At Financial Canadian, we often get asked about the differences between credit cards and personal loans. These two financial products serve distinct purposes and come with their own set of advantages and drawbacks.

In this post, we’ll break down the key features of credit cards and personal loans, helping you make an informed decision about which option might be best for your financial needs.

How Credit Cards Work in Canada

The Basics of Credit Card Operations

Credit cards are popular financial tools in Canada, offering convenience and flexibility for everyday purchases. When you use a credit card, you borrow money from the card issuer. You have a predetermined credit limit, which is the maximum amount you can spend. Credit card companies determine this limit through a complex underwriting process involving mathematical formulas and extensive testing. Each month, you receive a statement showing your purchases and the minimum payment due. If you pay the full balance by the due date, you typically avoid interest charges. However, if you carry a balance, the card issuer charges interest on the unpaid amount.

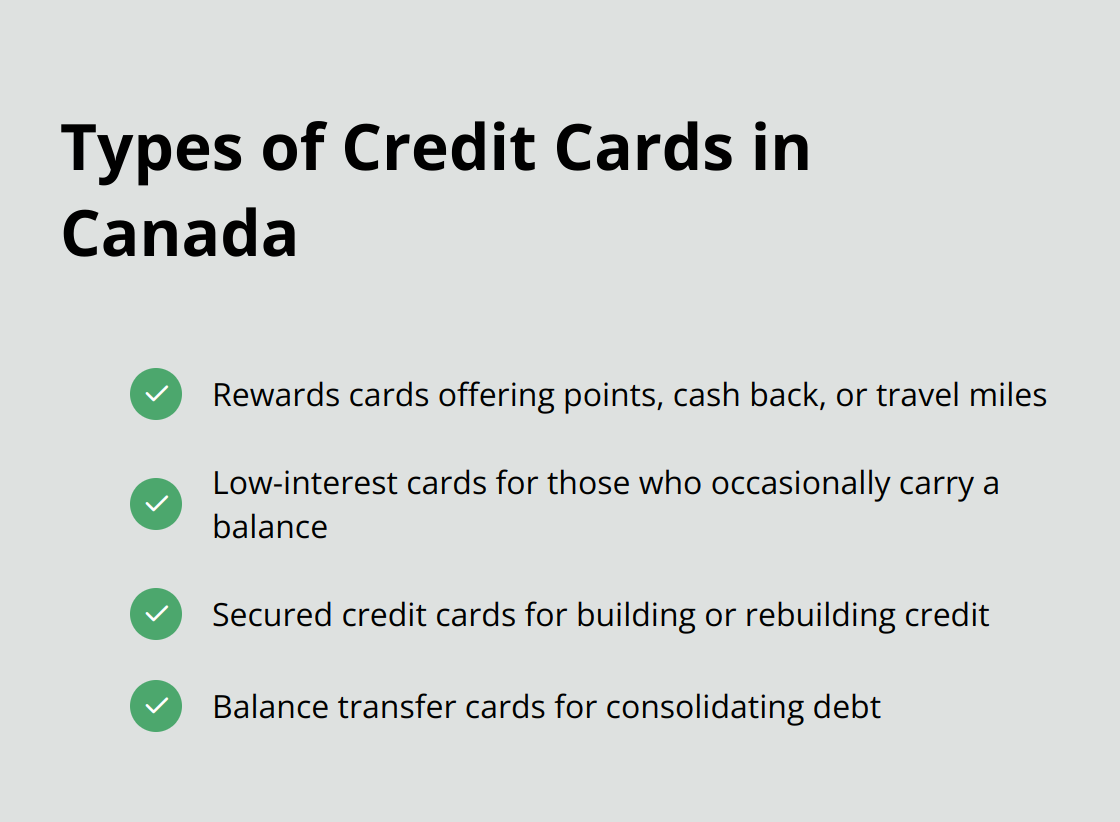

Types of Credit Cards in Canada

Canada offers a diverse range of credit cards to suit different needs and lifestyles. Rewards cards are particularly popular, allowing cardholders to earn points, cash back, or travel miles on their purchases. Some cards offer up to 5% cash back on specific categories like groceries or gas.

Other types of credit cards include:

- Low-interest cards (for those who occasionally carry a balance)

- Secured credit cards (for individuals looking to build or rebuild their credit)

- Balance transfer cards (useful for consolidating debt, often offering promotional 0% interest periods for up to 12 months)

The Advantages of Credit Cards

Credit cards provide several benefits:

- Convenient way to make purchases, especially online or when traveling

- Purchase protection and extended warranties on items bought with the card

- Potential to build your credit score when used responsibly

- Rewards programs (points, cash back, or travel miles)

- Fraud protection (limited liability for unauthorized charges)

The Drawbacks of Credit Cards

Despite their benefits, credit cards come with potential drawbacks:

- High interest rates (averaging around 19.5% in Canada as of 2025)

- Late payment fees and potential damage to your credit score

- Risk of overspending (the “buy now, pay later” model can lead to accumulating debt if not managed carefully)

- Annual fees (some premium rewards cards charge $100+ per year)

Choosing the Right Credit Card

To select the best credit card for your needs, consider the following factors:

- Your spending habits and financial goals

- The card’s interest rate and fees

- Rewards programs and their alignment with your lifestyle

- Additional perks (travel insurance, concierge services, etc.)

- Your credit score (which affects your eligibility for certain cards)

Credit cards can be powerful financial tools when used wisely. The key is to understand how they work and choose the right card for your needs. In the next section, we’ll explore personal loans and how they differ from credit cards as a borrowing option.

Personal Loans Demystified

What Are Personal Loans?

Personal loans provide borrowers with a lump sum of money that they repay over a fixed term. Unlike credit cards, personal loans offer a set amount of funds upfront, typically ranging from $1,000 to $50,000, with repayment periods usually between one to seven years.

How Personal Loans Function

When you take out a personal loan, you agree to repay the borrowed amount plus interest in fixed monthly installments. The interest rate on personal loans in Canada varies widely, from as low as 5% to as high as 47%, depending on factors such as your credit score, income, and the lender’s policies. It’s important to compare offers from multiple lenders to secure the best rate.

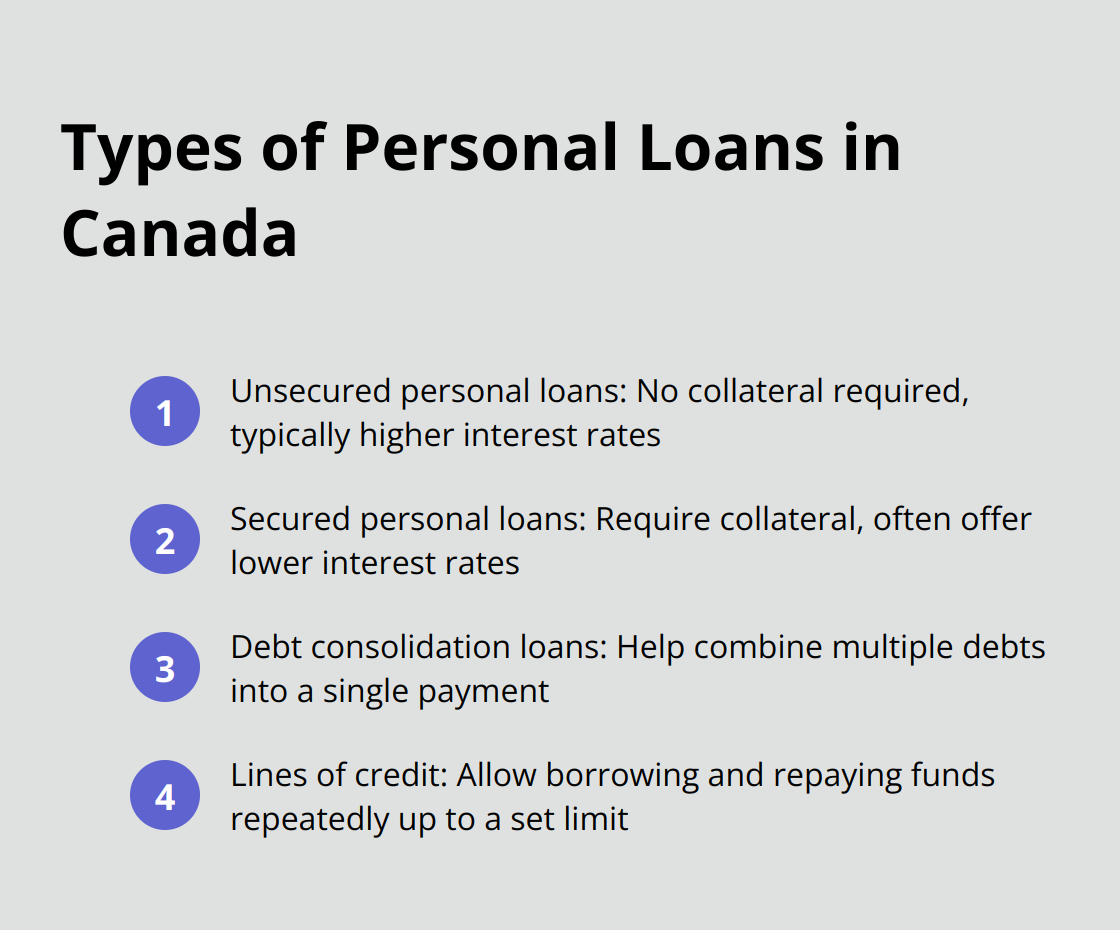

Types of Personal Loans in Canada

Canada offers several types of personal loans:

Advantages of Personal Loans

Personal loans offer several benefits over other forms of borrowing:

- Lower interest rates than credit cards (making them a good option for large purchases or debt consolidation)

- Fixed repayment terms (which help with budgeting)

- Potential positive impact on credit score (through regular, on-time payments)

A line of credit gives you ongoing access to funds that you can use and re-use as needed. You’re charged interest only on the amount you use.

Considerations and Drawbacks

While personal loans can benefit many borrowers, they also come with potential drawbacks:

- Fixed repayment schedule (which commits you to payments even if your financial situation changes)

- Missed payments can damage your credit score and lead to additional fees

- Origination fees (which can range from 1% to 8% of the loan amount)

It’s essential to factor in these costs when comparing loan offers. Try to assess your financial situation and needs thoroughly before deciding on a personal loan.

Now that we’ve explored personal loans in detail, let’s compare them directly with credit cards to help you make the best choice for your financial needs.

Credit Cards vs Personal Loans: Which Is Right for You?

Interest Rates and Fees

Credit cards and personal loans have different interest rate structures. In Canada, credit card interest rates can vary, and the market is expected to grow in 2025 amid lower cost of living and interest rates, according to TransUnion. Personal loan rates can be much lower, starting from 5% for borrowers with excellent credit scores.

However, interest rates aren’t the only consideration. Credit cards often include additional fees such as annual fees, balance transfer fees, and cash advance fees. Personal loans may have origination fees, which are nonrefundable fees associated with lending arrangements.

Repayment Terms and Flexibility

Credit cards offer more flexibility in repayment. You can choose to pay the minimum amount due each month or pay off the entire balance. However, this flexibility can result in prolonged debt if you consistently only pay the minimum.

Personal loans have fixed repayment terms, usually ranging from one to seven years. You’ll know exactly how much you need to pay each month and when the loan will be fully repaid. This structure can benefit budgeting and help avoid the temptation to only make minimum payments.

Impact on Credit Score

Credit cards and personal loans affect your credit score differently. Credit cards influence your credit utilization ratio (the amount of credit you’re using compared to your credit limit). Try to keep this ratio below 30% for a good credit score.

Personal loans, being installment credit, don’t affect your credit utilization ratio. However, they impact your credit mix, which accounts for 10% of your FICO score. Having a mix of different types of credit (revolving and installment) can positively impact your score.

Timely payments are crucial for both options. Late payments on either credit cards or personal loans can significantly damage your credit score.

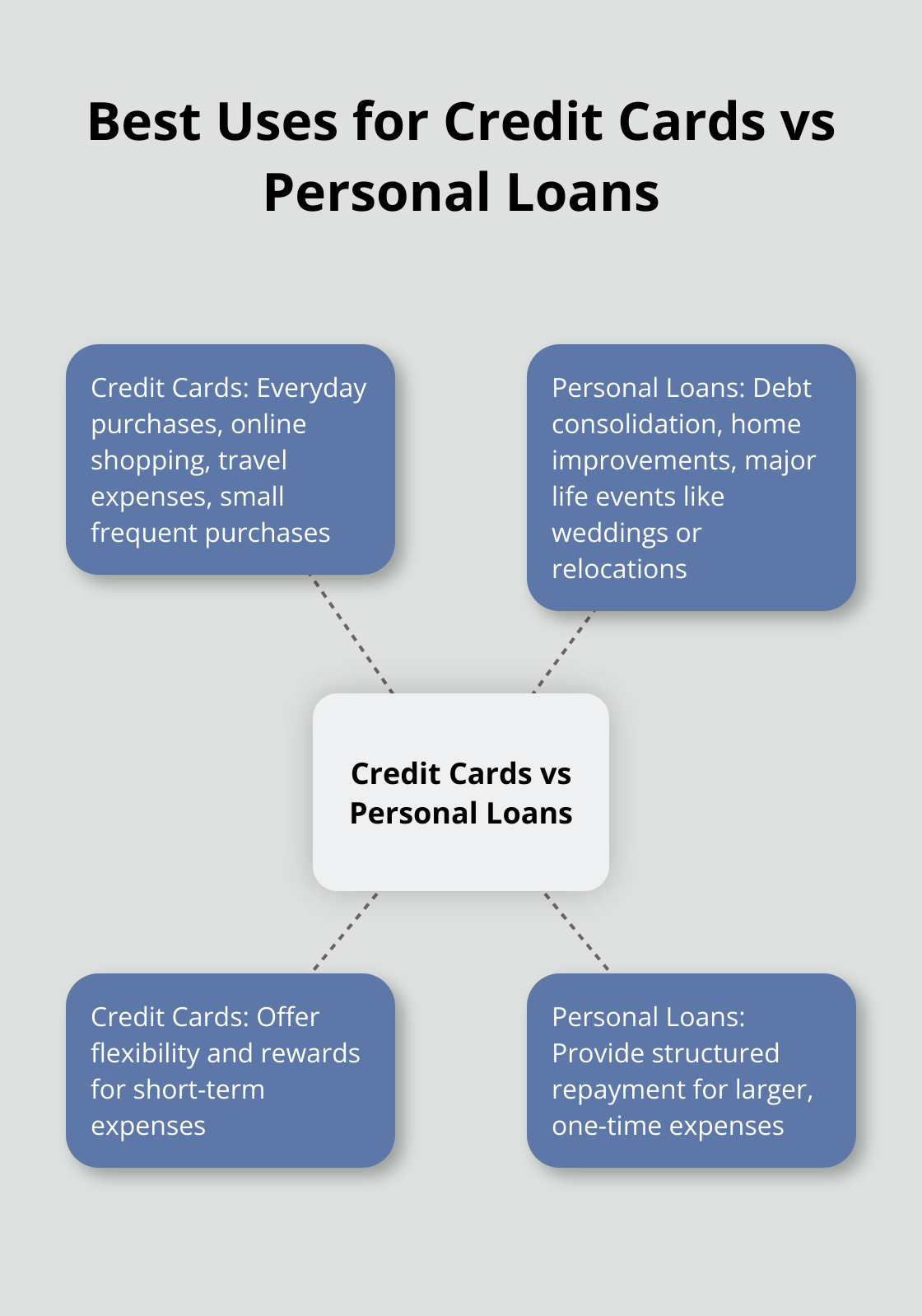

Best Uses for Credit Cards and Personal Loans

The best choice between a credit card and a personal loan depends on your specific financial situation, the purpose of the funds, and your ability to repay. Always compare offers from multiple lenders and consider factors beyond just the interest rate when making your decision.

Final Thoughts

Credit cards and personal loans serve different financial needs. Credit cards offer flexibility for everyday spending and rewards, while personal loans provide structured repayment for larger expenses. Your choice depends on your financial situation, borrowing purpose, and repayment ability.

Your credit score influences your options and rates for both credit cards and personal loans. Compare offers from multiple lenders, considering interest rates, fees, repayment terms, and additional benefits. Responsible use of either option can improve your credit score over time.

At Financial Canadian, we understand the importance of informed financial decisions. We specialize in web design services to help businesses establish a strong online presence. Our goal is to empower clients with financial knowledge and digital solutions for success in today’s landscape.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment