Building credit from scratch feels overwhelming when you’re staring at dozens of card options. The wrong choice can cost you hundreds in fees while barely moving your credit score.

We at Financial Canadian have analyzed the market to identify which cards actually help beginners build credit fast. Finding the best credit card to help build credit requires knowing exactly what features matter most for your financial future.

Which Credit Cards Build Credit Fastest

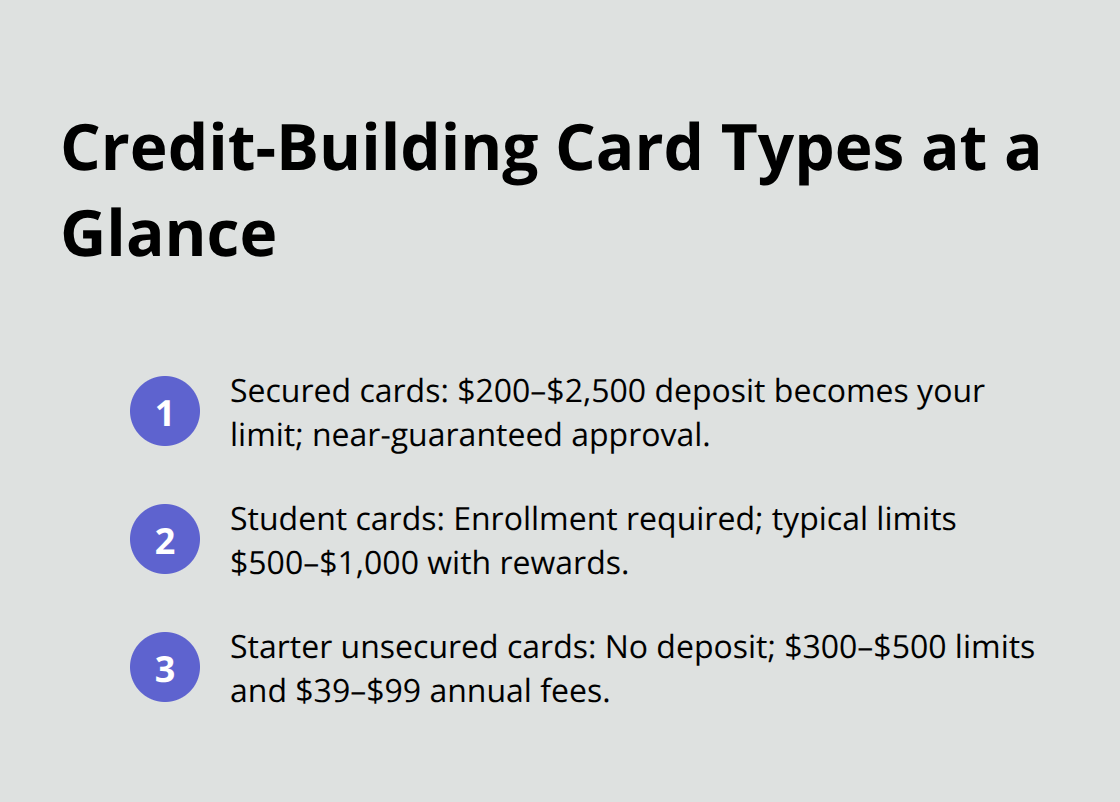

Three card types dominate the credit-building landscape, each one targets different financial situations. Secured credit cards require a cash deposit between $200 and $2,500 that becomes your credit limit, which makes approval nearly guaranteed regardless of credit history. Capital One Secured and Discover it Secured lead this category because they report to all three credit bureaus and offer potential upgrades to unsecured cards after responsible use. Student credit cards like the Discover it Student Cash Back require enrollment verification but offer higher approval odds for young borrowers with limited income, typically they start with $500 to $1,000 credit limits.

Secured Cards Guarantee Approval

Secured cards work differently than traditional credit cards because your deposit eliminates the lender’s risk. Most major banks offer secured options, but you should avoid cards that charge annual fees above $35 or those that require additional monthly maintenance fees. Your deposit earns no interest, but responsible use typically qualifies you for unsecured card upgrades with deposit refunds. Choose secured cards from established issuers like Bank of America or Wells Fargo that automatically review accounts for graduation to unsecured status.

Student Cards Offer Better Terms

Student credit cards provide more favorable terms than secured options but require college enrollment verification. These cards typically waive annual fees permanently and offer rewards programs (which makes them superior choices for qualified borrowers). Approval requires proof of income as low as $100 monthly from part-time work or allowances. Most student cards graduate to regular cards upon completion of studies without new applications.

Major Issuer Starter Cards Skip Deposits

Starter cards from major issuers like Capital One Platinum and Credit One Bank Platinum target fair credit applicants without security deposits. These unsecured options start with $300 to $500 credit limits but charge annual fees that range from $39 to $99. While more expensive than secured alternatives, they build credit identically and avoid cash deposits tied up for months (which appeals to borrowers who need immediate access to their funds).

The card type you choose matters less than the specific features each card offers for credit development.

What Credit Card Features Build Credit Fastest

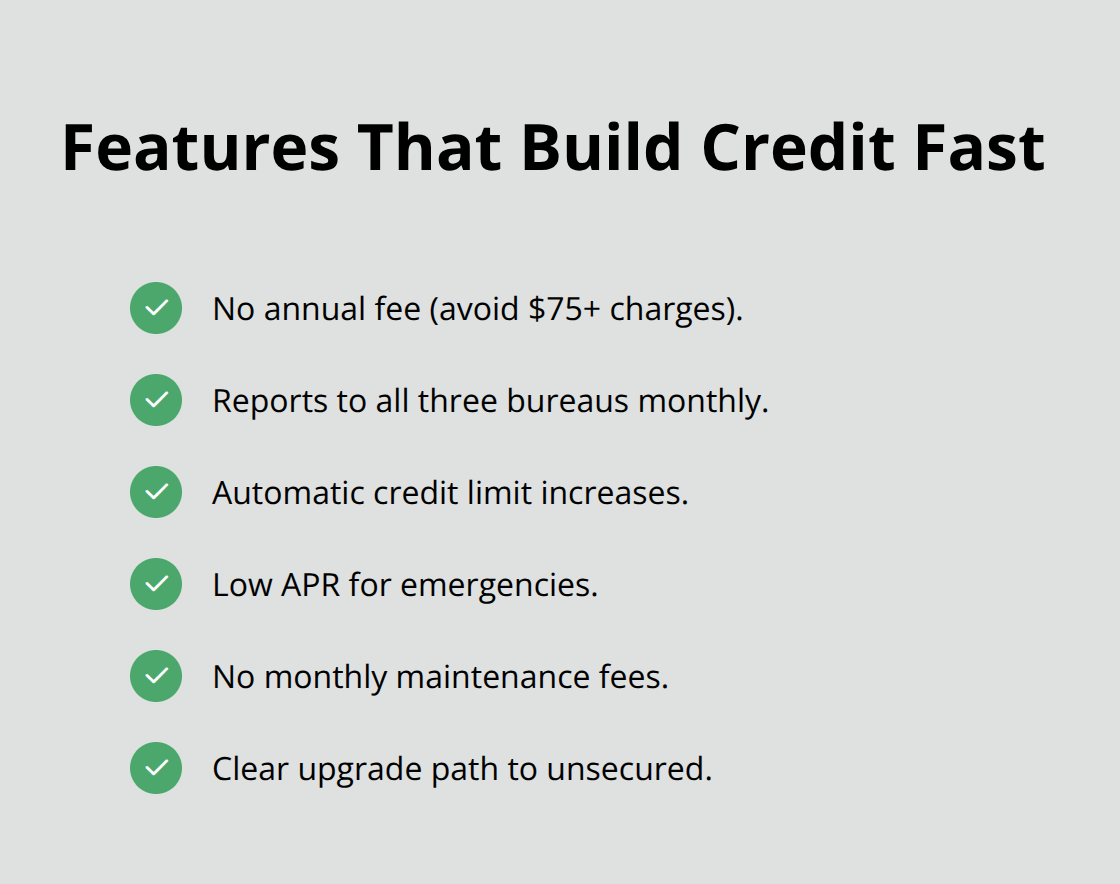

Annual fees destroy your credit-building progress before it starts. Cards that charge $75 or more annually cost you $375 over five years while they provide identical credit-building benefits to no-fee alternatives. Discover it Secured charges zero annual fees and reports to Experian, TransUnion, and Equifax monthly, which makes it superior to fee-heavy competitors like Credit One Bank cards that charge $95 annually. Fee-free secured cards from major banks like Wells Fargo and Bank of America offer the same credit bureau reporting without they bleed your budget dry.

Credit Limit Growth Accelerates Score Improvements

Automatic credit limit increases multiply your credit-building power without hard credit inquiries. Capital One reviews secured card accounts every six months and increases limits based on payment history, while Discover it Secured typically doubles initial limits after eight months of on-time payments. Cards without increase policies trap you at low limits that restrict your credit utilization improvements. Choose cards from issuers with documented increase policies rather than vague promises about potential reviews.

Triple Bureau Reporting Maximizes Credit Impact

Cards that report to only one or two credit bureaus waste months of credit-building effort. Build your credit with a card that reports to all three bureaus, which makes single-bureau reporting cards nearly useless for comprehensive credit development. Avoid store cards and some credit union options that skip TransUnion or Equifax reporting. Major issuer cards like Chase Freedom Student and Bank of America Student consistently report to all bureaus within 30 days of statement closing dates, which means your progress appears across your entire credit profile.

Low Interest Rates Protect Your Progress

High APRs can sabotage your credit-building efforts when unexpected expenses force you to carry balances. Secured cards typically offer APRs between 22% and 26%, but some student cards provide rates as low as 18% for qualified applicants. Lower rates give you breathing room during financial emergencies without interest charges that spiral out of control (and potentially damage the payment history you’ve worked to build). Once you understand these essential features, you need to know exactly how to use your new card to maximize credit score gains.

How Do You Build Credit With Your New Card

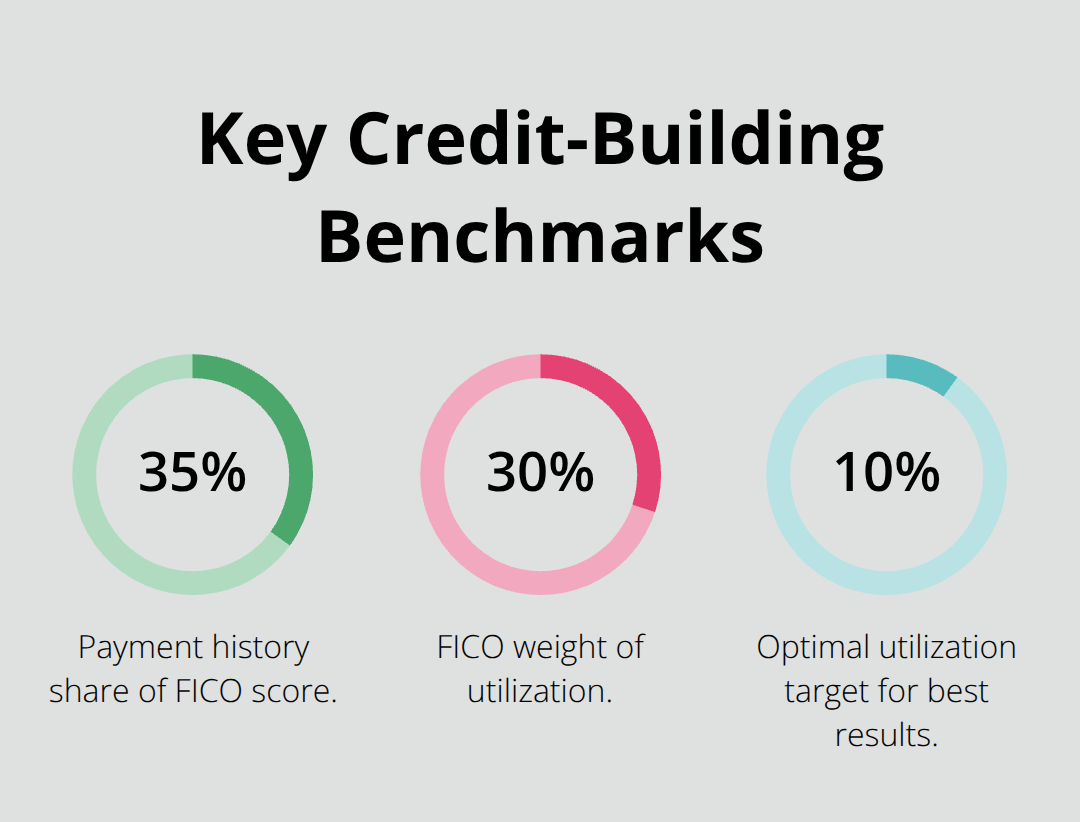

Your credit utilization ratio impacts 30% of your FICO score, which makes it the second most important factor after payment history. Keep your balance below 30% of your credit limit, but optimal scores require utilization below 10%. If you have a $500 credit limit, spend no more than $50 monthly and pay it off before your statement closes. This strategy shows lenders you use credit responsibly without dependence on it. Many cardholders pay after the statement date, which reports higher utilization to credit bureaus even when they pay in full.

Payment Schedule Determines Your Credit Score

Payment history accounts for 35% of your credit score according to FICO, which makes on-time payments your most powerful credit-building tool. Set up automatic payments for at least the minimum amount due, but pay your full balance to avoid interest charges.

Credit card companies report late payments to bureaus after 30 days past due (which can drop your score by 60 to 110 points). Pay your balance before the statement date to report zero utilization, or make multiple payments throughout the month to keep reported balances low.

Free Tools Track Your Credit Progress

Monitor your credit score monthly with free services like Credit Karma or through your card issuer’s app. Most major banks including Capital One and Chase provide FICO scores updated monthly at no cost. Your score should increase 10 to 20 points within three months of responsible use, with significant improvements after six months of perfect payment history. Check your credit reports quarterly through AnnualCreditReport.com to verify your new card appears on all three bureaus and reports accurate payment information.

Multiple Payments Lower Reported Balances

Make several small payments throughout your billing cycle instead of one large payment at month-end. This approach keeps your daily balance low and reduces the balance reported to credit bureaus on your statement date. Credit bureaus receive balance information on your statement date (not your payment date), so strategic payment schedules can show zero utilization even when you use your card regularly. This technique works especially well with low-limit starter cards where small purchases quickly approach the 30% threshold.

Final Thoughts

Secured credit cards provide the fastest path to credit development with guaranteed approval and deposits that start at $200. Student cards deliver better terms for enrolled borrowers, while starter cards from major issuers skip deposits but charge annual fees. The best credit card to help build credit reports to all three bureaus, charges no annual fees, and provides automatic limit increases.

You can start credit development today when you apply for a fee-free secured card from Capital One or Discover. Set up automatic payments for your full balance and keep expenses below 10% of your credit limit. Monitor your progress monthly through free credit score services and expect 10 to 20 point improvements within three months.

Strong credit history unlocks mortgage rates 1% to 2% lower than poor credit borrowers (which saves $50,000 on a typical home loan). Good credit also reduces insurance premiums, eliminates utility deposits, and improves rental application success rates. We at Financial Canadian help businesses establish their digital presence with comprehensive web design services that boost online visibility and drive growth.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment