At Financial Canadian, we understand the challenges of securing loans with less-than-perfect credit.

Poor credit personal installment loans can be a viable option for those facing financial hurdles. These loans offer more flexibility and potentially better terms compared to payday loans.

In this guide, we’ll explore how you can access personal installment loans even with a low credit score, and provide practical tips to improve your chances of approval.

What Are Personal Installment Loans for Poor Credit?

Definition and Structure

Personal installment loans for poor credit provide financial assistance to individuals with low credit scores. These loans typically range from $1,000 to $35,000. Borrowers repay the loan in fixed monthly installments over a set period (usually 12 to 60 months).

Installment Loans vs. Payday Loans

Installment loans offer significant advantages over payday loans:

- Longer repayment periods: While payday loans require full repayment within two weeks, installment loans spread payments over months or years.

- More manageable payments: A $1,000 payday loan might demand full repayment plus fees in 14 days. In contrast, a $1,000 installment loan allows repayment over 12 months in smaller, fixed amounts.

- Lower risk of debt traps: The extended repayment structure helps borrowers avoid the debt cycle often associated with payday loans.

Credit Score Requirements

Credit score requirements vary widely among lenders. Your lender or insurer may use a different FICO® Score than FICO® Score 8, or another type of credit score altogether.

However, lenders don’t solely focus on credit scores. They also evaluate:

- Income stability

- Debt-to-income ratio

- Employment history

- Collateral (for secured loans)

For example, OneMain Financial (which caters to borrowers with poor credit) examines the overall financial picture. They might approve a loan for someone with a 500 credit score if they have a stable job and low debt-to-income ratio.

Interest Rates and Fees

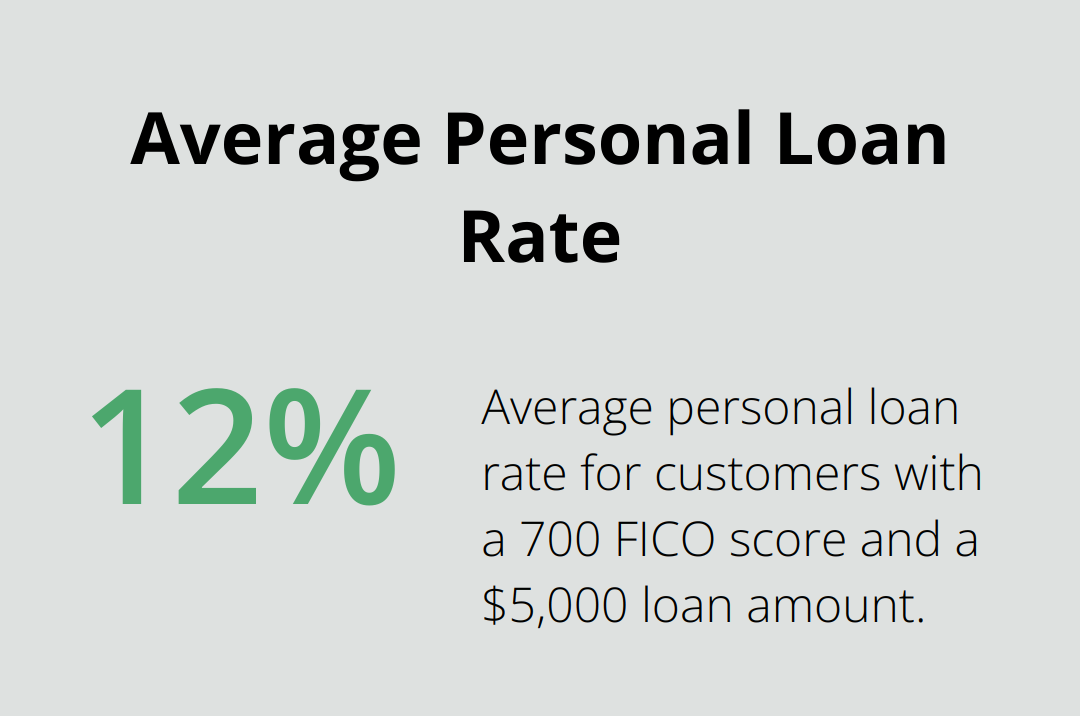

Personal installment loans for poor credit often come with higher interest rates. According to Bankrate Monitor data, as of Aug. 13, 2025, the average personal loan rate is 12.58 percent for customers with a 700 FICO score and a $5,000 loan amount.

We at Financial Canadian always recommend comparing offers from multiple lenders. This approach can help you find the most competitive rates, even with poor credit. A slightly lower APR can save you hundreds (or even thousands) of dollars over the life of your loan.

The Application Process

Applying for a personal installment loan typically involves these steps:

- Pre-qualification: Many lenders offer this option, which doesn’t affect your credit score.

- Formal application: You’ll need to provide personal and financial information.

- Document submission: This may include proof of income, bank statements, and identification.

- Approval and funding: If approved, you’ll receive the funds, often within a few business days.

As we move forward, let’s explore the various options available for personal installment loans with poor credit, including specialized online lenders and credit unions.

Where Can You Find Personal Installment Loans for Poor Credit?

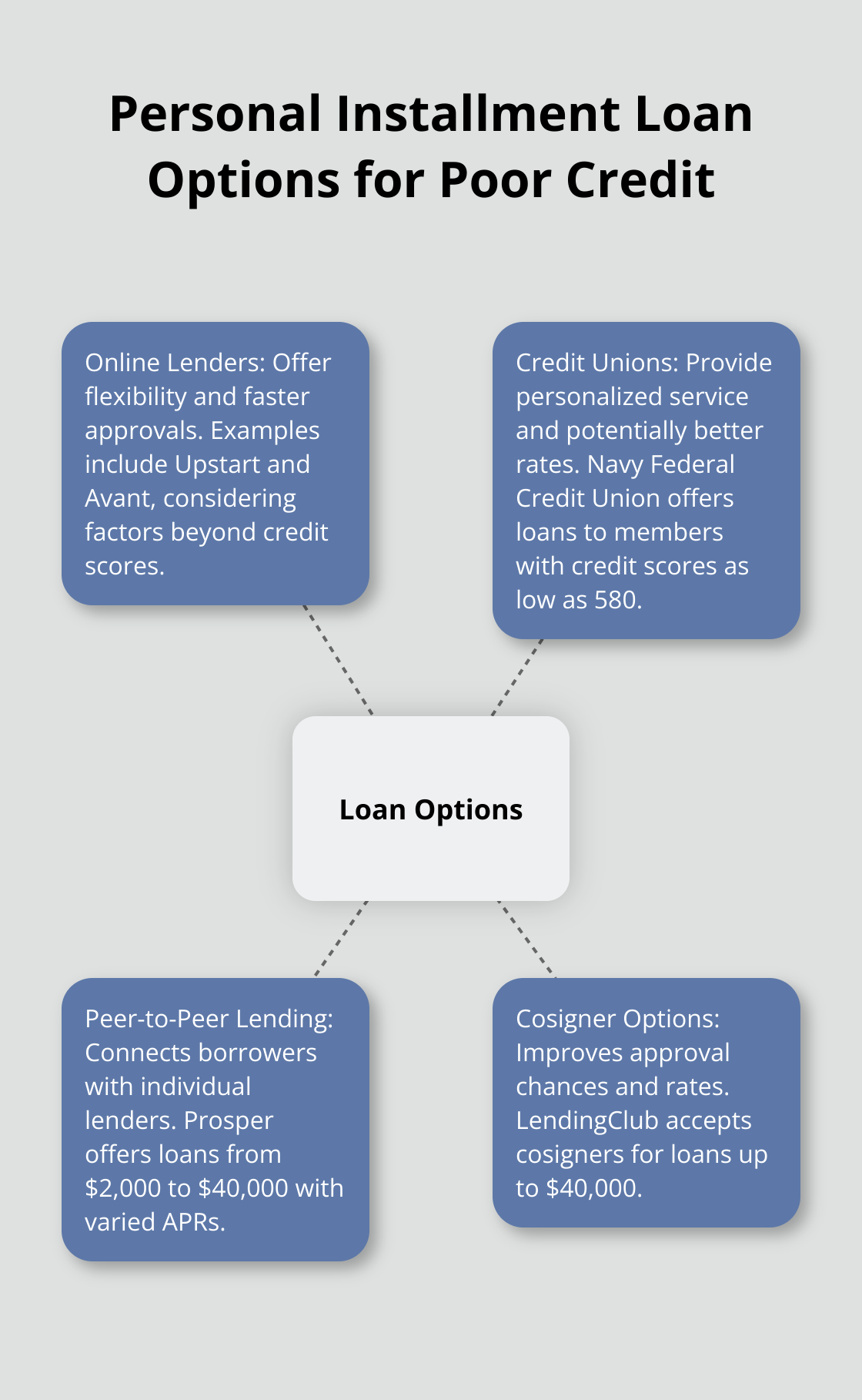

Online Lenders Specializing in Bad Credit Loans

Online lenders offer more flexibility and faster approvals compared to traditional banks for those with poor credit. These lenders often look beyond credit scores when evaluating applications.

Upstart considers factors like education and job history. They offer loans from $1,000 to $50,000 with APRs ranging from 7.8% to 35.99%. Avant caters to borrowers with credit scores as low as 580 and provides loans between $2,000 and $35,000.

You should compare multiple lenders to find the best rates and terms for your situation.

Credit Unions: A Community-Based Approach

Credit unions often provide more personalized service and potentially better rates than large banks, especially for those with poor credit.

Navy Federal Credit Union offers personal loans to members with credit scores as low as 580. Their loan amounts range from $250 to $50,000, with APRs starting at 7.49% for those with excellent credit.

You’ll need to become a member of the credit union to apply for a loan. Membership criteria vary but often include living in a specific area or working for certain employers.

Peer-to-Peer Lending Platforms

Peer-to-peer (P2P) lending platforms connect borrowers directly with individual lenders, potentially offering more flexible terms for those with poor credit.

Prosper offers loans from $2,000 to $40,000 with APRs ranging from 7.95% to 35.99%. They consider applicants with credit scores as low as 640.

P2P lending can be a good option, but interest rates can be high for borrowers with poor credit. You should carefully review the terms before accepting a loan offer.

Exploring Cosigner Options

If you struggle to qualify for a loan on your own, you can ask a friend or family member with good credit to cosign. This can significantly improve your chances of approval and potentially secure better rates.

LendingClub accepts cosigners and offers loans up to $40,000 with APRs ranging from 8.30% to 36.00%.

It’s important to understand the responsibilities involved. Your cosigner becomes equally responsible for repaying the loan. Late payments or defaults will negatively impact both your credit scores.

The Importance of Soft Credit Checks

When exploring these options, you should prioritize lenders who perform soft credit checks for pre-qualification. This allows you to compare offers without impacting your credit score (which is particularly important when you have poor credit).

Many online lenders (such as Upstart and Avant) offer this feature. You can typically see your potential rates and terms within minutes, without any impact on your credit score.

As you consider these various options for personal installment loans with poor credit, it’s essential to understand how to improve your chances of approval. Let’s explore some strategies to enhance your loan application in the next section.

How to Boost Your Loan Approval Odds

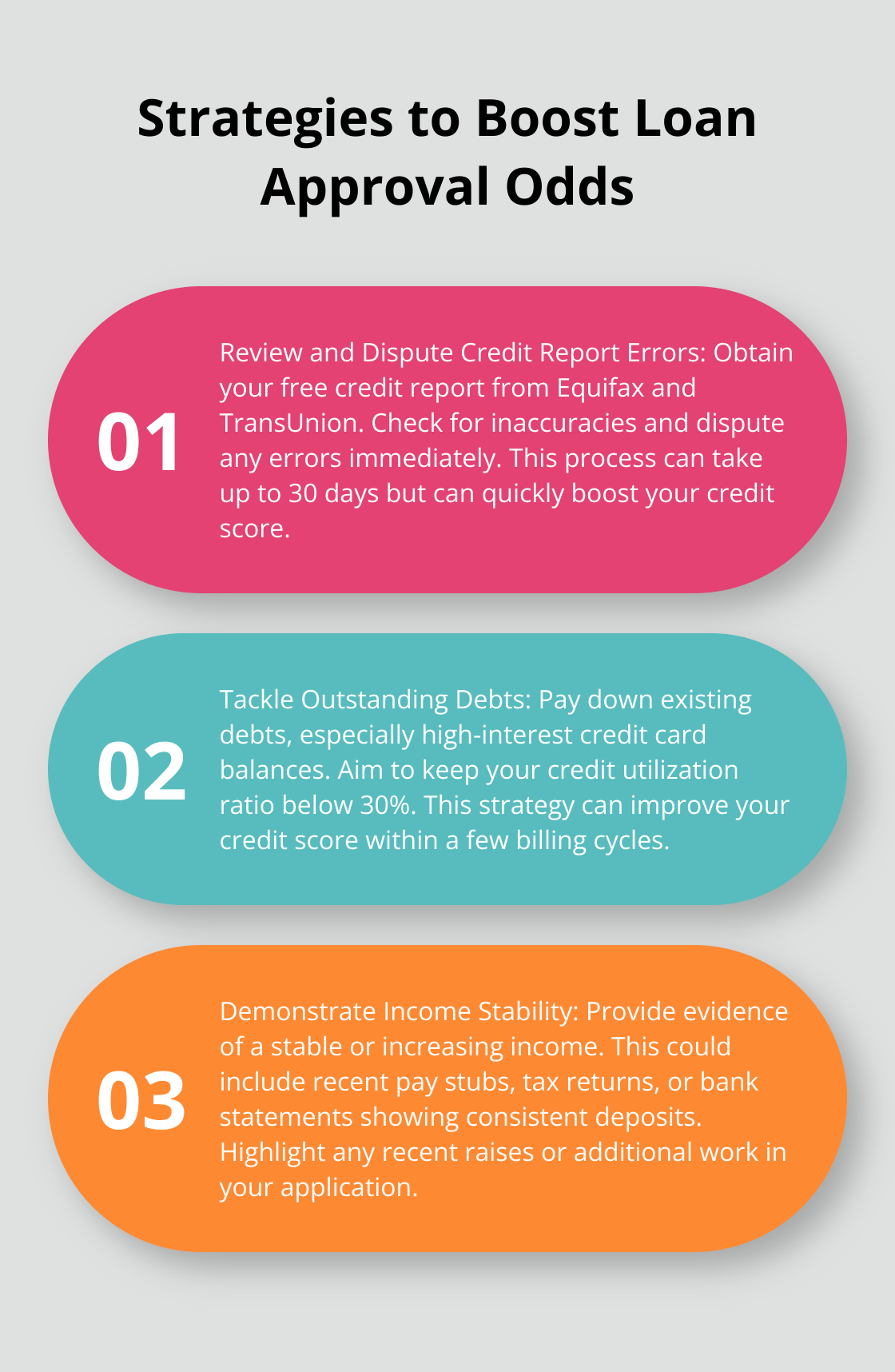

Review and Dispute Credit Report Errors

Start by obtaining your free credit report from Equifax and TransUnion. Check these reports for any inaccuracies. The Federal Trade Commission states that one in five consumers has an error on their credit report. If you find mistakes, dispute them immediately with the credit bureaus. This process can take up to 30 days, but removing errors can quickly boost your credit score.

Tackle Outstanding Debts

Pay down existing debts, especially high-interest credit card balances. The credit utilization ratio (which accounts for 30% of your FICO score) measures how much of your available credit you use. Try to keep this ratio below 30%. For example, if you have a $1,000 credit limit, keep your balance under $300. This strategy can improve your credit score within a few billing cycles.

Consider Secured Loan Options

If you struggle to qualify for an unsecured loan, offer collateral. Secured loans often have lower interest rates and are easier to obtain with poor credit. For instance, you might use your vehicle as collateral for a secured personal loan. (Be aware that you risk losing the asset if you default on the loan.)

Demonstrate Income Stability

Lenders want assurance that you can repay the loan. Steady income is a strong signal to lenders that you have a reliable source of funds coming in regularly, making it more likely that you can meet your loan obligations. Provide evidence of a stable or increasing income. This could include recent pay stubs, tax returns, or bank statements showing consistent deposits. If you’ve recently received a raise or taken on additional work, highlight this information in your application.

Leverage a Co-signer

A co-signer with good credit can significantly improve your chances of approval and help you secure better rates. Experian reports that adding a co-signer with excellent credit could potentially lower your APR by 3-5 percentage points. (Choose someone who understands and accepts the risk of being equally responsible for the loan.)

Final Thoughts

Poor credit personal installment loans provide financial relief for those with less-than-perfect credit scores. These loans offer more manageable repayment terms compared to payday loans, but often come with higher interest rates. You should borrow only what you need and can realistically repay to avoid further financial strain.

Improving your credit score will open doors to better loan terms in the future. You can boost your creditworthiness by making on-time payments, reducing your debt-to-income ratio, and addressing errors on your credit report. Your current credit situation is not permanent, and patience combined with persistence will lead to stronger financial opportunities.

We at Financial Canadian offer comprehensive web design services to help businesses establish a strong online presence. While our focus differs from personal finance, we understand the importance of reliable information when making financial decisions. You can find a solution that meets your immediate needs while setting the stage for a stronger financial future (with the right approach and careful consideration of your options).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment