Getting a personal loan with horrible credit feels impossible, but it’s not. Millions of Canadians face this challenge every year.

We at Financial Canadian know the right strategies can open doors even with poor credit scores. The key lies in understanding your options and approaching the right lenders with a solid plan.

What Constitutes Horrible Credit in Canada

Credit Score Thresholds That Matter

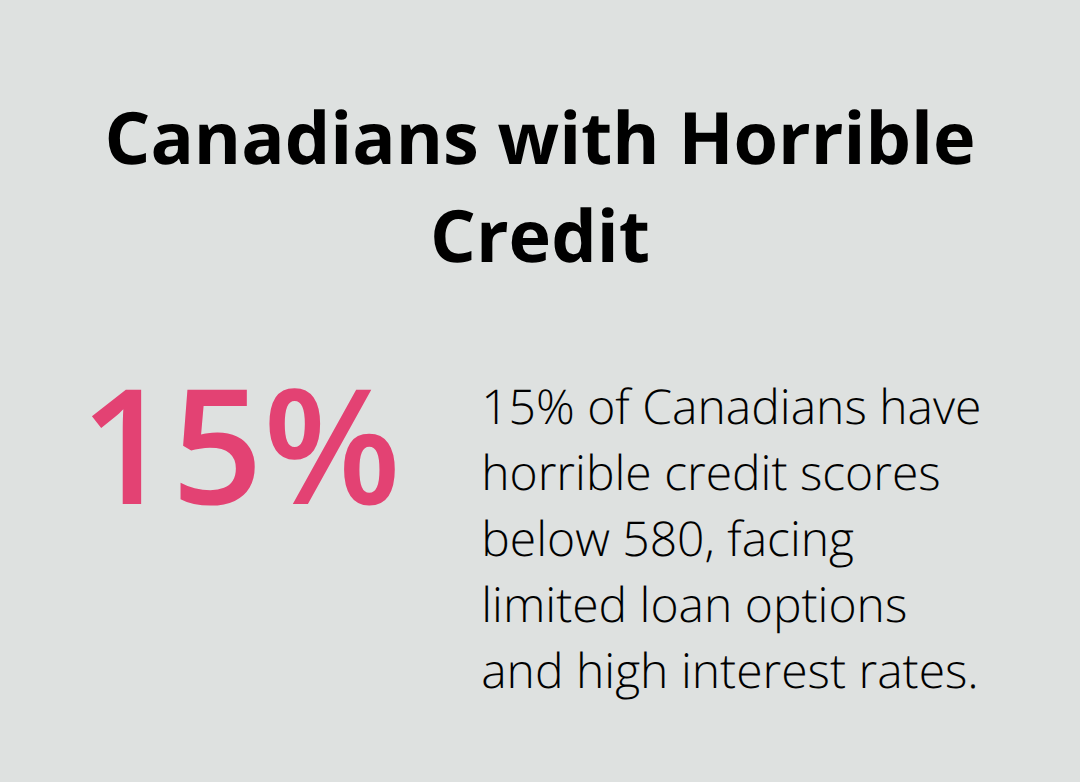

Horrible credit in Canada means a credit score below 580, according to Equifax data. This puts you in the poor credit category where traditional banks reject your loan applications almost instantly. TransUnion considers scores between 300-559 as poor, while anything below 650 makes it extremely difficult to secure favorable loan terms. About 15% of Canadians fall into this category and face limited options with sky-high interest rates.

Your Loan Options with Poor Credit

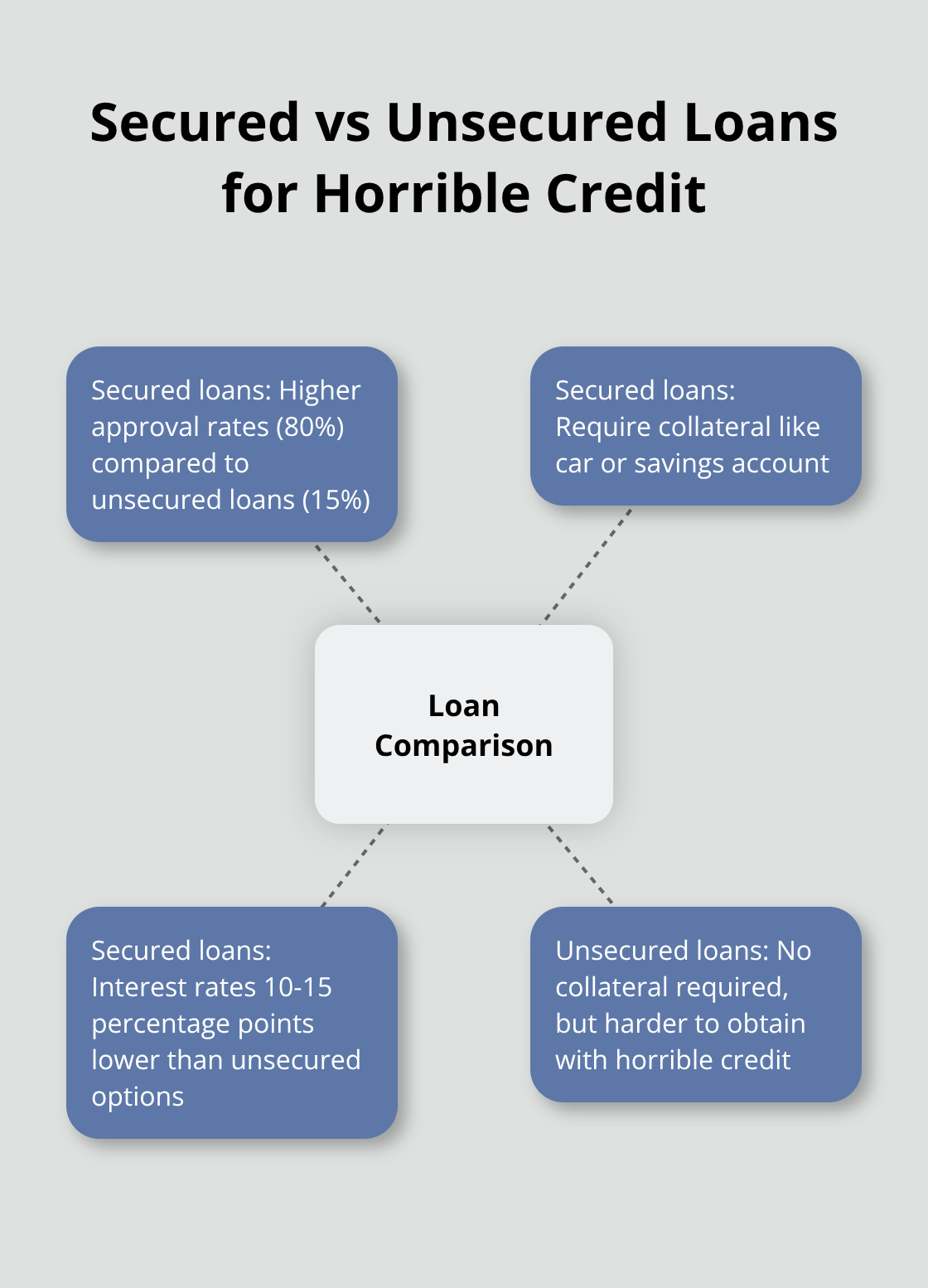

Secured personal loans represent your best option with horrible credit. These loans require collateral like your car or savings account, but approval rates jump to 80% compared to 15% for unsecured loans. OneMain Financial approves secured loans even with scores as low as 450 and offers amounts up to $20,000. Alternative lenders like Paymi or PayDay All Day provide smaller amounts between $300-$5,000 with approval rates above 90%, though interest rates often exceed 40% annually.

The Financial Impact of Low Scores

Credit scores below 580 trigger interest rates between 6-24% on personal loans from major Canadian banks and financial institutions. A $5,000 loan at 24% APR costs significantly more over three years than the same loan at 6%. Lenders like Avant start approvals at 580 credit scores with competitive rates, while Upstart considers alternative data like education and income, potentially lowering rates even with poor credit scores.

The good news? You can take specific steps to improve your approval chances and access better terms, even with horrible credit.

How Can You Boost Your Loan Approval Odds?

Get a Co-signer with Strong Credit

A co-signer with a credit score above 700 can significantly improve your approval chances. Your co-signer becomes legally responsible for the loan if you default, which dramatically reduces lender risk. Credit unions like Meridian Credit Union approve 90% of applications with qualified co-signers, even when primary borrowers have scores below 500.

Choose someone with stable income, low debt-to-income ratios, and excellent payment history. Parents or siblings often serve as co-signers, but they must understand the financial commitment. If you miss payments, their credit score suffers too.

Secure Your Loan with Valuable Assets

Collateral transforms rejection into approval for borrowers with horrible credit. Vehicle title loans through companies like Canada Drives approve 95% of applications regardless of credit scores and offer amounts up to 50% of your car’s value. Savings-secured loans use your bank account as collateral, with approval rates near 100% at most credit unions.

Home equity represents the strongest collateral option, with rates as low as 3.5% through traditional banks. Equipment, jewelry, or investment accounts also work as collateral. Secured loans typically offer interest rates 10-15 percentage points lower than unsecured options (which saves thousands over the loan term).

Document Your Financial Stability

Steady employment history and consistent income matter more than credit scores to many alternative lenders. Lenders like Paymi approve borrowers with two years of continuous employment, even with bankruptcy history. Provide recent pay stubs, tax returns, and employment verification letters to strengthen your application.

Self-employed borrowers need bank statements that show regular deposits over six months. Income stability beats high income – lenders prefer $40,000 annually for three years over $80,000 for six months. Some lenders accept government benefits, disability payments, or pension income as income sources (which expands your options significantly).

These strategies work best when you target the right lenders who specialize in bad credit loans and understand your specific situation.

Which Lenders Actually Approve Bad Credit Applications

Online Lenders That Say Yes When Banks Say No

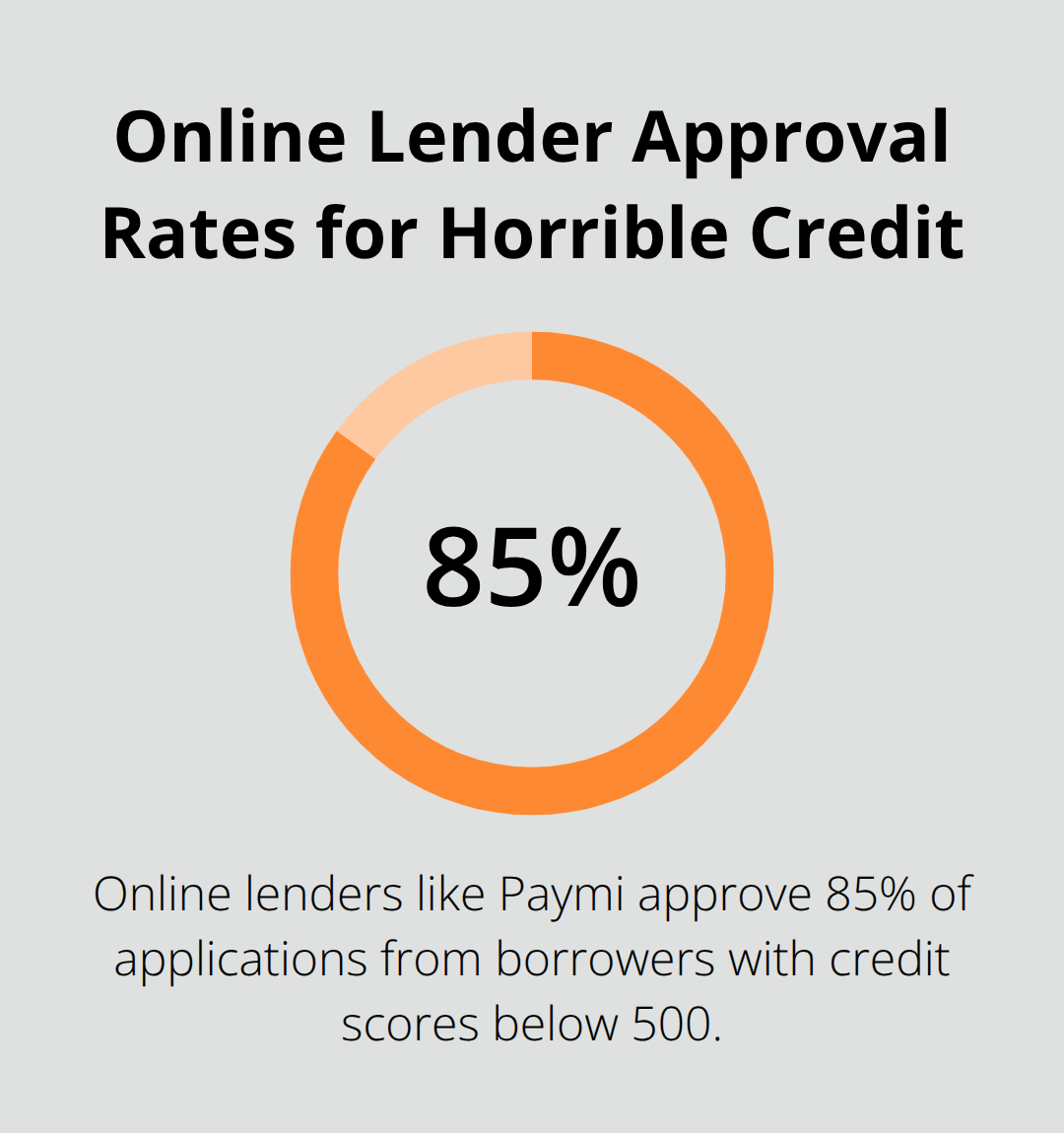

Paymi approves 85% of applications from borrowers with credit scores below 500 and funds loans within 24 hours. Their loan amounts range from $500 to $5,000 with interest rates between 19.9% and 46.96%, which makes them accessible for emergency expenses. PayDay All Day offers similar approval rates but focuses on smaller amounts up to $1,500 for short-term needs. These lenders use alternative data like employment history and bank account activity rather than credit scores alone.

Lending Loop specializes in personal loans for Canadians with poor credit and approves amounts up to $35,000 with flexible repayment terms. Their approval process takes under 48 hours and considers factors like rent payment history and utility bill payments. Spring Financial operates across Canada except Quebec and approves loans from $500 to $35,000 with competitive rates that start at 9.99% for secured options. Both lenders report payments to credit bureaus, which helps borrowers rebuild their credit scores over time.

Credit Unions That Work With Your Situation

Meridian Credit Union approves 78% of bad credit applications and offers personal loans up to $50,000 with rates that start at 7.25% for members. Their community-focused approach means loan officers review applications individually rather than use automated systems that reject low scores instantly. Vancity Credit Union in British Columbia approves loans for members with scores as low as 450 when they demonstrate stable income and provide detailed explanations for past credit issues.

Local credit unions like Libro Credit Union in Ontario and Conexus Credit Union in Saskatchewan offer personalized service and flexible criteria. These institutions often require membership but provide better rates than online lenders (membership typically costs $5-25 and requires a small savings account balance). The improved loan terms justify these minimal requirements for borrowers with horrible credit.

Alternative Platforms That Consider More Than Credit Scores

Peer-to-peer platforms like Paymi and alternative lenders focus on your complete financial picture rather than just credit scores. These platforms connect borrowers directly with individual investors who fund loans based on income stability and employment history. Approval rates reach 70% for borrowers with scores below 600, and interest rates often beat traditional bad credit lenders by 5-10 percentage points.

Some platforms use cash flow underwriting technology to analyze your spending patterns and cash flow (which provides a more accurate picture of your ability to repay). This approach helps borrowers with temporary credit issues but stable finances access better rates and terms than traditional bad credit products offer.

Final Thoughts

You can secure a personal loan with horrible credit when you apply the right strategies and target appropriate lenders. Check your credit report for errors first, then focus on secured loans with collateral or find a qualified co-signer. Online lenders like Paymi and Spring Financial approve 85% of bad credit applications, while credit unions offer personalized service with better rates.

Document your income stability through recent pay stubs and employment verification letters to strengthen your application. Alternative platforms analyze your complete financial picture rather than just credit scores (which opens more opportunities for approval). These lenders often provide better terms than traditional bad credit products and help you access funds when banks reject your application.

Make every payment on time to rebuild your credit score and avoid additional debt while you repay your loan. Set up automatic payments to prevent missed deadlines and monitor your credit report monthly for improvements. We at Financial Canadian provide comprehensive web design services that help businesses establish strong digital presence and drive growth.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment