Debt problems in Canada are more common than you might think, and they don’t have to define your financial future. At Financial Canadian, we’ve created this guide to help you take concrete action and regain control of your money.

The steps ahead are straightforward and practical. You’ll learn how to assess your situation, choose a repayment strategy that works, and find professional support when you need it.

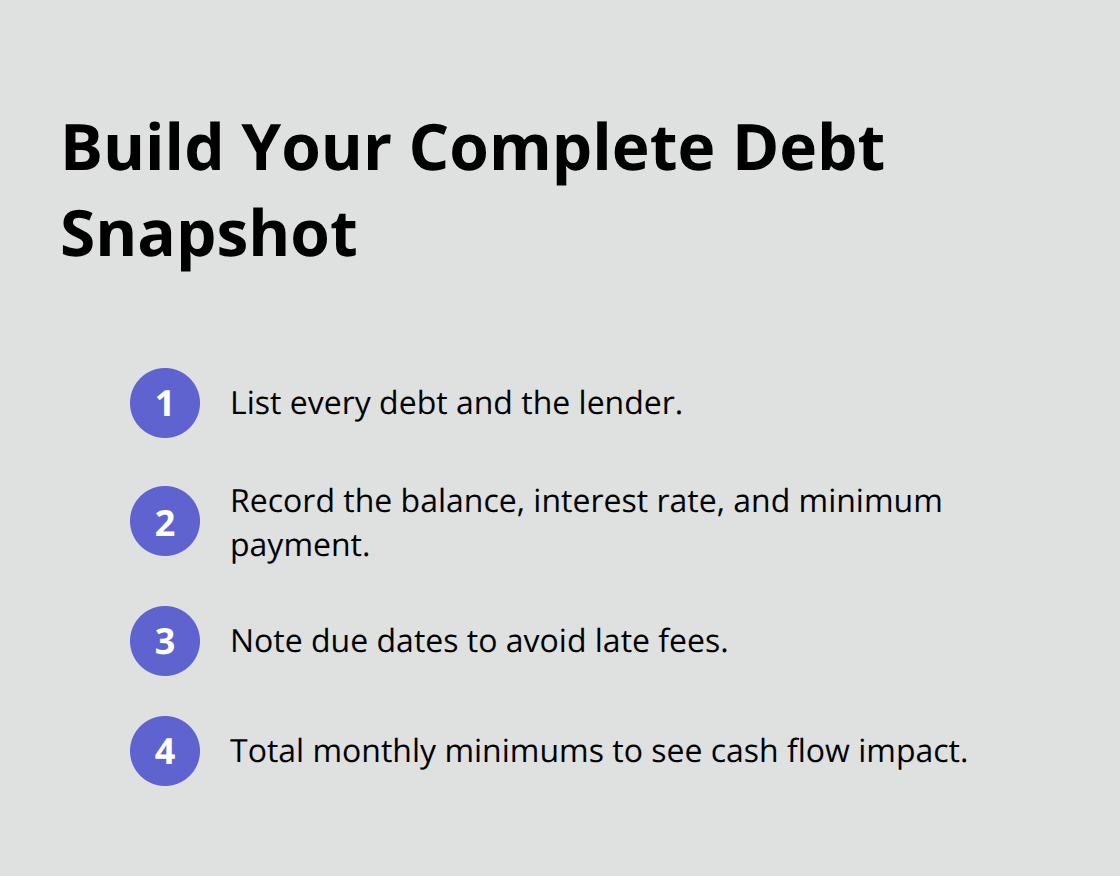

Understanding Your Debt Situation

The first step in regaining control is knowing exactly what you owe. Many Canadians underestimate their total debt because they treat each obligation separately instead of seeing the full picture. List every debt you have, including credit cards, personal loans, car loans, student loans, and any other outstanding balances. Next to each one, write down the current balance, the interest rate, and the minimum monthly payment. This takes an hour at most, but it transforms vague anxiety into concrete numbers you can actually work with.

According to IMF data, household debt in Canada sits at 103% of GDP, the second-highest in the OECD, which means many of your neighbors carry similar burdens. The difference between those who escape debt and those who don’t often comes down to whether they face the numbers head-on.

What Your Interest Rates Really Cost

Interest rates are where debt becomes expensive. A credit card charging 21% annually costs you far more than a car loan at 6%, even if the car loan balance is larger. Calculate the annual interest cost for each debt by multiplying the balance by the rate. This reveals which debts bleed your money fastest. High-interest credit card debt demands your immediate attention because every month you delay, the interest compounds and pulls you further behind. If you have multiple cards, the debt snowball method tackles the smallest balance first for quick wins, while the avalanche method targets the highest interest rate to minimize total interest paid over time. Your choice depends on whether you need psychological momentum from early wins or maximum efficiency. The Bank of Canada rate rose from 0.5% in 2021 to 5% in 2023, which means debts issued at low rates have become much more expensive to service. If you locked in low rates years ago, your situation is better than those who borrowed recently at higher rates.

Know What Money You Actually Have

Next, map your monthly cash flow by listing all income and all expenses for the past three months. Include irregular expenses like car insurance, property taxes, or medical costs by averaging them across months. Subtract total expenses from total income to see what’s left. This number tells you how much you can realistically put toward debt repayment each month. Many people overestimate this figure because they don’t account for discretionary spending or small recurring charges. Be brutally honest here. If you have negative cash flow, you cannot pay down debt without either increasing income or cutting expenses. Some Canadians in this position benefit from debt consolidation, which combines multiple debts into a single payment at a lower interest rate, freeing up monthly cash flow. Others need to explore formal options like consumer proposals or bankruptcy, which provide immediate relief and legal protection from creditors while you stabilize your situation.

With your debt mapped and your cash flow understood, you’re ready to choose a repayment strategy that actually fits your financial reality.

Strategies to Pay Down Debt Faster

Once you know your full debt picture and your monthly cash flow, the real work starts. The most effective approach depends on your psychological makeup and your interest rate structure. Two proven methods compete for your attention, and each works best for different people.

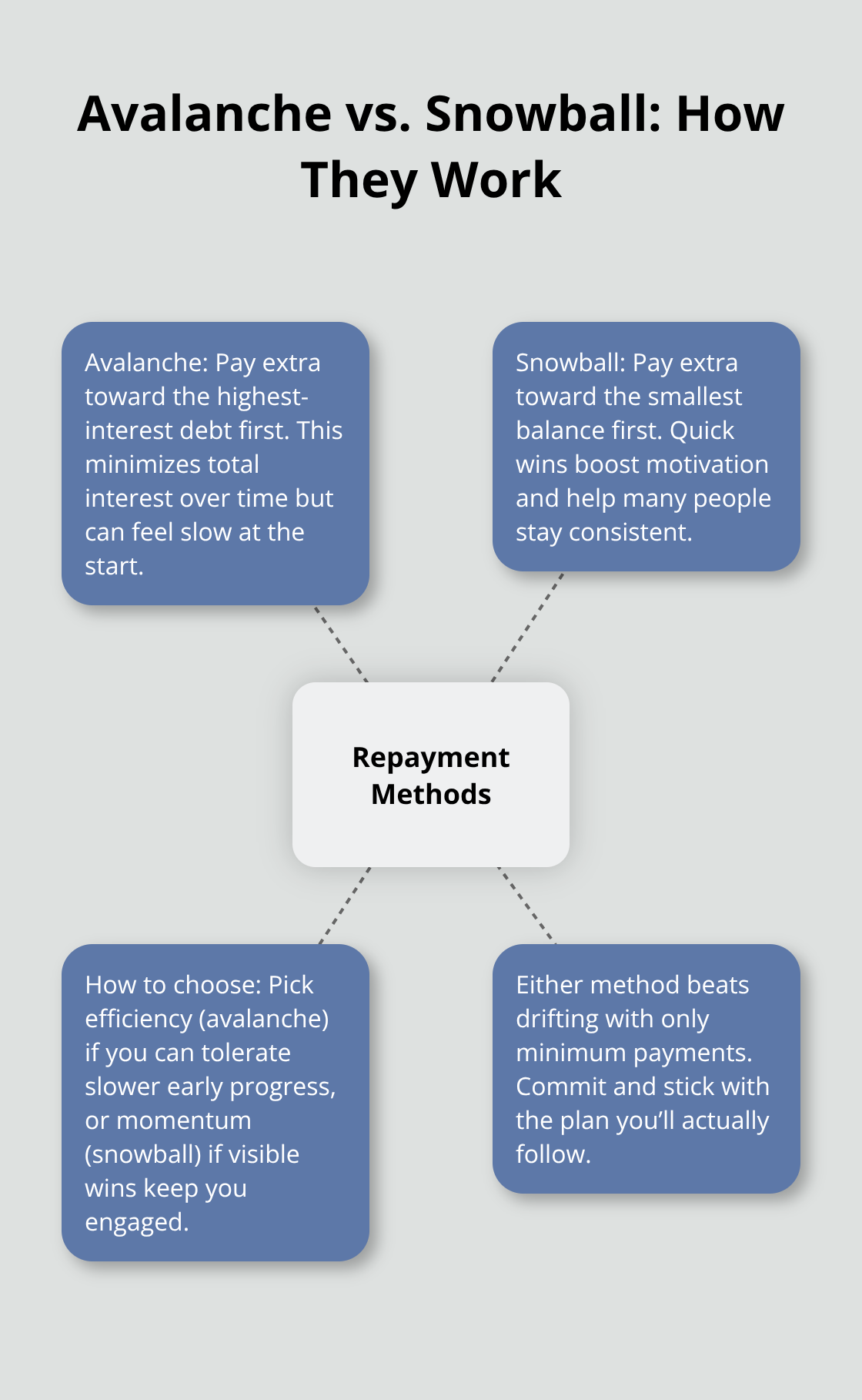

Choose Your Repayment Method

The debt avalanche method targets your highest-interest debts first, which mathematically minimizes total interest paid over time. If you carry a 21% credit card balance alongside a 6% car loan, attacking the credit card aggressively saves you hundreds or thousands in interest charges. However, the debt snowball method works differently: you pay minimums on everything except your smallest balance, then throw all extra money at that smallest debt until it vanishes. This approach delivers a quick win within weeks or months, which motivates many people to stick with their plan. Research shows that psychological momentum matters as much as math; people who see progress tend to maintain discipline longer than those grinding toward a distant finish line.

Try the avalanche method if you’re motivated by efficiency and can stomach slow initial progress. Try the snowball method if you need visible wins to stay committed. Either way, you make a deliberate choice rather than drifting with minimum payments that trap you in debt for years.

Negotiate Lower Rates with Your Creditors

Negotiating with creditors directly works better than most people expect, especially if you’ve paid on time. Call your credit card company and ask for a rate reduction, citing your payment history or competitor offers. Many issuers reduce rates by 2–4 percentage points to keep good customers, saving you significant interest without changing your payment amount. This conversation takes 15 minutes and costs nothing, yet most people never attempt it. Your creditor would rather keep you as a paying customer at a lower rate than lose you to a competitor. If you carry multiple cards, start with the one offering the highest rate and the longest payment history with that issuer. Success here frees up cash flow without requiring you to restructure your entire debt portfolio.

Consolidate High-Interest Debts

For debts you cannot negotiate individually, consolidation combines multiple high-interest obligations into a single loan at a lower rate. This works best when your new rate is genuinely lower than your weighted average rate across existing debts. A consolidation loan at 10% makes sense if you’re averaging 18% across credit cards and personal loans. However, consolidation only works if you stop accumulating new debt; people who consolidate then max out their cards again end up with both the consolidation loan and fresh credit card balances. The hard truth is that debt repayment requires sustained behavior change, not just financial restructuring. If your cash flow is too tight to make meaningful progress even after negotiating rates or consolidating, formal options like consumer proposals offer faster relief. A consumer proposal is a legally binding agreement between you and your creditors to repay a percentage of what you owe in exchange for full debt forgiveness, making it a practical path when personal effort alone cannot close the gap between your income and your obligations.

When personal strategies reach their limits, professional guidance becomes your next logical step.

Seeking Professional Help and Resources

If your debt repayment efforts stall despite honest effort, professional guidance stops being optional and becomes practical. Credit counselling from a certified counsellor works best when you’ve already tried negotiating rates or consolidating debts but still face a cash flow gap. A counsellor assesses your complete financial picture, identifies spending patterns you might have missed, and creates a realistic budget that accounts for both essentials and the psychological spending you’ll actually do. This matters because generic budgets fail when they ignore human behavior. Accredited credit counselling agencies across Canada have helped millions of people break free from debt over five decades, signaling deep experience with situations like yours. A typical counselling session costs nothing or very little because these are not-for-profit organizations funded to help Canadians. During one-on-one sessions, certified counsellors provide personalized budgeting tools and money-management strategies tailored to your situation rather than generic advice. Many agencies also offer workshops and webinars on financial literacy, helping you understand where your money goes and how to prevent future debt accumulation.

Assess Your Financial Health Before Counselling

You can assess your current financial health before committing to counselling. Some organizations provide free debt and money quizzes that reveal your exact position and suggest next steps. These assessments take 10–15 minutes and cost nothing, making them a low-risk way to understand whether counselling fits your needs. The quiz results often point you toward specific resources or counsellors in your area, accelerating your path to professional support.

Understand Consumer Proposals

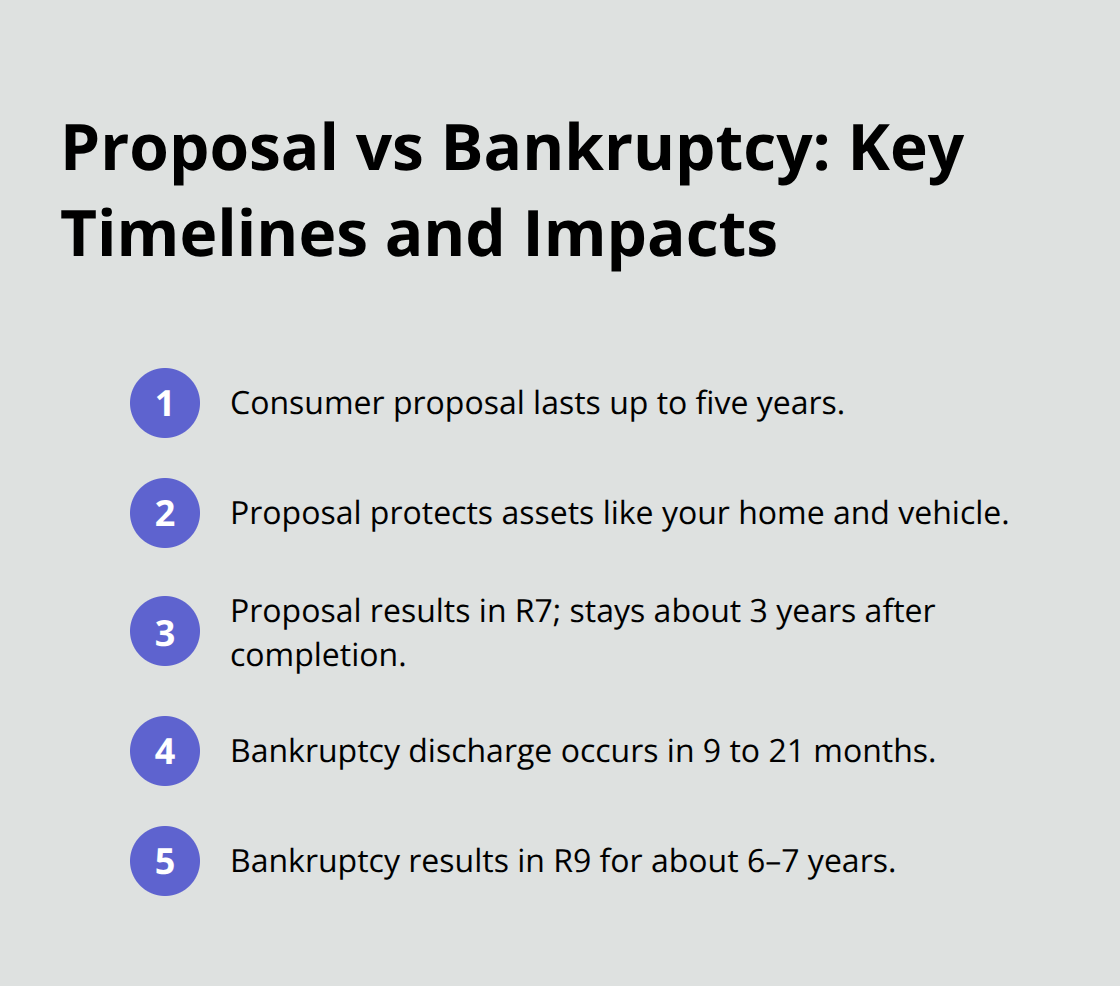

Formal debt relief options exist when personal repayment and counselling cannot bridge the gap between what you owe and what you can afford. A consumer proposal lets you negotiate with creditors through a Licensed Insolvency Trustee to repay only a portion of your unsecured debts over up to five years. This protects your assets, including your home and vehicle, while eliminating credit cards, bank loans, payday loans, and tax debt through a single affordable monthly payment. The proposal results in an R7 credit rating and stays on your file about 3 years after completion, making it less damaging to your credit than bankruptcy.

Consider Bankruptcy as a Faster Option

Bankruptcy works faster for people with very low income who cannot afford any proposal repayment. You surrender non-exempt assets but receive discharge in 9 to 21 months, completely erasing unsecured debts and stopping creditor collection calls immediately. Both options require two counselling sessions and legal protection under Canada’s Bankruptcy and Insolvency Act. Bankruptcy results in an R9 credit rating lasting about 6–7 years, which is longer than a proposal but still recoverable over time.

Choose Between Proposal and Bankruptcy

The key difference between these options is asset protection and payment predictability. Choose a proposal if you own a home or car you want to keep and can afford some repayment. Choose bankruptcy if your income is too low to support any proposal. Start with a free consultation with a Licensed Insolvency Trustee to compare your specific options and understand which path actually fits your circumstances.

Final Thoughts

Your financial future depends on the action you take this week, not on how much you owe today. Start by listing your debts and mapping your cash flow, then call a creditor to negotiate a rate reduction. Each step moves you closer to the stability and control you deserve.

Credit counselling from accredited agencies provides real guidance without judgment, and these not-for-profit organizations have helped millions of Canadians over decades. Licensed Insolvency Trustees offer free consultations to compare your options, while consumer proposals and bankruptcy provide legal protection when personal effort reaches its limit. These resources aren’t luxuries-they’re practical tools designed specifically for Canadians facing debt problems and seeking a clear path forward.

At Financial Canadian, we believe every Canadian deserves access to clear, practical debt problems advice. Canada offers substantial resources to support your journey, and our website connects you with guidance tailored to your situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment