Buying your first home in Canada is one of the biggest financial decisions you’ll make. The mortgage landscape can feel overwhelming with fixed rates, variable rates, insured mortgages, and more options than you might expect.

We at Financial Canadian have created this guide to help first time homebuyers Canada navigate these choices with clarity. You’ll learn about programs designed to help you, mistakes to avoid, and practical steps to move forward confidently.

Understanding Your Mortgage Options in Canada

Buying your first home in Canada requires you to navigate multiple mortgage choices that will shape your monthly payments and long-term financial stability. The options available can feel overwhelming, but breaking them down into clear categories helps you match the right mortgage to your situation.

Fixed-Rate vs Variable-Rate: Payment Certainty or Potential Savings

As of April 2026, fixed-rate mortgages are rising due to higher bond yields, making variable-rate mortgages comparatively more affordable right now. However, affordability today doesn’t mean it’s the right choice for you. According to the 2025 CMHC Mortgage Consumer Survey, 62% of Canadian buyers chose fixed rates while only 25% selected variable rates, revealing that most first-time buyers prioritize payment certainty over potential savings.

If you need predictable monthly payments and can’t tolerate fluctuation, fixed-rate mortgages protect your budget regardless of what the Bank of Canada does with interest rates. Variable rates follow the prime rate set by the Bank of Canada plus or minus a lender’s discount, which means your payment can increase if rates rise. From June 2024 to October 2025, the Bank of Canada cut rates 9 times, but inflation and energy pressures pushed rates higher again by April 2026. This volatility matters: if you choose variable and rates climb, your payment could jump hundreds of dollars monthly.

The practical advantage of variable rates only materializes if you can handle payment swings and genuinely expect rates to fall further. Most first-time buyers lack the financial cushion for this uncertainty, which explains why fixed-rate dominance persists.

Insured vs Conventional Mortgages: Down Payment Trade-Offs

If you put down less than 20%, you’ll need mortgage loan insurance CMHC. This insurance lets lenders offer down payments as low as 5%, making homeownership accessible when you don’t have substantial savings. The trade-off is clear: mortgage loan insurance premiums get added to your mortgage balance and cost thousands over the life of your loan.

When you calculate affordability, factor these insurance costs into your monthly payment estimates using CMHC’s affordability calculator. Conventional mortgages require 20% down but eliminate insurance costs entirely, which saves money if you can accumulate that down payment. For most first-time buyers, an insured mortgage represents the only realistic path to homeownership.

Closed vs Open Mortgages: Rate Savings vs Flexibility

Closed mortgages lock you into your rate and terms for the entire mortgage period, typically offering lower rates because the lender has payment certainty. Open mortgages let you pay off the balance early without penalties, but lenders charge higher rates as compensation for that flexibility. For first-time buyers, closed mortgages make sense because you’re unlikely to sell or refinance within the first few years, and the rate savings matter more than early repayment flexibility.

Your mortgage choice sets the foundation for everything that follows in your homebuying journey. With these options clarified, you can now explore the government programs and incentives specifically designed to help first-time buyers like you reduce costs and build equity faster.

Government Programs That Actually Reduce Your Costs

The Home Buyers’ Plan and RRSP Withdrawals

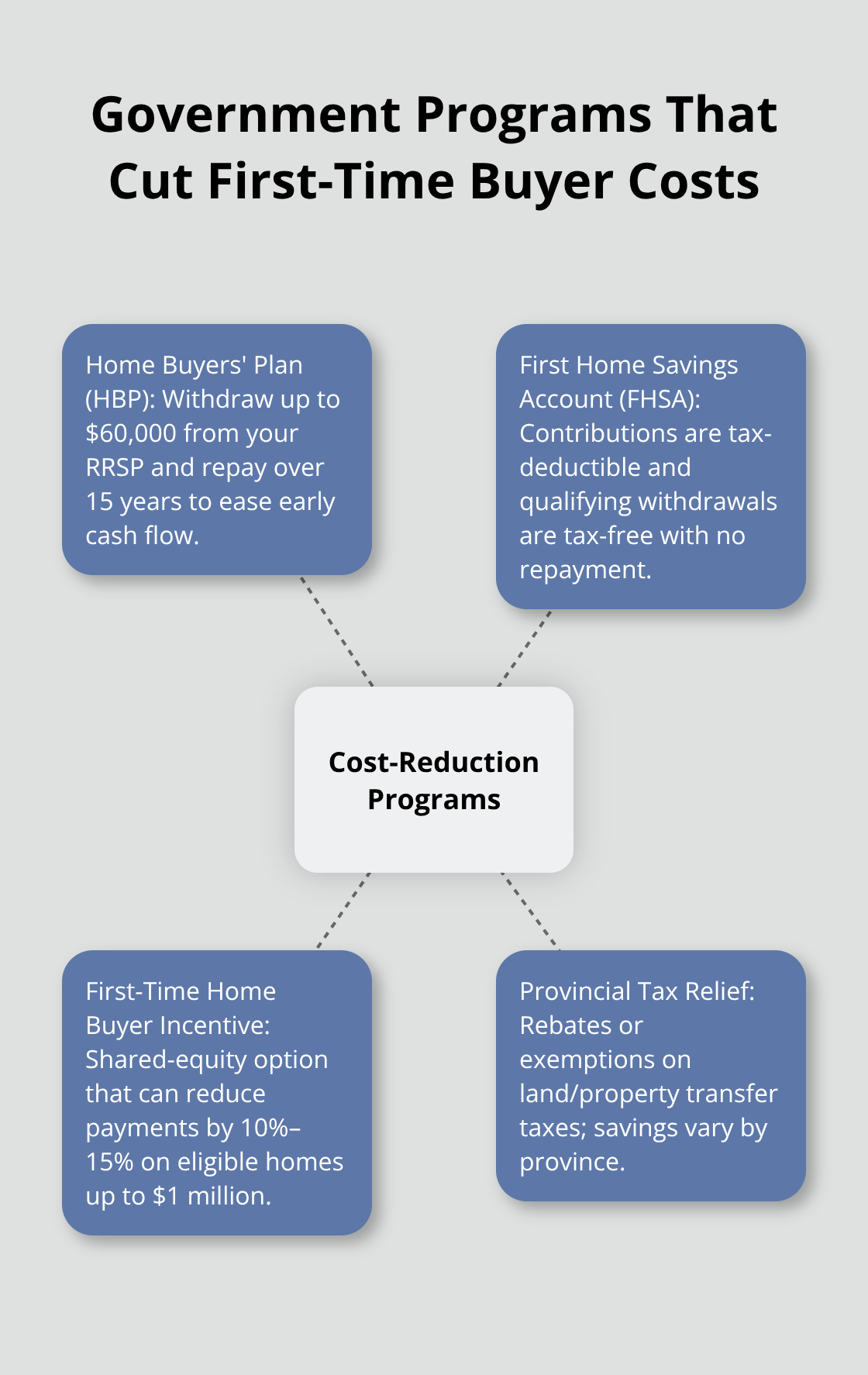

Canada’s government has created several programs specifically to lower the barrier to homeownership, and you should use them. The Home Buyers’ Plan lets you withdraw up to $60,000 from your RRSP to purchase your first home, with a 15-year repayment period that gives you breathing room during the critical early years of ownership. This works best if you have substantial RRSP savings already accumulated, because withdrawing early means losing years of compound growth on that money.

The First Home Savings Account: A Superior Alternative

The First Home Savings Account offers a better structure for many buyers: contributions are tax-deductible, and withdrawals for a qualifying home purchase are entirely tax-free, meaning you don’t need to repay anything. If you have the discipline to save consistently, the FHSA outperforms the Home Buyers’ Plan because you keep all the growth tax-free.

The First-Time Home Buyer Incentive

The First-Time Home Buyer Incentive shares a portion of your mortgage with the government, reducing your monthly costs immediately and making you eligible for larger mortgages with smaller down payments. This program applies to properties at or below $1 million and can cut your mortgage payment by 10% to 15%, which translates to thousands of dollars in annual savings during your first years of ownership.

Provincial Tax Relief and Land Transfer Savings

Provincial governments offer substantial tax relief through provincial tax relief land transfer tax rebates and exemptions. Ontario provides a full rebate on land transfer tax for first-time buyers on properties up to $500,000, saving purchasers thousands in closing costs. British Columbia offers a first-time buyer exemption on the property transfer tax for homes under $500,000, while Alberta has no property transfer tax at all. Research your specific province’s incentives before making an offer, because these savings directly reduce your closing costs and the amount you need to borrow.

Combining Programs for Maximum Impact

Most first-time buyers overlook these programs because they assume government help is minimal or difficult to access. The reality is that combining the FHSA, provincial tax relief, and the First-Time Home Buyer Incentive can reduce your effective borrowing cost by 15% to 20% compared to buyers who ignore them entirely. Understanding your credit score and overall financial health strengthens your position when accessing these programs. With these government tools working in your favor, you’re now ready to understand the mistakes that derail many first-time buyers and how to avoid them.

Where First-Time Buyers Stumble

Accepting Pre-Approval as Permission to Overspend

Most first-time buyers understand the mortgage mechanics but fail at the financial discipline required to stay within realistic bounds. The problem isn’t knowledge-it’s that real estate agents, lenders, and online calculators all push you toward the maximum mortgage you technically qualify for, not the maximum you can actually afford. When a lender tells you that you qualify for a $650,000 mortgage based on your gross debt service ratio, that number reflects what the bank will lend, not what protects your financial security.

CMHC’s debt service calculators show that lenders approve mortgages where your GDS ratio reaches 39% and your TDS ratio hits 40%, meaning nearly two-fifths of your gross income goes toward all debt payments. This leaves minimal room for life’s interruptions-job loss, medical emergencies, or interest rate increases. Treat pre-approval as a ceiling you should undercut significantly, not permission to spend that amount.

Calculate what you genuinely need monthly for property taxes, utilities, maintenance, and insurance, then work backward to determine your actual comfortable mortgage size. Most buyers discover too late that they’ve stretched into a property that consumes 45% to 50% of their income once all ownership costs are included.

Overlooking Hidden Costs Until Closing Day

Hidden costs blindside buyers because they focus entirely on mortgage payment and down payment. Property inspections cost $400 to $600, appraisals cost $300 to $400, and legal fees run $1,500 to $2,500 depending on your province and property complexity. Home insurance quotes vary wildly-expect $1,200 to $2,000 annually depending on location and property value.

Property taxes Toronto Vancouver in Toronto average 0.75% of home value annually, while Vancouver sits around 0.3%, creating thousands in annual variation. Condo fees, if applicable, add $250 to $500 monthly and increase unpredictably when the building needs major repairs. Mortgage default insurance premiums, if your down payment is under 20%, add 2% to 4% to your mortgage balance immediately.

Many buyers calculate affordability using only mortgage payment plus property tax, then face sticker shock during closing when legal fees, inspections, and insurance quotes arrive. Add up every cost you’ll face in year one, then add 20% as a buffer for unknowns. That total should never consume more than 32% of your gross household income.

Shopping for Rates Passively Rather Than Actively

The final critical mistake is rate shopping passively rather than actively. About 77% of rate shoppers inquire for fixed rates while only 8% inquire for variable, yet most buyers contact just one or two lenders before accepting an offer. The difference between the lowest and highest rate quoted by different lenders on identical mortgage terms routinely reaches 0.5% to 0.75%, which translates to $150 to $225 monthly on a $500,000 mortgage over five years.

That’s $9,000 to $13,500 in unnecessary interest paid because you didn’t invest three hours contacting multiple lenders. Contact at least five lenders-banks, credit unions, and mortgage brokers-and request quotes for identical terms. Don’t accept the first approval; use competing offers as leverage to negotiate better rates or lower fees with your preferred lender.

Final Thoughts

You now possess the knowledge that separates confident first-time homebuyers in Canada from those who stumble through the process. Fixed-rate mortgages offer payment certainty while variable rates provide potential savings when rates fall. Insured mortgages enable homeownership with smaller down payments, though conventional mortgages eliminate insurance costs if you accumulate 20% down. Closed mortgages deliver better rates for buyers who won’t need early repayment flexibility, and government programs (the Home Buyers’ Plan, First Home Savings Account, First-Time Home Buyer Incentive, and provincial tax relief) reduce your effective borrowing cost by 15% to 20% when combined strategically.

The mistakes that derail buyers are entirely preventable through disciplined planning. Treat pre-approval as a ceiling you should undercut, not permission to overspend on a property beyond your realistic means. Calculate every ownership cost before committing to a property, then add a 20% buffer for unknowns that will inevitably surface. Shop rates actively across at least five lenders rather than accepting the first offer, because rate differences routinely cost you $9,000 to $13,500 over five years.

Start your action plan this week by contacting multiple lenders for pre-approval quotes. Calculate your realistic budget using CMHC’s affordability calculator and research your province’s specific tax incentives. Contact a mortgage broker to compare options across lenders simultaneously, and you’ll close on your first home with confidence rather than regret.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment