Student loans in Canada affect millions of borrowers, yet many don’t fully understand their repayment options or how to manage their debt strategically. At Financial Canadian, we’ve created this student loan guide Canada to help you navigate federal and provincial loans, explore repayment strategies, and find pathways to debt relief.

Whether you’re just starting repayment or looking to accelerate your payoff, this guide covers the practical steps you need to take control of your student debt.

How Canadian Student Loans Actually Work

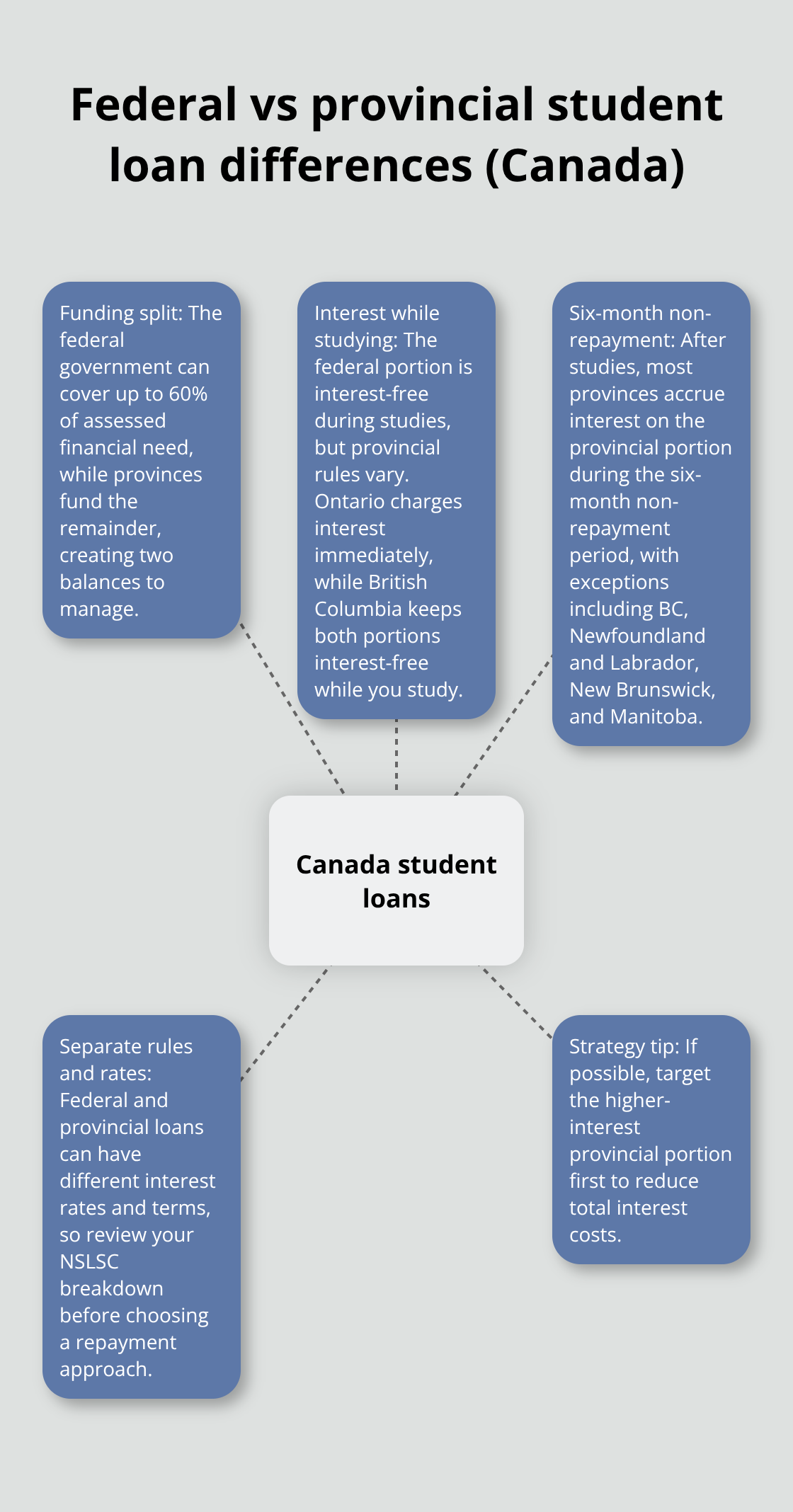

Canada’s student loan system splits between federal and provincial components, and understanding this split matters because it directly affects your repayment timeline and interest costs. The federal government provides up to 60% of your assessed financial need through the Canada Student Loan Program, while your province covers the remaining portion through its own loan program. Ontario borrowers receive an Ontario Student Loan alongside their federal loan, while British Columbia borrowers get a BC Student Loan. This dual-loan structure means you manage two separate debts with different interest rates and rules.

The federal portion stays interest-free while you study, but the provincial portion varies by province. Ontario charges interest immediately, while British Columbia keeps both portions interest-free during your studies. After your studies end, you enter a six-month non-repayment period where you make no payments, though interest continues accumulating on the provincial portion in most provinces except British Columbia, Newfoundland and Labrador, New Brunswick, and Manitoba.

During this six-month window, you can start paying down principal, pay accrued interest as a lump sum, or let interest capitalize into your balance, which increases your total debt.

Understanding Your Loan Limits and Composition

The federal government caps your annual loan at roughly $165 per week, meaning a full-time student typically borrows around $8,580 yearly from the federal portion alone. Your actual borrowing limit depends on your assessed financial need, which factors in tuition costs, living expenses, and family contribution. When repayment begins, the federal portion charges prime rate plus 0%, while Ontario adds 1% to prime, creating a gap where Ontario borrowers pay more interest overall. This is why comparing your loan breakdown matters before repayment starts. Your NSLSC online account shows your exact loan composition and interest rates before you make any repayment decisions.

Customizing Your Repayment Timeline

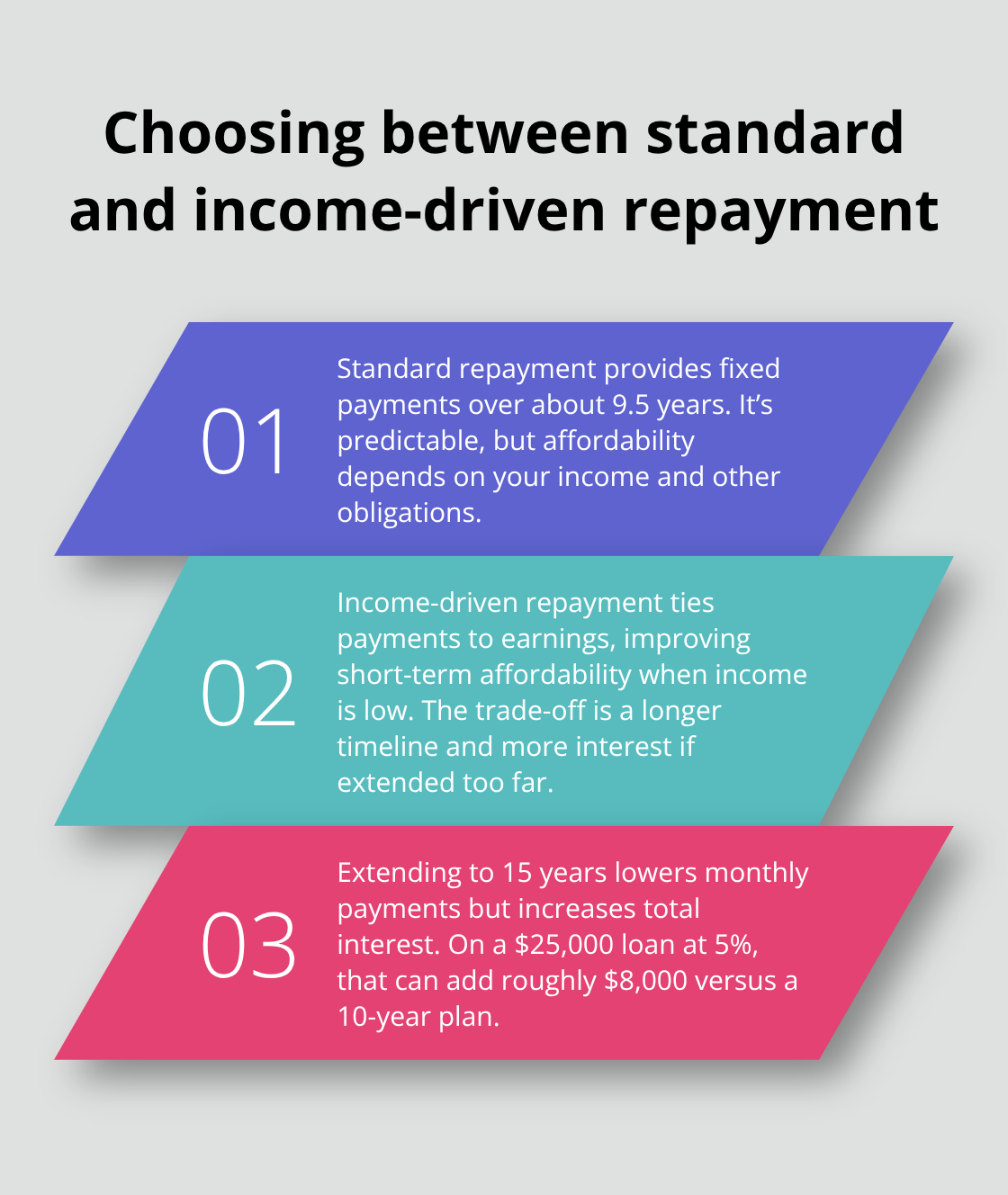

You’re not locked into a standard repayment schedule. The NSLSC allows you to adjust monthly payments directly through your secure online account, which lets you extend your repayment term up to 15 years if needed. Lowering your monthly payment extends how long you repay and increases total interest paid, so this strategy only makes sense if you face temporary cash flow issues. Alternatively, you can pay more aggressively to shorten your repayment window and save thousands in interest. A borrower with $25,000 in debt at a 5% blended interest rate saves roughly $8,000 by repaying over 10 years instead of 15 years. If your financial situation improves-say you land a better job-increasing payments becomes one of your strongest wealth-building moves because every extra dollar goes directly to principal rather than interest.

Interest Relief and Hardship Support

If your income drops significantly or you face unemployment, the Repayment Assistance Plan offers zero or reduced payments for six months. This program prevents default without requiring you to prove permanent disability. For borrowers with permanent disabilities, the RAP-D program may eliminate payments entirely while you remain in good standing. Apply through your NSLSC account rather than waiting until missed payments damage your credit. Medical or parental leave lets you pause repayment for up to 18 consecutive months with no interest accrual and no payments, which protects borrowers facing health crises or new parenthood.

These flexibility options exist precisely because life circumstances change, and your loan structure should adapt to your reality rather than force you into default. Understanding which program fits your situation now positions you to explore the specific repayment strategies that work best for your income level and career path.

Choosing Your Repayment Path

Standard repayment stretches your loan over 9.5 years with fixed monthly payments, but this one-size-fits-all approach doesn’t work for everyone. The NSLSC Loan Repayment Estimator shows your exact monthly payment before repayment starts, so you know whether the standard timeline fits your actual income. A borrower earning $40,000 annually might struggle with a $280 monthly payment, while someone earning $65,000 handles it comfortably.

How Income-driven repayment Changes Your Strategy

Income-driven repayment flips this logic by tying your payment directly to what you earn rather than what you borrowed. If your income drops below your loan payments, income-contingent repayment schemes link what you owe to your actual earnings, which reduces defaults according to research from the Library of Parliament. The catch is that these schemes worry policymakers about adverse selection-if borrowers know payments shrink with lower income, some might deliberately underreport earnings.

What matters practically is that extending repayment from 9.5 years to 15 years lowers monthly payments significantly but costs you thousands more in interest. A $25,000 loan at 5% interest costs roughly $8,000 extra if you stretch repayment to 15 years instead of 10 years. This trade-off makes sense only if you face temporary income challenges, not as a permanent strategy.

The Real Cost of Extended Repayment Terms

Lowering your monthly payment extends how long you repay and increases total interest paid. A borrower with $25,000 in debt at a 5% blended interest rate saves roughly $8,000 by repaying over 10 years instead of 15 years. If your financial situation improves-say you land a better job-increasing payments becomes one of your strongest wealth-building moves because every extra dollar goes directly to principal rather than interest.

Consolidation and Refinancing: When to Use Each

Consolidation and refinancing sound similar but work differently in the Canadian context. Federal and provincial loans already function as a consolidated system through NSLSC, so you don’t combine separate lenders like you might in the United States. What you can do is customize your repayment plan directly through your NSLSC account to match your cash flow without refinancing elsewhere.

Private refinancing through banks or credit unions might offer lower rates if your credit improved since graduation, but this move means losing access to federal protections like income-driven repayment, interest relief, and forgiveness programs. A borrower with $30,000 in loans and a strong credit score might refinance at prime plus 0.5% instead of prime plus 1%, saving roughly $150 annually. However, that same borrower loses the ability to access the Repayment Assistance Plan if they face job loss, which costs far more than the refinancing savings.

Making the Refinancing Decision

The strategic move here is straightforward: use NSLSC’s built-in flexibility first through customized payments and interest relief programs. Only refinance privately if you’ve achieved stable high income, don’t anticipate financial hardship, and can secure a rate meaningfully lower than your current federal-provincial blend. Your next step involves understanding which forgiveness programs apply to your career path, since certain professions qualify for automatic debt relief that makes refinancing irrelevant.

Taking Control of Your Student Debt

Build a Realistic Repayment Budget

Your NSLSC account shows your loan balance, interest rate, and monthly payment amount, but this data alone doesn’t create a workable budget. Track your actual spending for one month across housing, food, transportation, insurance, and discretionary categories. Most Canadian borrowers redirect 10 to 20 percent of their monthly income toward debt repayment once they identify unnecessary expenses. A borrower earning $45,000 annually has roughly $2,800 monthly after taxes, and cutting subscriptions, dining out, or entertainment spending by $300 monthly accelerates payoff significantly.

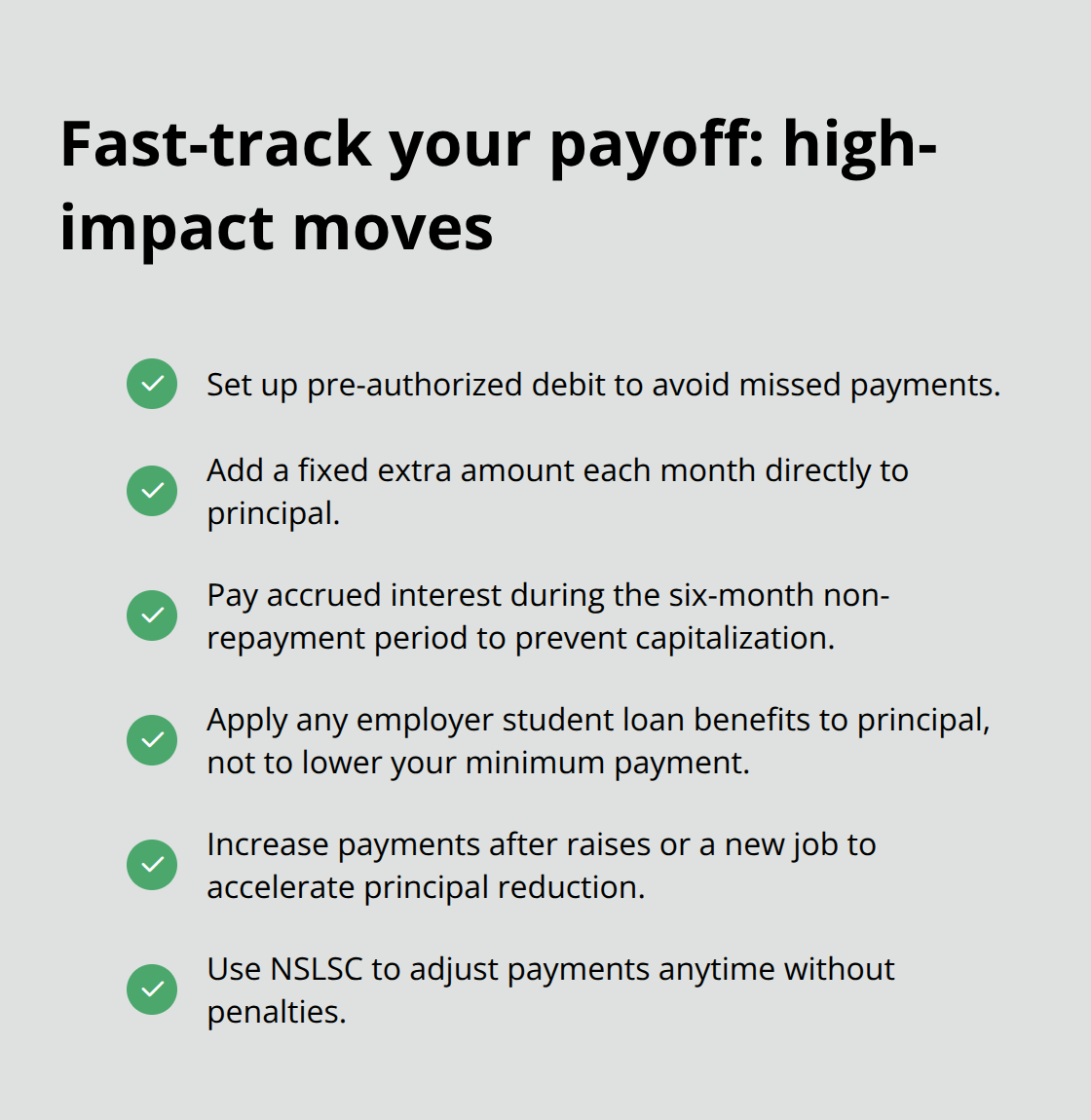

Set up pre-authorized debit for your minimum NSLSC payment first to avoid missed payments that damage credit. Then direct any additional funds to principal reduction. This approach prevents the common mistake of increasing spending when income rises instead of channeling raises directly to debt elimination.

Accelerate Principal Reduction Strategically

Every dollar above your minimum payment reduces the amount that generates interest. A $25,000 loan at prime plus 1 percent accrues roughly $208 monthly in interest alone at current rates, meaning your standard payment covers interest before touching principal in early years. Add $200 monthly to your payments and you’ll eliminate the loan roughly three years faster while saving approximately $4,000 in total interest.

The NSLSC allows payment increases directly through your account without penalties, so there’s no downside to accelerating repayment. During the six-month non-repayment period after graduation, pay accrued interest immediately rather than letting it capitalize into your balance. This single decision prevents your $25,000 loan from becoming $25,500 before repayment even begins. If your employer offers a student loan repayment benefit, apply that money directly to principal rather than reducing your monthly payment. Research shows that borrowers who treat debt repayment as a non-negotiable monthly expense like rent eliminate loans three to five years faster than those who pay minimums.

Investigate Forgiveness Programs for Your Career

Forgiveness programs represent your strongest opportunity for debt elimination if your career path qualifies, yet most borrowers never investigate whether they’re eligible. The Canada Student Loan Forgiveness program applies to professionals delivering in-person services in eligible Canadian communities, including nurses, nurse practitioners, and certain other healthcare and education roles. Saskatchewan extends this further by offering up to $20,000 in forgiveness over five years for nurses and veterinary professionals in designated communities, providing $4,000 annually toward loan elimination.

Apply through your NSLSC account rather than waiting until you’ve made years of unnecessary payments. Some provincial programs tie forgiveness to geographic location or service commitments, meaning a nurse working in rural communities might qualify for forgiveness that urban-based nurses don’t access. Check whether your specific role, location, and employer match forgiveness criteria before committing to personal loan refinancing, since forgiveness programs eliminate debt entirely rather than just lowering your interest rate. Confirm whether forgiveness applies to your situation within your first year after graduation, because these programs change and eligibility windows sometimes close. If forgiveness doesn’t apply, then focus on the accelerated principal reduction strategy outlined above rather than hoping for debt relief that won’t materialize.

Final Thoughts

Your student loan repayment strategy matters far more than your loan balance alone. Borrowers who take control early-by customizing payments, exploring forgiveness programs, and accelerating principal reduction-eliminate debt years faster than those who simply pay minimums. The difference between a borrower who extends repayment to 15 years and one who maintains a 10-year timeline reaches roughly $8,000 in additional interest on a $25,000 loan.

Start by logging into your NSLSC account to confirm your exact loan composition, interest rates, and repayment start date. Set up pre-authorized debit immediately to prevent missed payments that damage your credit score. Then determine whether forgiveness programs apply to your career-nurses, healthcare professionals, and educators in eligible communities should investigate whether they qualify for automatic debt elimination before committing to aggressive repayment schedules.

If forgiveness doesn’t apply, calculate how much extra you can pay monthly toward principal. Even $150 additional monthly payments compress your repayment timeline significantly while saving thousands in interest. We at Financial Canadian created this student loan guide Canada to help you navigate these decisions and take control of your debt rather than letting it control your financial future.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment