Finding the right personal loan online in Canada means comparing more than just interest rates. We at Financial Canadian know that borrowers need to evaluate fees, terms, customer service, and lender credibility all at once.

This guide walks you through the exact steps to compare lenders remotely and apply safely.

What Actually Matters When Comparing Online Loan Rates

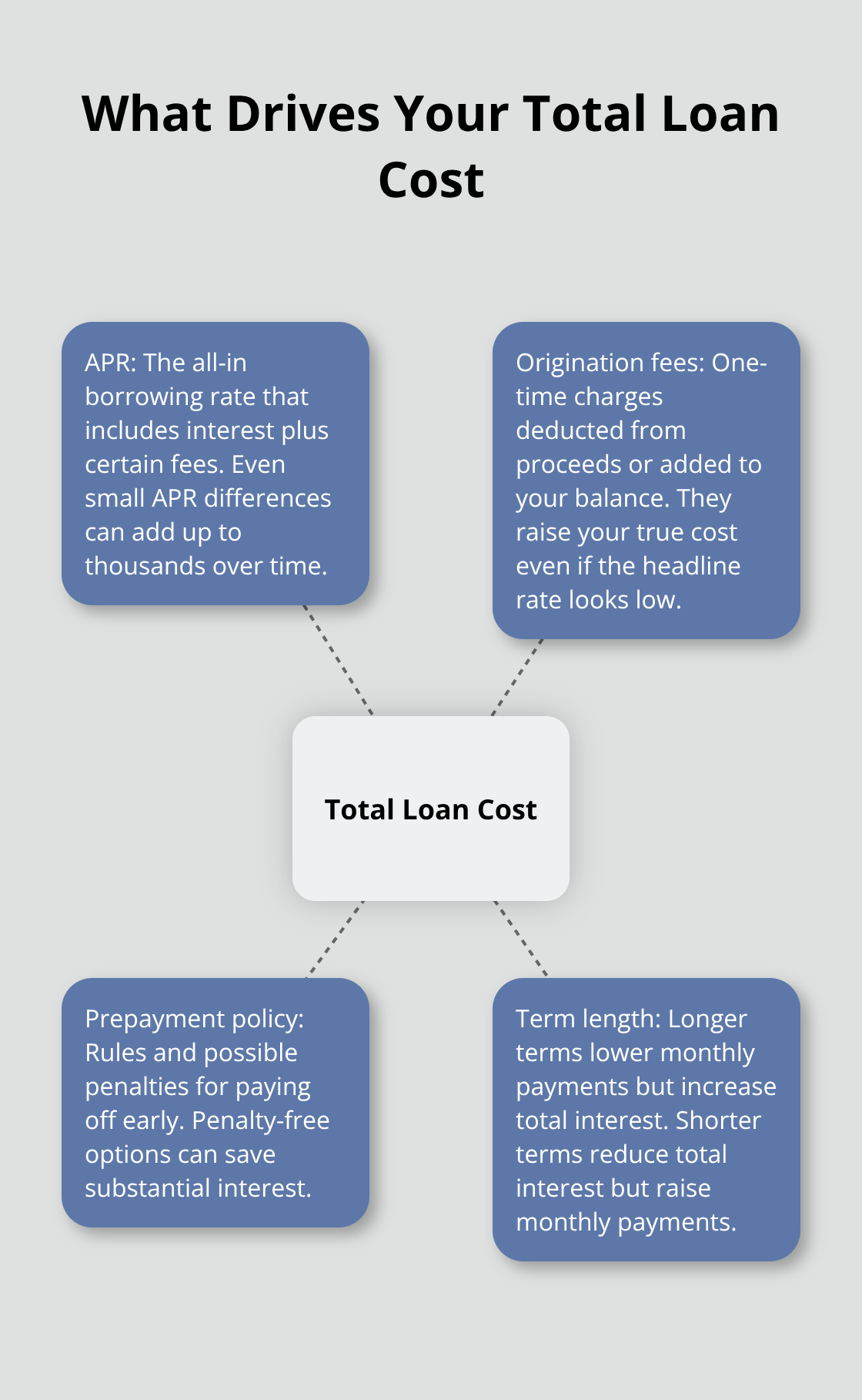

Focus on APR, Not the Advertised Rate

The interest rate you see advertised is rarely the full story. When you compare personal loans online in Canada, you need to focus on the Annual Percentage Rate, or APR, because it includes both the interest rate and origination fees rolled into one number. According to Ratehub.ca, personal loan APRs in Canada typically range from 6% to 35% depending on your credit, income, and which lender you choose. Major banks advertise starting rates around 6% to 10% APR for well-qualified borrowers, but that’s the floor-not what most people actually receive.

The difference between a 7% APR and a 12% APR on a $15,000 loan over five years costs you roughly $1,800 more in total interest. This makes comparing APRs across multiple lenders non-negotiable. Try getting prequalifications from at least three to five lenders without submitting a hard credit inquiry, since soft checks don’t impact your credit score. This approach lets you see actual rate estimates in minutes and compare them side by side.

Choose Between Fixed and Variable Rates

Fixed-rate loans lock in your monthly payment for the entire term, which makes budgeting predictable. Variable-rate loans track the Bank of Canada’s target rate and can fluctuate, which means your payment could increase if rates rise. The BoC held the overnight rate at 2.25% in March 2026, so variable rates are currently stable, but that could change. If you prefer certainty, fixed-rate loans eliminate the guessing game.

Uncover Hidden Fees and Prepayment Penalties

Origination fees are where lenders hide real costs. Lenders typically charge between 0.5% to 8% of your total loan amount and can be deducted from what you receive or added to your balance. On a $20,000 loan with a 5% origination fee, you pay $1,000 upfront-money you never see. Always ask lenders to provide a written quote showing the exact APR, origination fee, monthly payment, and total interest you’ll pay over the loan term. When you compare any online lender, look beyond interest rates at the complete cost picture, including administration fees and early repayment penalties.

Prepayment penalties are another trap. Some lenders allow you to pay off your loan early without penalties, while others charge you to do so. If you think you might pay off the loan faster (say, from a bonus or inheritance), confirm that the lender allows penalty-free prepayment.

Calculate Total Cost Across Different Term Lengths

Loan terms in Canada typically run from 6 months to 5 years, though some lenders offer up to 7 years. Longer terms lower your monthly payment but increase total interest significantly. A $10,000 loan at 10% APR costs you $1,058 in interest over three years but $2,748 over seven years. You must calculate the total cost, not just the monthly payment, before you commit.

Compare the complete package: APR, origination fee, prepayment options, and term length. This approach gives you the true cost of borrowing and sets you up to evaluate lender reputation and approval speed in the next section.

Key Factors to Assess When Choosing an Online Lender

Verify Lender Reputation Through Independent Sources

Lender reputation matters far more than most borrowers realize, and checking it properly takes only minutes. Read verified customer reviews on independent platforms like Trustpilot or Google Reviews rather than relying on testimonials on the lender’s own website. Look for patterns in complaints-if multiple people mention slow funding, hidden fees, or poor customer service, that’s a red flag. Forbes Advisor Canada profiles major banks like TD Bank, CIBC, RBC, Scotiabank, and BMO alongside non-bank lenders like Fairstone and easyfinancial, giving you vetted options with established track records. Avoid lenders with no online presence or regulatory oversight, as these are often predatory operators charging rates above 25% with aggressive collection practices.

Evaluate Approval Speed and Documentation Needs

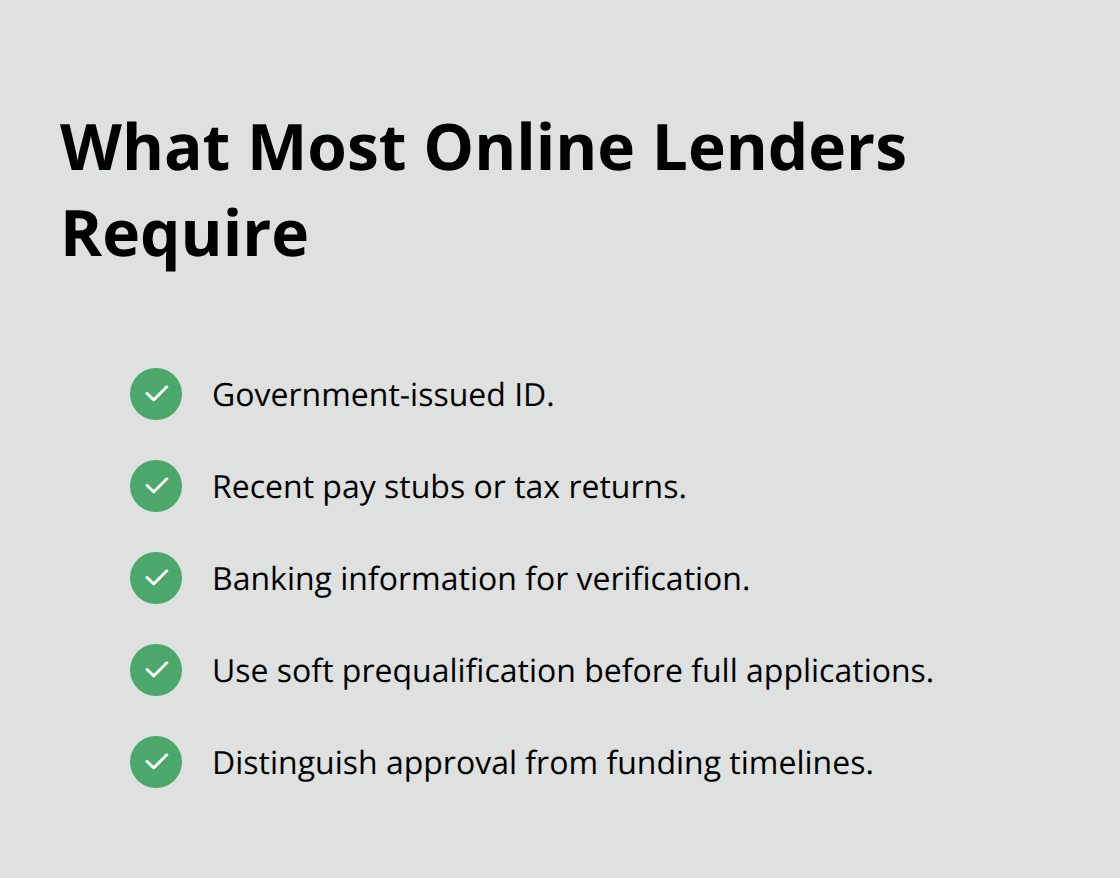

Approval speed and documentation requirements directly impact your ability to access funds when you need them. Online lenders typically require government-issued ID, recent pay stubs or tax returns, and banking information-documents most people can upload in under five minutes. Soft prequalification tools let you see rate estimates without triggering a hard credit pull, so use these first to narrow your options to two or three lenders before submitting formal applications.

When evaluating approval timelines, distinguish between approval and funding: some lenders approve in minutes but fund the next business day, while others deposit directly the same day. Online loan eligibility depends on factors like credit score, income stability, and existing debt levels, which lenders assess during your application.

Assess Customer Service Quality and Lender Partnerships

Customer service quality separates mediocre lenders from reliable ones. Test a lender’s responsiveness before applying by calling their support line or using their chat feature with a simple question-response time and clarity matter when you need to clarify loan terms or resolve payment issues. Lenders partnered with established banks (like CIBC’s partnership with Borrowell for online personal loans) typically offer stronger customer support than standalone operators. Verify that your chosen lender operates in your province and supports remote applications entirely, since availability varies across Canada.

Once you’ve narrowed your choices to lenders with solid reputations, fast approval processes, and responsive support teams, the next step involves protecting yourself during the application and signing process.

How to Apply for a Personal Loan Online Safely

Verify Lender Credentials and Regulatory Status

Applying for a personal loan online in Canada requires more caution than most borrowers expect. Lenders operating in Canada fall under different regulatory bodies depending on their structure: banks are governed by the Bank Act and overseen by OSFI, while consumer protection is largely handled at the provincial level through frameworks like Ontario’s Consumer Protection Act. This fragmented oversight means you cannot assume every online lender follows the same standards.

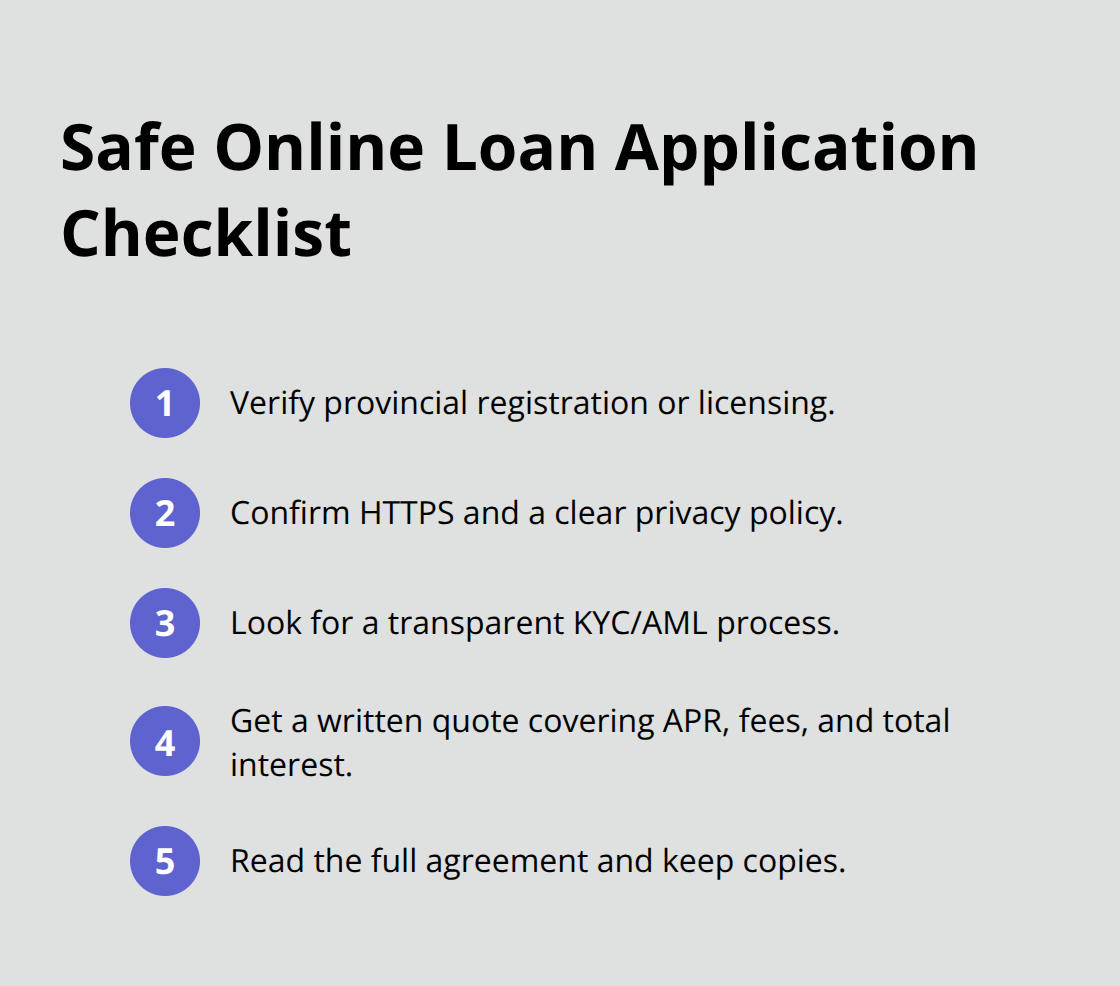

Start by confirming that your chosen lender is registered with provincial regulators in your province and operates transparently about their licensing. Use the National Registration Search to check if an individual or firm is registered. Lenders that hide their regulatory status or lack clear company information are warning signs to avoid entirely.

Protect Your Personal and Financial Information

Before uploading any documents, verify the lender’s website uses HTTPS encryption (the padlock icon in your browser’s address bar confirms this), and confirm their privacy policy explicitly states how they protect your data. Any business classified as a reporting entity must have a full KYC and Anti-Money Laundering compliance program in place, but legitimate lenders will explain this process upfront rather than requesting excessive personal information unexpectedly.

Request a written quote showing the exact APR, origination fee, monthly payment, and total interest cost before you proceed. Never apply with lenders that pressure you to decide quickly or demand upfront fees. These tactics indicate predatory operators that charge rates above 25% with aggressive collection practices.

Read and Understand the Full Loan Agreement

Once you’ve verified credentials, read the loan agreement word-for-word before signing anything electronically. The agreement must clearly state the interest rate (fixed or variable), total fees, payment schedule, prepayment penalties, and what happens if you miss a payment. Ontario Regulation 17/05 requires lenders to disclose mandatory items in fixed and open credit agreements, so check that these disclosures appear in your quote and final agreement.

Pay specific attention to whether prepayment penalties exist, since some lenders charge fees for early repayment while others allow it penalty-free. If the agreement contains unclear language or contradicts the written quote you received, contact the lender’s support team before signing and request clarification in writing. Many borrowers skip this step and later discover hidden fees or unexpected payment terms.

Confirm Funding Details and Keep Records

After signing, keep copies of all documents in a secure folder and confirm the exact deposit date and amount before funds hit your account. If something feels off during any stage of the process, trust that instinct and apply with a different lender instead. Legitimate lenders will answer your questions clearly and provide written confirmation of all terms before you commit.

Final Thoughts

Comparing personal loans online in Canada comes down to three core actions: calculate total cost by examining APR and fees rather than advertised rates, verify lender credentials through independent sources and regulatory checks, and read agreements thoroughly before signing anything electronically. The difference between choosing a lender based on headline rate versus true APR can cost you thousands in unnecessary interest. Taking time to gather written quotes from multiple lenders pays off immediately.

Most borrowers rush through this process and regret it later. Origination fees hide real costs, prepayment penalties can trap you into paying more, and lender reputation matters far more than approval speed alone. Legitimate lenders answer your questions clearly, provide written quotes upfront, and never pressure you into quick decisions-avoid any operator that demands upfront fees or hides their regulatory status.

The online lending market in Canada has expanded significantly, giving you access to banks, credit unions, and fintech platforms all competing for your business. Start with soft prequalifications to see rate estimates without damaging your credit, then narrow your choices to two or three lenders before submitting formal applications. Gather quotes from at least three lenders, compare their total costs side by side, and apply with the operator that offers the best combination of rate, fees, and customer support-or contact Financial Canadian for guidance on finding the right fit for your situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment