Your credit score shapes whether you get approved for a mortgage, car loan, or credit card-and what interest rate you’ll pay. At Financial Canadian, we’ve created this Canada credit score guide to help you understand exactly how your score works, where to check it for free, and what steps actually move the needle.

The difference between a score of 650 and 750 can cost you thousands in interest over the life of a loan. That’s why knowing how to check, monitor, and improve your score matters.

How Your Credit Score Gets Calculated in Canada

The Two Bureaus That Control Your Score

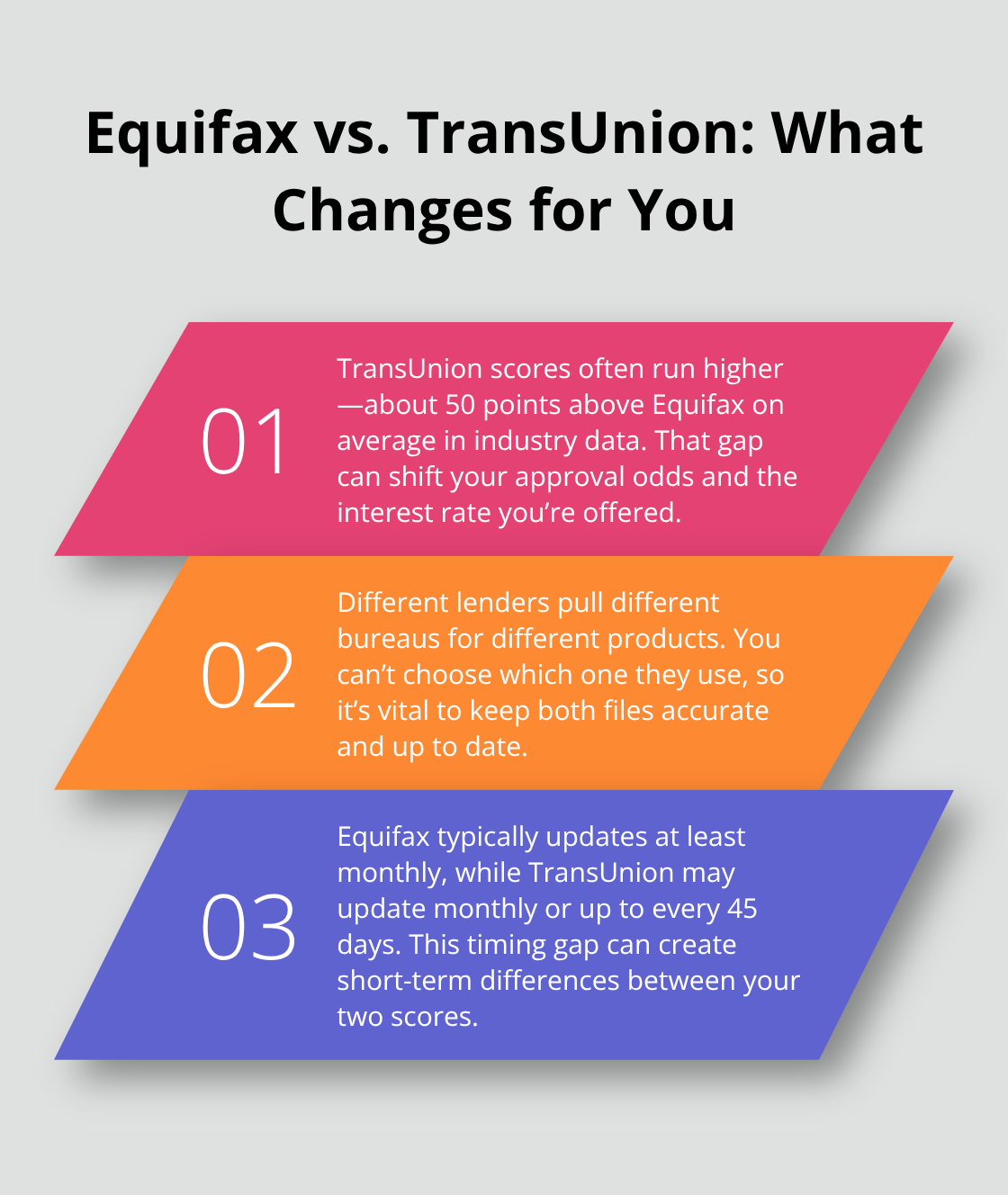

Your credit score is a three-digit number between 300 and 900 that lenders use to decide whether you qualify for credit and what interest rate you’ll pay. In Canada, two national credit bureaus collect your financial data and generate scores: Equifax and TransUnion. Here’s what most people miss-these two bureaus don’t always report the same information. Lenders report to different bureaus, so a loan appearing on your Equifax file might not show up on TransUnion. This means your score can differ by as much as 100 points between the two bureaus.

According to industry data from Neo Financial, TransUnion scores tend to run about 50 points higher than Equifax scores. When you apply for a mortgage, a lender might pull from Equifax, but a credit card issuer pulls from TransUnion. You can’t control which bureau a lender checks, which is why you need accurate information on both files. Equifax updates at least monthly, while TransUnion updates monthly or up to every 45 days.

The longer the delay, the more outdated your information becomes on one bureau while the other catches up.

What Factors Actually Move Your Score

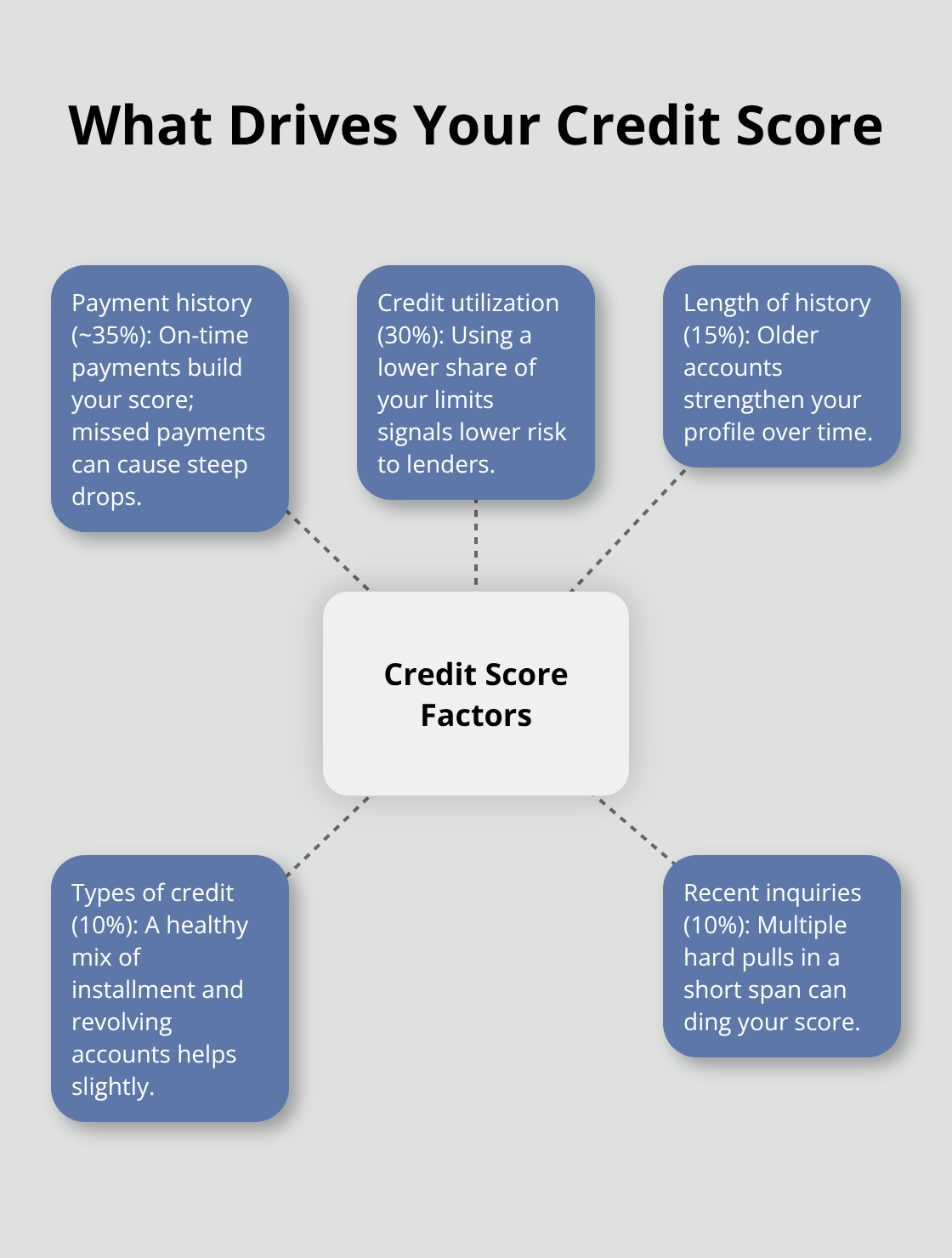

Both bureaus weight your credit data using similar categories: payment history (~35%), credit utilization (30%), length of credit history (15%), types of credit (10%), and recent inquiries (10%). However, the exact weights differ between bureaus and change over time. Payment history is the heaviest factor, meaning missed payments destroy your score far more than high balances do. Credit utilization measures how much of your available credit you use-if you have a $5,000 limit and carry a $4,000 balance, that’s 80% utilization, which damages your score. Lenders see high utilization as a sign you’re desperate for credit.

The length of your credit history matters too, which is why closing old credit cards hurts your score even after you’ve paid them off. A closed account stops building history but stays on your report for years. Hard inquiries happen when you apply for credit and a lender pulls your file; too many in a short period signals you’re hunting for credit aggressively. Soft inquiries, like checking your own score, don’t affect your rating.

Understanding Your Score Range

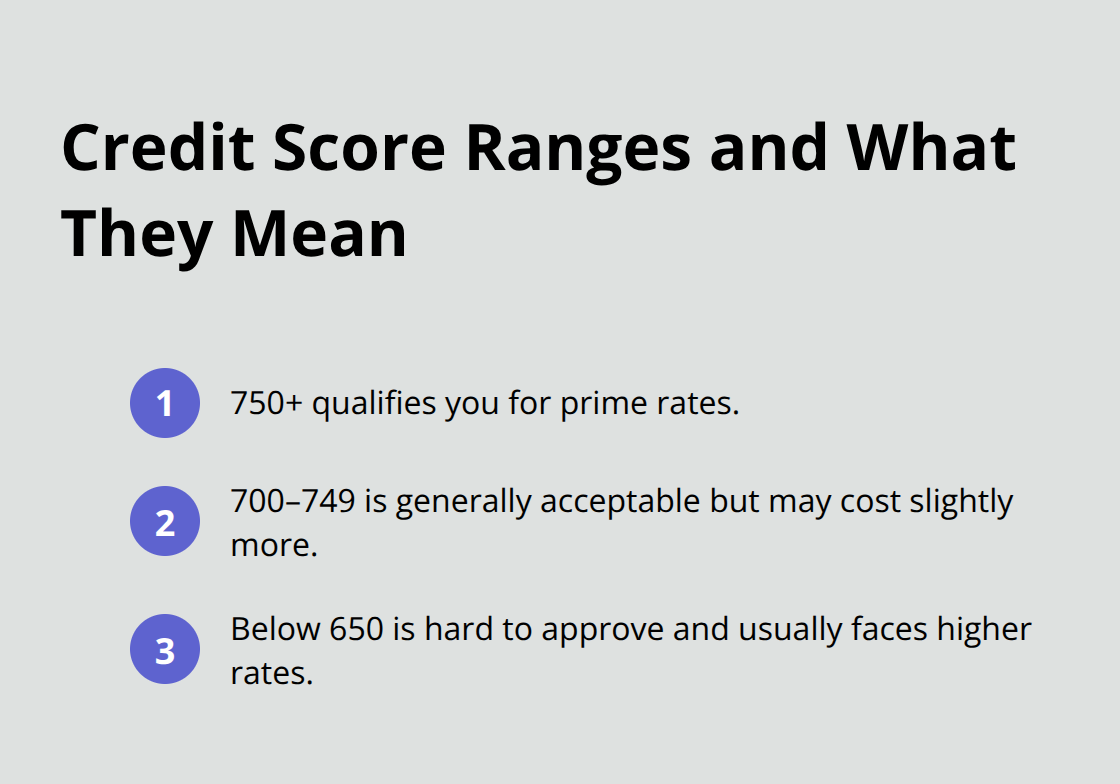

A score above 750 qualifies you for prime rates on mortgages and loans. Between 700 and 749, you’re acceptable but may pay slightly higher rates. Below 650, approval becomes difficult and rates climb sharply.

You can get your credit score and report free once per year from each bureau through myEquifax or TransUnion’s online portal, or by requesting by mail or phone. Since these two bureaus maintain separate files with different update schedules, checking both reports annually helps you spot errors and understand why lenders might treat you differently depending on which bureau they pull from.

Checking Your Credit Score for Free

Getting your credit score requires no paid subscription or credit card application. Canadians can request a free credit report from each bureau once per year through official channels. Equifax offers access via myEquifax online, while TransUnion provides reports through their online portal, by mail, or by phone. You can also visit annualcreditreport.com to request your free annual report. Since Equifax and TransUnion maintain separate files with different update schedules, checking both reports annually gives you an accurate picture of your credit health. Many people check only one bureau and miss errors or outdated information on the other. The VantageScore 3.0 model is commonly used, though different lenders may use different scoring models entirely. This means your score from one source might differ from what a lender actually sees when you apply. Request both reports in the same month each year so you have a consistent timeline for monitoring changes. When you pull your own reports, it counts as a soft inquiry and does not affect your score at all.

What Your Report Actually Contains

Your credit report lists every credit account you’ve opened, closed, or defaulted on, along with payment history for the past six years. Negative accounts stay on your report for six years from the date they first went delinquent, which is longer than most people realize. The report shows your current balances, credit limits, payment status for each account, and any collections or legal actions against you. Hard inquiries appear when lenders pull your file during a credit application; too many within months signals you’re desperately seeking credit. Rent payment reporting has grown significantly in Canada through services like Borrowell Rent Advantage and FrontLobby, which report to Equifax, so your rental history may now boost your score if you pay on time.

Finding and Fixing Errors on Your Report

Check your report carefully for errors like accounts you didn’t open, incorrect payment statuses, or duplicate entries. Disputing errors is free and straightforward through either bureau’s online portal or by mail. Errors happen frequently enough that checking both reports annually catches problems before they damage your approval odds on a mortgage or major loan. A single error-such as a payment marked late when you paid on time-can lower your score by 50 points or more. The bureaus must investigate your dispute within 30 days and remove inaccurate information if they cannot verify it. Once you identify errors, act on them immediately rather than waiting for the next annual check. The sooner you correct mistakes, the sooner your score recovers and lenders see your true creditworthiness.

How to Actually Improve Your Credit Score

Pay Bills on Time to Build Score Momentum

The fastest way to raise your score is to pay every bill on time, starting immediately. Payment history accounts for roughly 35% of your credit score, which means a single missed payment can drop your score by 100 points or more. Set up automatic payments for at least the minimum on every credit account-credit cards, loans, utilities, phone bills, anything that reports to the bureaus. If you’ve already missed payments, the damage fades over time; a missed payment from two years ago hurts far less than one from last month. Consistent on-time payments for six months typically raise your score by 50 to 100 points.

Lower Your Credit Card Balances Aggressively

The second lever is reducing your credit card balances aggressively. Credit utilization (how much of your available credit you actually use) makes up 30% of your score. If you have a $10,000 total credit limit across all cards and carry $8,000 in balances, you’re at 80% utilization-a score killer. Dropping that to $2,000 (20% utilization) can boost your score by 40 to 80 points within one or two billing cycles because the bureaus update monthly or every 45 days. Paying down existing debts works faster than waiting for on-time payments to accumulate, so if you’re in a hurry to improve your score before applying for a mortgage or major loan, focus here first.

Dispute Errors and Manage Hard Inquiries

Dispute errors on your credit report the moment you spot them. Pull both your Equifax and TransUnion reports once per year through their official channels and compare them side by side for discrepancies. A single error-a payment marked late when you paid on time, a duplicate account, or an account you never opened-can tank your score by 50 points. The bureaus must investigate disputes within 30 days and remove information they cannot verify, so don’t assume errors will fix themselves. Hard inquiries from credit applications also chip away at your score for about six months, so space out applications for new credit by at least three months. Avoid applying for multiple credit cards or loans within a short window; each application triggers a hard inquiry that signals desperation to lenders.

Keep Old Credit Cards Open

If you’re tempted to close old credit cards after paying them off, resist that urge. Closing a card reduces your total available credit and lowers your utilization ratio, which damages your score even though the account stays on your report for years. Keep old cards open with zero balances instead. These three actions-paying on time, lowering utilization, and disputing errors-move the needle fastest and cost nothing to execute.

Final Thoughts

Three actions move your credit score faster than anything else: pay bills on time, lower your credit card balances, and fix errors on your reports. Payment history drives 35% of your score, so one missed payment can cost you 100 points, while reducing credit utilization from 80% to 20% boosts your score by 40 to 80 points in a single billing cycle. Disputing errors takes minutes but often yields 50-point gains, and these steps cost nothing to execute.

A higher credit score translates directly to lower interest rates on mortgages, car loans, and credit cards-the difference between a 650 and 750 score saves you thousands of dollars over the life of a loan. Lenders approve applications faster when your score sits above 750, and you gain access to better terms and higher credit limits. A strong score also affects your ability to rent apartments, secure employment in certain industries, and negotiate better insurance rates.

Start by requesting your free annual reports from both Equifax and TransUnion right now, then compare them side by side for errors and dispute anything inaccurate. Set up automatic payments for at least the minimum on every account, and if you carry high balances, make it your priority to pay them down before applying for major credit. Check both reports again in six months to track your progress, and visit Financial Canadian to explore tools and guidance tailored to your needs as you work through this Canada credit score guide.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment