Car loan rates in Canada vary significantly depending on your lender, credit score, and down payment. A difference of just 1% in interest can cost you thousands of dollars over the life of your loan.

At Financial Canadian, we’ve put together this guide to help you understand current rates and find the best deal for your situation. You’ll learn proven strategies to lower your rate and avoid costly mistakes that many borrowers make.

Current Car Loan Rates in Canada Right Now

Statistics Canada reports the average new car loan rate at 6.5% APR as of October 2025, but this figure hides substantial variation across lenders and credit profiles. Major banks like TD, RBC, Scotiabank, CIBC, and BMO advertise starting rates around 7.20% APR-figures that only apply to borrowers with excellent credit. If your credit score exceeds 750, you can realistically target rates between 3.99% and 6.99%. Borrowers scoring 660–749 typically see 5.99%–9.99%, while those in the 560–659 range face 8.99%–14.99%. Anyone below 560 should expect 10.99% or higher. Your actual rate depends far more on your financial profile than on any advertised average.

Where You Can Find Better Rates Than Banks

Manufacturer financing often beats traditional lenders by a significant margin. Subaru offers promotional rates as low as 1.99%, while Nissan, Mazda, and Jeep sit at 2.49%, 2.95%, and 3.44% respectively. Ford and Mercedes-Benz both offer 3.99%, and Honda and Hyundai reach 4.99%. These promotions typically apply to specific models and terms, so you’ll need to check eligibility before assuming you qualify. Online lenders and credit unions also compete aggressively: CarDoor starts at 6.45%, while TD Auto Finance through the TD Wheels App begins at 2.99% for new cars. Most borrowers make a critical mistake by accepting their dealer’s first offer without comparing external options. A pre-approval from a bank or credit union before you visit a dealership gives you concrete leverage and prevents dealers from inflating rates under time pressure.

Why Down Payment Size Matters More Than You Think

A larger down payment reduces the lender’s risk and can shift you into a lower rate bracket entirely, potentially saving thousands in interest. On a $30,000 vehicle at 8% APR over 60 months, a 10% down payment ($3,000) means you finance $27,000 at roughly $608 monthly with $9,480 in total interest. Increasing your down payment to 25% ($7,500) reduces the financed amount to $22,500, cutting monthly payments to roughly $507 and total interest to $7,920-a $1,560 difference on the same car. Your credit score and down payment work together: excellent credit with a modest down payment still beats average credit with a large one, but combining both maximizes your negotiating position.

How to Lock in Your Best Rate Before You Shop

Pre-approval separates serious borrowers from casual shoppers in the eyes of dealers. When you obtain pre-approval from multiple lenders, you establish a benchmark rate and maximum loan amount before stepping onto a dealership lot. This knowledge prevents dealers from presenting inflated rates as your only option. Lenders conduct a soft credit check for pre-approval, which doesn’t damage your credit score, while the actual loan application involves a hard check. You should apply with at least two or three lenders to compare offers side by side. Written pre-approval letters specify your maximum borrowing amount, the rate you qualify for, and the loan term-all contingent on the vehicle you choose. This documentation becomes your shield against high-pressure sales tactics and dealer financing schemes that prioritize their commission over your savings.

How to Lock in the Best Rate Before You Negotiate

Check Your Credit Score and Fix Errors First

Your credit score is the single most important factor lenders use to price your loan, yet most borrowers apply without checking theirs first. Pull your credit report from Equifax or TransUnion at least 30 days before you apply for a car loan, then dispute any errors immediately-a single missed payment or incorrect account can drop your score by 50 points and cost you thousands in higher interest. If your score sits below 660, wait before you apply and focus on paying down existing debt aggressively. Each percentage point of credit utilization you reduce shows up on your next report, and lenders recalculate your rate based on real-time data. Paying off a credit card balance or closing unused accounts won’t instantly fix a poor history, but it signals financial discipline to underwriters. Once your score reaches 700 or higher, you unlock access to rates below 7% at most lenders. The difference between 720 and 800 is negligible in terms of rate reduction, so don’t wait for a perfect score-delaying your car purchase costs you money through continued depreciation of whatever vehicle you’re driving now.

Compare Rates Across Multiple Lenders Within Two Weeks

Shopping rates across multiple lenders is non-negotiable, yet roughly 60% of Canadian car buyers accept their dealership’s financing without comparing alternatives. Apply for pre-approval with at least three separate lenders-your bank, a credit union, and one online lender like CarDoor or TD Auto Finance-and complete all applications within a two-week window so multiple hard inquiries count as a single credit check. Each pre-approval letter shows your maximum borrowing amount, approved term, and rate; comparing them side by side reveals exactly how much negotiating power you hold.

A dealer might quote you 7.5% when your bank pre-approved you at 6.2%-that 1.3% difference on a $25,000 loan over five years costs you roughly $1,700 in extra interest. Once you arrive at the dealership with written pre-approval in hand, you can negotiate the vehicle price separately from financing, preventing the dealer from using low monthly payments to hide a higher purchase price.

Watch for Manufacturer Financing Promotions

Manufacturer financing promotions deserve special attention because they often beat bank offers significantly. These limited-time offers create urgency, which can pressure you into a quick decision-resist that pressure and verify the rate applies to your chosen vehicle and desired term. The best strategy combines manufacturer rates with your pre-approval letters: if the promotional rate exceeds your bank offer, you have concrete proof to negotiate with the dealer or walk away entirely. This comparison transforms you from a passive buyer into an informed negotiator who controls the conversation.

Mistakes That Wreck Your Car Loan Deal

Most borrowers sabotage their own financing by making one critical error: they treat the dealership’s first offer as their only option. Walking into a dealership without pre-approval letters from external lenders puts you at an immediate disadvantage because dealers control the conversation and can quote rates that exceed what you’d qualify for elsewhere. A borrower with a 720 credit score might accept 7.8% from a dealer when their bank pre-approved them at 6.1%, adding roughly $2,100 in unnecessary interest on a $25,000 five-year loan. The dealership benefits when you ignore rate shopping because they earn a commission on the financing spread, meaning they profit more when you accept a higher rate. Your only defense is obtaining written pre-approval from at least two lenders before you step onto the lot, then using those offers to negotiate or walk away entirely. Dealers expect most buyers to accept their terms without comparison, so when you arrive armed with competing offers, you immediately shift the power dynamic in your favor.

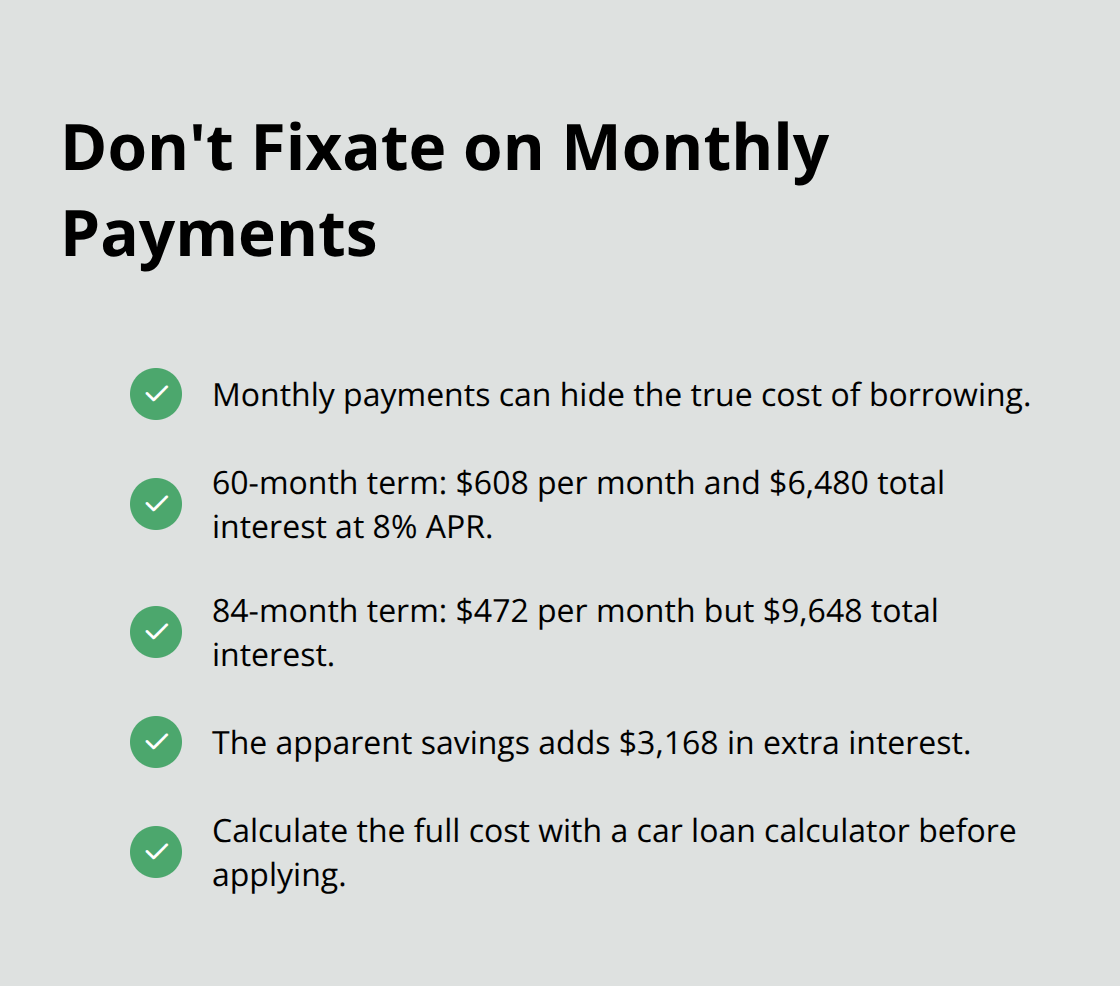

The Hidden Cost of Focusing Only on Monthly Payments

Dealers intentionally emphasize monthly payments because a smaller number obscures the true cost of borrowing. A $30,000 vehicle financed at 8% APR costs you $608 monthly over 60 months with $6,480 in total interest, but extending the term to 84 months drops the payment to $472 while pushing total interest to $9,648. That $136 monthly savings actually costs you an extra $3,168 in interest over the loan’s life.

Most borrowers fixate on fitting a payment into their monthly budget without calculating the total interest they’ll pay, which means they routinely choose longer terms that drain thousands from their finances. Calculate the total cost before you negotiate by adding the down payment, all monthly payments, and any fees to see the real price of your vehicle. A dealer will never volunteer this number because it reveals how much you’re actually paying for credit, so you must calculate it yourself using a car loan calculator before you apply anywhere.

Rate Locks Disappear When You Delay Your Application

Pre-approval rates expire depending on the lender, which means delaying your vehicle purchase costs you real money. If you obtain pre-approval at 6.2% but wait four months before finalizing your purchase, that rate vanishes and you’ll need to reapply at whatever the current market rate is. Market rates fluctuate based on the Bank of Canada’s decisions and overall lending conditions, so a delay that coincides with rising rates could push you from 6.2% to 7.1% on the same loan amount. Once you’ve secured pre-approval and found a vehicle, complete your purchase within the approval window to lock in your rate. Lenders understand that borrowers need time to shop for vehicles, which is why pre-approval windows exist, but procrastinating beyond that window forces you to start over and accept whatever rate environment exists at that time. The combination of shopping early, securing pre-approval quickly, and purchasing within 60 days protects you from rate fluctuations and keeps your financing cost predictable.

Final Thoughts

Securing the best car loan rates in Canada requires three concrete actions: check your credit score before applying, compare offers from at least three lenders within two weeks, and calculate the total cost of borrowing rather than fixating on monthly payments. The difference between accepting your dealer’s first offer and shopping around can easily exceed $2,000 in unnecessary interest on a single vehicle purchase. Your credit score, down payment size, and loan term are the levers you control to shift rates in your favor, and manufacturer financing promotions deserve serious consideration alongside traditional bank offers.

Pull your credit report from Equifax or TransUnion and dispute any errors immediately to start your car loan search. Once your score reaches 700 or higher, apply for pre-approval with your bank, a credit union, and one online lender like CarDoor or TD Auto Finance, then compare the written pre-approval letters side by side. This documentation becomes your negotiating power when you arrive at the dealership and transforms you from a passive buyer into someone who controls the conversation.

The most expensive mistake is delaying your purchase after securing pre-approval because rate locks expire and market conditions shift. Once you find your vehicle, complete the purchase within your approval window to lock in your rate. We at Financial Canadian offer resources and tools to help you make informed choices about car loan rates Canada and your broader financial planning.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment