Personal loans Canada rates swing wildly depending on who you borrow from and your financial profile. A rate that works for one borrower might cost another thousands in extra interest.

At Financial Canadian, we break down what these averages actually mean for your wallet and show you how to find better terms.

Personal Loan Rates in Canada Right Now

Canada’s personal loan market splits into two distinct tiers, and your credit profile determines which one you access. Canada’s prime rate sets the floor for most variable-rate loans, but lenders add their own margins on top. If you have solid credit, you might secure a rate around 9.75% to 11%, while borrowers with weaker credit histories face rates climbing toward 24% or higher. Some alternative lenders charge all the way to 34.99% APR. This isn’t just a number game-the difference between a 10% and a 20% rate on a $15,000 loan over five years means you’ll pay roughly $4,200 more in interest. Banks like RBC, TD, and CIBC rarely advertise their rates online; you must apply to see what they’ll actually offer. Alternative lenders such as Spring Financial post rates starting at 9.99% for loans up to $35,000 with terms from 6 to 84 months. The real trend since 2023 is that lenders have tightened their standards.

Current personal loan interest rates in Canada typically range from 6% to 35% APR depending on your credit profile, and a 6% rate is now almost impossible to find unless you have exceptional credit and an established relationship with a major bank.

Bank vs Alternative Lender Trade-offs

Banks demand higher income thresholds, stricter credit requirements, and often insist you maintain an account with them before they’ll approve you. In return, they reward qualified applicants with lower rates. Alternative lenders flip the script-they approve faster, sometimes within the same day, and care less about your credit history, but they charge higher rates to offset their risk. Spring Financial, for example, approves loans online without a branch visit and allows early repayment with zero penalties, which helps if you want to pay down the balance faster. The catch is their rates reflect the added risk they take on. Private lenders occupy the middle ground, offering flexibility but with variable pricing that depends heavily on your circumstances. When you shop around, avoid applying to five lenders at once; each application triggers a hard credit inquiry that temporarily dents your score. Instead, research which lenders match your profile, then apply strategically to two or three options.

Your Credit Score Controls Your Rate

Lenders use your credit score as the primary lever for pricing. Your credit score controls your rate, with a score above 700 proving you manage your credit well and qualifying you for better terms. A score between 650 and 700 pushes you into mid-range pricing around 14% to 18%. Below 650, you’re looking at 20% or higher. This matters because even a 100-point improvement in your score before you apply can save you thousands over the loan term. If you’re sitting on accounts with high balances, you should pay those down before you apply; this reduces your debt-to-income ratio and signals lower risk to lenders. Dispute any errors on your credit report immediately-they’re more common than you’d think, and removing one can boost your score by 20 to 50 points. Secured loans, where you pledge an asset like a vehicle or savings account as collateral, typically cost 2 to 5 percentage points less than unsecured loans because the lender has recourse if you default.

How Lender Type Shapes What You Pay

The lender you choose affects not just your rate but also your approval speed and flexibility. Major banks require established relationships and solid income documentation, which slows the process but locks in competitive rates for those who qualify. Online lenders and alternative providers move faster and care more about your current situation than your past, making them accessible to borrowers banks reject. This speed comes at a price-literally. The trade-off between convenience and cost is real, and you need to calculate the total interest you’ll pay over the full term, not just focus on the advertised rate. A same-day approval at 24% might feel urgent, but it costs far more than waiting two weeks for a bank approval at 11%. Understanding these differences helps you match the right lender to your timeline and financial situation, which sets you up to make smarter choices about which loan actually fits your budget.

How Loan Rates Hit Your Monthly Budget

The Real Cost of Rate Differences

A $15,000 personal loan at 10% costs roughly $283 per month over five years, but that same loan at 20% jumps to $398 monthly. Over 60 months, you pay an extra $6,900 in interest just because your rate doubled. This is why the rate matters far more than most borrowers realize when they calculate affordability.

Your monthly payment isn’t just about the principal you’re borrowing-it’s heavily weighted toward interest in the early months, especially at higher rates.

Fixed vs Variable: The Budget Impact

If you have a variable-rate loan and Canada’s prime rate climbs again from its current 4.45% level, your payment swings upward immediately, which can break a tight budget. Fixed-rate loans protect you from this shock because your payment stays locked in regardless of what happens to prime, making budgeting predictable and easier to defend against rate volatility. Variable-rate loans initially feel cheaper, but they’re a gamble-if rates stay flat or fall, you win, but if they rise even 1 or 2 percentage points, your monthly outflow increases without warning.

The Bank of Canada’s rate decisions ripple directly through variable loans, so tracking rate trends gives you a heads-up about whether your payment might jump. If you’re already stretched thin on cash flow, a fixed rate eliminates that uncertainty and lets you plan with confidence. If you borrow $20,000 at a variable rate starting at 11% and prime rises by 2 percentage points as it did in 2022–2023, your rate could hit 13% or higher, pushing monthly payments up by $40 to $60 depending on your term.

Stress-Test Your Budget Against Rate Shocks

Can your budget absorb a payment increase without cutting essential spending or missing other obligations? If the answer is no, lock in a fixed rate now and accept paying slightly more today for certainty. Conversely, if you have stable income with cash reserves and can weather a rate increase, a variable loan saves you money most of the time.

When you compare offers from different lenders, demand the total interest cost in dollars, not just the APR percentage-it’s the only number that matters to your wallet. Spring Financial and other online lenders disclose this clearly in their quotes, while some banks bury it in the fine print.

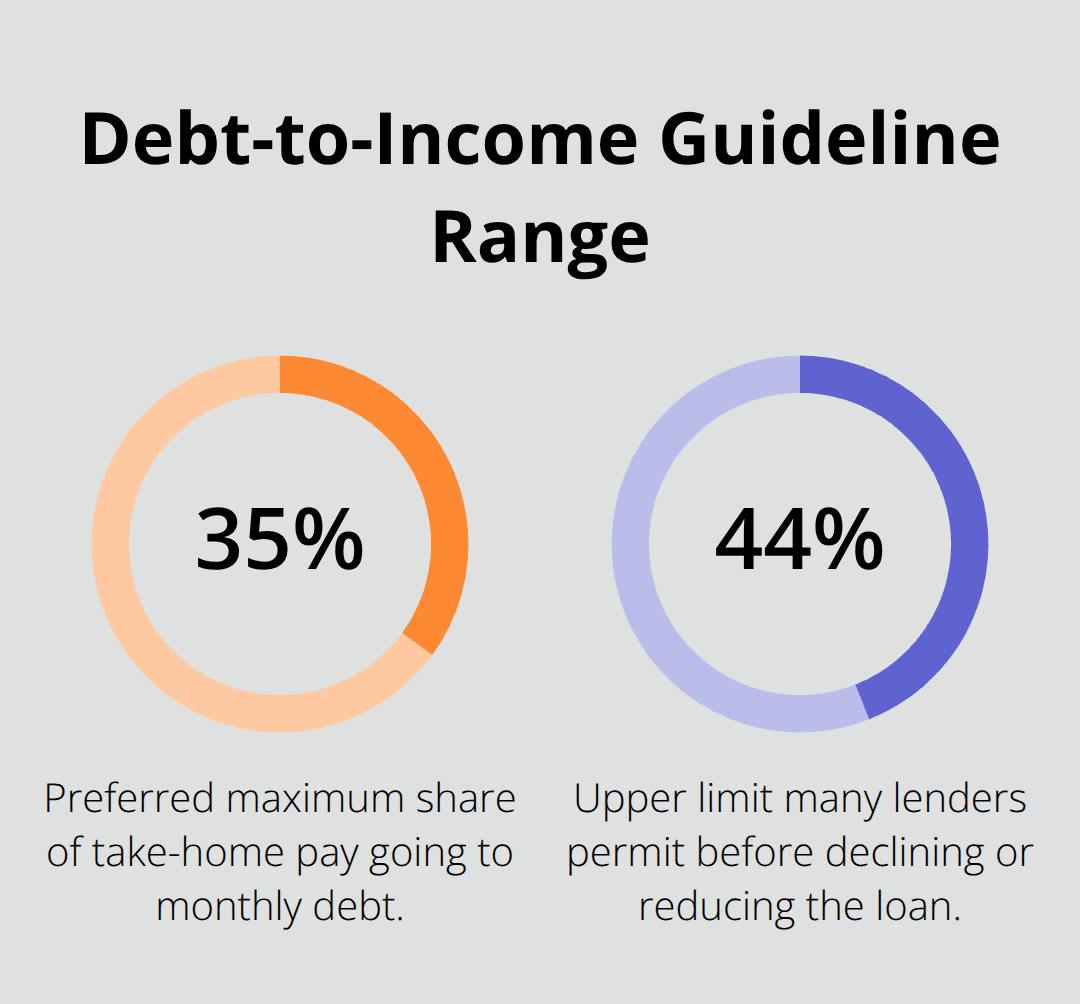

Debt-to-Income Ratio and Affordability

Your debt-to-income ratio also shapes affordability-lenders want to see your total monthly debt payments staying below 35 to 44 percent of your take-home pay, and you should hold yourself to that standard too. If adding this loan pushes you above that threshold, you’re overextended and should either borrow less or delay until you’ve paid down other balances.

The harsh truth is that many borrowers focus on the monthly payment alone and ignore total interest, which is exactly how they end up paying thousands more than necessary over the loan’s life. Once you understand how rates translate into real monthly costs, you’re ready to explore strategies that actually lower what you pay.

How to Lock In Better Rates Before You Apply

Fix Your Credit Report First

Your credit score isn’t fixed-it moves based on your recent financial behaviour, which means you can improve it in weeks or months before applying for a loan. Start by pulling your credit report from Equifax or TransUnion and check for errors; disputes take 30 days to investigate, but removing a wrong account or corrected late payment can boost your score 20 to 50 points instantly. Errors on credit reports happen more often than most borrowers realize, and they cost you real money in higher rates.

Pay Down High Balances Strategically

Next, reduce your highest-balance credit cards to below 30 percent of their limits; this single move often lifts your score 40 to 100 points because lenders view low utilization as responsible borrowing. Credit card utilization and credit score impact matters significantly for your borrowing profile. If you have 90 days before you need the loan, focus exclusively on reducing visible debt; skip new applications, avoid closing old accounts, and make all payments on time.

Understand How Score Improvements Translate to Savings

A score above 700 qualifies you for rates around 9.75 to 11 percent, while a score between 650 and 700 pushes you toward 14 to 18 percent-that’s a real 3 to 7 percentage point gap that costs thousands over five years. Moving from a 20 percent rate to a 12 percent rate on a $15,000 five-year loan saves you roughly $3,600 in interest, which makes the effort of improving your score before applying one of the smartest financial moves you can make.

Apply Strategically and Negotiate Hard

Once your credit profile is stronger, apply to two or three lenders whose products fit your needs, not to every option you find. Each hard inquiry shaves points off your score temporarily, so avoid the scatter-gun approach that many borrowers use. Compare the total interest cost in dollars across your offers, not just the APR; some lenders disclose this clearly in their quotes, while others hide it deep in the fine print. If you have a co-signer with better credit-a parent, spouse, or trusted friend-their stronger profile can lower your approved rate by 2 to 5 percentage points, though this ties their credit to your loan and obligates them if you default.

Leverage Your Existing Relationships

Negotiate with banks directly if you have an established relationship with them; some will offer rate discounts or waive fees for loyal customers, especially if you maintain a healthy account balance or direct deposit with them. The hard truth is that lenders don’t volunteer their best rates-you have to earn them through a stronger credit position and then push back on their initial offer.

Final Thoughts

Personal loans Canada rates swing wildly based on your credit score, the lender you select, and how strategically you shop around. A 5 percentage point difference costs you thousands in extra interest over the loan’s life, which is why understanding what these averages mean for your wallet matters far more than accepting the first offer you receive. Your rate depends on three factors you control: your credit profile, your choice of lender, and how hard you negotiate before signing.

Start by pulling your credit report and fixing any errors, then reduce high credit card balances to below 30 percent of their limits. These steps alone boost your score enough to qualify for rates 3 to 7 percentage points lower than you’d get today. Once your profile strengthens, apply to two or three lenders whose products match your needs, demand the total interest cost in dollars from each one, and stress-test your budget against potential rate increases.

Visit Financial Canadian to explore tools and calculators that support smarter borrowing decisions. Your next step is to take action on your credit profile today, not tomorrow-every month you delay costs you money in higher rates when you finally borrow.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment