Buying a home in Canada involves navigating mortgages, down payments, and qualification requirements that can feel overwhelming. We at Financial Canadian break down mortgages Canada explained so you understand exactly what to expect before you apply.

This guide walks you through the types of mortgages available, what lenders look for, and the steps from pre-approval to closing day. You’ll have the concrete information you need to move forward with confidence.

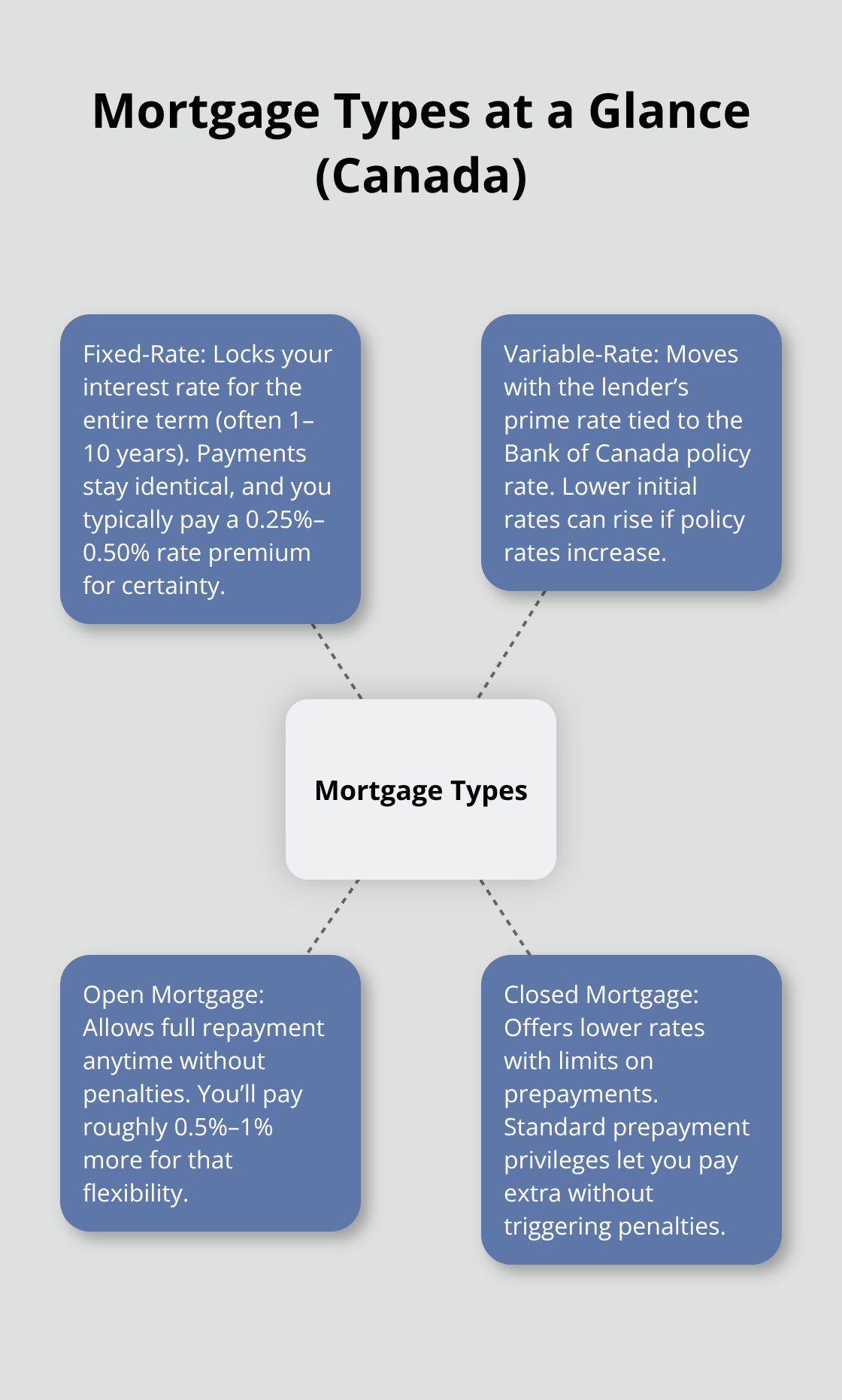

Types of Mortgages Available in Canada

Fixed-Rate Mortgages Lock Your Payment in Place

Fixed-rate mortgages eliminate interest rate risk by locking your rate for the entire term, typically ranging from one to ten years. Your monthly payment stays identical whether rates rise or fall, providing complete payment predictability. Fixed rates typically run 0.25% to 0.50% higher than variable rates when you sign, so you pay for that security upfront. This premium protects you if the Bank of Canada raises its policy rate-a real concern given recent rate movements.

Fixed-rate mortgages dominate Canadian borrowing because they eliminate guesswork from your budget. When rates rise, fixed-rate borrowers keep their original rate while variable-rate borrowers face payment increases. Most Canadian homeowners choose fixed rates for this reason: they want certainty, not surprises.

Variable-Rate Mortgages Follow Market Movements

Variable-rate mortgages tie your interest rate to the lender’s prime rate, so your payment fluctuates as the Bank of Canada adjusts its policy rate. The current policy rate sits at 3.75% as of March 2026, down from the 5% peak in 2022, which affects how attractive variable rates appear compared to fixed options. Variable-rate mortgages make sense only if you can absorb payment increases without financial strain and plan to sell or refinance within five years.

These mortgages appeal to borrowers with flexible budgets and short time horizons. If you expect a promotion, inheritance, or bonus income within a few years, variable rates reward your confidence with lower initial payments.

Open and Closed Mortgages Differ in Flexibility

Open mortgages let you pay off the entire balance without penalty at any time, while closed mortgages restrict prepayment options but offer lower rates as compensation. Open mortgages suit buyers who expect significant life changes or sudden windfalls that allow early payoff, though the 0.5% to 1% rate premium stings over time. Closed mortgages represent the practical choice for most Canadians because they balance reasonable rates with standard flexibility through closed mortgages prepayment privileges that allow overpayments without triggering penalties.

Your choice ultimately depends on your risk tolerance and timeline-not on market predictions or rate forecasts that nobody can accurately make. Understanding mortgage insurance requirements and comparing available options helps you select the right mortgage structure for your situation.

How to Qualify for a Mortgage in Canada

Your Credit Score Determines Your Rate

Lenders require a credit score above 620 to approve most mortgages in Canada, though scores above 700 qualify you for better rates and more flexible terms. Scores between 620 and 680 attract 0.5% to 1.5% higher rates than excellent credit profiles. This penalty compounds significantly over a 25-year mortgage, so improving your score before applying makes far more financial sense than accepting a punitive rate. Check your credit report with Equifax or TransUnion to identify errors or missed payments that drag your score down.

Income and Debt-to-Income Ratio Set Your Borrowing Limit

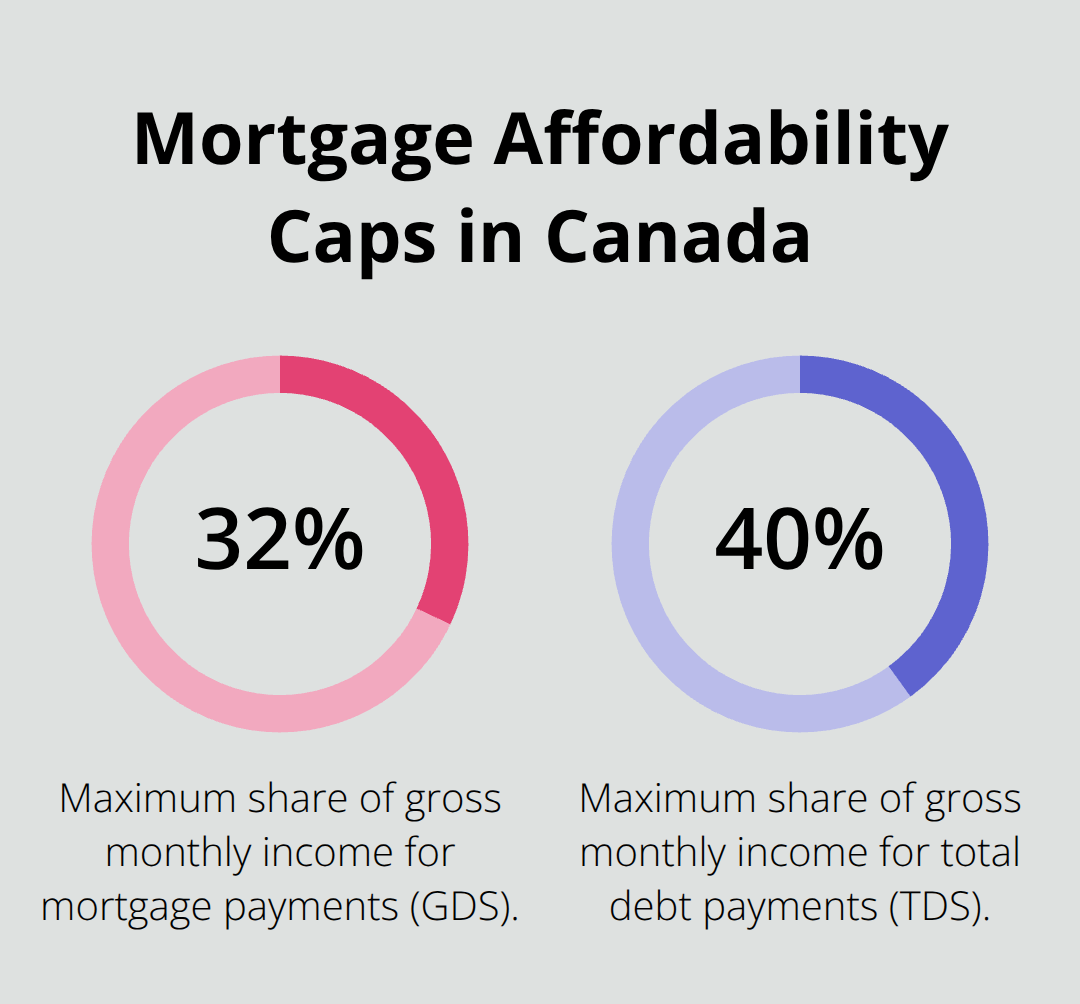

Lenders calculate your debt-to-income ratio using your gross monthly income and existing debt obligations to determine how much you can borrow. Most Canadian lenders cap your mortgage payment at 32% of your gross monthly income, and your total debt payments (mortgage, car loans, credit cards, student loans) cannot exceed 40% of that income. A borrower earning $6,000 monthly should keep mortgage payments below $1,920. Someone earning $50,000 annually can typically afford a mortgage payment around $1,300 monthly, which translates to roughly $260,000 in borrowing power at current rates.

Down Payment Size and CMHC Insurance

The down payment requirement depends on your purchase price: you need 5% down on the first $500,000 of your home’s value, then 10% on the portion between $500,000 and $999,999. Down payments below 20% trigger mandatory mortgage loan insurance through CMHC, which adds between 2% and 4% to your mortgage balance depending on your down payment percentage. A 10% down payment costs roughly 3.1% in insurance, while a 15% down payment costs approximately 2.8%, so the difference between these two options saves you several thousand dollars over your mortgage term.

Understanding these three qualification factors positions you to move forward with your mortgage application. The next step involves getting pre-approved so you know your exact borrowing power before you start house hunting.

The Mortgage Application Process

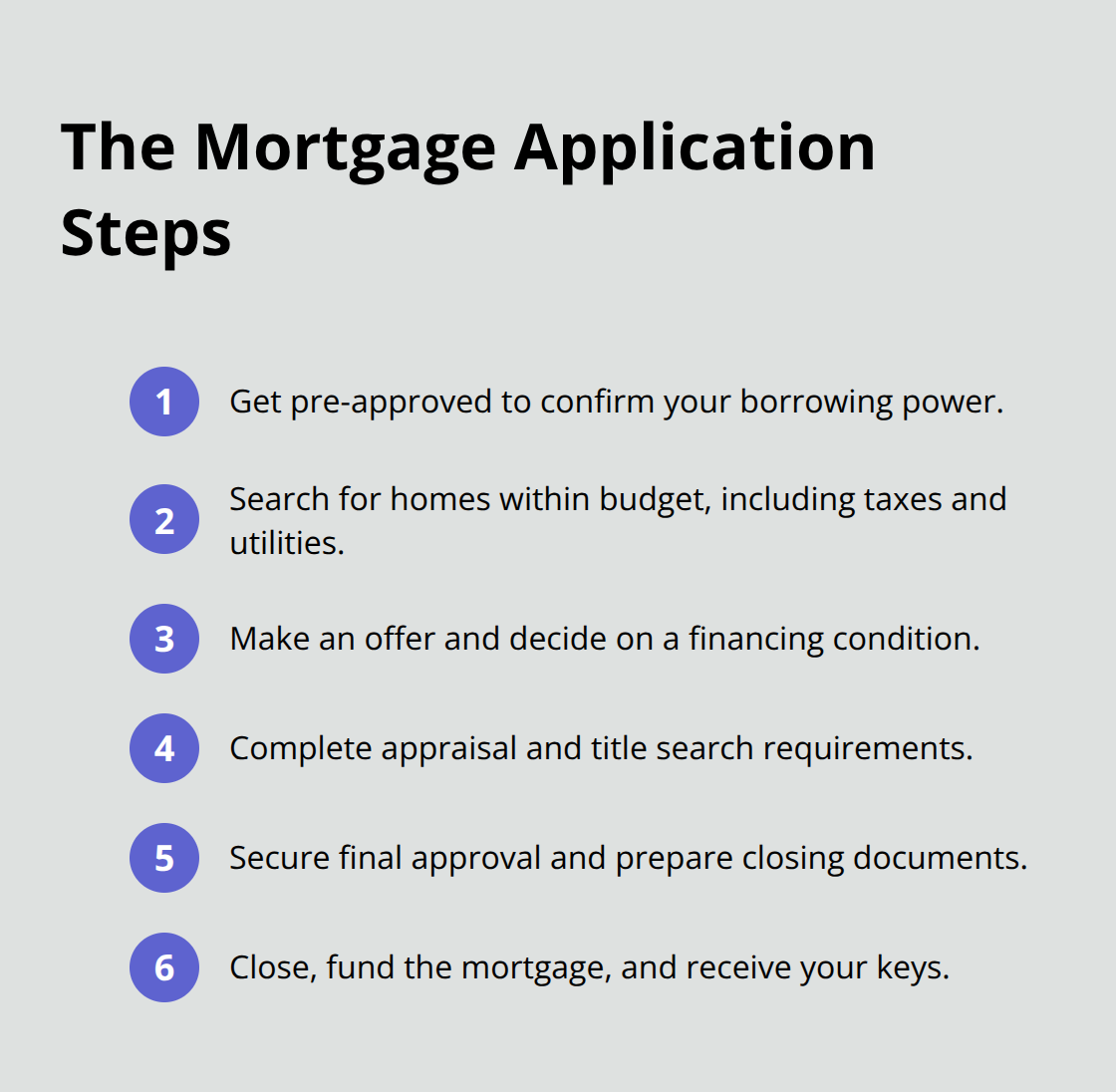

Get Pre-Approved to Know Your Borrowing Power

Pre-approval should happen before you spend a single dollar on a house search. A lender reviews your credit, income, and debts and confirms exactly how much you can borrow. This process typically takes three to five business days and costs nothing. Armed with a pre-approval letter showing your maximum borrowing power, you enter the housing market with concrete numbers instead of guesses. Real estate agents take pre-approved buyers seriously because they know the financing will actually close.

During pre-approval, lenders request recent pay stubs, two years of tax returns, recent bank statements, and a list of your debts. Self-employed borrowers need additional documentation including financial statements and notice of assessments. Bring your credit report from Equifax or TransUnion to correct any errors before the lender pulls their own report. Your pre-approval remains valid for 120 days in most cases, so timing matters if you plan a delayed search. Some lenders offer rate holds that lock your approved rate for 30 to 120 days, protecting you from rate increases between pre-approval and final approval (this protection costs nothing and provides valuable insurance against market movements during your house hunt).

Search for Properties Within Your Budget

House hunting with pre-approval in hand shifts your focus to finding a property that matches both your budget and your lifestyle needs. Tour homes within your approved borrowing range and consider factors beyond the mortgage payment: property taxes, home insurance, maintenance costs, and utilities add hundreds of dollars monthly to your true housing expense. A home at your maximum approved price may leave no room for these additional costs or unexpected repairs. Try for mortgages representing 80% of your pre-approved amount, creating breathing room for life’s surprises.

When you find a property you want, your real estate agent prepares an offer that includes your pre-approval letter as proof you can close the deal. Making an offer triggers the most critical decision point before final approval. You must decide whether to include a financing condition that allows you to back out if your lender rejects the mortgage application. In competitive markets with multiple offers, sellers demand unconditional offers from pre-approved buyers, meaning you lose your deposit if financing falls through. This risk is real but manageable if your pre-approval was thorough. Only remove financing conditions if your pre-approval came with a rate hold and the lender confirmed no additional documentation is needed.

Complete the Appraisal and Title Search

Final approval happens after the property is under contract and the lender orders a property appraisal to confirm the home’s value supports your mortgage amount. This appraisal typically costs $300 to $500 and takes 10 to 14 days. If the appraisal comes in lower than your purchase price, you face a difficult choice: increase your down payment, renegotiate the purchase price, or walk away. This scenario occurs in roughly 5% to 10% of transactions, so it remains a real possibility despite pre-approval.

Your lender also orders a title search to confirm the seller actually owns the property and no liens or claims exist against it. Title insurance costs approximately $150–$800. Sellers increasingly demand home inspections within 10 days and final approval within 30 days, so your timeline compresses significantly once your offer is accepted.

Close the Deal and Receive Your Keys

The final week before closing involves a property inspection, a final walkthrough to confirm the seller completed promised repairs, and a meeting with your lawyer or notary to review closing documents. Your lawyer prepares the mortgage deed, reviews the purchase agreement, and handles the money transfer on closing day. Closing costs including legal fees, title insurance, property tax adjustments, and lender fees typically range from 1.5% to 4% of your purchase price (a $400,000 home purchase costs $6,000 to $16,000 in closing costs, so budget accordingly).

On closing day, funds transfer to the seller’s lawyer, documents are signed and registered, and the keys officially become yours. Most lenders fund the mortgage within 24 hours of closing, completing your transition from renter to homeowner.

Final Thoughts

Mortgages Canada explained comes down to three concrete factors: your credit score determines your rate, your debt-to-income ratio caps your borrowing at 32% of gross income, and your down payment size triggers CMHC insurance costs between 2% and 4%. These numbers matter far more than market predictions or rate forecasts that shift weekly. A borrower with a 650 credit score and 10% down faces different options than someone with a 750 score and 20% down, so your personal qualification determines your path forward.

If you haven’t checked your credit score, pull your report from Equifax or TransUnion today and correct any errors before approaching lenders. If you’re ready to move forward, contact a lender for pre-approval within the next week so you know your exact borrowing power. Pre-approval takes three to five business days and costs nothing, yet it transforms your house search from guessing to precision.

We at Financial Canadian help you compare mortgage rates and understand your options across lenders. Your path to homeownership starts with accurate information and honest assessment of your finances, not wishful thinking about rates or market conditions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment