Credit card interest rates in Canada range from 8.99% to over 29%, making the right choice worth thousands in savings annually.

We at Financial Canadian have analyzed dozens of low interest credit cards Canada offers to help you find the best options. Most Canadians pay far more than necessary on credit card interest simply because they don’t know where to look or how to qualify for better rates.

What Makes a Credit Card Low Interest in Canada

Any credit card with an interest rate below 13% qualifies as low interest in the Canadian market, according to the Canadian Bankers Association. The Bank of Canada reports that the average purchase interest rate sits at 20.65% as of November 2024, which makes cards under 13% significantly better deals. The National Bank Syncro Mastercard currently leads with the lowest rate at 8.90%, while the RBC RateAdvantage Visa starts at Prime plus 4.99%. These rates can save you hundreds or thousands annually compared to typical rewards cards that charge 19.99% to 23.99%.

Fixed vs Variable Rate Cards

Fixed rate cards maintain the same interest rate throughout your card ownership and provide predictable monthly payments. Variable rate cards fluctuate with the Bank of Canada’s prime rate, which currently affects most low interest options. The Desjardins Flexi Visa offers fixed rates at 10.90% and 12.90% with no annual fee, while variable rate cards like the Scotiabank Value Visa provide 0.99% introductory rates on balance transfers for nine months. Variable cards typically offer better promotional rates but deliver less long-term certainty.

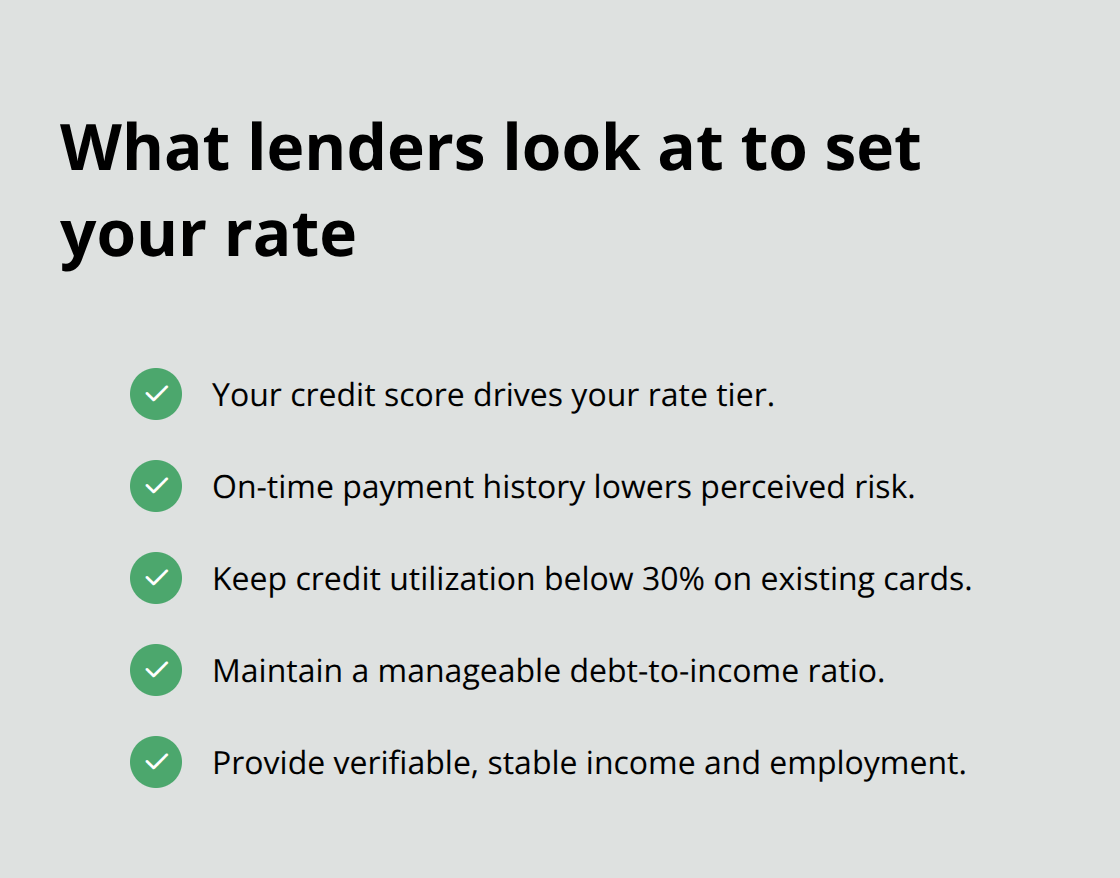

How Lenders Set Your Interest Rate

Your credit score determines which interest rate tier you receive within a card’s range. Lenders evaluate your payment history, credit use below 30%, and debt-to-income ratio when they set rates. Income verification and employment stability also influence approval odds and rate offers.

Cards advertise ranges like 8.99% to 21.99%, but only applicants with credit scores of at least 700 typically qualify for the lowest advertised rates. Poor credit scores often result in penalty rates that exceed 25% (making credit improvement essential before you apply).

Interest Rate Calculation Methods

Credit card companies calculate interest daily based on your Annual Percentage Rate divided by 365 days, then charge you monthly. Most cards offer a 21-day grace period where you pay no interest if you pay your full balance on time. Cash advances typically carry higher rates and start accumulating interest immediately without any grace period. Balance transfer fees usually range from 1% to 3% of the transferred amount, which affects your total cost savings when you move debt between cards.

The next step involves knowing where to find these low interest options and how to compare them effectively across different lenders. Whether you have good credit, or bad credit, understanding your options helps you secure the best available rates.

Where to Find Low Interest Credit Cards in Canada

Canada’s Big Six banks control the credit card market and offer competitive low interest options. Royal Bank of Canada leads with the RateAdvantage Visa at Prime plus 4.99%, while National Bank delivers the lowest rate at 8.90% on their Syncro Mastercard. TD Bank and BMO typically offer rates between 12.99% and 15.99% on their low interest products.

Credit unions like Vancity and Meridian often provide competitive rates because they operate as member-owned cooperatives with lower profit margins. Desjardins stands out among Quebec institutions with their Flexi Visa that offers fixed rates at 10.90% without annual fees.

Online Comparison Platforms Speed Up Your Research

RateSupermarket and LowestRates aggregate real-time rates from dozens of lenders and let you compare options in minutes rather than visit individual bank websites. These platforms show current promotional rates, balance transfer offers, and qualification requirements side by side. CardFinder specializes in pre-qualification checks that won’t hurt your credit score and helps you identify realistic options before formal applications.

Most comparison sites earn commissions from lenders, so they highlight cards with higher referral fees rather than necessarily the best rates for your situation (which means you need to look beyond their featured recommendations).

Credit Unions Offer Hidden Gems

Local credit unions frequently provide rates 1-3% lower than major banks but require membership in specific communities or professions. Servus Credit Union in Alberta offers rates as low as 9.99% to members, while Coast Capital Savings provides competitive options across British Columbia. These institutions focus on member benefits rather than shareholder profits, which translates to better rates for qualified applicants.

Skip Credit Card Brokers and Financial Advisors

Credit card brokers add unnecessary costs and complexity to what should be a straightforward process. These intermediaries typically push products that pay them the highest commissions rather than find you the lowest rates. Financial advisors focus on investments and insurance, not credit card optimization (making their credit card advice often outdated or generic).

The most effective approach involves direct applications with lenders after initial research through comparison sites. This strategy helps you access promotional rates that brokers can’t match and avoid unnecessary markups. For consumers who need additional quick finance options beyond credit cards, specialized lenders can provide alternative solutions. Your next step requires understanding the qualification requirements that determine which low interest rates you can actually obtain.

How to Qualify for the Best Low Interest Rates

Lenders require credit scores of 660 or higher for their advertised low interest rates, with the best rates reserved for scores above 700. According to Equifax, super-prime consumers (those with credit scores of 750 or higher) represent the only growth segment in new credit card originations. The National Bank Syncro Mastercard at 8.90% typically requires scores of 720 or better, while the RBC RateAdvantage Visa accepts scores at 660 but offers Prime plus 4.99% only to applicants with scores above 680.

Credit Score Requirements for Different Rate Tiers

Banks structure their interest rates in tiers based on credit score ranges. Scores between 660-699 qualify for mid-tier rates around 12.99% to 15.99%, while scores of 700-749 access rates between 9.99% to 12.99%. Premium rates below 10% require scores of 750 or higher at most major lenders. Applicants with scores below 660 face rejection or receive rates above 19.99% (which defeats the purpose of a low interest card).

Income Requirements Vary by Card Type

Major banks require minimum annual incomes between $15,000 and $35,000 for low interest cards, with higher requirements for premium products. TD Bank requires $12,000 annual income for their low interest Visa, while Scotiabank sets the bar at $15,000 for their Value Visa. Employment verification through recent pay stubs or tax returns becomes mandatory for incomes below $60,000. Self-employed applicants face stricter documentation requirements that include two years of tax returns and business financial statements.

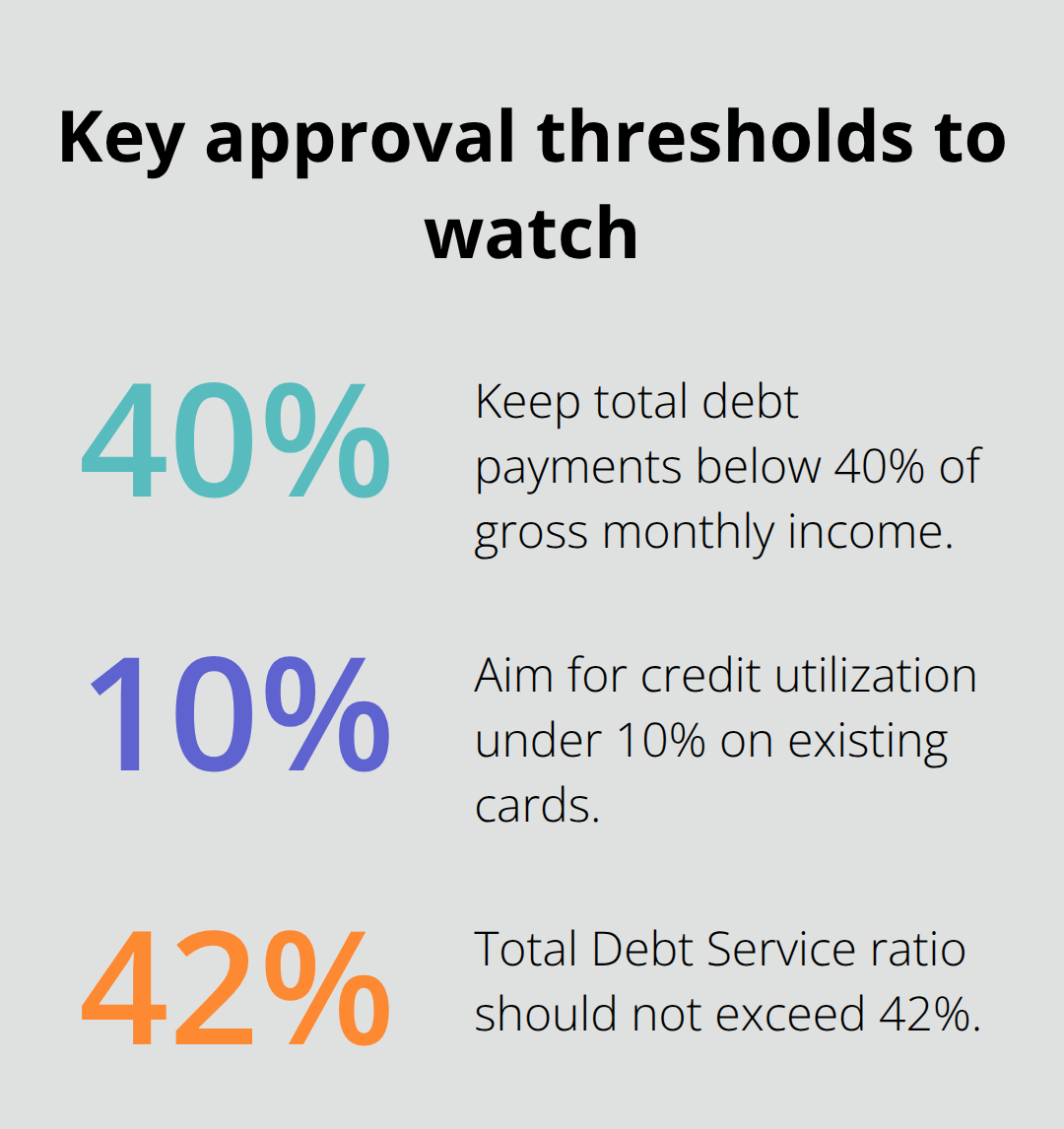

Debt-to-Income Ratios Determine Final Approval

Canadian lenders prefer total debt payments below 40% of gross monthly income, which includes the new credit card limit you request. Someone who earns $4,000 monthly should keep total debt payments under $1,600 to qualify for the best rates. Credit utilization below 10% on cards you already have signals responsible credit management and improves approval odds significantly. The Total Debt Service ratio must not exceed 42%, and applicants above this threshold typically receive higher rates or face rejection, regardless of credit scores.

Strategies to Improve Your Qualification Odds

Pay down existing balances before you apply to improve your debt ratios and secure better interest rates on new cards. Request credit limit increases on current cards to lower your utilization percentage without additional debt. Check your credit report for errors and dispute any inaccuracies that could lower your score. Wait at least six months between credit applications to avoid multiple inquiries that damage your credit profile. If you have bad credit, specialized lenders can still help you find financing options while you work to improve your credit standing.

Final Thoughts

Low interest credit cards Canada provides require a strategic approach that combines thorough research with realistic qualification expectations. Check your credit score and improve it to at least 700 before you apply for the best rates. Compare options across major banks, credit unions, and online platforms to identify cards with rates below 13%.

Focus on your debt-to-income ratio and keep credit utilization under 30% to maximize approval odds. Apply directly with lenders after you use comparison tools for initial research. Avoid brokers who add unnecessary costs and complexity to the process (consider fixed-rate cards for predictable payments or variable-rate options for promotional offers).

Your financial success depends on informed decisions about credit products. We at Financial Canadian help businesses establish strong digital footprints with our comprehensive web design service. Take action by checking your credit score, researching current rates, and applying for cards that match your qualification profile.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment