Investment loan interest can significantly reduce your tax burden when claimed correctly. The Canada Revenue Agency allows deductions for interest paid on loans used to generate investment income.

We at Financial Canadian break down the investment loan interest tax deduction Canada rules and requirements. This guide covers eligibility criteria, calculation methods, and strategies to maximize your deductions.

What Makes Investment Interest Tax Deductible

The Canada Revenue Agency applies three strict tests to determine if your investment loan interest qualifies for tax deduction. Your borrowed funds must generate income through dividends, interest, rent, or royalties. Capital gains alone do not meet the income requirement, which eliminates many growth stock investments from eligibility.

Interest Rate Standards the CRA Enforces

The CRA can deny interest deductions in excess of a reasonable amount. Interest payments that exceed typical market rates often face scrutiny during audits. Lenders must charge rates that reflect current market conditions and your creditworthiness.

Documentation Requirements That Pass CRA Review

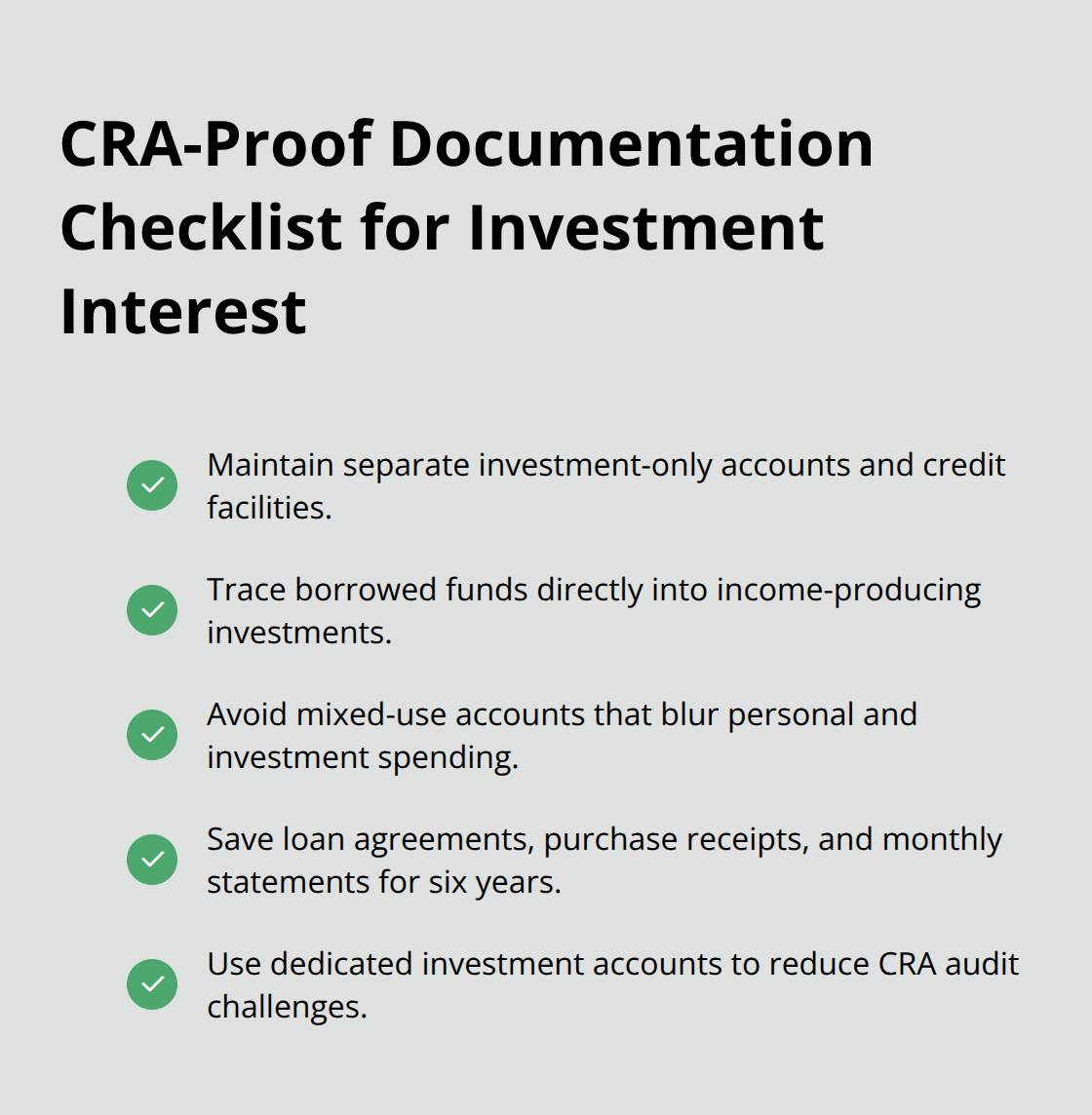

Maintain separate bank accounts and credit facilities exclusively for investment purposes. The CRA demands clear paper trails that show borrowed funds flowed directly into income-producing investments. Mixed-use accounts create complications during audits and may result in partial or complete deduction denials.

Save all loan agreements, investment purchase receipts, and monthly statements for at least six years. Investment advisors report that clients with dedicated investment accounts face fewer CRA challenges compared to those who use general-purpose credit lines.

Interest Deduction Limits You Must Know

Quebec residents face additional restrictions that limit investment expense deductions to annual investment income earned. This provincial rule can significantly reduce tax benefits for Quebec taxpayers with high borrowing costs relative to investment returns.

Interest on loans for RRSP, TFSA, or life insurance purchases remains completely non-deductible regardless of investment performance. The CRA also prohibits deductions when borrowed funds purchase tax-exempt investments (such as municipal bonds). Compound interest becomes deductible only when you actually pay it, not when it accrues on your loan balance.

These eligibility requirements form the foundation for your deduction claim, but the calculation process involves specific steps and forms that determine your actual tax savings.

How to Calculate and Claim Investment Interest Deductions

Track Your Investment Interest Payments Throughout the Year

Add all investment interest payments you made during the tax year to calculate your total deductible amount. The CRA requires cash-basis reporting for most taxpayers, which means you deduct interest only when you actually pay it, not when it becomes due.

Investment advisors at major Canadian banks report that clients who make quarterly interest payments often miss deductions because they fail to track mid-year payments. Keep monthly loan statements and bank records that show each interest payment amount and date.

Interest compounds daily on most investment loans, but you can only deduct the portion you actually paid during the tax year. This distinction becomes important when your loan agreement allows deferred interest payments or when you pay interest annually rather than monthly.

Report Investment Interest on Line 22100 of Your Tax Return

Enter your total deductible investment interest on Line 22100 under carrying charges and interest expenses. The CRA processes tax returns annually, and investment interest claims face higher audit rates when documentation appears incomplete.

Attach Form T776 if you claim rental property interest alongside investment loan interest, but keep investment and rental interest calculations separate. Quebec residents must also complete provincial forms and apply the investment income limitation rule that restricts deductions to actual investment income earned.

Avoid Common Filing Errors That Trigger CRA Reviews

Tax preparation software often miscategorizes investment interest as mortgage interest, which creates problems during CRA reviews. Double-check that your software places investment loan interest on the correct line item (mortgage interest goes on different tax lines and follows different deduction rules).

Never combine personal loan interest with investment loan interest on your tax return. The CRA can deny your entire deduction if you mix non-deductible personal interest with legitimate investment interest expenses.

These calculation steps set the foundation for your deduction claim, but strategic approaches can help you maximize the tax benefits from your investment borrowing decisions.

How Can You Maximize Your Investment Interest Deductions

Separate Investment Credit Lines Generate Better Tax Results

Establish dedicated investment credit lines with major Canadian banks rather than use existing personal lines of credit. Royal Bank of Canada and TD Bank offer investment-specific credit facilities that automatically track interest payments for tax purposes. These specialized accounts eliminate the documentation headaches that arise when you mix personal and investment borrowing on the same credit line.

Investment advisors at Scotiabank report that clients with dedicated investment credit facilities claim more in deductions compared to those who use mixed-purpose accounts. The CRA audits mixed-use accounts at higher rates because they require complex tracing of fund usage. A separate investment credit line creates an automatic paper trail that satisfies CRA documentation requirements without additional record-keeping efforts.

Time Your Interest Payments to Maximize Annual Deductions

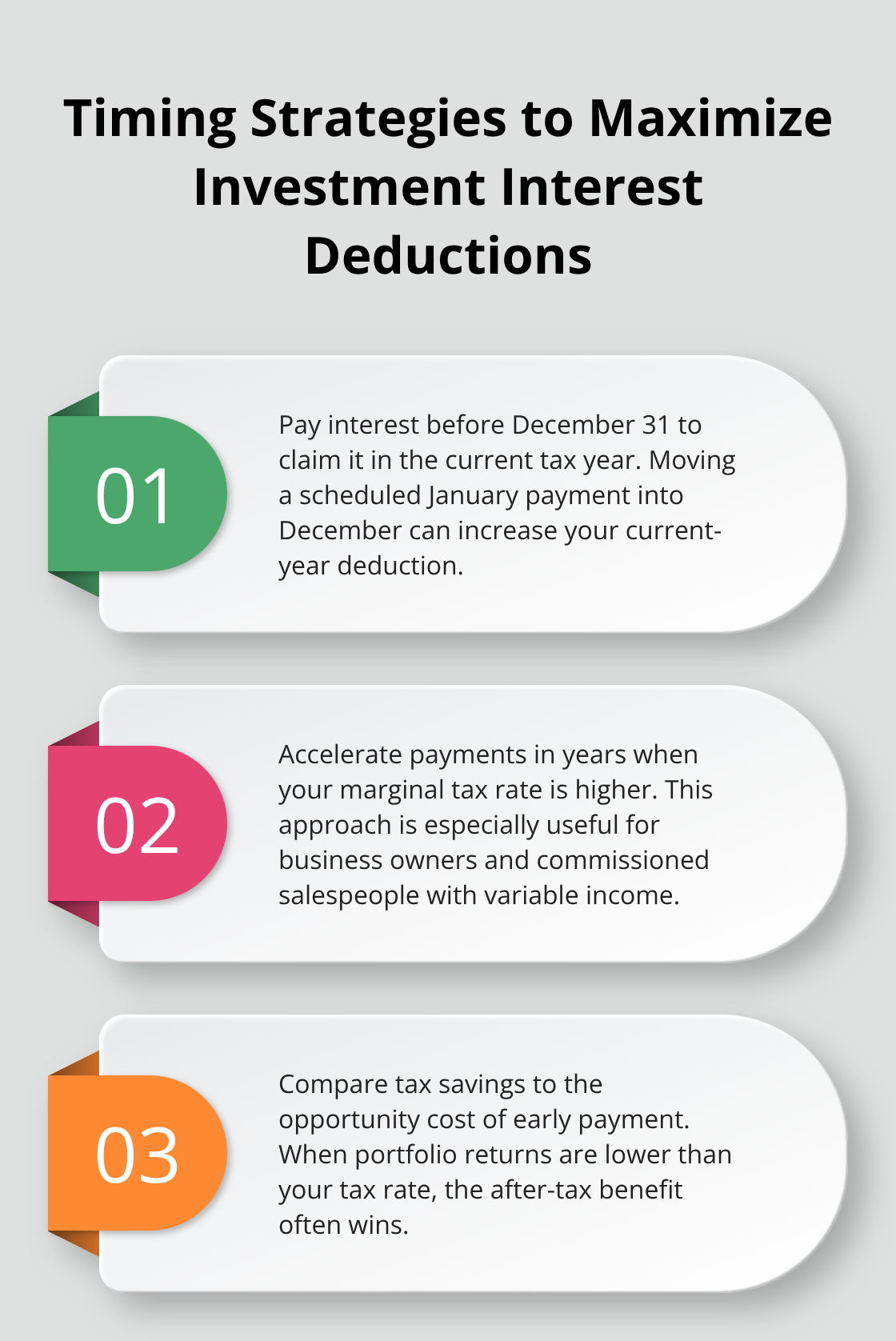

Pay investment loan interest before December 31st to claim the full deduction in the current tax year. Many investment loans allow quarterly or annual interest payment schedules, which creates opportunities to time your payments for maximum tax benefits. Accelerated interest payments into high-income years generate larger tax savings compared to spread payments across multiple years.

Tax professionals at PwC Canada recommend that you make January interest payments in December when your marginal tax rate exceeds 40%. This strategy works particularly well for business owners and commissioned salespeople who experience variable annual income. The tax savings from accelerated interest payments often exceed the opportunity cost of early payment (especially when your investment portfolio generates lower returns than your marginal tax rate).

Structure Your Investment Portfolio for Maximum Deductibility

Focus your borrowed funds on dividend-paying stocks and interest-bearing securities rather than growth investments. The CRA only allows deductions when investments produce regular income through dividends, interest, rent, or royalties. Capital gains alone do not qualify for interest deduction purposes, which makes growth-focused portfolios less tax-efficient when you use borrowed money.

Canadian dividend stocks from major banks and utilities provide the most reliable income streams for interest deduction purposes. These investments typically yield 3-5% annually through dividends, which satisfies CRA income requirements while you benefit from potential capital appreciation as a bonus.

Final Thoughts

Investment loan interest tax deduction Canada rules demand strict adherence to CRA requirements and meticulous documentation. Your borrowed funds must produce income through dividends, interest, rent, or royalties to qualify for deductions. Capital gains alone never satisfy the income test, which excludes many growth investments from eligibility.

Successful claims require separate investment accounts and detailed tracking of all interest payments throughout the tax year. You must report your deductible interest on Line 22100 and maintain comprehensive records for at least six years. Quebec residents face additional limitations that restrict deductions to actual investment income earned annually (which can significantly reduce available tax benefits).

Strategic borrowing through dedicated investment credit lines and proper payment timing before December 31st maximizes your tax benefits. Professional tax advice becomes essential when you deal with complex investment structures or significant borrowing amounts. We at Financial Canadian offer comprehensive web design services to help businesses establish their digital presence and grow their operations effectively.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment