At Financial Canadian, we often receive questions about secured credit cards. These financial tools can be a lifeline for those with limited or poor credit history.

Let’s define a secured credit card: it’s a type of credit card that requires a cash deposit as collateral. This deposit typically determines your credit limit and provides security for the card issuer.

Understanding how secured credit cards work can help you make informed decisions about your financial future.

What Are Secured Credit Cards?

Definition and Purpose

Secured credit cards are financial tools designed for individuals with limited or poor credit history. These cards can serve as a first step to begin building credit for those with no credit history or help those with a low credit score that makes it difficult to qualify for traditional credit cards.

How Secured Credit Cards Work

A secured credit card requires a cash deposit that serves as collateral. This deposit, which can range from $200 to $2,000, typically becomes your credit limit. For example, if you deposit $500, your credit limit will usually be $500. This setup reduces the risk for card issuers, making it easier for people with lower credit scores to qualify.

The Security Deposit

The security deposit is the key feature that distinguishes secured cards from traditional credit cards. This deposit is held by the card issuer and is generally refundable when you close the account or upgrade to an unsecured card. It’s important to note that this deposit is not used to pay your monthly bills – you’re still responsible for making regular payments.

Credit Reporting and Building Credit

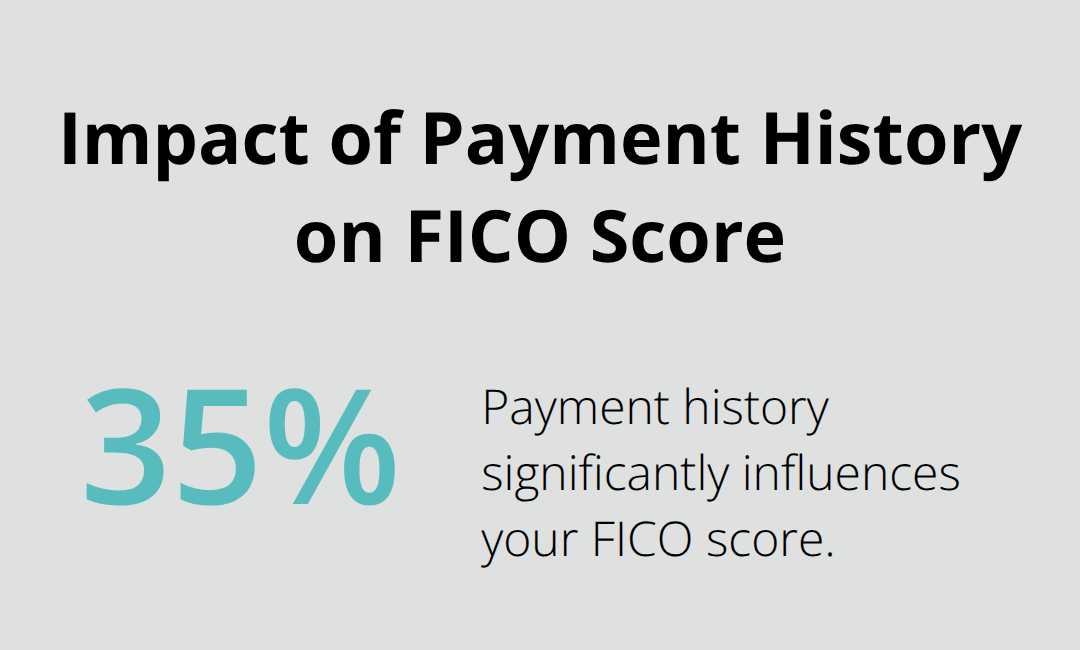

One of the most valuable aspects of secured credit cards is that most issuers report your payment history to the major credit bureaus (Equifax, Experian, and TransUnion). This reporting is essential for building your credit score. According to Experian, payment history accounts for about 35% of your FICO score, so making on-time payments can significantly impact your credit over time.

Fees and Interest Rates

While secured cards can be beneficial, they often come with higher fees and interest rates compared to traditional credit cards. Annual fees can range from $0 to $125, and APRs can be as high as 35.99%. It’s essential to read the terms carefully before applying and to pay your balance in full each month to avoid high interest charges.

A secured credit card is a stepping stone. With responsible use, you can improve your credit score and eventually qualify for an unsecured card with better terms and benefits. Now, let’s explore the application process and eligibility requirements for secured credit cards in more detail.

How Do Secured Credit Cards Work?

Secured credit cards function differently from traditional unsecured cards, but they can be an excellent tool for building or rebuilding credit. Many Canadians have successfully used these cards to improve their financial standing.

Application Process

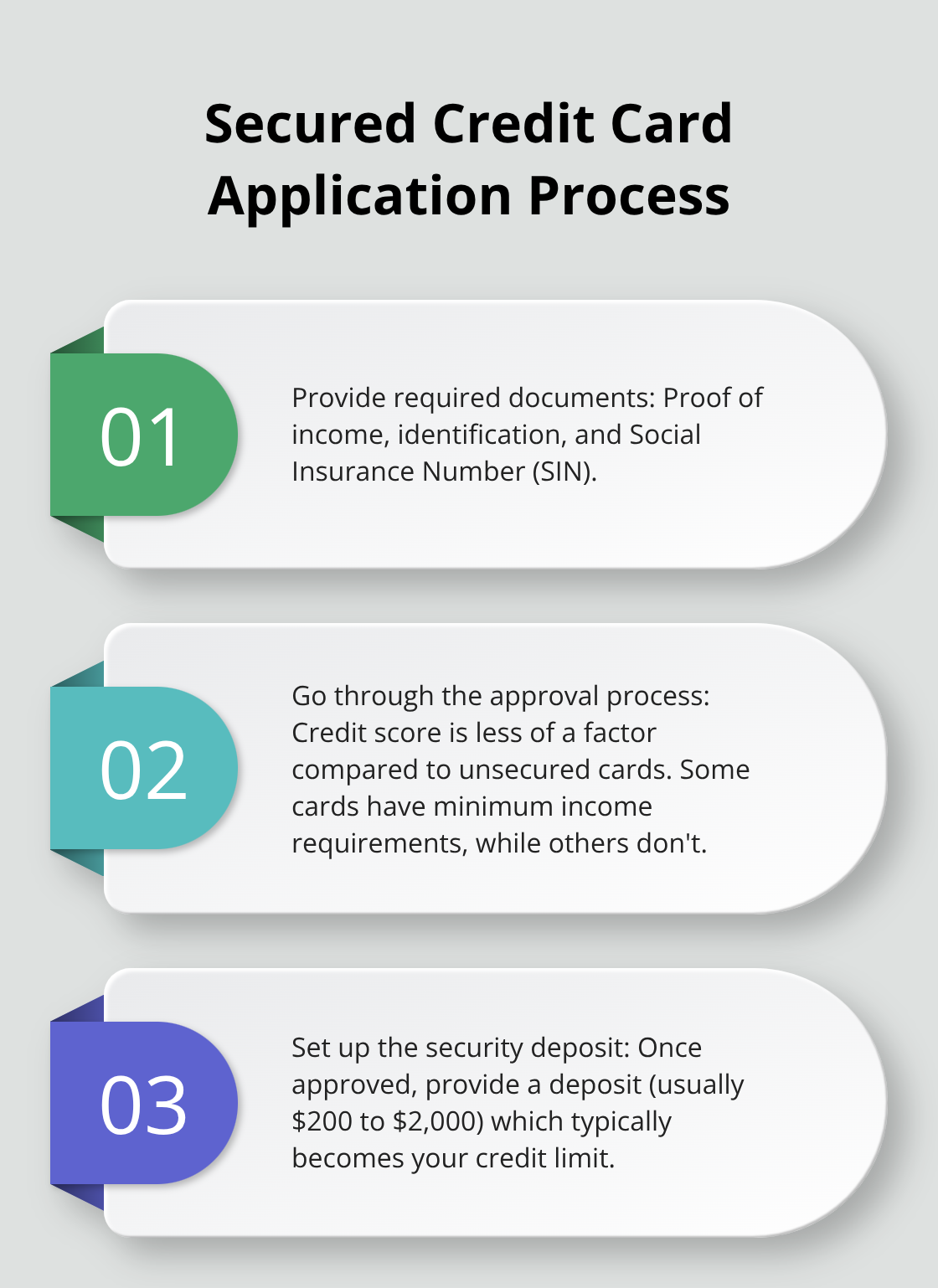

The application process for a secured credit card is straightforward. Most major banks and credit card companies offer these products. To apply, you’ll typically need to provide:

- Proof of income

- Identification

- Social Insurance Number (SIN)

Unlike unsecured cards, your credit score is less of a factor in the approval process.

Many issuers have minimum income requirements. For example, the BMO CashBack Secured Mastercard requires an annual income of at least $15,000. However, some cards (like the Home Trust Secured Visa) have no minimum income requirement.

Security Deposit Setup

Once approved, you’ll need to provide a security deposit. This amount usually ranges from $200 to $2,000 and becomes your credit limit. For instance, if you deposit $500, your credit limit will typically be $500.

Some issuers offer flexibility. The Capital One Guaranteed Secured Mastercard allows deposits between $75 and $300, with a credit limit of up to $2,500 based on your creditworthiness.

Credit History Building

Using a secured credit card responsibly can significantly impact your credit score. Most issuers report to major credit bureaus like TransUnion.

To maximize credit building, try to use less than 30% of your credit limit. For a card with a $500 limit, keep your balance below $150. Also, always pay your bill on time and in full to avoid interest charges and demonstrate responsible credit use.

Fees and Interest Rates

Secured credit cards often come with higher fees and interest rates than unsecured cards. Annual fees can range from $0 to $59 or more. For example, the Refresh Financial Secured Card has a $12.95 annual fee, while the Home Trust Secured Visa offers a no-annual-fee option.

Interest rates on these cards are typically high. The CIBC Secured Credit Card has an interest rate of 19.99% on purchases, which is standard for many secured cards in Canada.

Some cards also charge additional fees. The Refresh Financial Secured Card has a $3 monthly maintenance fee on top of its annual fee. Always read the terms and conditions carefully before applying.

Understanding how secured credit cards work allows you to use them effectively to build your credit and eventually qualify for better financial products. Now, let’s explore the benefits and drawbacks of secured credit cards to help you make an informed decision.

Are Secured Credit Cards Worth It?

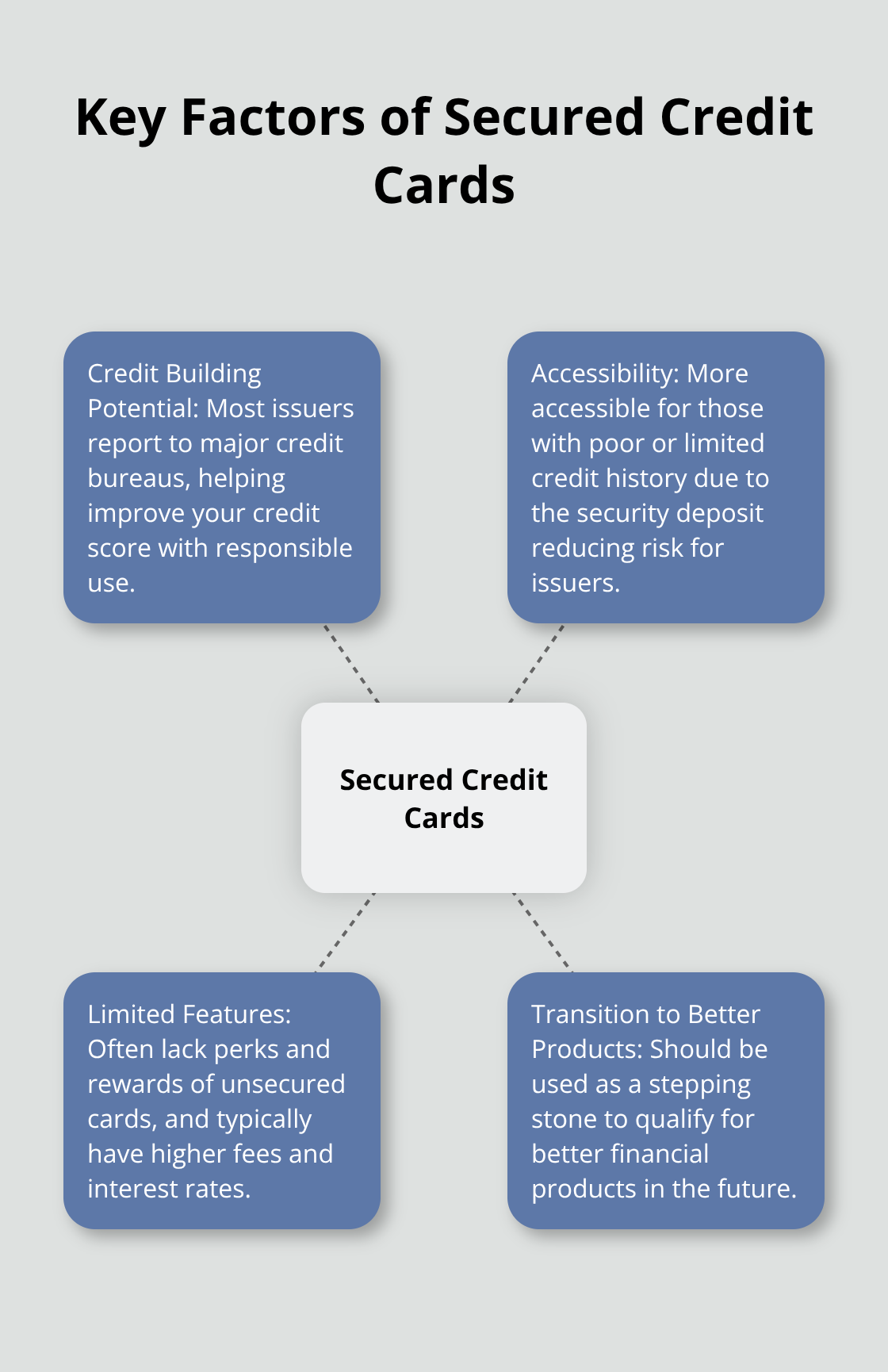

Credit Building Potential

Secured credit cards offer a powerful tool for credit improvement. Most issuers report payment history to major credit bureaus, which can positively impact your credit profile.

This potential for improvement requires responsibility. Late payments or maxing out your card can harm your credit score as easily as responsible use can improve it. We suggest you set up automatic payments to avoid missing due dates.

Accessibility for High-Risk Borrowers

Secured credit cards provide more accessibility than traditional credit cards for those with poor or limited credit history. The security deposit reduces the risk for issuers, increasing their willingness to approve applications from high-risk borrowers.

For example, some secured cards have no minimum income requirement and boast high approval rates (making them excellent options for those rejected for unsecured cards). However, the security deposit can present a financial challenge for some applicants.

Limited Features and Higher Costs

While secured cards can benefit users, they often lack the perks and rewards of unsecured cards. You’ll rarely find travel points, cash back, or sign-up bonuses with most secured cards. Additionally, secured cards typically come with higher fees and interest rates.

Secured credit cards generally have higher annual percentage rates and higher annual fees than unsecured cards. You should compare different options and read the fine print before applying.

Transition to Better Credit Products

A secured credit card should serve as a stepping stone, not a long-term solution. Many issuers offer the opportunity to graduate to an unsecured card after you demonstrate responsible use over time. Some card providers may review your account for a credit limit increase or upgrade to an unsecured card after as little as six months of on-time payments.

When you consider a secured credit card, think about your long-term financial goals. These cards can help rebuild credit, but shouldn’t become a permanent fixture in your wallet. Instead, use them as a tool to qualify for better financial products in the future.

Final Thoughts

Secured credit cards provide a path to better credit for those with limited or poor financial history. These cards require a security deposit, which typically sets the credit limit and reduces risk for issuers. Individuals new to credit, rebuilding after setbacks, or struggling to qualify for unsecured cards should consider this option.

To define a secured credit card: it’s a financial tool that reports to major credit bureaus, helping establish or improve credit scores when used responsibly. Users should pay their balance in full each month, keep credit utilization low, and set up automatic payments to avoid missed due dates. Regular credit report reviews allow users to track progress and address errors promptly.

At Financial Canadian, we understand the importance of building a strong online presence. Our web design services can help create your digital footprint, much like how a secured credit card builds your financial profile. We offer websites tailored to your business needs, ensuring you make a lasting impression in the digital world.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment