Home renovations can transform your living space, but they often come with a hefty price tag. At Financial Canadian, we understand that figuring out how to finance a home renovation can be challenging.

Whether you’re dreaming of a kitchen makeover or a complete home overhaul, we’re here to guide you through the various financing options available. In this post, we’ll explore practical ways to fund your renovation project while keeping your financial health in check.

Assessing Your Renovation Budget

Define Your Project Scope

Start your home renovation journey by clearly outlining your project goals. Do you plan to update a single room or tackle multiple areas? Create a list of must-haves and nice-to-haves to help prioritize your budget decisions.

A 2024 Houzz study reveals findings from a survey of 3437 U.S. homeowners about their recent or planned kitchen renovation projects.

Calculate All Costs

Look beyond the big-ticket items when budgeting. Include costs for permits, design fees, and temporary housing (if needed). The Home Improvement Research Institute reports that 61% of homeowners postponed or canceled projects in 2023 due to budget concerns. Avoid this pitfall with thorough cost estimation.

Try to add 10% to 25% to your initial budget for unexpected expenses. This buffer can cover surprises like structural issues or material price increases.

Align Budget with Finances

Examine your current financial situation closely. How much can you realistically afford to spend on this renovation? Consider your income, savings, and other financial obligations.

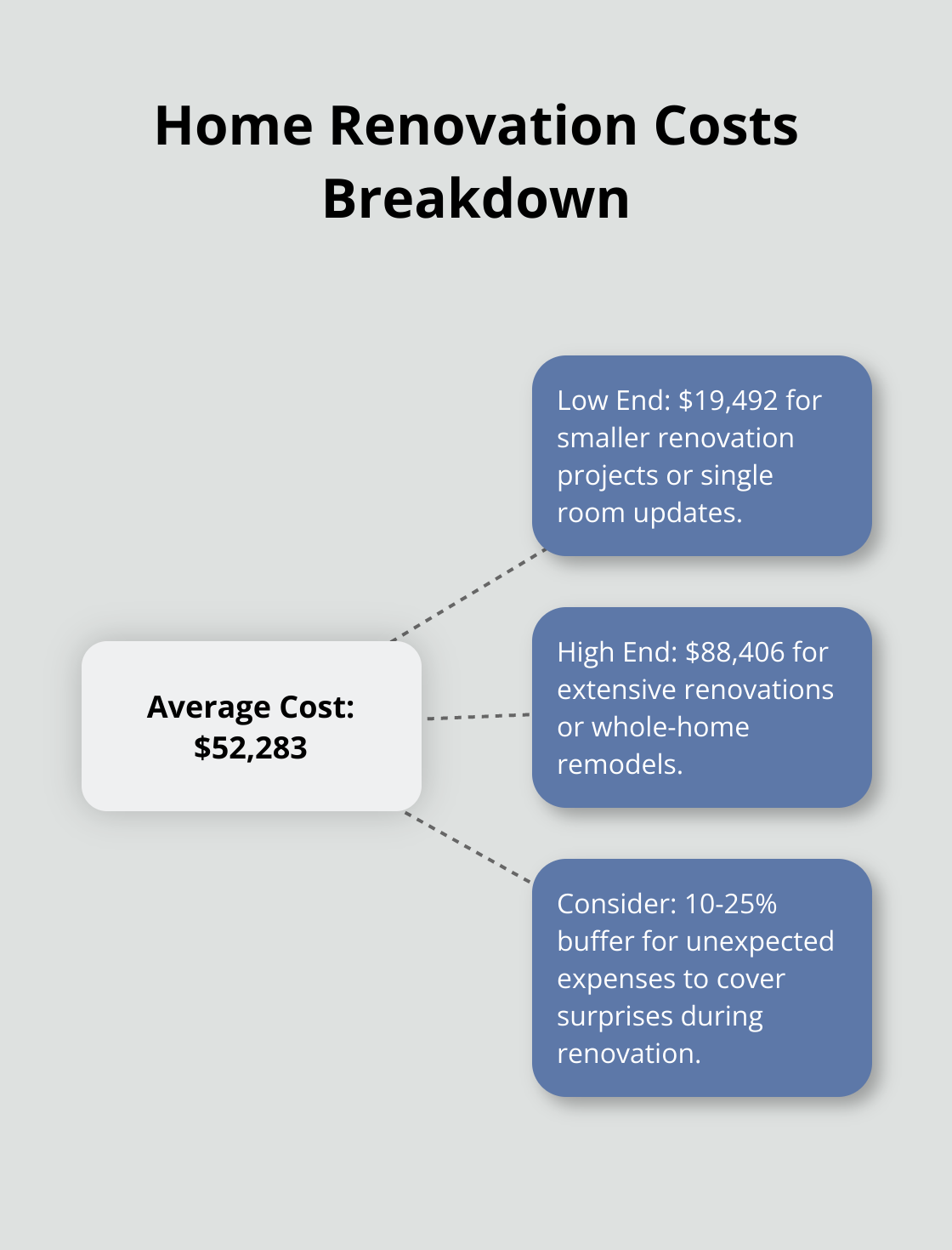

If you plan to finance your renovation, check your credit score. This will impact your loan options and interest rates. Angi reports that the average cost of a home renovation is $52,283 (with a range from $19,492 to $88,406). Use these figures to gauge where your project falls on the spectrum.

Cash remains the best way to pay for home renovations. If that’s not possible, explore financing options that align with your financial goals. FinancialCanadian.com offers comprehensive guides on various financing options to help you make an informed decision.

Consider Long-Term Value

Think about how your renovation will impact your home’s value. Some projects (like kitchen upgrades or adding a home office) can significantly boost your property’s worth. This consideration helps justify costs and can influence your budget decisions.

Get Multiple Quotes

Don’t settle for the first contractor you find. Obtain at least three quotes for your project. This practice not only ensures competitive pricing but also gives you a better understanding of the market rates for your specific renovation.

Thorough budget assessment sets the stage for smart financial decisions throughout your project. This careful planning can help you avoid overspending and ensure your renovation enhances both your home and financial well-being. Now, let’s explore the popular financing options available for your home renovation project.

Financing Options for Your Home Renovation

Home Equity Loans and HELOCs

Home equity loans and Home Equity Lines of Credit (HELOCs) stand out as popular choices for homeowners with significant equity. These options typically offer lower interest rates compared to unsecured loans because your home serves as collateral.

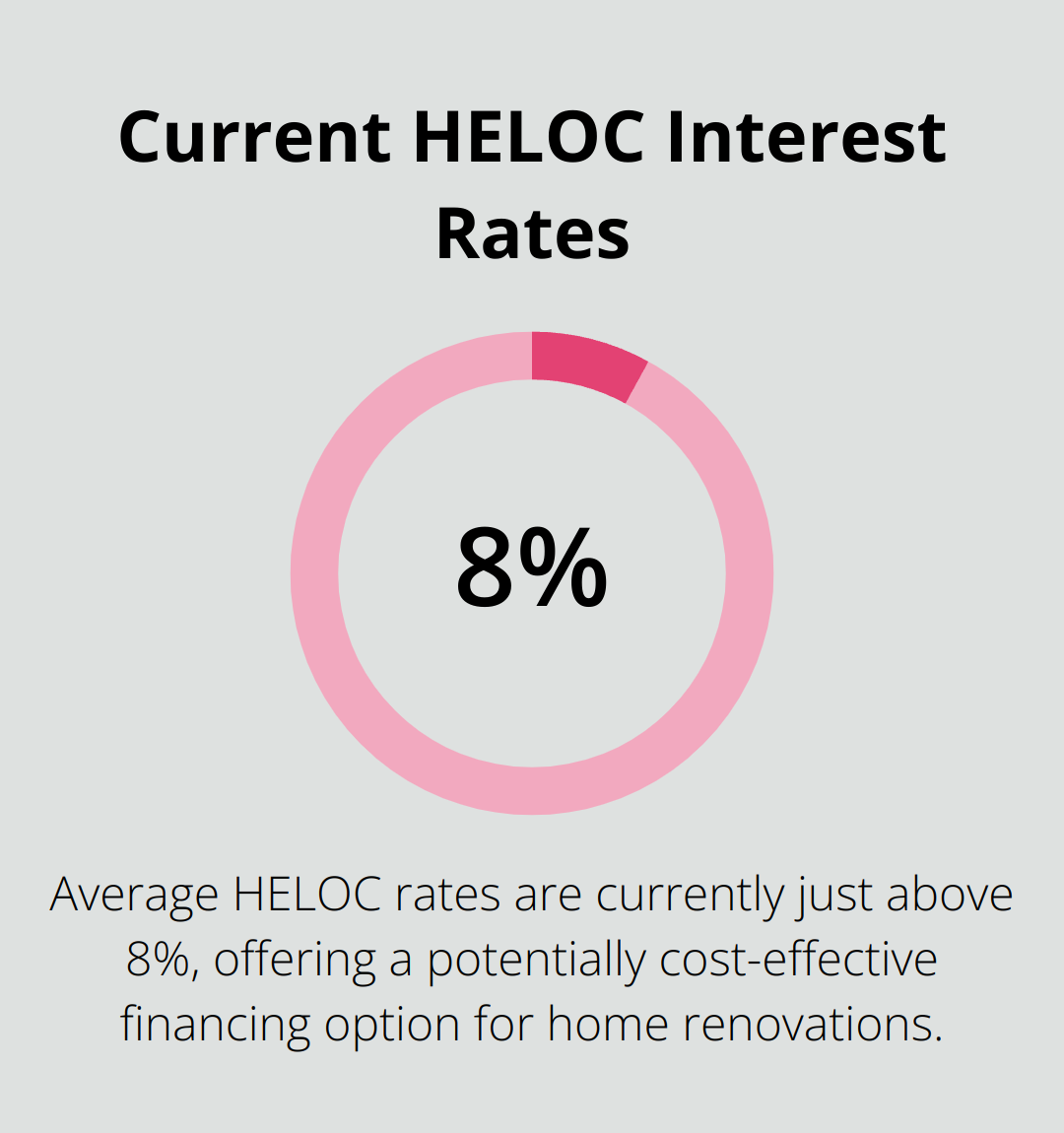

A home equity loan provides a lump sum that you repay in fixed monthly installments. HELOCs, in contrast, offer a revolving credit line that you can draw from as needed. Average HELOC rates are currently just above 8%, according to data from Bankrate.

However, exercise caution. Using your home as collateral puts you at risk of foreclosure if you default on payments. Borrow only what you can comfortably repay.

Personal Loans and Credit Cards

Personal loans and credit cards present viable alternatives for those who prefer not to tap into their home equity or lack sufficient equity.

Personal loans feature fixed interest rates and predictable monthly payments. As of May 2025, personal loan rates range from 6% to 36% (depending on your credit score and income).

Credit cards can suit smaller renovations or serve as a short-term solution. Some cards offer 0% APR introductory periods, which can benefit you if you pay off the balance before the promotional period ends. However, watch out for high interest rates after the promotional period expires.

Government-Backed Renovation Loans

The government offers several loan programs designed specifically for home improvements. The FHA 203(k) loan insures mortgages covering the purchase or refinancing and rehabilitation of a home that is at least a year old.

Another option is the Title I Property Improvement Loan program, insured by the Federal Housing Administration. These loans let you borrow up to $25,000 for single-family home improvements, with repayment terms of up to 20 years.

Government-backed loans often have more lenient credit requirements and competitive interest rates. However, they may come with specific usage restrictions and require more paperwork.

Choosing the Right Option

The best financing option depends on various factors, including your credit score, home equity, and the size of your renovation project. Consider the long-term implications of any financing decision on your overall financial health.

To navigate the complexities of each choice, try to compare the terms, rates, and requirements of different financing options. Websites like FinancialCanadian.com offer comprehensive guides and comparisons to help you make an informed decision.

As you weigh your options, it’s important to consider not just the immediate costs, but also how each choice will impact your long-term financial goals. Let’s explore how to evaluate these factors in the next section.

Selecting Your Ideal Renovation Financing

Compare Interest Rates and Terms

Start your financing decision by comparing Annual Percentage Rates (APRs) of different options. Credit cards can offer various options for cash back, travel rewards, and 0% APR introductory periods. Personal loans range from 6% to 36%.

Examine loan terms carefully. Home equity loans and HELOCs typically allow repayment periods up to 30 years, while personal loans usually span 2 to 7 years. Longer terms result in lower monthly payments but increase total interest paid over time.

Evaluate Your Financial Health

Your credit score plays a significant role in determining financing options and rates. Canadian credit scores range from 300 to 900, with scores above 760 considered excellent and qualifying for the best rates. Scores below 660 may lead to higher interest rates or difficulties in loan qualification.

Income also factors into lender decisions. Most lenders prefer a debt-to-income ratio below 43%. Calculate this ratio by dividing your monthly debt payments by your gross monthly income. If your ratio exceeds this threshold, focus on increasing income or reducing debt before applying for a loan.

Consider Long-Term Financial Impact

Different financing options can affect your future financial goals. A home equity loan might offer lower rates but increases your mortgage debt and could impact your ability to sell or refinance your home later.

Personal loans keep your home equity intact but often come with higher rates and shorter repayment terms, potentially straining your monthly budget.

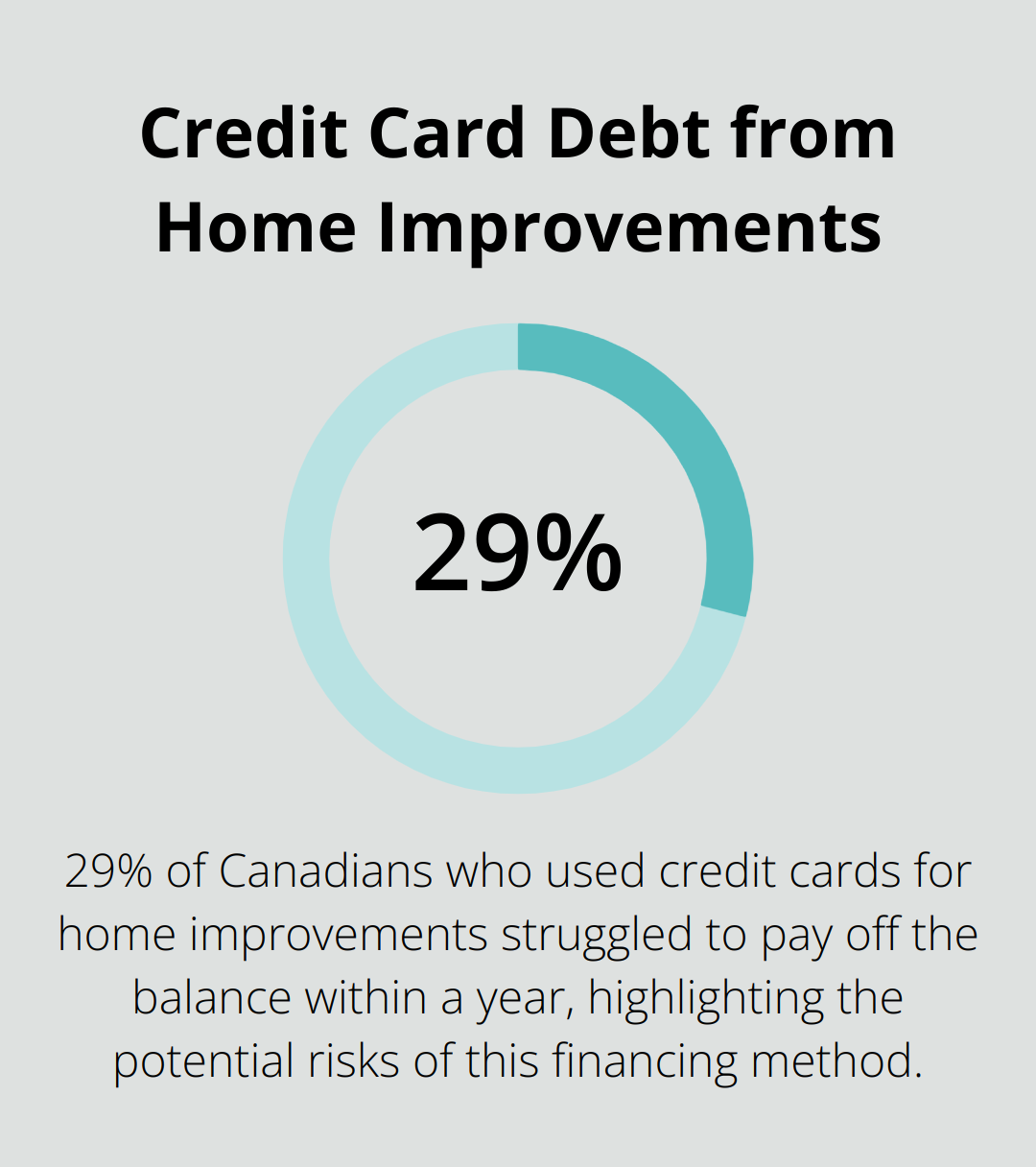

Credit cards can tempt you for smaller renovations, but carrying a balance can quickly accumulate significant debt. A 2024 study by the Financial Consumer Agency of Canada found that 29% of Canadians who used credit cards for home improvements struggled to pay off the balance within a year.

Seek Expert Advice

While online resources provide valuable information, consulting with a financial advisor or mortgage professional can offer personalized insights. These experts can help you understand tax implications of different financing options and how they align with your overall financial strategy.

Many banks and credit unions offer free consultations (take advantage of these services to get expert opinions on your specific situation).

Align with Your Renovation Goals

Choose a financing option that matches the scale and timeline of your renovation project. For major renovations, a home equity loan or HELOC might provide the necessary funds. For smaller projects, a personal loan or strategically used credit card might suffice.

Consider the potential return on investment for your renovation. Some projects (like kitchen or bathroom upgrades) tend to add more value to your home, potentially justifying a larger loan.

Final Thoughts

Financing a home renovation requires careful planning and consideration of various options. Home equity loans, HELOCs, personal loans, credit cards, and government-backed programs each offer unique advantages and potential drawbacks. Your credit score, available equity, project scope, and long-term financial goals will determine the best financing method for your renovation.

Expert advice from financial advisors and mortgage professionals can provide valuable insights tailored to your specific circumstances. These professionals can help you navigate the complexities of different financing options and ensure your renovation plans align with your overall financial strategy. Accurate cost estimation, including a buffer for unexpected expenses, will help you avoid common pitfalls that lead to project delays or cancellations.

At Financial Canadian, we understand the challenges of financing a home renovation. We offer web design services to help businesses establish a strong online presence, and we recognize the importance of sound financial planning in all aspects of life. Our commitment is to provide you with the resources and support you need to make informed decisions about your home improvement projects.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment