income sources including full-time employment, pensions, disability benefits, and child tax credits. If you’ve been employed for less than two months, you must wait until you reach that threshold. Once you submit your application, approval happens instantly in most cases, with funds arriving via bank transfer or Interac e-Transfer within minutes to a few hours.

The speed comes from automation that skips the paperwork and credit checks entirely.

The True Cost of Borrowing

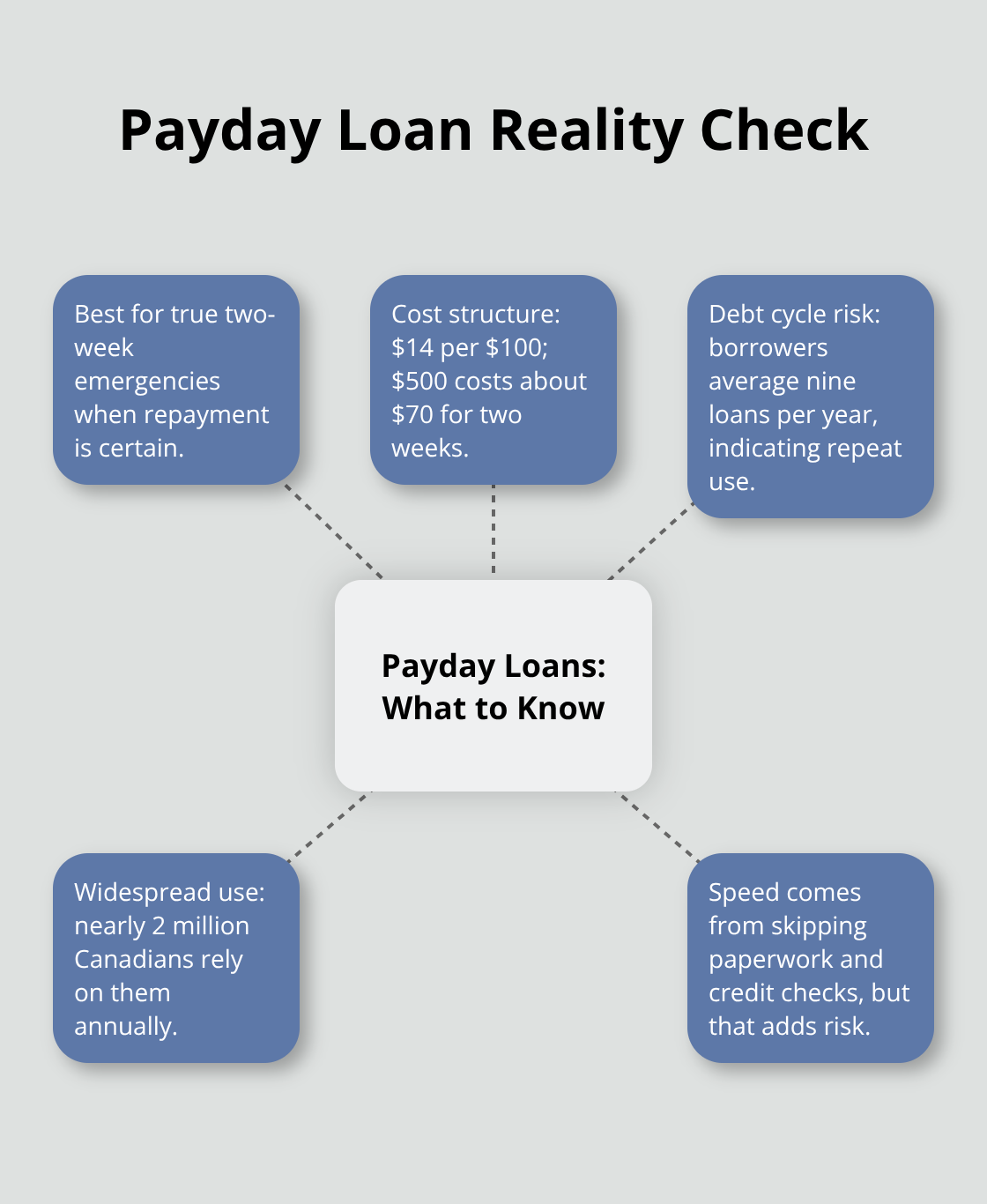

This convenience carries a steep price tag. Payday loans use a fixed fee structure rather than traditional interest rates, charging $14 per $100 borrowed for loans up to 62 days. A $300 loan for 14 days costs $42, meaning you repay $342 total. This translates to an annual percentage rate of 365% for a 14-day loan and 82.4% for a 62-day loan, making payday loans among the most expensive borrowing options available. These rates dwarf personal lines of credit, which typically charge between 7% and 21% annually depending on your credit score.

Who Actually Qualifies

Payday lenders in Canada approve most applicants, even those with poor credit or no credit history. This accessibility explains their popularity during emergencies, but it masks a dangerous reality. Lenders operate in eight provinces including Ontario, British Columbia, Alberta, and Saskatchewan, though coverage extends to remote areas where traditional banks don’t reach. The catch: approval doesn’t mean you should borrow. The high-cost structure makes payday loans suitable only for genuine emergencies lasting two weeks or less. If you need $500 for a car repair and can repay it in two weeks, the $70 fee might be justifiable. But if you use payday loans to cover regular expenses or ongoing shortfalls, you enter debt trap territory.

The Debt Cycle Reality

Studies show borrowers take out an average of nine payday loans per year, suggesting that initial loans rarely solve underlying financial problems. The speed and ease of access work against you here because they remove the friction that might otherwise force you to find cheaper alternatives or address root causes of financial instability. This pattern reveals why payday loans function as a symptom of deeper money problems rather than a solution.

Understanding this reality matters as you weigh whether a payday loan fits your emergency or whether alternatives deserve serious consideration.

The Real Trade-Off Between Speed and Cost

Speed Solves Immediate Crises

Payday loans offer genuine speed that traditional lenders cannot match. You receive approval in minutes, funds arrive within hours, and you solve an immediate crisis without visiting a bank or waiting days for processing. This matters when your car breaks down and you need $400 for repairs to keep your job, or when an unexpected medical bill arrives before your next paycheck. The accessibility also extends to people with damaged credit histories, since payday lenders skip credit checks entirely and focus only on income verification. For a two-week emergency, the convenience justifies the cost in specific situations.

The Hidden Cost of Easy Access

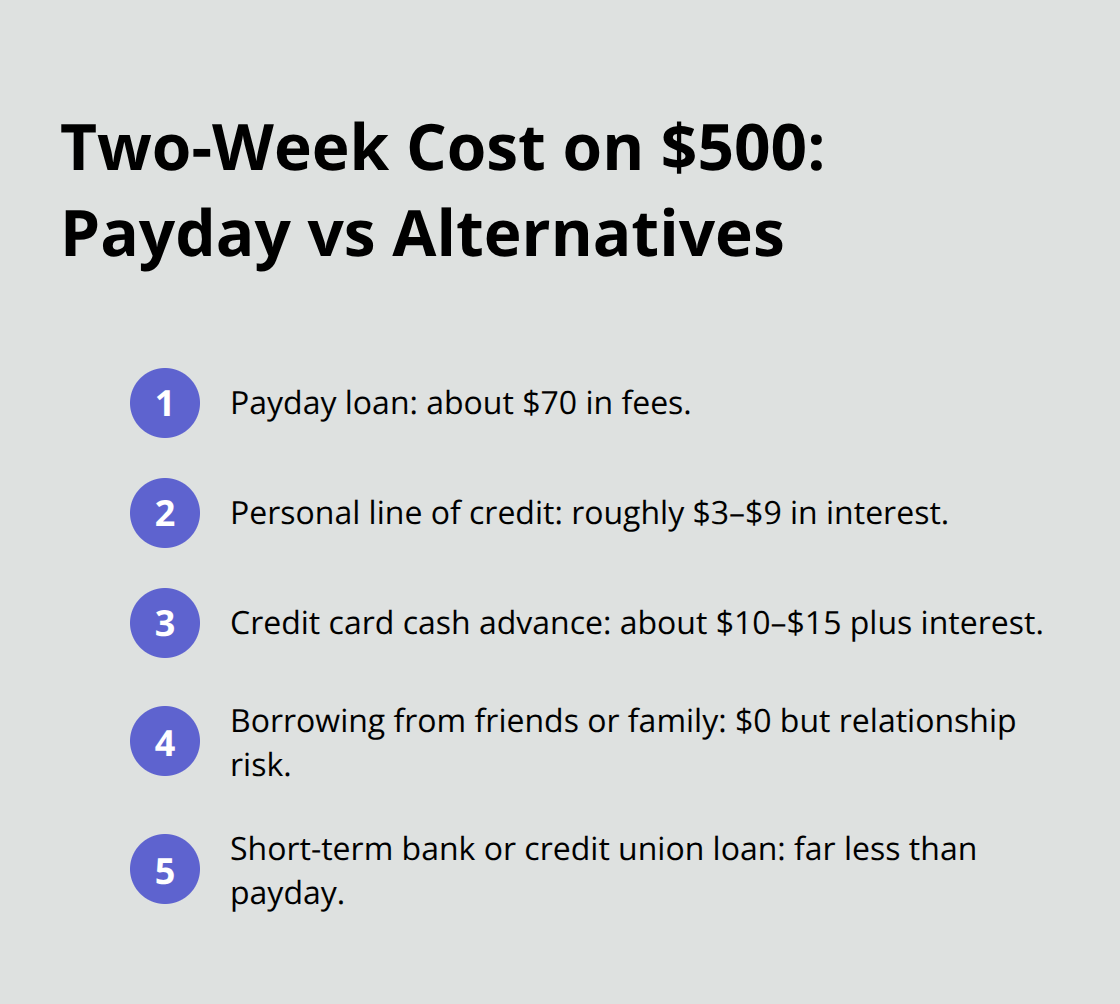

This speed becomes your worst enemy if you treat payday loans as flexible borrowing tools rather than emergency-only solutions. The ease of approval masks the brutal economics underneath. A $500 payday loan costs you $70 for two weeks, but if you cannot repay it and roll it over, the costs compound rapidly. Nearly 2 million Canadians use payday loans each year, indicating that initial loans rarely solve problems and instead create rolling debt cycles. Each rollover extends your repayment period and adds fresh fees, transforming a $70 emergency cost into $200 or $300 in total charges.

How Alternatives Stack Up

The comparison to alternatives reveals why payday loans fail most borrowers. A personal line of credit charges 7% to 21% annually, which translates to roughly $3 to $9 in interest on a $500 loan over two weeks. Credit card cash advances charge similar rates plus a one-time fee (typically 2% to 3%), costing around $10 to $15 on $500. Borrowing from friends or family costs nothing but requires relationships you can afford to strain.

Even a short-term personal loan from your bank or a credit union charges far less than payday loans.

When the Math Fails

The mathematics are straightforward: payday loans work only when you have no other option and can repay within two weeks. If you need longer than two weeks, the 365% APR becomes indefensible compared to alternatives. If you lack access to other borrowing options, that signals a deeper problem that payday loans will worsen rather than solve. This reality makes understanding your actual alternatives essential before you commit to high-cost borrowing.

Better Borrowing Options Than Payday Loans

Personal Lines of Credit Beat Payday Loans on Cost

Personal lines of credit outperform payday loans for most emergency situations because they charge a fraction of the cost while offering flexible repayment terms. Personal loan interest rates in Canada typically range from 6% to 35% APR, depending on factors such as credit history and income, which means a $500 emergency costs significantly less in interest over two weeks rather than the $70 you’d pay with a payday loan. Most banks and credit unions in Canada offer these products, and many approve applications within one to three business days. If you already have an existing line of credit with your bank, you can access funds immediately without reapplying. The catch is that you need reasonably decent credit to qualify, which excludes people with severely damaged credit histories. However, if you have any credit history at all, a line of credit deserves serious consideration before you look at payday loans.

Credit Card Cash Advances Offer Speed and Lower Costs

Credit card cash advances present another legitimate alternative, though they carry fees and interest charges. A cash advance costs roughly $10 to $15 upfront plus interest, making it substantially cheaper than payday loans for two-week emergencies. The advantage here is speed: if you already have a credit card, you can access cash within hours at an ATM or through your bank. The disadvantage is that cash advances count as new debt that affects your credit utilization ratio and credit score. Use this option only if your credit card has available room and you can repay quickly.

Borrowing from Friends or Family Requires Honesty

Borrowing from friends or family costs nothing financially but requires honest conversations about repayment timelines and amounts. This option works best when the sum is modest (under $500) and you can return the money within two weeks, preserving the relationship. The psychological advantage is real: knowing you owe money to someone you see regularly creates powerful motivation to repay on schedule, unlike payday loans where you owe an anonymous lender. The disadvantage is that money between loved ones often strains relationships, even when both parties intend to keep things professional. Before you ask someone for help, have a clear repayment plan in writing and stick to it religiously. If borrowing from family feels impossible or inappropriate, that’s a signal you should explore credit card cash advances or personal lines of credit before considering payday loans.

Why Most Canadians Have Better Options Available

The reality is that payday loans trap people who lack access to better options, but most Canadians have at least one alternative available. Spending an extra day or two exploring these options costs nothing and saves you hundreds of dollars in fees and interest charges. A personal line of credit, a credit card cash advance, or a loan from someone you trust all cost substantially less than the 365% APR that payday lenders charge.

Final Thoughts

Payday loans solve genuine emergencies when you need cash within hours and can repay within two weeks. If your car breaks down, you face an unexpected medical bill, or your rent is due before your next paycheck, emergency payday cash in Canada provides speed that traditional lenders cannot match. The approval happens in minutes, funds arrive within hours, and you avoid the multi-day waiting period that banks require. This speed matters when the alternative is missing work, losing your housing, or facing serious consequences.

However, speed comes at a brutal cost. The 365% APR for a 14-day loan makes payday borrowing the most expensive option available, and the ease of access creates dangerous temptation to use these loans repeatedly. Nearly 2 million Canadians use payday loans annually, and most take out multiple loans per year, suggesting that initial borrowing rarely solves underlying problems. Instead, it creates rolling debt cycles where fees compound and borrowers find themselves trapped.

Before you apply for a payday loan, exhaust your alternatives. A personal line of credit costs a fraction of what payday lenders charge and offers flexible repayment terms. A credit card cash advance costs roughly $10 to $15 upfront plus interest, making it substantially cheaper for two-week emergencies. Borrowing from friends or family costs nothing financially and creates powerful motivation to repay on schedule. The hard truth is that payday loans work only when you have genuinely exhausted every other option and can repay within two weeks. If you need longer than two weeks, the mathematics become indefensible. If you lack access to other borrowing options, that signals a deeper financial problem that payday loans will worsen rather than solve. We at Financial Canadian help you explore your actual borrowing options before emergencies hit, so you understand which tools fit which situations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment