A line of credit in Canada gives you access to borrowed funds whenever you need them, without the rigid structure of a traditional loan. You only pay interest on what you actually use, making it a smart tool for managing unexpected expenses or funding planned projects.

At Financial Canadian, we believe a line of credit deserves a closer look if you’re tired of credit card interest rates eating into your budget. This guide walks you through how they work, why they matter, and how to pick the right one for your situation.

How Lines of Credit Work in Canada

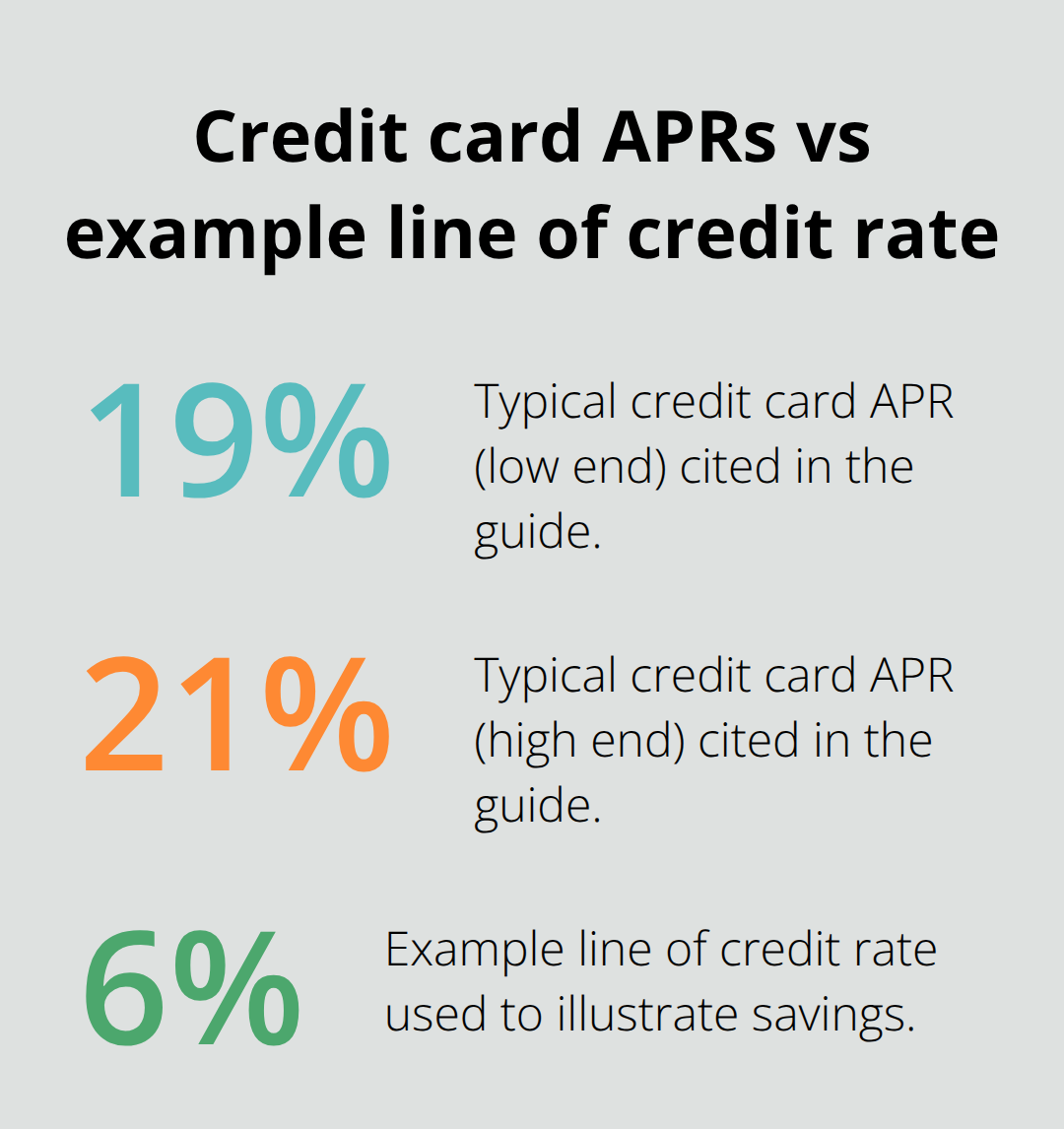

A line of credit functions as a revolving account where Canadian lenders approve you for a maximum amount, and you draw from that pool only when needed. Unlike a personal loan that deposits a lump sum into your account, you access funds gradually through your bank account, debit card, cheques, or online transfers. Interest accrues only on what you’ve actually borrowed, not on the full approved amount. This structure makes lines of credit fundamentally different from credit cards, which charge interest on your entire balance and typically carry rates between 19% and 21% according to Statistics Canada data.

Secured vs. Unsecured Lines

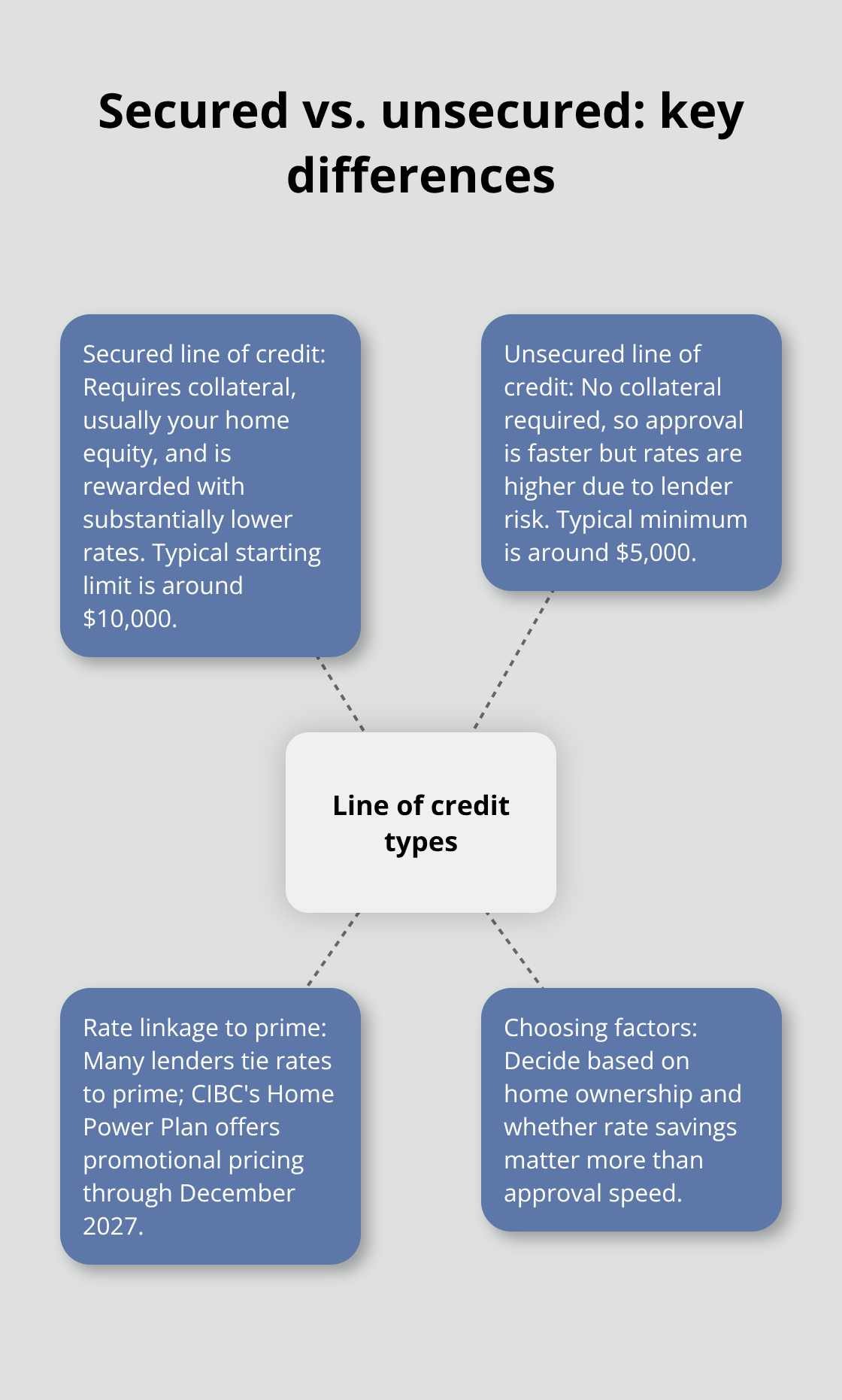

Lines of credit in Canada come in two forms: secured and unsecured. A secured line of credit requires collateral, usually your home equity, and lenders reward this security with lower rates. CIBC’s Home Power Plan ties rates to the prime rate with promotional pricing through December 2027. Unsecured lines skip the collateral requirement, meaning faster approval but higher interest rates since the lender carries more risk. Most Canadian lenders set unsecured lines with minimums around $5,000, while secured options typically start at $10,000.

How Interest Rates Change

Canadian lenders almost exclusively offer variable-rate lines of credit, meaning your borrowing costs change whenever the Bank of Canada adjusts the prime rate. This unpredictability matters when you carry a balance over months or years. CIBC and other major banks tie their rates directly to prime, so when the central bank moves, your payments adjust immediately. Some borrowers dislike this volatility, but others view it as a fair trade for ongoing access to funds.

What Lenders Look For

The approval process for a line of credit hinges on three factors: your credit score, income verification, and debt-to-income ratio. Most Canadian lenders want a credit score above 650, though 700 or higher significantly improves your odds and rate offerings. You’ll need recent pay stubs, tax returns, and possibly employment letters. Applications take days rather than weeks because lenders assess you for preapproved access rather than a specific purchase.

Repayment Flexibility

Monthly repayment requirements vary by lender but typically demand you cover interest plus a small principal payment. Some lines require full repayment within a set timeframe, usually annually or on a schedule specified in your agreement. The key advantage here is flexibility: you can pay more aggressively when cash flow allows, or stick to minimums during tight months. Once you understand how lines of credit function, the next step involves identifying which type matches your financial situation and comparing what different lenders actually offer.

Why a Line of Credit Beats Credit Cards for Most Borrowers

The Math Behind Lower Interest Rates

Credit card interest rates destroy your savings. At 19% to 21%, a $5,000 balance costs you $950 to $1,050 annually in interest alone. A line of credit at prime plus 1% or 2% cuts that cost dramatically, especially when prime sits lower. Even unsecured lines from major Canadian lenders typically charge 5 to 8 percentage points below credit card rates. The difference compounds over time. If you need $10,000 for a kitchen renovation and carry that balance for two years, a credit card costs you roughly $2,000 in interest while a 6% line of credit costs around $600. That’s not minor savings-that’s money staying in your account instead of flowing to your lender. Homeowners access even better rates through secured lines backed by home equity, which lenders reward with the lowest rates available to most borrowers.

Access Funds Only When You Need Them

A line of credit solves the cash flow problem that catches most borrowers. You access funds when you actually need them rather than committing to a fixed loan amount upfront. Renovations run over budget, medical expenses arrive unexpectedly, or your vehicle needs repairs-a line of credit lets you draw exactly what you need without reapplying or paying interest on unused funds. This structure differs fundamentally from personal loans, which deposit a lump sum and charge interest on the entire amount immediately. With a line of credit, you control when money flows out and how much you actually borrow.

Repayment That Matches Your Reality

Monthly repayment flexibility matters when income fluctuates. During profitable months, you pay aggressively and reduce your balance. During slower months, you cover interest and a minimum principal payment. This breathing room prevents the financial strain that fixed loan payments create when cash flow tightens. Unsecured options provide approval speed without collateral risk, while secured lines backed by home equity offer the lowest rates available. The flexibility to borrow, repay, and borrow again without closing and reopening accounts makes a line of credit the practical choice for anyone managing variable expenses or building an emergency fund. You design repayment around your actual financial reality rather than fitting your finances into a payment schedule designed for someone else’s circumstances.

Choosing Between Secured and Unsecured

Secured lines require collateral (usually your home) but reward that security with substantially lower rates. Unsecured lines skip the collateral requirement, meaning faster approval but higher interest rates since the lender carries more risk. Most Canadian lenders set unsecured lines with minimums around $5,000, while secured options typically start at $10,000. Your choice depends on whether you own a home and how much rate savings matter versus approval speed.

Once you understand which type fits your situation, the next step involves evaluating specific lender offers and identifying the terms that align with your financial goals.

Which Line of Credit Actually Saves You Money

Selecting the right line of credit requires moving past promotional rates and examining what you actually pay over time. The difference between a secured line of credit at prime plus 0.5% and an unsecured line at prime plus 2.5% sounds small until you calculate real costs. On a $15,000 balance held for two years, that 2% rate difference costs you roughly $600 in additional interest. Start by determining whether you own a home with equity available. Homeowners should almost always pursue secured lines because the rate advantage is substantial and immediate.

Secured Lines for Homeowners

CIBC’s Home Power Plan requires a minimum $10,000 borrowing amount and a property valuation fee of $300, but the promotional rate equal to prime through December 2027 then converts to their ongoing rate. After that promotional period expires, you’ll pay whatever prime rate CIBC sets, so calculate what happens when rates rise. If you don’t own a home or lack sufficient equity, unsecured lines remain your option despite higher rates. Most Canadian lenders charge 5 to 8 percentage points above prime for unsecured access, which still beats credit cards significantly.

Comparing Lender Offers Side by Side

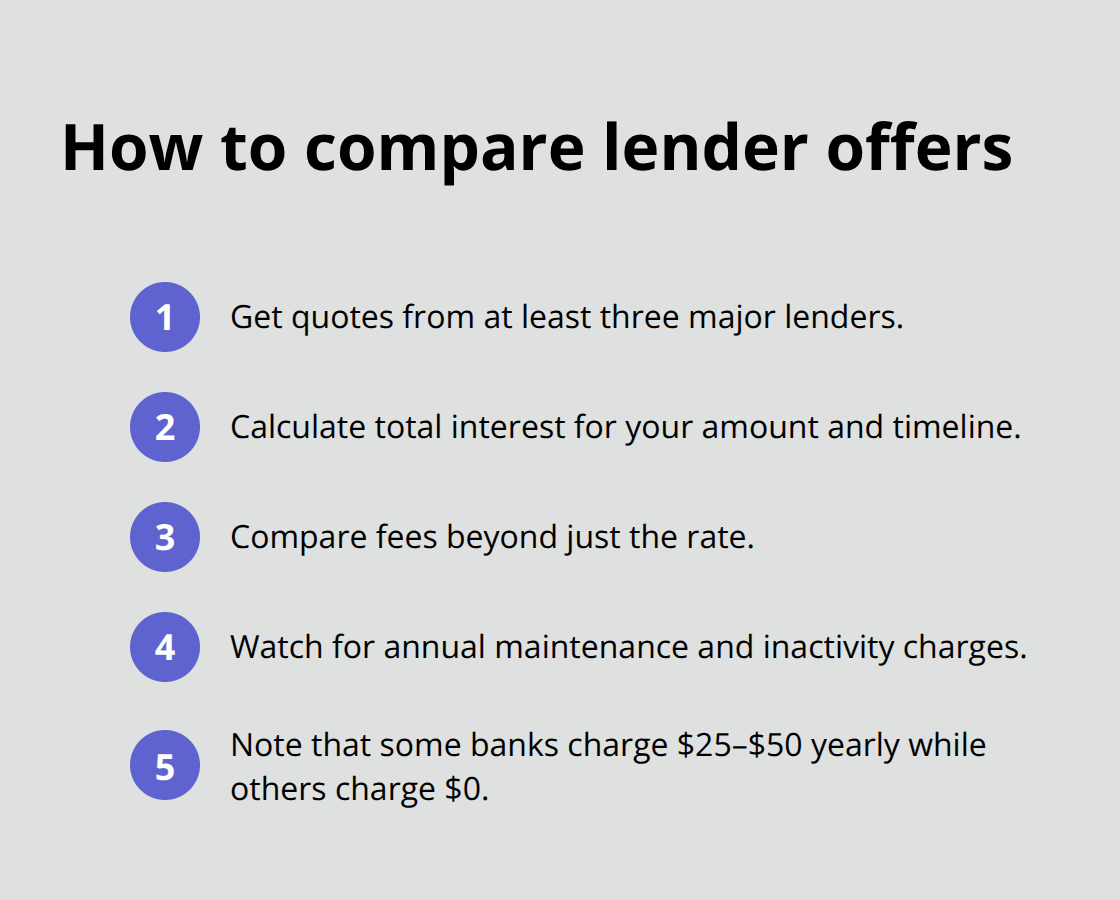

The real comparison work happens when you evaluate specific lender offers against each other. Pull rate quotes from at least three major lenders and calculate total interest on your expected borrowing amount over your expected repayment timeline. A rate difference of 1% on $10,000 borrowed for one year equals $100 in your pocket rather than your lender’s. Don’t stop at interest rates because fees hide in the fine print. Transaction fees, annual maintenance charges, and inactivity fees vary wildly between lenders. Some Canadian banks charge nothing for account maintenance while others levy $25 to $50 annually.

CIBC’s personal line of credit includes 24-hour access through branches, machines, telephone, online, and mobile banking with no transaction fees, which matters when you need funds quickly. Check whether your lender charges for early repayment or if they penalize you for paying off your balance faster than scheduled. The strongest lines of credit offer flexibility without penalty, allowing you to accelerate repayment whenever cash flow permits. Personal lines of credit only charge interest on the amount you’ve actually borrowed, potentially saving you money if you don’t use the full credit limit.

Speed Versus Rate Savings

The approval timeline and documentation requirements also influence your choice practically. Unsecured lines typically approve within days because lenders assess your creditworthiness without property appraisals or valuation fees. Secured lines take longer due to property evaluation requirements but deliver substantially lower rates. If you need funds urgently, speed matters more than rate savings. Insurance options merit attention even though they’re optional add-ons. CIBC offers disability and life insurance underwritten by Canada Life Assurance Company, protecting your line of credit balance if you become unable to work or pass away. This protection costs extra but appeals to borrowers with dependents or tight monthly budgets where missed payments create genuine hardship.

Evaluating Lender Responsiveness

Test the lender’s actual responsiveness before committing. Call their customer service line, ask specific questions about rate changes, and assess whether they explain terms clearly. A lender who communicates transparently about how your rate adjusts when prime changes and what happens when promotional periods expire deserves preference over one offering marginally lower rates but vague explanations. The right line of credit isn’t always the cheapest one available; it’s the one whose terms you fully understand and whose rates remain competitive throughout your repayment period.

Final Thoughts

A line of credit in Canada solves a real problem that credit cards and fixed loans ignore: the need for flexible access to funds without paying interest on money you haven’t borrowed. Secured lines backed by home equity deliver the lowest rates available, while unsecured options provide faster approval when you lack collateral. The strongest case for using a line of credit emerges when your expenses don’t follow a predictable schedule-home renovations that run over budget, vehicle repairs that arrive unexpectedly, or medical costs that strain your cash flow all become manageable with a line of credit standing ready.

A line of credit makes less sense if you’re borrowing for a single, large purchase like a home or vehicle where a mortgage or car loan offers better terms and fixed repayment schedules. It also falls short if you lack the discipline to avoid overborrowing or if you struggle with variable-rate uncertainty when prime rates fluctuate. Start by checking your credit score and determining whether you own a home with available equity, then pull rate quotes from at least three major Canadian lenders.

Calculate total interest costs over your expected repayment timeline and pay close attention to fees beyond interest rates. Most applications complete within days, and lenders now offer online approval processes that eliminate unnecessary paperwork. We at Financial Canadian help you navigate financial decisions with clear, practical guidance that cuts through complexity and builds confidence in your money choices.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment