At Financial Canadian, we often receive questions about personal lines of credit. This flexible financial tool can be a valuable resource for managing your finances.

What is a personal line of credit? It’s a revolving credit account that allows you to borrow money up to a predetermined limit, repay it, and borrow again as needed.

In this post, we’ll explore how personal lines of credit work, their types, and their pros and cons to help you decide if they’re right for your financial situation.

How Does a Personal Line of Credit Work?

Understanding the Basics

A personal line of credit offers a flexible borrowing option that allows you to access funds up to a predetermined limit. Unlike traditional loans, you don’t receive a lump sum upfront. Instead, you can withdraw money as needed, paying interest only on the amount you use.

Accessing Your Funds

When a lender approves you for a personal line of credit, they set a credit limit. You can then withdraw funds up to this limit through various methods:

- Writing checks

- Using a linked debit card

- Transferring money to your checking account

This flexibility makes it an excellent tool for managing unexpected expenses or irregular cash flow.

Repayment and Interest

As you use your line of credit, you’ll receive monthly statements showing your balance and minimum payment due. You have the option to pay the minimum, the full balance, or any amount in between. Interest accrues on the outstanding balance, typically at a variable rate. The Bank of Canada provides data on interest rates for new and existing loans in Canadian dollars.

The Revolving Nature

One key feature of a personal line of credit is its revolving nature. As you repay the borrowed amount, that credit becomes available again. For example:

- You have a $10,000 limit

- You borrow $3,000

- You still have $7,000 available

- After repaying $1,000, your available credit increases to $8,000

This cycle continues throughout the life of the credit line.

Comparison with Personal Loans

Personal lines of credit differ significantly from personal loans. While both are forms of borrowing, personal loans provide a one-time lump sum with fixed repayment terms. In contrast, lines of credit offer ongoing access to funds with more flexible repayment options.

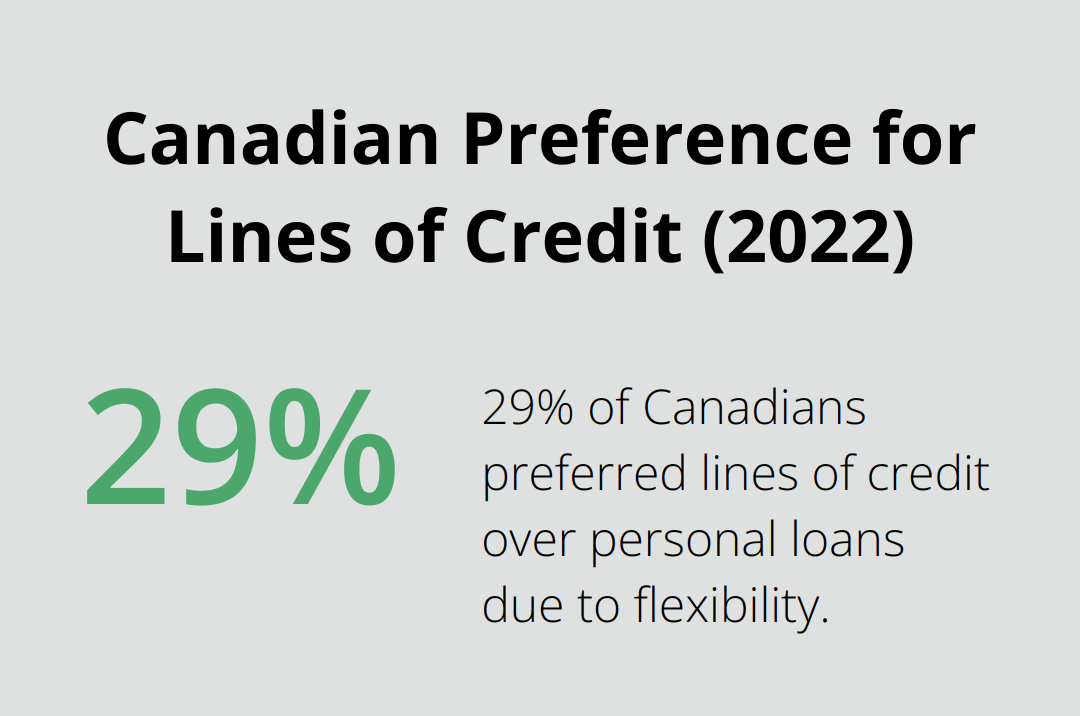

A 2022 study by the Financial Consumer Agency of Canada found that 29% of Canadians preferred lines of credit over personal loans due to this flexibility. This preference highlights the importance of considering your specific financial needs when choosing between these options.

If you need a set amount for a one-time expense, a personal loan might suit you better. However, if you seek ongoing financial flexibility, a personal line of credit could be the optimal choice.

Now that we’ve covered how personal lines of credit work, let’s explore the different types available to Canadian consumers.

Types of Personal Lines of Credit

Unsecured Personal Lines of Credit

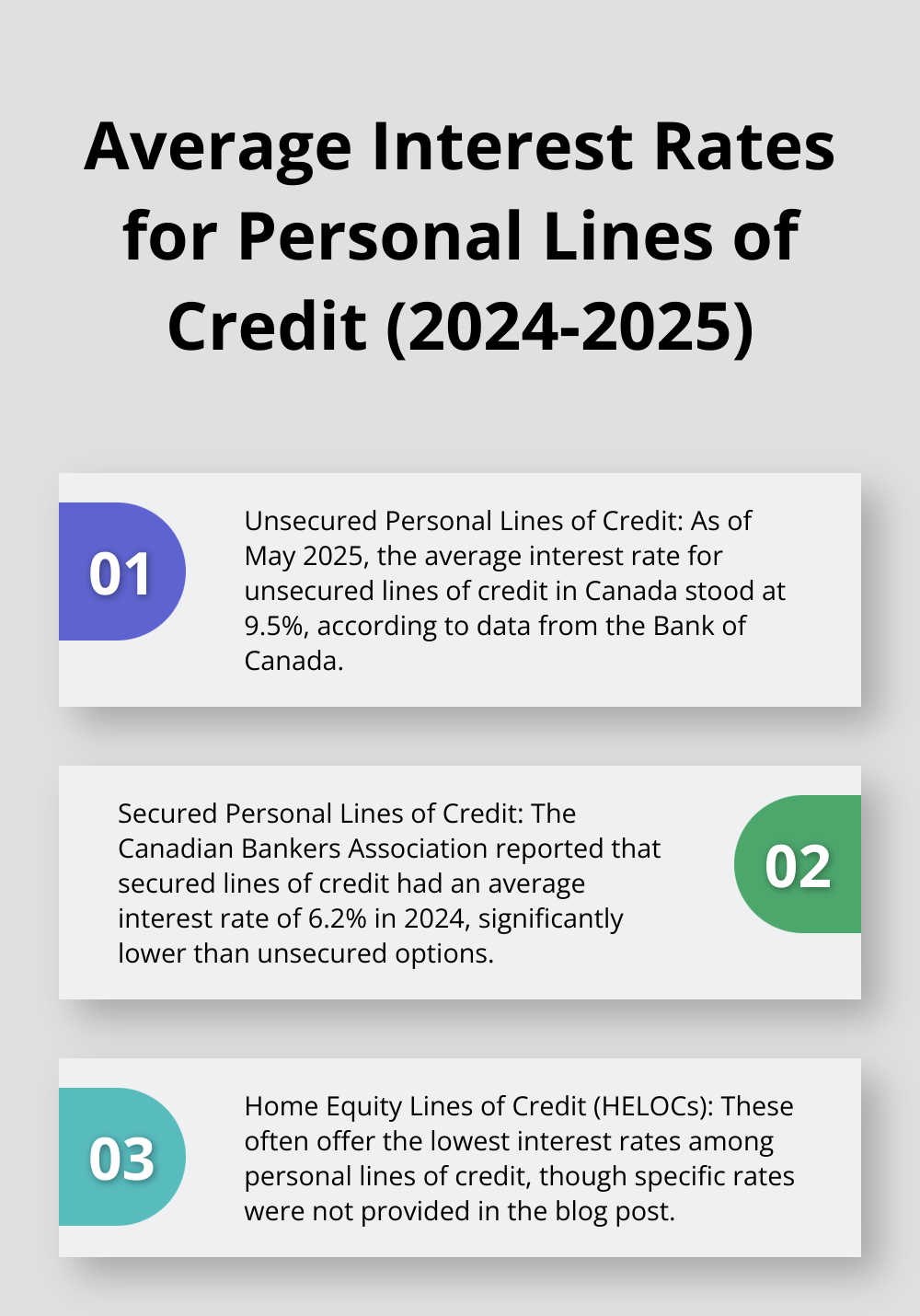

Unsecured personal lines of credit don’t require collateral. Lenders base these primarily on your creditworthiness. Generally, a credit score of 660 and over is considered good in Canada. However, interest rates tend to be higher due to the increased risk for lenders. As of May 2025, the average interest rate for unsecured lines of credit in Canada stood at 9.5% (according to data from the Bank of Canada).

To qualify for an unsecured line of credit, you typically need a credit score of at least 650. Some lenders may require higher scores for better rates. Check your credit score first and take steps to improve it if necessary before applying for an unsecured line of credit.

Secured Personal Lines of Credit

Secured personal loans require collateral, such as a vehicle or investment account. This collateral reduces the lender’s risk, often resulting in lower interest rates. The Canadian Bankers Association reported that secured lines of credit had an average interest rate of 6.2% in 2024, significantly lower than unsecured options.

When you consider a secured line of credit, assess the value of your potential collateral. Lenders typically offer credit limits up to 80% of the collateral’s value. For example, if you have a $50,000 investment portfolio, you might qualify for a $40,000 line of credit.

Home Equity Lines of Credit (HELOCs)

HELOCs are a specific type of secured line of credit that uses your home’s equity as collateral. They often offer the lowest interest rates among personal lines of credit. Rising interest rates have created financial challenges for mortgage holders, according to CMHC’s Residential Mortgage Industry Report.

To qualify for a HELOC, you need at least 20% equity in your home. The maximum amount you can borrow is typically 65% of your home’s value, minus any outstanding mortgage balance. For instance, if your home is worth $500,000 and you owe $300,000 on your mortgage, your maximum HELOC limit would be $25,000 (65% of $500,000 = $325,000, minus $300,000 mortgage).

HELOCs offer significant borrowing power but come with risks. If you default, you could lose your home. Always consider your ability to repay before taking out a HELOC.

Choosing the Right Type

The type of personal line of credit you choose depends on your financial situation, credit score, and available assets. Unsecured lines offer flexibility but come with higher rates. Secured lines (including HELOCs) provide lower rates but require collateral.

Try to match your needs with the features of each type. If you have a high credit score and prefer not to risk assets, an unsecured line might be best. If you own a home and want the lowest possible rate, a HELOC could be ideal.

As you weigh your options, consider consulting with financial experts to help you make an informed decision. The right choice can provide financial flexibility and peace of mind. Now, let’s explore the advantages and disadvantages of personal lines of credit to give you a complete picture of this financial tool.

The Pros and Cons of Personal Lines of Credit

Flexibility: A Double-Edged Sword

Personal lines of credit offer significant flexibility. You can borrow what you need, when you need it, up to your credit limit. This feature proves particularly useful for managing irregular expenses or funding ongoing projects with uncertain costs.

However, this flexibility can lead to overspending. A 2024 study by the Financial Consumer Agency of Canada found that 35% of line of credit users had difficulty tracking their spending and repayments. To avoid this pitfall, create a clear repayment plan before you borrow and stick to it rigorously.

Interest Rates: Lower Than Credit Cards, But Variable

According to a recent report, rates of arrears on credit cards and auto loans have risen further for households without a mortgage. This suggests that personal lines of credit may still offer advantages in terms of interest rates compared to credit cards.

However, these rates are usually variable, which means they can fluctuate with market conditions. In a rising interest rate environment, your borrowing costs could increase unexpectedly. Always factor in potential rate increases when you plan your repayments.

Impact on Credit Score: A Balancing Act

Using a personal line of credit responsibly can positively impact your credit score. Regular, on-time payments and maintaining a low credit utilization ratio (ideally below 30%) can boost your creditworthiness.

On the flip side, maxing out your credit line or missing payments can severely damage your credit score. A 2024 TransUnion study revealed that consumers who consistently used more than 70% of their available credit saw an average drop of 30 points in their credit score over six months.

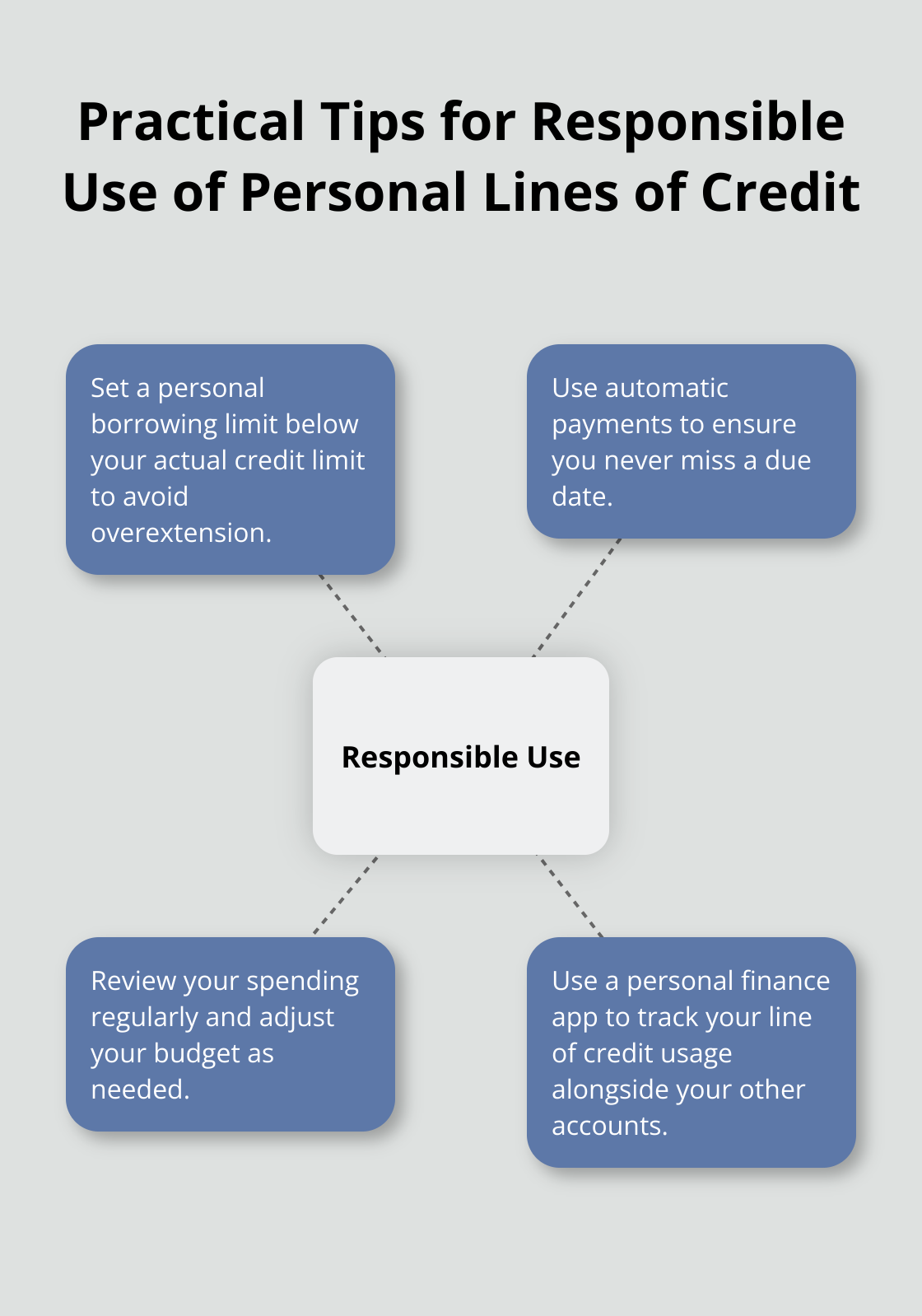

Practical Tips for Responsible Use

To maximize the benefits and minimize the risks of a personal line of credit, consider these practical tips:

Comparing Offers

Personal lines of credit can be powerful financial tools, but they require careful management. If you consider this option, compare offers from various lenders to find the best terms for your situation. The key to successfully using a personal line of credit lies in understanding its features and using them to your advantage while avoiding potential pitfalls.

Final Thoughts

Personal lines of credit provide flexible financial tools for Canadians who seek adaptable borrowing options. These revolving credit accounts allow users to access funds as needed, with interest charged only on the amount used. When you consider what a personal line of credit is and if it suits your needs, reflect on your financial goals and circumstances.

Financial Canadian can help you navigate the application process for a personal line of credit. Our expert team will ensure you understand all terms and conditions, empowering you to make informed financial decisions. We also offer comprehensive web design services to help businesses establish a strong online presence.

A personal line of credit can become a valuable addition to your financial toolkit if you use it wisely. You can leverage this financial instrument to support your goals and maintain financial flexibility. Understanding its features, benefits, and potential risks will help you make the most of this borrowing option.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment