Buying your first home in Canada is one of the biggest financial decisions you’ll make. Most first-time homebuyers in Canada feel overwhelmed by the process-from figuring out how much to borrow to navigating mortgage options and closing costs.

We at Financial Canadian have created this guide to walk you through each step, so you can move forward with confidence and avoid costly mistakes.

Know Your Numbers Before House Hunting

Your financial foundation determines everything that follows in homeownership. Start by calculating your actual take-home income, not your gross salary. Include all reliable income sources: employment, self-employment, rental income, or investment returns. Then list every monthly debt obligation: car loans, student loans, credit cards, and personal lines of credit. Add these together to find your total debt servicing ratio, which lenders scrutinize heavily.

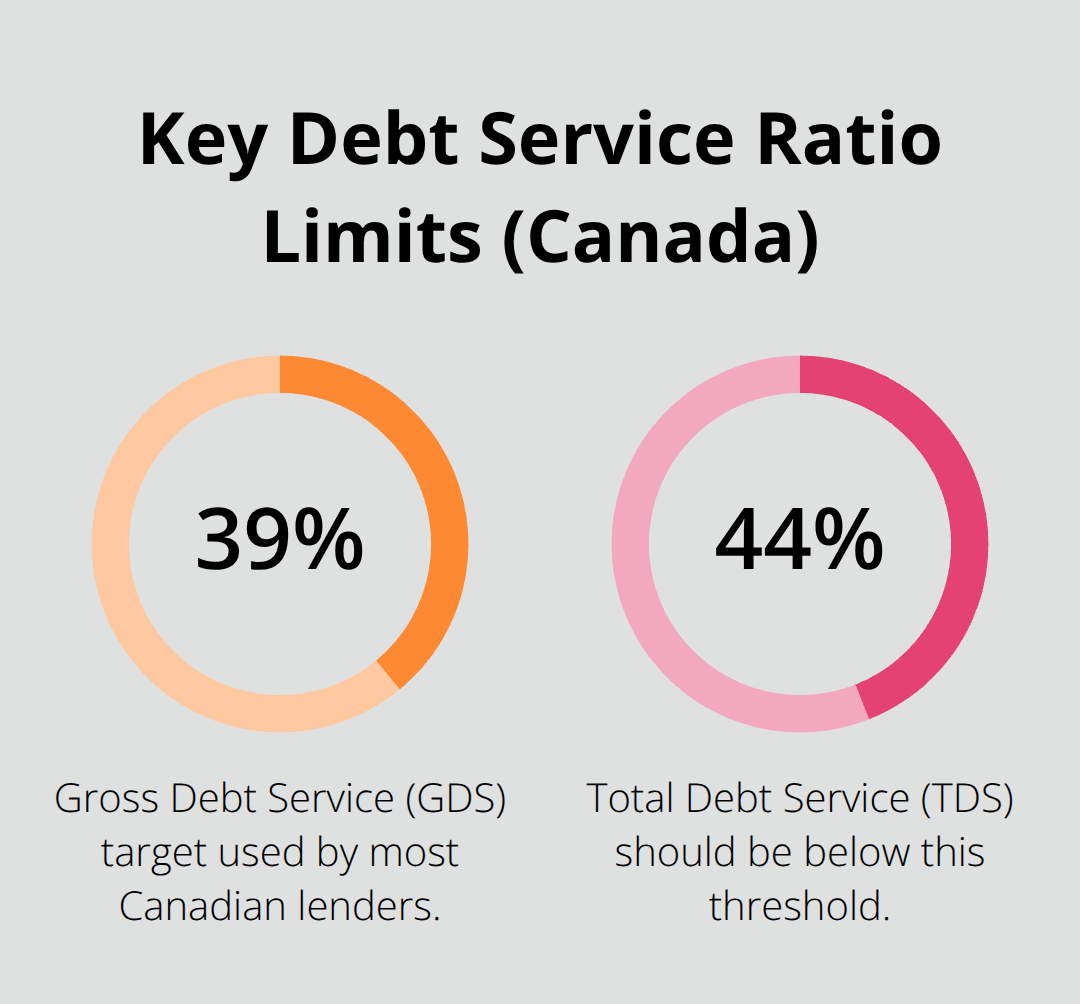

Understanding Debt Service Ratios

Most Canadian lenders want your Gross Debt Service ratio at 39 percent and your Total Debt Service ratio below 44 percent, according to CMHC guidelines. This means if you earn $5,000 monthly after tax, lenders typically won’t approve a mortgage payment exceeding $1,950. The math is brutal but necessary.

Checking Your Credit Score

Pull your credit report from Equifax or TransUnion before you start house hunting, not after you’ve found the perfect property. Your credit score directly impacts your mortgage rate. A score above 740 qualifies you for the best rates, while scores between 680 and 739 mean higher rates and stricter lending conditions.

Missing even one payment or carrying high credit card balances tanks your score. If your score sits below 680, focus on paying down debt and rebuilding credit before applying for a mortgage. This delay costs nothing now but saves thousands in interest later.

Calculating What You Can Actually Borrow

Use CMHC’s free Affordability Calculator and Debt Service Calculator to model different scenarios. These tools show exactly how much you can borrow based on your income and debts without guessing. A $400,000 mortgage at current rates requires roughly $1,900 monthly payments, plus property taxes, insurance, and utilities.

Many first-time buyers underestimate these additional costs. Property taxes vary by province but average 0.5 to 1.2 percent of home value annually. Homeowners insurance costs $800 to $1,500 yearly depending on location and coverage. Factor these into your affordability calculation.

Accounting for Mortgage Insurance

If you put down less than 20 percent, mortgage insurance becomes mandatory. CMHC’s insurance premiums depend on your down payment size. A 5 percent down payment on a $400,000 home means paying roughly $11,200 in insurance costs added to your mortgage. First-time buyers often overlook this expense when calculating affordability.

Getting Pre-Approved

Obtain pre-approval before making any offers. Pre-approval shows sellers you’re serious and gives you a locked-in rate for 120 days, protecting you from rate increases during your search. With your numbers confirmed and your financial readiness established, you’re ready to explore mortgage options that match your situation.

Navigating Mortgage Options and Pre-Approval

Fixed-Rate Mortgages Lock In Your Budget

Fixed-rate mortgages lock in your interest rate for the entire term, meaning your monthly payment stays identical whether rates climb to 7 percent or fall to 2 percent. This predictability matters enormously for first-time buyers who need stable monthly budgets. Variable-rate mortgages start lower-typically 0.5 to 1 percent below fixed rates-but fluctuate with prime rate changes. If rates rise, your payment increases mid-term, potentially straining your finances. Most first-time buyers should choose fixed rates because the budget certainty outweighs small initial savings. You’re paying for peace of mind, and that’s worth it when you’re already stretching financially.

Understanding Mortgage Insurance Costs

Put down less than 20 percent and CMHC mortgage insurance becomes mandatory-you cannot avoid it. This insurance protects the lender, not you, yet you pay the full cost. A 10 percent down payment triggers insurance premiums around 2.8 to 3.1 percent of your mortgage amount. A 5 percent down payment costs roughly 2.8 to 4.0 percent depending on your mortgage size.

These aren’t small numbers. On a $400,000 home with 5 percent down, you’re adding $11,200 to $16,000 in insurance costs.

However, the First-Time Home Buyer Incentive can reduce this burden by allowing you to borrow up to 5 percent of the home’s purchase price interest-free from the government over a 10-year period, effectively lowering your required down payment and reducing mortgage insurance costs. This program works through participating lenders and genuinely saves thousands for qualified buyers.

Getting Pre-Approved Strengthens Your Position

Pre-approval is non-negotiable before you start viewing homes seriously. The pre-approval process takes 3 to 5 business days and involves your lender verifying income, employment, assets, and debts. You receive a written commitment stating the maximum mortgage amount the lender will provide, locked at a specific rate for 120 days. This locked rate protects you if prime rates climb during your house hunt.

More importantly, pre-approval strengthens your offer in competitive markets. Sellers see you’re financially vetted and serious, not a casual browser. In hot markets, pre-approval can be the difference between your offer being accepted or rejected. With your mortgage strategy confirmed and your pre-approval in hand, you’re ready to search for properties that fit both your budget and your lifestyle.

Finding and Securing Your First Home

Start your property search armed with your pre-approval letter and a clear budget ceiling. Many first-time buyers waste months viewing homes above their price range, which clouds judgment and delays the actual purchase. Set your maximum at 85 percent of your pre-approved amount, not the full approval. This buffer protects you against bidding wars that push prices higher than appraisals support. Search using real estate platforms like Realtor.ca and MLS listings specific to your province, filtering by your target neighborhoods and must-have features. Spend two to four weeks searching before making offers-rushing into the first property you see leads to regret and overpaying. Location matters more than the house itself because you can renovate a kitchen but cannot move the property. Research neighborhood crime rates through Statistics Canada data, school ratings if you have children, and commute times to your workplace. Factor in property taxes specific to your municipality; they vary dramatically across Canada and directly impact your true monthly housing costs.

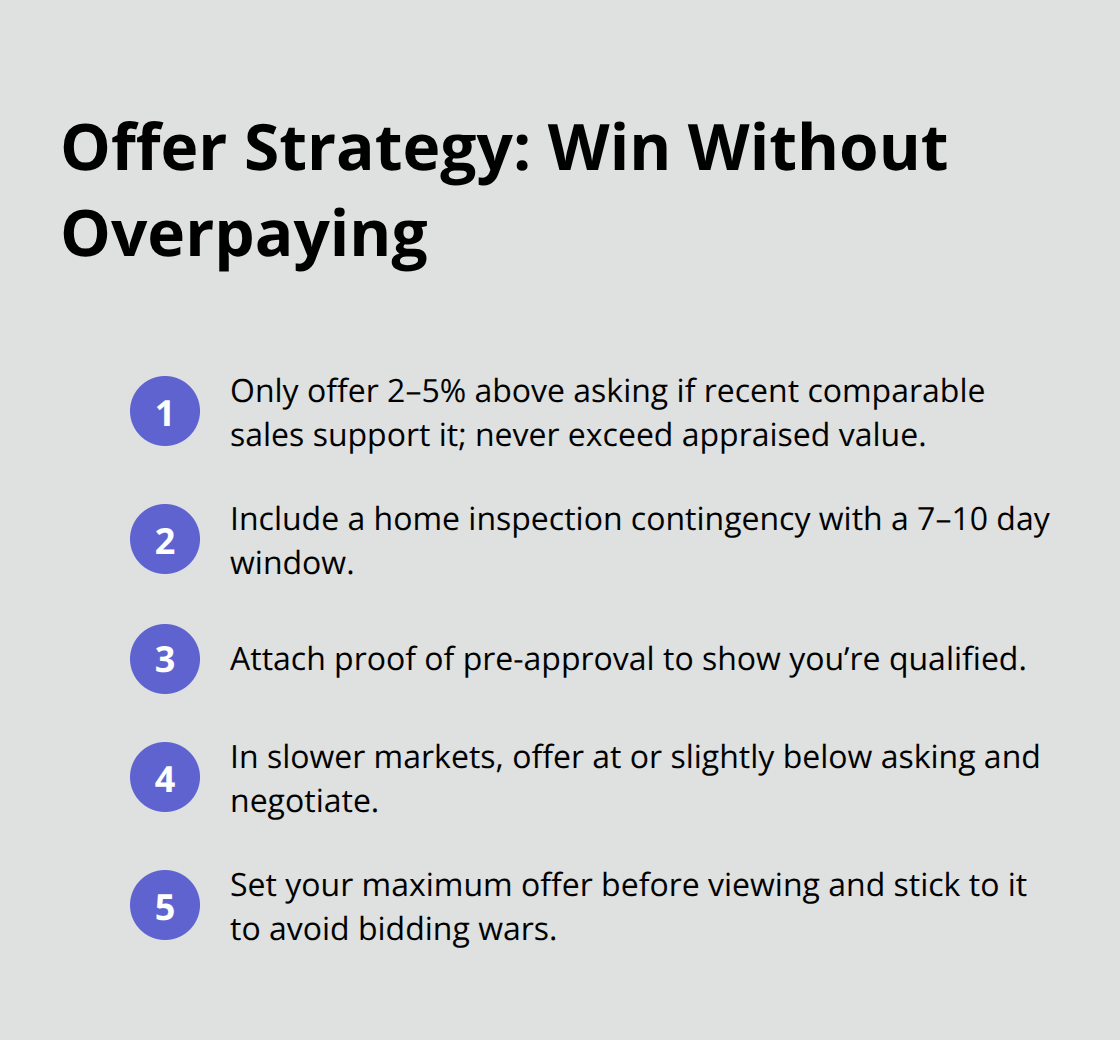

Making Offers That Win Without Overpaying

When you find a property, your offer strategy determines whether you win or waste money. In competitive markets, offering above asking price feels necessary but destroys your financial cushion. Instead, offer 2 to 5 percent above asking if comparable homes sold recently at that price, but never exceed what the appraisal will support-lenders won’t finance more than the appraised value regardless of your offer. Include a home inspection contingency allowing you to walk away if major issues surface, typically within 7 to 10 days. This contingency costs nothing but protects against inheriting expensive repairs. Include proof of pre-approval with your offer to show the seller you’re serious and financially qualified.

In slower markets, offer at or slightly below asking; sellers are desperate and will negotiate. Avoid bidding wars by setting your maximum offer before viewing the property and sticking to it ruthlessly. Once your offer receives acceptance, the clock starts-you typically have 30 days to close according to standard Canadian timelines, though some markets allow 45 to 60 days.

Inspections Reveal Hidden Problems

Hire a professional home inspector with proper credentials from the Canadian Association of Home & Property Inspectors. The inspection costs $400 to $600 and checks structural integrity, roof condition, electrical systems, plumbing, heating, and foundation stability. Request the inspector’s full written report within 48 hours, then share it with your real estate agent and lender. If major issues emerge-foundation cracks, roof leaks, electrical hazards-you can renegotiate the price downward, request repairs, or walk away entirely if your contingency allows. Never skip the inspection to save money or speed closing-catching a $15,000 roof replacement before purchase beats discovering it after signing.

Appraisals Determine What Lenders Will Finance

The lender orders a separate appraisal costing $300 to $500, which determines the property’s market value. If the appraisal comes in lower than your offer price, you face a difficult choice: increase your down payment to cover the difference, renegotiate with the seller, or withdraw if contingencies permit. This happens frequently in hot markets where bidding wars inflate prices beyond market value. The appraisal protects both you and the lender from overpaying for a property that won’t hold its value.

Final Steps to Homeownership

Closing represents the final stretch where your mortgage funds the purchase and legal ownership transfers to you. The typical closing timeline runs 30 days from offer acceptance, though some situations extend longer depending on your lender’s underwriting speed and local requirements. Your lender orders a title search to confirm the property’s title is free of liens or legal claims, and title insurance protects you against future title problems obtained at closing. You’ll also need homeowners insurance in place-lenders require proof of coverage before releasing funds, and you’ll pay for the first year by closing day.

Review your Closing Disclosure at least three business days before signing, as this document outlines your final loan terms, interest rate, monthly payment, and all closing costs itemized. Compare it carefully to your initial loan estimate and raise any discrepancies with your lender immediately (closing costs typically range from 2 to 5 percent of your loan amount and include appraisal fees, title insurance, legal fees, and property taxes). Conduct a final walkthrough one to two days before closing to confirm the home’s condition matches your expectations and that any agreed-upon repairs are completed.

On closing day, bring photo identification, proof of homeowners insurance, and your purchase agreement, then sign multiple documents in a process that typically takes one to two hours. Avoid large purchases or new credit before closing, as these actions damage your credit score and debt-to-income ratio, potentially jeopardizing your approval. After you sign, the lender releases funds to the title company, the seller receives payment, and the deed records with local government, making you the official owner-protect yourself against closing scams by using two-factor authentication and verifying wire instructions with trusted sources before sending funds. For first-time homebuyers in Canada, closing marks the moment years of planning and saving become reality, and we at Financial Canadian offer resources to guide your homeownership journey as you establish your new life.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment